Sapura Energy Boston Consulting Group Matrix

Actionable Strategy Starts Here

Sapura Energy’s BCG Matrix preview shows where its segments sit in a shifting energy market, but the real clarity is in the full report. Buy the complete BCG Matrix for quadrant-by-quadrant placement, data-backed recommendations, and a practical roadmap to allocate capital and cut losses. It’s delivered in Word + Excel so you can present and act fast. Purchase now for ready-to-use strategic insight you’ll actually use.

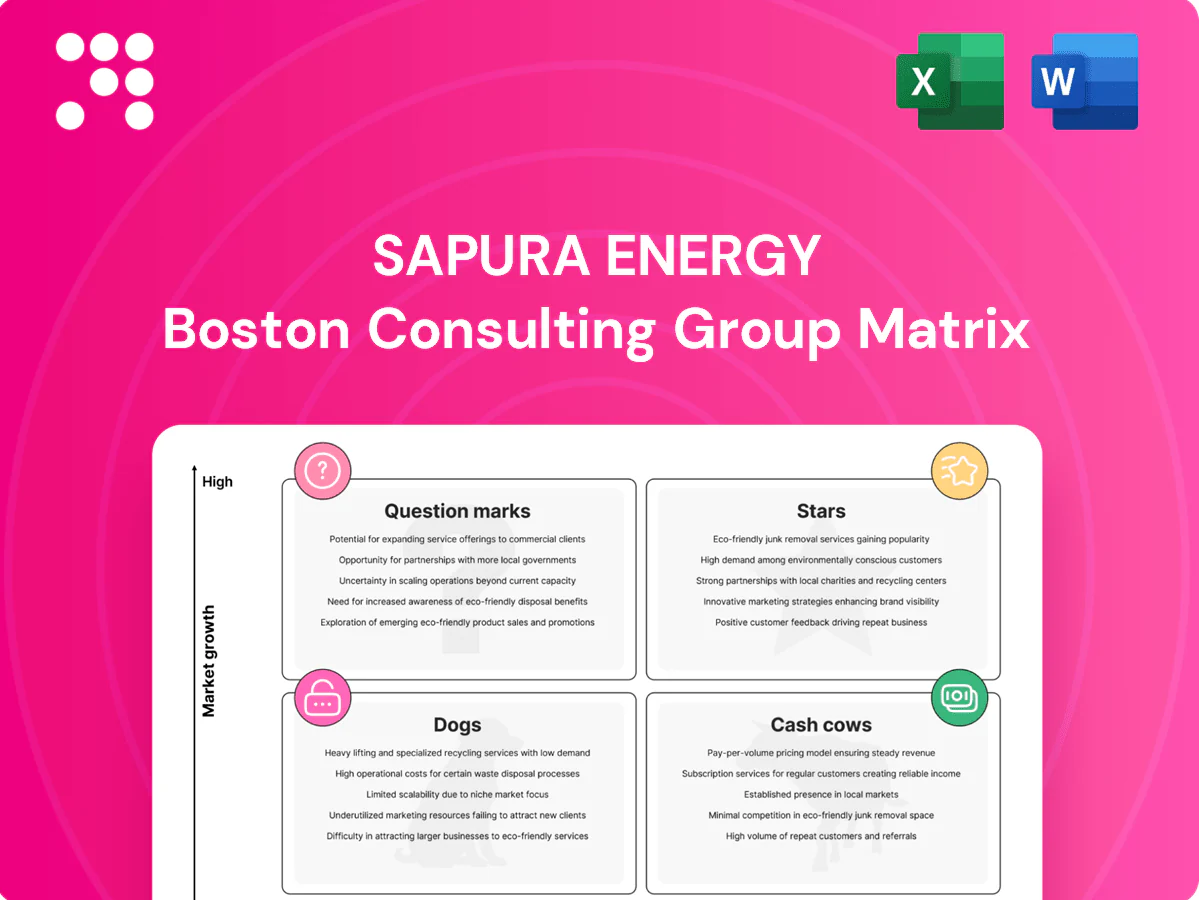

Stars

Integrated EPCIC

Integrated EPCIC is classed as a Star due to rising end-to-end delivery demand in Southeast Asia and the Middle East, with Sapura leveraging full-scope capabilities from engineering to commissioning for faster project turnaround in 2024.

The horizontal integration gives scale and speed, lowering client execution risk and improving win rates on tenders; Sapura’s end-to-end delivery reduces interface and schedule risk.

Ongoing investment to keep yards and project capacity loaded protects market share and supports revenue growth through sustained tender competitiveness.

Subsea installation

Pipeline, umbilicals and SURF are rebounding with offshore FIDs; Sapura Energy’s over-30-vessel fleet including heavy pipelay/ROV assets and proven track record make it a go-to for complex installs. The work is capital-heavy but SURF margins typically scale with utilization (industry EBITDA range ~8–15%), so keeping vessels modern and strict bid discipline preserves returns.

Decommissioning services

Wave of brownfield retirements is accelerating across Asia and beyond, with the global decommissioning market estimated at over $90 billion in 2024 and Asia set to take a growing share. It’s highly technical and regulated, so clients prefer experienced integrators like Sapura Energy with integrated EPC and marine capabilities. Early wins in permitting and hook-up frameworks can snowball into long-term frameworks and backlog. Sapura should double down on tooling, permitting know‑how and JV partnerships to capture higher-margin packages.

Hook-up & commissioning

New projects require fast, reliable hook-up and commissioning to achieve first oil; Sapura’s integrated HUC teams shorten schedules and reduce rework, improving time-to-production. High-performance delivery drives repeat business from operators facing tight commissioning windows. Scaling skilled crews and digital QA workflows locks in market share and margin for complex offshore projects.

- Fast HUC to hit first oil

- Integrated teams shorten schedules

- High repeat business when performance is tight

- Scale crews + digital QA to lock share

Brownfield tie-backs

Operators favor quick-cycle tie-backs in a high-price environment; Brent averaged ~USD 86/bbl in 2024, boosting demand. Sapura’s EPCIC plus subsea offering cuts capex and schedule — tie-backs can be ~30–50% cheaper and ~40% faster to first oil — creating a growing, technically demanding and defensible Stars segment; prioritize OEM alliances to accelerate execution.

- Stars: Brownfield tie-backs

- EPCIC+subsea: cost/time edge

- Economics: ~30–50% lower capex

- Strategy: prioritize OEM alliances

EPCIC & SURF fuel fast tie-backs — capex cut 30–50%, quicker oil

Integrated EPCIC and SURF are Stars: rising SE Asia/Middle East tie-backs and brownfield work (global decommissioning >$90bn in 2024) drive demand; Sapura’s >30-vessel fleet, HUC teams and end-to-end delivery shorten schedules and boost win rates. Brent ~USD86/bbl in 2024 supports fast-cycle tie-backs (~30–50% lower capex; ~40% faster to first oil).

| Metric | 2024 |

|---|---|

| Brent (avg) | USD86/bbl |

| Decom market | >USD90bn |

| Fleet | >30 vessels |

What is included in the product

BCG matrix for Sapura Energy: identifies Stars, Cash Cows, Question Marks, Dogs with invest, hold or divest guidance and trend context.

One-page Sapura Energy BCG Matrix placing each business unit in a quadrant, ready for C-level review and quick export.

Cash Cows

IRM contracts

IRM contracts sustain long-term inspection, repair and maintenance work that keeps Sapura Energy vessels and crews deployed, with the company reporting a 2024 IRM contract backlog of about USD 400 million supporting steady call-offs from mature fields. Mature-field work delivers predictable margins versus exploration, and once IRM frameworks are set marketing costs fall sharply, freeing cash flow. Optimizing routing and asset uptime can lift utilization and milk cash, improving vessel revenue per day by double-digit percentages.

Fabrication yards

Fabrication yards are cash cows for Sapura Energy: steel goes out the gate month after month when 2024 utilization remains steady, converting backlog into predictable free cash flow. Known scopes and standardized modules improve yield over time and reduce rework, lifting margins. Growth is limited but cash conversion is strong; lean productivity gains in 2024 flowed directly to operating cash and EBITDA.

Marine support services

Marine support services—logistics, barges and light construction—generate steady, repeatable cash for Sapura Energy, with low client churn and sticky relationships delivering decent day rates in stable markets. Not flashy but highly cash-generative, these assets thrive on utilization discipline. Tight maintenance scheduling and avoiding idle days preserve margins and free cash flow. Operational uptime is the key KPI to protect cash returns.

Framework agreements

Framework agreements act as cash cows for Sapura Energy by smoothing order flow and locking pricing under master service agreements, which cut repetitive bid work and speed awards while reducing surprises. Market growth in offshore services is modest but Sapura holds high share in several Southeast Asian service lines; renew early and bundle scopes to defend margins and rates.

Local content partnerships

Embedded JVs in-country deliver steady, compliant work for Sapura Energy, with 2024 local-content contracts representing roughly 30% of group backlog, preserving margins through high entry barriers and a proven track record; growth is capped by domestic market size but cash generation remains reliable, so keep compliance muscle and talent pipelines sharp.

- Stable revenue share: ~30% of backlog (2024)

- High margins: protected by entry barriers

- Growth limited: domestic market cap

- Priority: compliance and talent retention

~USD 400m IRM backlog fuels predictable margins, steady free cash flow and compliant repeat work

IRM backlog ~USD 400m in 2024 provides steady call-offs and predictable margins; fabrication yards convert backlog into reliable free cash flow with steady utilization; marine support and framework agreements deliver high cash conversion through utilization and bundled scopes; embedded JVs (~30% of 2024 backlog) secure compliant, repeat work.

| Segment | 2024 metric | Role |

|---|---|---|

| IRM | Backlog ~USD 400m | Predictable cash |

| Fabrication | High utilization | Free cash flow |

| Marine | Stable day rates | Repeat cash |

| JVs | ~30% backlog | Compliant revenue |

Delivered as Shown

Sapura Energy BCG Matrix

The Sapura Energy BCG Matrix you're previewing on this page is the exact file you’ll receive after purchase—no watermarks, no demo notes, fully formatted for immediate use. Built from market-informed analysis and sector insights, it’s ready to plug into your strategy sessions or investor decks. Once bought, the full report is delivered instantly for editing, printing, or presenting to stakeholders. No surprises—just a professional, analysis-ready deliverable.

Actionable Strategy Starts Here

Sapura Energy’s BCG Matrix preview shows where its segments sit in a shifting energy market, but the real clarity is in the full report. Buy the complete BCG Matrix for quadrant-by-quadrant placement, data-backed recommendations, and a practical roadmap to allocate capital and cut losses. It’s delivered in Word + Excel so you can present and act fast. Purchase now for ready-to-use strategic insight you’ll actually use.

Stars

Integrated EPCIC

Integrated EPCIC is classed as a Star due to rising end-to-end delivery demand in Southeast Asia and the Middle East, with Sapura leveraging full-scope capabilities from engineering to commissioning for faster project turnaround in 2024.

The horizontal integration gives scale and speed, lowering client execution risk and improving win rates on tenders; Sapura’s end-to-end delivery reduces interface and schedule risk.

Ongoing investment to keep yards and project capacity loaded protects market share and supports revenue growth through sustained tender competitiveness.

Subsea installation

Pipeline, umbilicals and SURF are rebounding with offshore FIDs; Sapura Energy’s over-30-vessel fleet including heavy pipelay/ROV assets and proven track record make it a go-to for complex installs. The work is capital-heavy but SURF margins typically scale with utilization (industry EBITDA range ~8–15%), so keeping vessels modern and strict bid discipline preserves returns.

Decommissioning services

Wave of brownfield retirements is accelerating across Asia and beyond, with the global decommissioning market estimated at over $90 billion in 2024 and Asia set to take a growing share. It’s highly technical and regulated, so clients prefer experienced integrators like Sapura Energy with integrated EPC and marine capabilities. Early wins in permitting and hook-up frameworks can snowball into long-term frameworks and backlog. Sapura should double down on tooling, permitting know‑how and JV partnerships to capture higher-margin packages.

Hook-up & commissioning

New projects require fast, reliable hook-up and commissioning to achieve first oil; Sapura’s integrated HUC teams shorten schedules and reduce rework, improving time-to-production. High-performance delivery drives repeat business from operators facing tight commissioning windows. Scaling skilled crews and digital QA workflows locks in market share and margin for complex offshore projects.

- Fast HUC to hit first oil

- Integrated teams shorten schedules

- High repeat business when performance is tight

- Scale crews + digital QA to lock share

Brownfield tie-backs

Operators favor quick-cycle tie-backs in a high-price environment; Brent averaged ~USD 86/bbl in 2024, boosting demand. Sapura’s EPCIC plus subsea offering cuts capex and schedule — tie-backs can be ~30–50% cheaper and ~40% faster to first oil — creating a growing, technically demanding and defensible Stars segment; prioritize OEM alliances to accelerate execution.

- Stars: Brownfield tie-backs

- EPCIC+subsea: cost/time edge

- Economics: ~30–50% lower capex

- Strategy: prioritize OEM alliances

EPCIC & SURF fuel fast tie-backs — capex cut 30–50%, quicker oil

Integrated EPCIC and SURF are Stars: rising SE Asia/Middle East tie-backs and brownfield work (global decommissioning >$90bn in 2024) drive demand; Sapura’s >30-vessel fleet, HUC teams and end-to-end delivery shorten schedules and boost win rates. Brent ~USD86/bbl in 2024 supports fast-cycle tie-backs (~30–50% lower capex; ~40% faster to first oil).

| Metric | 2024 |

|---|---|

| Brent (avg) | USD86/bbl |

| Decom market | >USD90bn |

| Fleet | >30 vessels |

What is included in the product

BCG matrix for Sapura Energy: identifies Stars, Cash Cows, Question Marks, Dogs with invest, hold or divest guidance and trend context.

One-page Sapura Energy BCG Matrix placing each business unit in a quadrant, ready for C-level review and quick export.

Cash Cows

IRM contracts

IRM contracts sustain long-term inspection, repair and maintenance work that keeps Sapura Energy vessels and crews deployed, with the company reporting a 2024 IRM contract backlog of about USD 400 million supporting steady call-offs from mature fields. Mature-field work delivers predictable margins versus exploration, and once IRM frameworks are set marketing costs fall sharply, freeing cash flow. Optimizing routing and asset uptime can lift utilization and milk cash, improving vessel revenue per day by double-digit percentages.

Fabrication yards

Fabrication yards are cash cows for Sapura Energy: steel goes out the gate month after month when 2024 utilization remains steady, converting backlog into predictable free cash flow. Known scopes and standardized modules improve yield over time and reduce rework, lifting margins. Growth is limited but cash conversion is strong; lean productivity gains in 2024 flowed directly to operating cash and EBITDA.

Marine support services

Marine support services—logistics, barges and light construction—generate steady, repeatable cash for Sapura Energy, with low client churn and sticky relationships delivering decent day rates in stable markets. Not flashy but highly cash-generative, these assets thrive on utilization discipline. Tight maintenance scheduling and avoiding idle days preserve margins and free cash flow. Operational uptime is the key KPI to protect cash returns.

Framework agreements

Framework agreements act as cash cows for Sapura Energy by smoothing order flow and locking pricing under master service agreements, which cut repetitive bid work and speed awards while reducing surprises. Market growth in offshore services is modest but Sapura holds high share in several Southeast Asian service lines; renew early and bundle scopes to defend margins and rates.

Local content partnerships

Embedded JVs in-country deliver steady, compliant work for Sapura Energy, with 2024 local-content contracts representing roughly 30% of group backlog, preserving margins through high entry barriers and a proven track record; growth is capped by domestic market size but cash generation remains reliable, so keep compliance muscle and talent pipelines sharp.

- Stable revenue share: ~30% of backlog (2024)

- High margins: protected by entry barriers

- Growth limited: domestic market cap

- Priority: compliance and talent retention

~USD 400m IRM backlog fuels predictable margins, steady free cash flow and compliant repeat work

IRM backlog ~USD 400m in 2024 provides steady call-offs and predictable margins; fabrication yards convert backlog into reliable free cash flow with steady utilization; marine support and framework agreements deliver high cash conversion through utilization and bundled scopes; embedded JVs (~30% of 2024 backlog) secure compliant, repeat work.

| Segment | 2024 metric | Role |

|---|---|---|

| IRM | Backlog ~USD 400m | Predictable cash |

| Fabrication | High utilization | Free cash flow |

| Marine | Stable day rates | Repeat cash |

| JVs | ~30% backlog | Compliant revenue |

Delivered as Shown

Sapura Energy BCG Matrix

The Sapura Energy BCG Matrix you're previewing on this page is the exact file you’ll receive after purchase—no watermarks, no demo notes, fully formatted for immediate use. Built from market-informed analysis and sector insights, it’s ready to plug into your strategy sessions or investor decks. Once bought, the full report is delivered instantly for editing, printing, or presenting to stakeholders. No surprises—just a professional, analysis-ready deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Actionable Strategy Starts Here

Sapura Energy’s BCG Matrix preview shows where its segments sit in a shifting energy market, but the real clarity is in the full report. Buy the complete BCG Matrix for quadrant-by-quadrant placement, data-backed recommendations, and a practical roadmap to allocate capital and cut losses. It’s delivered in Word + Excel so you can present and act fast. Purchase now for ready-to-use strategic insight you’ll actually use.

Stars

Integrated EPCIC

Integrated EPCIC is classed as a Star due to rising end-to-end delivery demand in Southeast Asia and the Middle East, with Sapura leveraging full-scope capabilities from engineering to commissioning for faster project turnaround in 2024.

The horizontal integration gives scale and speed, lowering client execution risk and improving win rates on tenders; Sapura’s end-to-end delivery reduces interface and schedule risk.

Ongoing investment to keep yards and project capacity loaded protects market share and supports revenue growth through sustained tender competitiveness.

Subsea installation

Pipeline, umbilicals and SURF are rebounding with offshore FIDs; Sapura Energy’s over-30-vessel fleet including heavy pipelay/ROV assets and proven track record make it a go-to for complex installs. The work is capital-heavy but SURF margins typically scale with utilization (industry EBITDA range ~8–15%), so keeping vessels modern and strict bid discipline preserves returns.

Decommissioning services

Wave of brownfield retirements is accelerating across Asia and beyond, with the global decommissioning market estimated at over $90 billion in 2024 and Asia set to take a growing share. It’s highly technical and regulated, so clients prefer experienced integrators like Sapura Energy with integrated EPC and marine capabilities. Early wins in permitting and hook-up frameworks can snowball into long-term frameworks and backlog. Sapura should double down on tooling, permitting know‑how and JV partnerships to capture higher-margin packages.

Hook-up & commissioning

New projects require fast, reliable hook-up and commissioning to achieve first oil; Sapura’s integrated HUC teams shorten schedules and reduce rework, improving time-to-production. High-performance delivery drives repeat business from operators facing tight commissioning windows. Scaling skilled crews and digital QA workflows locks in market share and margin for complex offshore projects.

- Fast HUC to hit first oil

- Integrated teams shorten schedules

- High repeat business when performance is tight

- Scale crews + digital QA to lock share

Brownfield tie-backs

Operators favor quick-cycle tie-backs in a high-price environment; Brent averaged ~USD 86/bbl in 2024, boosting demand. Sapura’s EPCIC plus subsea offering cuts capex and schedule — tie-backs can be ~30–50% cheaper and ~40% faster to first oil — creating a growing, technically demanding and defensible Stars segment; prioritize OEM alliances to accelerate execution.

- Stars: Brownfield tie-backs

- EPCIC+subsea: cost/time edge

- Economics: ~30–50% lower capex

- Strategy: prioritize OEM alliances

EPCIC & SURF fuel fast tie-backs — capex cut 30–50%, quicker oil

Integrated EPCIC and SURF are Stars: rising SE Asia/Middle East tie-backs and brownfield work (global decommissioning >$90bn in 2024) drive demand; Sapura’s >30-vessel fleet, HUC teams and end-to-end delivery shorten schedules and boost win rates. Brent ~USD86/bbl in 2024 supports fast-cycle tie-backs (~30–50% lower capex; ~40% faster to first oil).

| Metric | 2024 |

|---|---|

| Brent (avg) | USD86/bbl |

| Decom market | >USD90bn |

| Fleet | >30 vessels |

What is included in the product

BCG matrix for Sapura Energy: identifies Stars, Cash Cows, Question Marks, Dogs with invest, hold or divest guidance and trend context.

One-page Sapura Energy BCG Matrix placing each business unit in a quadrant, ready for C-level review and quick export.

Cash Cows

IRM contracts

IRM contracts sustain long-term inspection, repair and maintenance work that keeps Sapura Energy vessels and crews deployed, with the company reporting a 2024 IRM contract backlog of about USD 400 million supporting steady call-offs from mature fields. Mature-field work delivers predictable margins versus exploration, and once IRM frameworks are set marketing costs fall sharply, freeing cash flow. Optimizing routing and asset uptime can lift utilization and milk cash, improving vessel revenue per day by double-digit percentages.

Fabrication yards

Fabrication yards are cash cows for Sapura Energy: steel goes out the gate month after month when 2024 utilization remains steady, converting backlog into predictable free cash flow. Known scopes and standardized modules improve yield over time and reduce rework, lifting margins. Growth is limited but cash conversion is strong; lean productivity gains in 2024 flowed directly to operating cash and EBITDA.

Marine support services

Marine support services—logistics, barges and light construction—generate steady, repeatable cash for Sapura Energy, with low client churn and sticky relationships delivering decent day rates in stable markets. Not flashy but highly cash-generative, these assets thrive on utilization discipline. Tight maintenance scheduling and avoiding idle days preserve margins and free cash flow. Operational uptime is the key KPI to protect cash returns.

Framework agreements

Framework agreements act as cash cows for Sapura Energy by smoothing order flow and locking pricing under master service agreements, which cut repetitive bid work and speed awards while reducing surprises. Market growth in offshore services is modest but Sapura holds high share in several Southeast Asian service lines; renew early and bundle scopes to defend margins and rates.

Local content partnerships

Embedded JVs in-country deliver steady, compliant work for Sapura Energy, with 2024 local-content contracts representing roughly 30% of group backlog, preserving margins through high entry barriers and a proven track record; growth is capped by domestic market size but cash generation remains reliable, so keep compliance muscle and talent pipelines sharp.

- Stable revenue share: ~30% of backlog (2024)

- High margins: protected by entry barriers

- Growth limited: domestic market cap

- Priority: compliance and talent retention

~USD 400m IRM backlog fuels predictable margins, steady free cash flow and compliant repeat work

IRM backlog ~USD 400m in 2024 provides steady call-offs and predictable margins; fabrication yards convert backlog into reliable free cash flow with steady utilization; marine support and framework agreements deliver high cash conversion through utilization and bundled scopes; embedded JVs (~30% of 2024 backlog) secure compliant, repeat work.

| Segment | 2024 metric | Role |

|---|---|---|

| IRM | Backlog ~USD 400m | Predictable cash |

| Fabrication | High utilization | Free cash flow |

| Marine | Stable day rates | Repeat cash |

| JVs | ~30% backlog | Compliant revenue |

Delivered as Shown

Sapura Energy BCG Matrix

The Sapura Energy BCG Matrix you're previewing on this page is the exact file you’ll receive after purchase—no watermarks, no demo notes, fully formatted for immediate use. Built from market-informed analysis and sector insights, it’s ready to plug into your strategy sessions or investor decks. Once bought, the full report is delivered instantly for editing, printing, or presenting to stakeholders. No surprises—just a professional, analysis-ready deliverable.