Sapiens SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

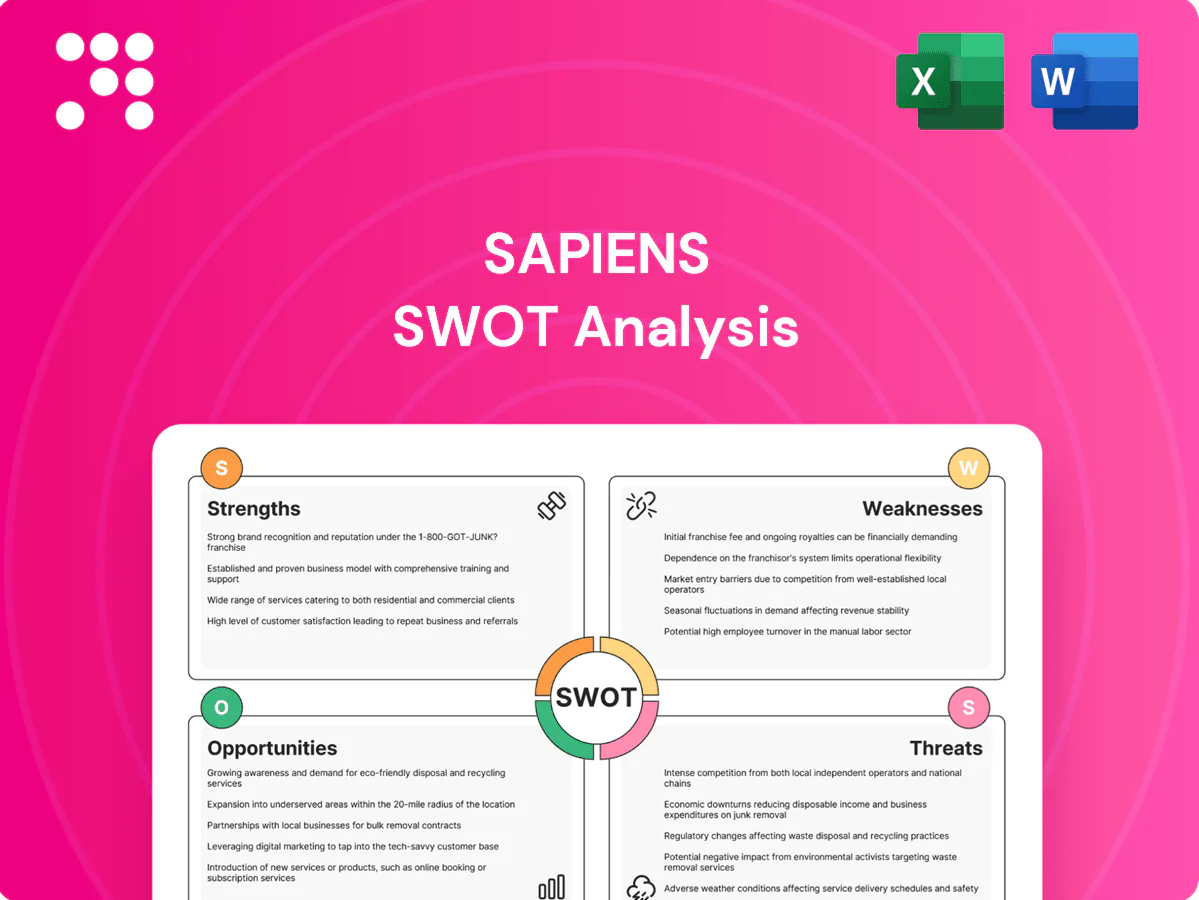

Sapiens SWOT Analysis reveals the insurer’s tech-driven strengths, market expansion opportunities, and exposure to regulatory and integration risks, giving a clear view of competitive positioning. This concise preview highlights key strategic implications for investors and managers. Purchase the full SWOT analysis to access a detailed, editable Word and Excel report with research-backed insights and actionable recommendations.

Strengths

Deep insurance domain focus

Sapiens specializes in P&C, Life, Annuities and reinsurance workflows, offering embedded product and claims logic that accelerates time-to-value for insurers. Founded in 1982 and listed on NASDAQ and TASE, the company leverages 40+ years of insurance IT experience and regulatory know-how. That vertical depth and prebuilt content provide credibility and faster deployments compared with generalist software vendors.

End-to-end product suite

Sapiens delivers an end-to-end suite across policy administration, billing, claims, underwriting, analytics and digital engagement, reducing point-to-point integrations and enabling a consistent UX and shared data model. Its modular architecture supports incremental adoption, and industry studies (McKinsey 2023) show core-platform moves can cut operating costs 20–40% versus multi-vendor stacks.

Proven implementations and references

Proven implementations and references include a large installed base with multiple successful go-lives for tier-1 and tier-2 carriers, demonstrating reduced delivery risk. Repeatable accelerators and prebuilt integration kits shorten timelines and increase predictability. Domain blueprints and embedded best practices consistently improve project outcomes and drive higher win rates in RFPs.

Recurring revenue and services attach

- Subscription + licenses + maintenance + services

- Predictable renewals from multi-year core contracts

- High stickiness enables modernization upsells

Partner ecosystem and integrations

Sapiens leverages alliances with major cloud providers, data vendors and insurtechs to deliver extensive prebuilt connectors for payments, KYC, fraud and data enrichment, enabling faster deployments and richer out‑of‑the‑box functionality. The partner-driven marketplace model accelerates innovation by allowing insurers to compose third‑party modules and commercialize extensions through the Sapiens ecosystem.

- Cloud alliances: prebuilt integrations

- Payments, KYC, fraud connectors

- Faster deployment, richer features

- Marketplace enables partner innovation

Modular insurance cores with 40+ years' expertise, NASDAQ/TASE-listed, cut costs 20–40%

Sapiens leverages 40+ years of insurance IT expertise and NASDAQ/TASE listings to deliver verticalized P&C, Life, Annuities and reinsurance platforms with embedded product and claims logic. Modular end-to-end suite reduces integrations and supports incremental adoption; McKinsey 2023 cites core-platform moves cut operating costs 20–40%. Strong partner ecosystem and multi-year contracts drive predictable recurring revenue and high renewal rates.

| Metric | Value |

|---|---|

| Years in market | 40+ |

| Cost reduction (McKinsey 2023) | 20–40% |

| Listed | NASDAQ & TASE |

| Focus | P&C, Life, Reinsurance |

What is included in the product

Provides a concise SWOT analysis of Sapiens, highlighting internal capabilities, operational gaps, market opportunities, and competitive threats to inform strategic decision-making.

Delivers a compact, visually clear Sapiens SWOT that converts fragmented intelligence into actionable priorities for faster strategic decisions.

Weaknesses

Niche concentration in insurance

Sapiens remains heavily concentrated in insurance, serving over 600 insurer clients worldwide and deriving the bulk of its revenue from that single vertical, unlike broader fintech or enterprise software peers with more diversified mixes. This exposes Sapiens to insurance premium and investment cycles, making revenue volatile through underwriting downturns. Dependence on one sector limits organic growth vectors and may cap TAM unless adjacent verticals or product extensions are pursued.

Complex legacy migrations

Replacing entrenched core systems carries high risk, often taking 12–36 months and commonly running 20–30% over budget with costs ranging from $5M–$50M for mid-to-large insurers. Data conversion, product configuration and change management create major delays and error risk, and McKinsey finds ~70% of transformations underdeliver. Services-heavy projects compress margins and cash flow, while customer hesitation frequently postpones purchase decisions.

Scale versus larger competitors

Sapiens operates with markedly smaller scale than global giants that deploy hundreds of millions to multibillion-dollar R&D and go-to-market budgets, limiting brand reach and perceived parity on large deals. Global sales coverage and partner networks are narrower, reducing geographic penetration and cross-sell leverage. In large RFPs this exposes Sapiens to pricing pressure and margin compression. Prioritizing features across lines of business becomes essential to focus limited investment and win-rate.

Lengthy enterprise sales cycles

Lengthy enterprise sales cycles at Sapiens stem from multi-stakeholder carrier decisions and extensive PoCs, stretching implementations and delaying contract signings. This elongates revenue recognition and increases forecasting variability, with wins often depending on system integrators’ available bandwidth. There is material risk of deal slippage into subsequent fiscal periods.

- Multi-stakeholder approvals

- Extended PoCs

- Delayed revenue recognition

- Forecast volatility

- Dependence on SI capacity

- Slippage risk to next fiscal period

Regional and product mix exposure

Insurance-core vendor risks: 12-36m, 20-30%, ~70%

Sapiens is heavily concentrated in insurance (600+ insurer clients), exposing revenue to underwriting cycles. Replacing cores typically takes 12–36 months and runs 20–30% over budget, with ~70% of transformations underdelivering. Smaller R&D/GTM scale vs global peers limits large-deal competitiveness and prolongs lengthy, multi-stakeholder sales cycles.

| Metric | Value |

|---|---|

| Insurer clients | 600+ |

| Implementation time | 12–36 months |

| Budget overrun | 20–30% |

| Transformation underdeliver | ~70% (McKinsey) |

What You See Is What You Get

Sapiens SWOT Analysis

This is the actual Sapiens SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the structure and findings. Once purchased, you’ll get the complete, editable file immediately. Buy now to unlock the full, detailed analysis.

Go Beyond the Preview—Access the Full Strategic Report

Sapiens SWOT Analysis reveals the insurer’s tech-driven strengths, market expansion opportunities, and exposure to regulatory and integration risks, giving a clear view of competitive positioning. This concise preview highlights key strategic implications for investors and managers. Purchase the full SWOT analysis to access a detailed, editable Word and Excel report with research-backed insights and actionable recommendations.

Strengths

Deep insurance domain focus

Sapiens specializes in P&C, Life, Annuities and reinsurance workflows, offering embedded product and claims logic that accelerates time-to-value for insurers. Founded in 1982 and listed on NASDAQ and TASE, the company leverages 40+ years of insurance IT experience and regulatory know-how. That vertical depth and prebuilt content provide credibility and faster deployments compared with generalist software vendors.

End-to-end product suite

Sapiens delivers an end-to-end suite across policy administration, billing, claims, underwriting, analytics and digital engagement, reducing point-to-point integrations and enabling a consistent UX and shared data model. Its modular architecture supports incremental adoption, and industry studies (McKinsey 2023) show core-platform moves can cut operating costs 20–40% versus multi-vendor stacks.

Proven implementations and references

Proven implementations and references include a large installed base with multiple successful go-lives for tier-1 and tier-2 carriers, demonstrating reduced delivery risk. Repeatable accelerators and prebuilt integration kits shorten timelines and increase predictability. Domain blueprints and embedded best practices consistently improve project outcomes and drive higher win rates in RFPs.

Recurring revenue and services attach

- Subscription + licenses + maintenance + services

- Predictable renewals from multi-year core contracts

- High stickiness enables modernization upsells

Partner ecosystem and integrations

Sapiens leverages alliances with major cloud providers, data vendors and insurtechs to deliver extensive prebuilt connectors for payments, KYC, fraud and data enrichment, enabling faster deployments and richer out‑of‑the‑box functionality. The partner-driven marketplace model accelerates innovation by allowing insurers to compose third‑party modules and commercialize extensions through the Sapiens ecosystem.

- Cloud alliances: prebuilt integrations

- Payments, KYC, fraud connectors

- Faster deployment, richer features

- Marketplace enables partner innovation

Modular insurance cores with 40+ years' expertise, NASDAQ/TASE-listed, cut costs 20–40%

Sapiens leverages 40+ years of insurance IT expertise and NASDAQ/TASE listings to deliver verticalized P&C, Life, Annuities and reinsurance platforms with embedded product and claims logic. Modular end-to-end suite reduces integrations and supports incremental adoption; McKinsey 2023 cites core-platform moves cut operating costs 20–40%. Strong partner ecosystem and multi-year contracts drive predictable recurring revenue and high renewal rates.

| Metric | Value |

|---|---|

| Years in market | 40+ |

| Cost reduction (McKinsey 2023) | 20–40% |

| Listed | NASDAQ & TASE |

| Focus | P&C, Life, Reinsurance |

What is included in the product

Provides a concise SWOT analysis of Sapiens, highlighting internal capabilities, operational gaps, market opportunities, and competitive threats to inform strategic decision-making.

Delivers a compact, visually clear Sapiens SWOT that converts fragmented intelligence into actionable priorities for faster strategic decisions.

Weaknesses

Niche concentration in insurance

Sapiens remains heavily concentrated in insurance, serving over 600 insurer clients worldwide and deriving the bulk of its revenue from that single vertical, unlike broader fintech or enterprise software peers with more diversified mixes. This exposes Sapiens to insurance premium and investment cycles, making revenue volatile through underwriting downturns. Dependence on one sector limits organic growth vectors and may cap TAM unless adjacent verticals or product extensions are pursued.

Complex legacy migrations

Replacing entrenched core systems carries high risk, often taking 12–36 months and commonly running 20–30% over budget with costs ranging from $5M–$50M for mid-to-large insurers. Data conversion, product configuration and change management create major delays and error risk, and McKinsey finds ~70% of transformations underdeliver. Services-heavy projects compress margins and cash flow, while customer hesitation frequently postpones purchase decisions.

Scale versus larger competitors

Sapiens operates with markedly smaller scale than global giants that deploy hundreds of millions to multibillion-dollar R&D and go-to-market budgets, limiting brand reach and perceived parity on large deals. Global sales coverage and partner networks are narrower, reducing geographic penetration and cross-sell leverage. In large RFPs this exposes Sapiens to pricing pressure and margin compression. Prioritizing features across lines of business becomes essential to focus limited investment and win-rate.

Lengthy enterprise sales cycles

Lengthy enterprise sales cycles at Sapiens stem from multi-stakeholder carrier decisions and extensive PoCs, stretching implementations and delaying contract signings. This elongates revenue recognition and increases forecasting variability, with wins often depending on system integrators’ available bandwidth. There is material risk of deal slippage into subsequent fiscal periods.

- Multi-stakeholder approvals

- Extended PoCs

- Delayed revenue recognition

- Forecast volatility

- Dependence on SI capacity

- Slippage risk to next fiscal period

Regional and product mix exposure

Insurance-core vendor risks: 12-36m, 20-30%, ~70%

Sapiens is heavily concentrated in insurance (600+ insurer clients), exposing revenue to underwriting cycles. Replacing cores typically takes 12–36 months and runs 20–30% over budget, with ~70% of transformations underdelivering. Smaller R&D/GTM scale vs global peers limits large-deal competitiveness and prolongs lengthy, multi-stakeholder sales cycles.

| Metric | Value |

|---|---|

| Insurer clients | 600+ |

| Implementation time | 12–36 months |

| Budget overrun | 20–30% |

| Transformation underdeliver | ~70% (McKinsey) |

What You See Is What You Get

Sapiens SWOT Analysis

This is the actual Sapiens SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the structure and findings. Once purchased, you’ll get the complete, editable file immediately. Buy now to unlock the full, detailed analysis.

Description

Go Beyond the Preview—Access the Full Strategic Report

Sapiens SWOT Analysis reveals the insurer’s tech-driven strengths, market expansion opportunities, and exposure to regulatory and integration risks, giving a clear view of competitive positioning. This concise preview highlights key strategic implications for investors and managers. Purchase the full SWOT analysis to access a detailed, editable Word and Excel report with research-backed insights and actionable recommendations.

Strengths

Deep insurance domain focus

Sapiens specializes in P&C, Life, Annuities and reinsurance workflows, offering embedded product and claims logic that accelerates time-to-value for insurers. Founded in 1982 and listed on NASDAQ and TASE, the company leverages 40+ years of insurance IT experience and regulatory know-how. That vertical depth and prebuilt content provide credibility and faster deployments compared with generalist software vendors.

End-to-end product suite

Sapiens delivers an end-to-end suite across policy administration, billing, claims, underwriting, analytics and digital engagement, reducing point-to-point integrations and enabling a consistent UX and shared data model. Its modular architecture supports incremental adoption, and industry studies (McKinsey 2023) show core-platform moves can cut operating costs 20–40% versus multi-vendor stacks.

Proven implementations and references

Proven implementations and references include a large installed base with multiple successful go-lives for tier-1 and tier-2 carriers, demonstrating reduced delivery risk. Repeatable accelerators and prebuilt integration kits shorten timelines and increase predictability. Domain blueprints and embedded best practices consistently improve project outcomes and drive higher win rates in RFPs.

Recurring revenue and services attach

- Subscription + licenses + maintenance + services

- Predictable renewals from multi-year core contracts

- High stickiness enables modernization upsells

Partner ecosystem and integrations

Sapiens leverages alliances with major cloud providers, data vendors and insurtechs to deliver extensive prebuilt connectors for payments, KYC, fraud and data enrichment, enabling faster deployments and richer out‑of‑the‑box functionality. The partner-driven marketplace model accelerates innovation by allowing insurers to compose third‑party modules and commercialize extensions through the Sapiens ecosystem.

- Cloud alliances: prebuilt integrations

- Payments, KYC, fraud connectors

- Faster deployment, richer features

- Marketplace enables partner innovation

Modular insurance cores with 40+ years' expertise, NASDAQ/TASE-listed, cut costs 20–40%

Sapiens leverages 40+ years of insurance IT expertise and NASDAQ/TASE listings to deliver verticalized P&C, Life, Annuities and reinsurance platforms with embedded product and claims logic. Modular end-to-end suite reduces integrations and supports incremental adoption; McKinsey 2023 cites core-platform moves cut operating costs 20–40%. Strong partner ecosystem and multi-year contracts drive predictable recurring revenue and high renewal rates.

| Metric | Value |

|---|---|

| Years in market | 40+ |

| Cost reduction (McKinsey 2023) | 20–40% |

| Listed | NASDAQ & TASE |

| Focus | P&C, Life, Reinsurance |

What is included in the product

Provides a concise SWOT analysis of Sapiens, highlighting internal capabilities, operational gaps, market opportunities, and competitive threats to inform strategic decision-making.

Delivers a compact, visually clear Sapiens SWOT that converts fragmented intelligence into actionable priorities for faster strategic decisions.

Weaknesses

Niche concentration in insurance

Sapiens remains heavily concentrated in insurance, serving over 600 insurer clients worldwide and deriving the bulk of its revenue from that single vertical, unlike broader fintech or enterprise software peers with more diversified mixes. This exposes Sapiens to insurance premium and investment cycles, making revenue volatile through underwriting downturns. Dependence on one sector limits organic growth vectors and may cap TAM unless adjacent verticals or product extensions are pursued.

Complex legacy migrations

Replacing entrenched core systems carries high risk, often taking 12–36 months and commonly running 20–30% over budget with costs ranging from $5M–$50M for mid-to-large insurers. Data conversion, product configuration and change management create major delays and error risk, and McKinsey finds ~70% of transformations underdeliver. Services-heavy projects compress margins and cash flow, while customer hesitation frequently postpones purchase decisions.

Scale versus larger competitors

Sapiens operates with markedly smaller scale than global giants that deploy hundreds of millions to multibillion-dollar R&D and go-to-market budgets, limiting brand reach and perceived parity on large deals. Global sales coverage and partner networks are narrower, reducing geographic penetration and cross-sell leverage. In large RFPs this exposes Sapiens to pricing pressure and margin compression. Prioritizing features across lines of business becomes essential to focus limited investment and win-rate.

Lengthy enterprise sales cycles

Lengthy enterprise sales cycles at Sapiens stem from multi-stakeholder carrier decisions and extensive PoCs, stretching implementations and delaying contract signings. This elongates revenue recognition and increases forecasting variability, with wins often depending on system integrators’ available bandwidth. There is material risk of deal slippage into subsequent fiscal periods.

- Multi-stakeholder approvals

- Extended PoCs

- Delayed revenue recognition

- Forecast volatility

- Dependence on SI capacity

- Slippage risk to next fiscal period

Regional and product mix exposure

Insurance-core vendor risks: 12-36m, 20-30%, ~70%

Sapiens is heavily concentrated in insurance (600+ insurer clients), exposing revenue to underwriting cycles. Replacing cores typically takes 12–36 months and runs 20–30% over budget, with ~70% of transformations underdelivering. Smaller R&D/GTM scale vs global peers limits large-deal competitiveness and prolongs lengthy, multi-stakeholder sales cycles.

| Metric | Value |

|---|---|

| Insurer clients | 600+ |

| Implementation time | 12–36 months |

| Budget overrun | 20–30% |

| Transformation underdeliver | ~70% (McKinsey) |

What You See Is What You Get

Sapiens SWOT Analysis

This is the actual Sapiens SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the structure and findings. Once purchased, you’ll get the complete, editable file immediately. Buy now to unlock the full, detailed analysis.