SATS Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

SATS faces intense competitive dynamics across airport services, catering margins, and logistics scale advantages that shape pricing power and growth prospects. Supplier concentration and capital intensity limit flexibility, while regulatory barriers curb but don’t eliminate new entrants. This snapshot highlights key tensions but omits force-by-force ratings and visuals. Unlock the full Porter’s Five Forces Analysis for a detailed, actionable strategic breakdown tailored to SATS.

Suppliers Bargaining Power

Prime-site landlords

Urban high-traffic locations in Nordic capitals are scarce, giving landlords strong leverage on rent and lease terms. Long leases and costly fit-out obligations raise switching costs for SATS. A soft retail market in 2024 eased rent inflation and enabled renegotiations. Operating across four Nordic countries and listed on Oslo Børs (ticker SATS) helps diversify landlord exposure.

Gym equipment OEMs

Leading OEMs such as Technogym (2023 revenue €669.7m) and Life Fitness exert moderate supplier power via differentiated products and service networks, but SATS can multi-source and stagger refresh cycles to negotiate better terms. Large order volumes and long relationships secure discounts and SLAs, while supply-chain constraints or software-console lock-ins (noted across the ~USD10bn commercial equipment market in 2024) can swing power back to OEMs.

Group content and licensing

Licensors like Les Mills, whose formats are used in over 21,000 clubs across 100+ countries, command licensing fees for popular group formats, giving suppliers leverage. Strong content differentiation sustains member engagement and limits SATS’ ability to substitute quickly, though SATS can mitigate dependency by developing proprietary classes. Digital rights and music licensing (managed via PROs such as STIM/ASCAP/PRS) add recurring cost complexity.

Utilities and energy

Energy-intensive HVAC and lighting make SATS sensitive to utility price swings; Nord Pool volatility — with day-ahead spikes historically above €200–300/MWh and 2024 average Nordic baseload ≈€40–60/MWh — can raise supplier power. Hedging and capex in efficiency reduce exposure; scale procurement and ESG-linked demand response can secure lower tariffs.

- exposure: high energy intensity

- risk: Nordic price spikes

- mitigation: hedging + efficiency

- opportunity: scale & ESG tariffs

Tech platforms and payments

Nordic landlords wield leverage; 2024 soft rents spur renegotiations, energy risk rises

Landlord leverage high in Nordic urban sites; 2024 softer retail rents enabled renegotiations. OEMs (Technogym rev €669.7m 2023) and Les Mills (21,000 clubs) hold moderate licensing/equipment power; SATS (FY2024 rev ≈SGD 1.9bn) mitigates via scale, multi-sourcing and in-house tech. Energy exposure (Nord Pool 2024 baseload ≈€40–60/MWh) raises supplier risk; hedging and efficiency cut vulnerability.

| Factor | 2024 datapoint |

|---|---|

| Revenue | ≈SGD 1.9bn |

| Technogym 2023 | €669.7m |

| Nord Pool avg | €40–60/MWh |

What is included in the product

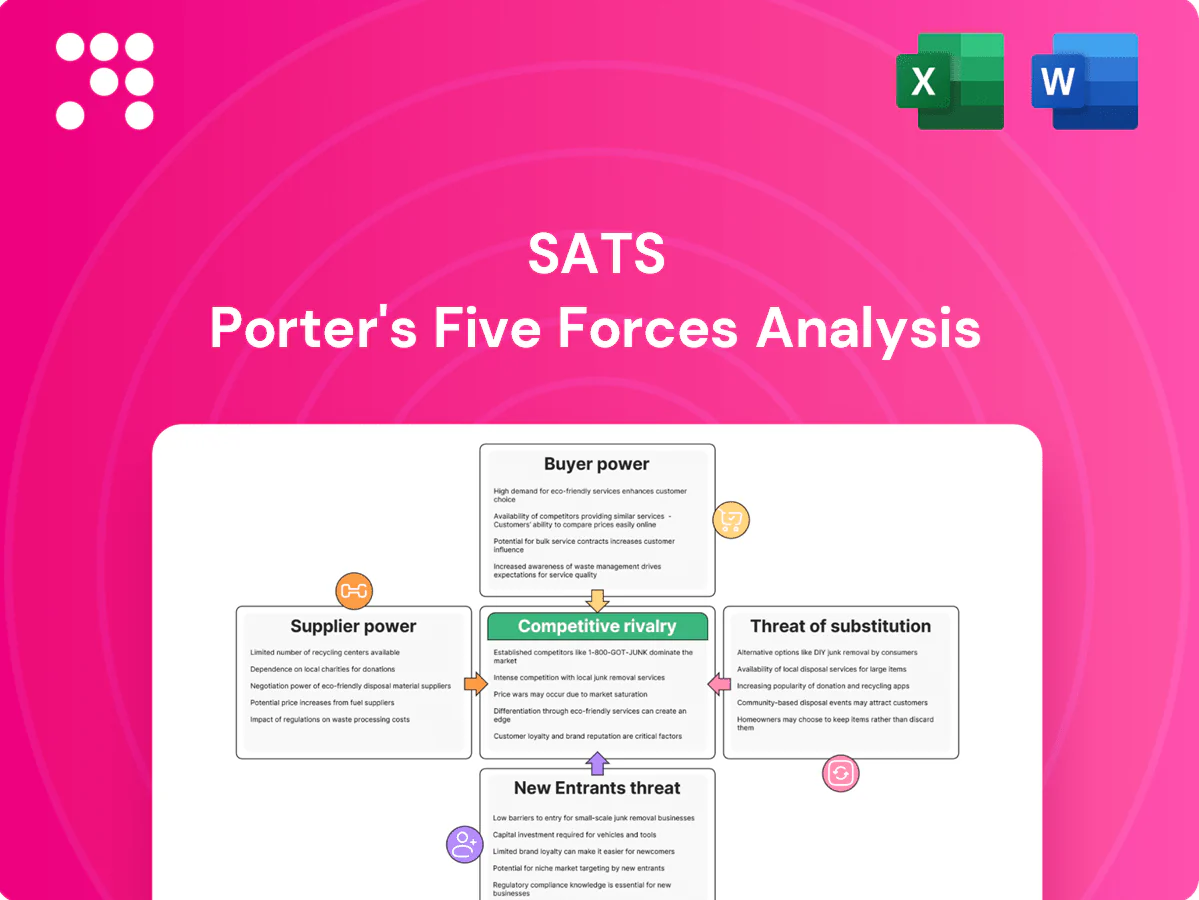

Comprehensive Porter’s Five Forces analysis tailored to SATS that uncovers competition drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, with strategic commentary and editable insights for investor decks, business plans, or internal strategy use.

A clear, one-sheet Porter's Five Forces for SATS that instantly visualizes strategic pressure with a customizable spider chart and scenario tabs for pre/post regulation or new entrants. Clean, copy-ready layout requires no macros, integrates into Excel/Word, and lets non-finance users swap in their own data for fast, boardroom-ready decisions.

Customers Bargaining Power

Low switching costs

Low switching costs let members cancel or move gyms easily, intensifying buyer power; SATS faces this despite operating >370 clubs and about 1.0 million members in 2024. Proximity and convenience often trump brand loyalty for many users, while flexible memberships and frequent promotions raise churn risk. SATS counters with network breadth and bundled services to retain members.

Price sensitivity

Budget chains set reference prices, squeezing SATS premium tiers and forcing competitive alignment; in 2024 consumers increasingly traded down or paused memberships amid macroeconomic tightness. Clear value communication on classes, PT and facilities proved decisive for retention. Tiered pricing and corporate discounts effectively segment willingness to pay.

Digital alternatives

Digital alternatives — apps and connected fitness, with over 300 SATS clubs in 2024 and rapid growth in on-demand consumption post-pandemic — let consumers substitute at marginal cost, raising expectations for hybrid, flexible experiences; buyers leverage this to demand extras and flexibility, while SATS’ omnichannel offerings can recapture value by bundling studio access with digital content and memberships.

Corporate and B2B buyers

Corporate and B2B buyers aggregate demand through wellness contracts that secure volume discounts and can dictate product features and reporting needs. These accounts span SATS' four Nordic markets, so losing a large client can materially reduce club utilization and revenues. SATS defends with proprietary outcomes data and multi‑market coverage to retain pricing and spread risk.

- Volume leverage: corporate contracts negotiate discounts

- Product influence: shape features and reporting

- Concentration risk: losing large account lowers utilization

- Defensive assets: outcomes data and multi‑market reach

Service quality transparency

Reviews, social media, and comparison sites have raised information symmetry for SATS customers, making cleanliness, crowding, and staff quality highly visible and directly affecting buyer leverage; a 2024 CX industry survey found 64% of travelers say a single poor service experience prompts cancellation. Real-time capacity feeds and NPS-driven recovery programs cut churn and strengthen supplier position when implemented effectively.

- reviews: visibility of cleanliness/staff

- real-time data: reduces churn

- NPS: recovery lowers cancellations

Buyers hold leverage; retention is critical for >370 clubs, ~1.0M members; 64% cancel after one bad CX

Low switching costs and digital substitutes give buyers strong leverage; SATS had >370 clubs and about 1.0 million members in 2024, driving focus on retention via bundles and omnichannel. Corporate buyers across four Nordic markets aggregate demand and can extract discounts; visible reviews and a 2024 CX survey (64% cancel after one bad experience) increase buyer influence.

| Metric | 2024 |

|---|---|

| Clubs | >370 |

| Members | ~1.0M |

| Markets | 4 Nordic |

| CX cancel rate | 64% (2024 survey) |

Full Version Awaits

SATS Porter's Five Forces Analysis

This preview shows the exact SATS Porter's Five Forces analysis you'll receive—no placeholders or samples. The full, professionally formatted document is identical and ready for immediate download after purchase. It includes thorough, actionable insights for strategic decisions.

A Must-Have Tool for Decision-Makers

SATS faces intense competitive dynamics across airport services, catering margins, and logistics scale advantages that shape pricing power and growth prospects. Supplier concentration and capital intensity limit flexibility, while regulatory barriers curb but don’t eliminate new entrants. This snapshot highlights key tensions but omits force-by-force ratings and visuals. Unlock the full Porter’s Five Forces Analysis for a detailed, actionable strategic breakdown tailored to SATS.

Suppliers Bargaining Power

Prime-site landlords

Urban high-traffic locations in Nordic capitals are scarce, giving landlords strong leverage on rent and lease terms. Long leases and costly fit-out obligations raise switching costs for SATS. A soft retail market in 2024 eased rent inflation and enabled renegotiations. Operating across four Nordic countries and listed on Oslo Børs (ticker SATS) helps diversify landlord exposure.

Gym equipment OEMs

Leading OEMs such as Technogym (2023 revenue €669.7m) and Life Fitness exert moderate supplier power via differentiated products and service networks, but SATS can multi-source and stagger refresh cycles to negotiate better terms. Large order volumes and long relationships secure discounts and SLAs, while supply-chain constraints or software-console lock-ins (noted across the ~USD10bn commercial equipment market in 2024) can swing power back to OEMs.

Group content and licensing

Licensors like Les Mills, whose formats are used in over 21,000 clubs across 100+ countries, command licensing fees for popular group formats, giving suppliers leverage. Strong content differentiation sustains member engagement and limits SATS’ ability to substitute quickly, though SATS can mitigate dependency by developing proprietary classes. Digital rights and music licensing (managed via PROs such as STIM/ASCAP/PRS) add recurring cost complexity.

Utilities and energy

Energy-intensive HVAC and lighting make SATS sensitive to utility price swings; Nord Pool volatility — with day-ahead spikes historically above €200–300/MWh and 2024 average Nordic baseload ≈€40–60/MWh — can raise supplier power. Hedging and capex in efficiency reduce exposure; scale procurement and ESG-linked demand response can secure lower tariffs.

- exposure: high energy intensity

- risk: Nordic price spikes

- mitigation: hedging + efficiency

- opportunity: scale & ESG tariffs

Tech platforms and payments

Nordic landlords wield leverage; 2024 soft rents spur renegotiations, energy risk rises

Landlord leverage high in Nordic urban sites; 2024 softer retail rents enabled renegotiations. OEMs (Technogym rev €669.7m 2023) and Les Mills (21,000 clubs) hold moderate licensing/equipment power; SATS (FY2024 rev ≈SGD 1.9bn) mitigates via scale, multi-sourcing and in-house tech. Energy exposure (Nord Pool 2024 baseload ≈€40–60/MWh) raises supplier risk; hedging and efficiency cut vulnerability.

| Factor | 2024 datapoint |

|---|---|

| Revenue | ≈SGD 1.9bn |

| Technogym 2023 | €669.7m |

| Nord Pool avg | €40–60/MWh |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored to SATS that uncovers competition drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, with strategic commentary and editable insights for investor decks, business plans, or internal strategy use.

A clear, one-sheet Porter's Five Forces for SATS that instantly visualizes strategic pressure with a customizable spider chart and scenario tabs for pre/post regulation or new entrants. Clean, copy-ready layout requires no macros, integrates into Excel/Word, and lets non-finance users swap in their own data for fast, boardroom-ready decisions.

Customers Bargaining Power

Low switching costs

Low switching costs let members cancel or move gyms easily, intensifying buyer power; SATS faces this despite operating >370 clubs and about 1.0 million members in 2024. Proximity and convenience often trump brand loyalty for many users, while flexible memberships and frequent promotions raise churn risk. SATS counters with network breadth and bundled services to retain members.

Price sensitivity

Budget chains set reference prices, squeezing SATS premium tiers and forcing competitive alignment; in 2024 consumers increasingly traded down or paused memberships amid macroeconomic tightness. Clear value communication on classes, PT and facilities proved decisive for retention. Tiered pricing and corporate discounts effectively segment willingness to pay.

Digital alternatives

Digital alternatives — apps and connected fitness, with over 300 SATS clubs in 2024 and rapid growth in on-demand consumption post-pandemic — let consumers substitute at marginal cost, raising expectations for hybrid, flexible experiences; buyers leverage this to demand extras and flexibility, while SATS’ omnichannel offerings can recapture value by bundling studio access with digital content and memberships.

Corporate and B2B buyers

Corporate and B2B buyers aggregate demand through wellness contracts that secure volume discounts and can dictate product features and reporting needs. These accounts span SATS' four Nordic markets, so losing a large client can materially reduce club utilization and revenues. SATS defends with proprietary outcomes data and multi‑market coverage to retain pricing and spread risk.

- Volume leverage: corporate contracts negotiate discounts

- Product influence: shape features and reporting

- Concentration risk: losing large account lowers utilization

- Defensive assets: outcomes data and multi‑market reach

Service quality transparency

Reviews, social media, and comparison sites have raised information symmetry for SATS customers, making cleanliness, crowding, and staff quality highly visible and directly affecting buyer leverage; a 2024 CX industry survey found 64% of travelers say a single poor service experience prompts cancellation. Real-time capacity feeds and NPS-driven recovery programs cut churn and strengthen supplier position when implemented effectively.

- reviews: visibility of cleanliness/staff

- real-time data: reduces churn

- NPS: recovery lowers cancellations

Buyers hold leverage; retention is critical for >370 clubs, ~1.0M members; 64% cancel after one bad CX

Low switching costs and digital substitutes give buyers strong leverage; SATS had >370 clubs and about 1.0 million members in 2024, driving focus on retention via bundles and omnichannel. Corporate buyers across four Nordic markets aggregate demand and can extract discounts; visible reviews and a 2024 CX survey (64% cancel after one bad experience) increase buyer influence.

| Metric | 2024 |

|---|---|

| Clubs | >370 |

| Members | ~1.0M |

| Markets | 4 Nordic |

| CX cancel rate | 64% (2024 survey) |

Full Version Awaits

SATS Porter's Five Forces Analysis

This preview shows the exact SATS Porter's Five Forces analysis you'll receive—no placeholders or samples. The full, professionally formatted document is identical and ready for immediate download after purchase. It includes thorough, actionable insights for strategic decisions.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

SATS faces intense competitive dynamics across airport services, catering margins, and logistics scale advantages that shape pricing power and growth prospects. Supplier concentration and capital intensity limit flexibility, while regulatory barriers curb but don’t eliminate new entrants. This snapshot highlights key tensions but omits force-by-force ratings and visuals. Unlock the full Porter’s Five Forces Analysis for a detailed, actionable strategic breakdown tailored to SATS.

Suppliers Bargaining Power

Prime-site landlords

Urban high-traffic locations in Nordic capitals are scarce, giving landlords strong leverage on rent and lease terms. Long leases and costly fit-out obligations raise switching costs for SATS. A soft retail market in 2024 eased rent inflation and enabled renegotiations. Operating across four Nordic countries and listed on Oslo Børs (ticker SATS) helps diversify landlord exposure.

Gym equipment OEMs

Leading OEMs such as Technogym (2023 revenue €669.7m) and Life Fitness exert moderate supplier power via differentiated products and service networks, but SATS can multi-source and stagger refresh cycles to negotiate better terms. Large order volumes and long relationships secure discounts and SLAs, while supply-chain constraints or software-console lock-ins (noted across the ~USD10bn commercial equipment market in 2024) can swing power back to OEMs.

Group content and licensing

Licensors like Les Mills, whose formats are used in over 21,000 clubs across 100+ countries, command licensing fees for popular group formats, giving suppliers leverage. Strong content differentiation sustains member engagement and limits SATS’ ability to substitute quickly, though SATS can mitigate dependency by developing proprietary classes. Digital rights and music licensing (managed via PROs such as STIM/ASCAP/PRS) add recurring cost complexity.

Utilities and energy

Energy-intensive HVAC and lighting make SATS sensitive to utility price swings; Nord Pool volatility — with day-ahead spikes historically above €200–300/MWh and 2024 average Nordic baseload ≈€40–60/MWh — can raise supplier power. Hedging and capex in efficiency reduce exposure; scale procurement and ESG-linked demand response can secure lower tariffs.

- exposure: high energy intensity

- risk: Nordic price spikes

- mitigation: hedging + efficiency

- opportunity: scale & ESG tariffs

Tech platforms and payments

Nordic landlords wield leverage; 2024 soft rents spur renegotiations, energy risk rises

Landlord leverage high in Nordic urban sites; 2024 softer retail rents enabled renegotiations. OEMs (Technogym rev €669.7m 2023) and Les Mills (21,000 clubs) hold moderate licensing/equipment power; SATS (FY2024 rev ≈SGD 1.9bn) mitigates via scale, multi-sourcing and in-house tech. Energy exposure (Nord Pool 2024 baseload ≈€40–60/MWh) raises supplier risk; hedging and efficiency cut vulnerability.

| Factor | 2024 datapoint |

|---|---|

| Revenue | ≈SGD 1.9bn |

| Technogym 2023 | €669.7m |

| Nord Pool avg | €40–60/MWh |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored to SATS that uncovers competition drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, with strategic commentary and editable insights for investor decks, business plans, or internal strategy use.

A clear, one-sheet Porter's Five Forces for SATS that instantly visualizes strategic pressure with a customizable spider chart and scenario tabs for pre/post regulation or new entrants. Clean, copy-ready layout requires no macros, integrates into Excel/Word, and lets non-finance users swap in their own data for fast, boardroom-ready decisions.

Customers Bargaining Power

Low switching costs

Low switching costs let members cancel or move gyms easily, intensifying buyer power; SATS faces this despite operating >370 clubs and about 1.0 million members in 2024. Proximity and convenience often trump brand loyalty for many users, while flexible memberships and frequent promotions raise churn risk. SATS counters with network breadth and bundled services to retain members.

Price sensitivity

Budget chains set reference prices, squeezing SATS premium tiers and forcing competitive alignment; in 2024 consumers increasingly traded down or paused memberships amid macroeconomic tightness. Clear value communication on classes, PT and facilities proved decisive for retention. Tiered pricing and corporate discounts effectively segment willingness to pay.

Digital alternatives

Digital alternatives — apps and connected fitness, with over 300 SATS clubs in 2024 and rapid growth in on-demand consumption post-pandemic — let consumers substitute at marginal cost, raising expectations for hybrid, flexible experiences; buyers leverage this to demand extras and flexibility, while SATS’ omnichannel offerings can recapture value by bundling studio access with digital content and memberships.

Corporate and B2B buyers

Corporate and B2B buyers aggregate demand through wellness contracts that secure volume discounts and can dictate product features and reporting needs. These accounts span SATS' four Nordic markets, so losing a large client can materially reduce club utilization and revenues. SATS defends with proprietary outcomes data and multi‑market coverage to retain pricing and spread risk.

- Volume leverage: corporate contracts negotiate discounts

- Product influence: shape features and reporting

- Concentration risk: losing large account lowers utilization

- Defensive assets: outcomes data and multi‑market reach

Service quality transparency

Reviews, social media, and comparison sites have raised information symmetry for SATS customers, making cleanliness, crowding, and staff quality highly visible and directly affecting buyer leverage; a 2024 CX industry survey found 64% of travelers say a single poor service experience prompts cancellation. Real-time capacity feeds and NPS-driven recovery programs cut churn and strengthen supplier position when implemented effectively.

- reviews: visibility of cleanliness/staff

- real-time data: reduces churn

- NPS: recovery lowers cancellations

Buyers hold leverage; retention is critical for >370 clubs, ~1.0M members; 64% cancel after one bad CX

Low switching costs and digital substitutes give buyers strong leverage; SATS had >370 clubs and about 1.0 million members in 2024, driving focus on retention via bundles and omnichannel. Corporate buyers across four Nordic markets aggregate demand and can extract discounts; visible reviews and a 2024 CX survey (64% cancel after one bad experience) increase buyer influence.

| Metric | 2024 |

|---|---|

| Clubs | >370 |

| Members | ~1.0M |

| Markets | 4 Nordic |

| CX cancel rate | 64% (2024 survey) |

Full Version Awaits

SATS Porter's Five Forces Analysis

This preview shows the exact SATS Porter's Five Forces analysis you'll receive—no placeholders or samples. The full, professionally formatted document is identical and ready for immediate download after purchase. It includes thorough, actionable insights for strategic decisions.