Savannah Energy PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

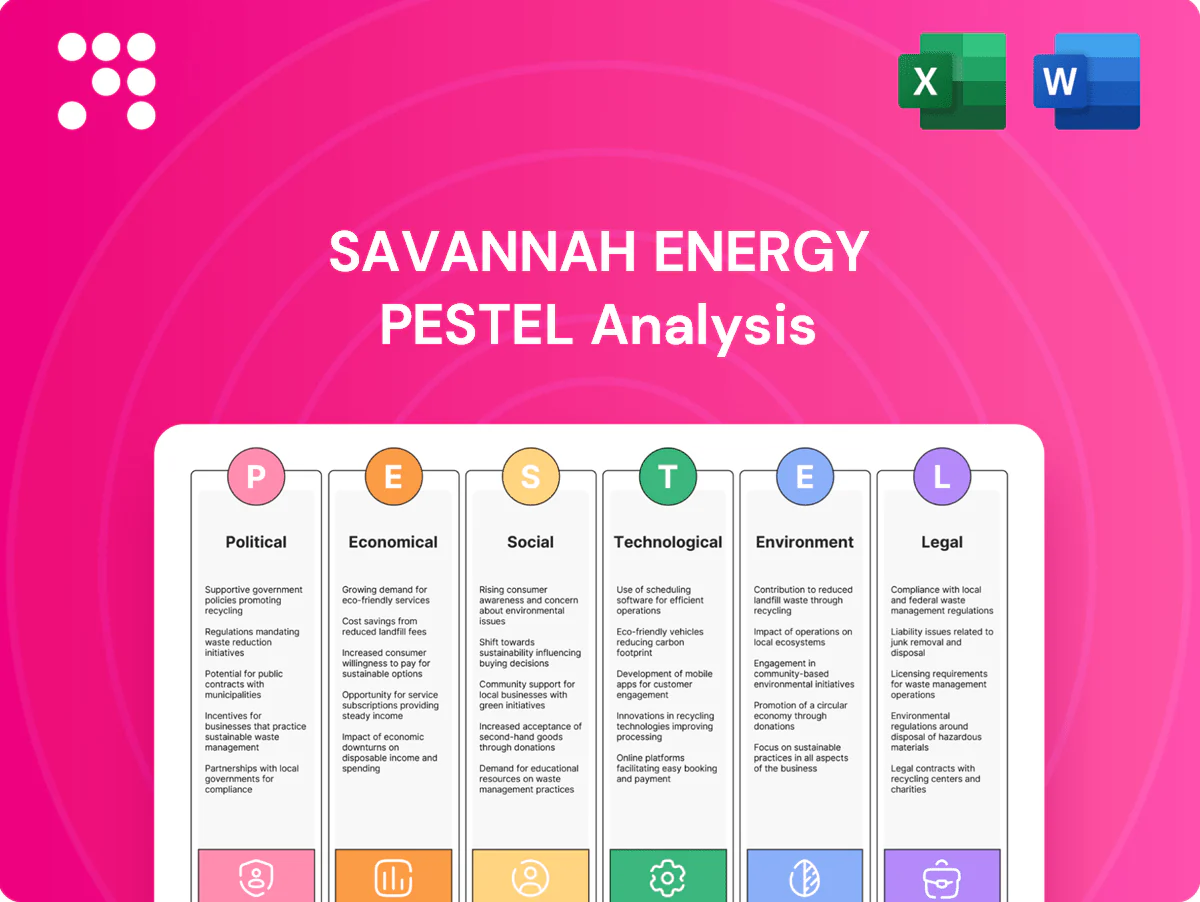

Discover how political shifts, regional economics, and environmental regulations are shaping Savannah Energy’s prospects in our concise PESTLE snapshot. This analysis highlights risks and opportunities for investors and strategists. Purchase the full PESTLE for the complete, actionable breakdown and downloadable templates.

Political factors

Regulatory stability in host nations

Operations depend on consistent energy policies and licensing regimes across the three African jurisdictions where Savannah Energy operates; policy reversals or fiscal term changes—seen regionally in 2024—can materially alter project economics and extend timelines by months or years. Proactive government engagement and continuous policy monitoring mitigate risk, and multi-country diversification reduces exposure to single-state volatility.

Resource nationalism and fiscal terms

Shifts in royalties, profit-oil splits and windfall taxes materially alter Savannah Energy cash flows; with Brent averaging about $86/bbl in 2024, fiscal take can jump sharply during upcycles. Governments in West Africa have signalled higher state participation when prices rise, pressuring margins. Robust PSC design and stabilization clauses protect project value, while transparent benefit-sharing and local content reporting improve host-state relations.

Security and geopolitical risk

Onshore assets and transmission corridors face insurgency, militancy and theft risks that have in some African basins caused production losses of up to 30% and forced capex schedule delays. Disruptions reduce uptime and raise remediation costs. Robust security protocols and community partnerships are essential. Political risk insurance complements measures; MIGA's gross exposure reached $24.8bn in FY2023.

Energy transition policy incentives

National plans increasingly support utility-scale solar and wind via competitive PPAs and fiscal incentives in 2024, and alignment with grid expansion agendas has sped approval timelines for large projects; participation in regional power pools (e.g., WAPP/ECOWAS) strengthens offtake certainty, while perceived policy credibility directly influences financing terms for renewables.

- PPAs growth in 2024: strengthened market signals

- Grid alignment: faster approvals for utility projects

- Regional pools: improved offtake certainty

- Policy credibility: key driver of financing spreads

Local content and government relations

Local content laws, notably Nigeria's 2010 Nigerian Content Act which targets c.70% domestic participation, shape Savannah Energy procurement, workforce composition and vendor selection, increasing onshore supplier spend and local hiring. Strong compliance builds political goodwill and operational resilience, reducing permit delays and fiscal disruptions. Long-term MoUs with ministries and capacity-building programs streamline project delivery and sustain partnerships.

- Local content target: c.70% (Nigerian Content Act 2010)

- Compliance reduces permitting risk

- MoUs accelerate approvals and CAPEX deployment

- Capacity-building secures local supply chains

Policy risk squeezes West Africa margins; Brent $86/bbl

Operations hinge on stable energy policy and licensing; 2024 Brent averaged $86/bbl and fiscal reversals can shift project NPV materially. Royalties, windfall taxes and rising state participation in West Africa compress margins. Security-related losses have reached c.30% in some basins, while Nigerian Content targets c.70% domestic participation. MIGA gross exposure was $24.8bn (FY2023).

| Metric | Value |

|---|---|

| Brent 2024 average | $86/bbl |

| Max reported production losses | c.30% |

| Nigerian Content target | c.70% |

| MIGA gross exposure FY2023 | $24.8bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Savannah Energy across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it provides forward-looking insights to identify risks, opportunities and strategic actions.

A concise, visually segmented PESTLE summary for Savannah Energy that distills regulatory, geopolitical, economic and environmental risks into an easily shareable format for quick alignment across teams and seamless inclusion in presentations or client reports.

Economic factors

Commodity price exposure

Revenues at Savannah are highly sensitive to Brent, which traded around $84/bbl in mid‑2025, and gas‑linked contracts, creating substantial cash‑flow volatility when prices swing. Active hedging of marketed volumes has been used to stabilise near‑term budgets and cap downside. A mixed oil, gas and renewables portfolio reduces cyclicality by smoothing commodity exposures. Maintaining conservative leverage metrics protects against prolonged downturns.

Power demand growth

African power demand growth underpins gas-to-power and renewables: Nigeria, where Savannah operates, has ~13 GW installed but only ~4–5 GW typically available in 2024, highlighting latent demand for firm capacity. Industrialization and urbanization (Africa urbanization projected toward ~60% by 2050) support multi-year load growth. Long-dated PPAs (typically 15–20 years) improve bankability, while persistent grid bottlenecks can constrain near-term monetization.

Currency and inflation risks

Revenue billed in USD while many expenses are in local currencies exposes Savannah to FX translation and liquidity risk; Nigeria headline inflation was 22.3% in Dec 2024 (NBS), boosting EPC and O&M unit costs. Natural FX hedges from dollar-linked offtake and indexed tariffs can offset volatility. Prudent treasury—forward cover and multicurrency cash pools—preserves margins.

Access to project finance

Capital intensity in Savannah Energy projects aligns with the global infrastructure investment gap—OECD/G20 estimate of about $15 trillion to 2040—driving need for blended finance from DFIs, export credit agencies and commercial banks.

Strong ESG credentials and de-risked PPAs materially improve access and can narrow funding spreads, while local capital market depth varies across West and Central African jurisdictions.

Phased development is used to reduce upfront funding strain and stage drawdowns to match offtake and cashflow milestones.

- DFIs/ECA/banks: blended finance required

- OECD/G20: $15 trillion infrastructure gap to 2040

- ESG + PPAs: lower cost of capital

- Local markets: depth varies by country

- Phased development: reduces funding strain

Infrastructure and logistics costs

Remote project sites raise transport, import and construction costs for Savannah Energy, increasing logistics premiums and contributing to multi-million-dollar uplift in project budgets and schedule risk.

Limited pipeline, road and port capacity in operating regions constrains throughput and can delay commissioning; co-developing enabling infrastructure has unlocked value in prior West African projects by improving time-to-first-gas and reducing unit costs.

Robust maintenance planning is essential to maximize uptime and control OPEX, where proactive asset management materially lowers unplanned shutdown costs and preserves revenue streams.

- Logistics premium: multi-million-dollar budget uplifts

- Capacity constraints: pipeline/port bottlenecks increase schedule risk

- Co-development: enables faster delivery and lower unit costs

- Maintenance focus: reduces unplanned downtime and OPEX

Policy risk squeezes West Africa margins; Brent $86/bbl

Revenues tied to Brent (~$84/bbl mid‑2025) and gas contracts drive cash‑flow volatility; active hedging and mixed oil/gas/renewables reduce cyclicality. Nigeria demand gap (13 GW installed, 4–5 GW available in 2024) supports gas‑to‑power; Dec‑2024 inflation 22.3% raises costs. Blended DFI/ECA finance narrows spreads; $15tn infrastructure gap to 2040 sustains capital needs.

| Metric | Value |

|---|---|

| Brent (mid‑2025) | $84/bbl |

| Nigeria available capacity (2024) | 4–5 GW |

| Nigeria inflation (Dec‑2024) | 22.3% |

| Infra gap | $15tn to 2040 |

Same Document Delivered

Savannah Energy PESTLE Analysis

The preview of the Savannah Energy PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the same content, structure and professional layout you’ll download immediately after payment. No placeholders or teasers—this is the real, final file.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, regional economics, and environmental regulations are shaping Savannah Energy’s prospects in our concise PESTLE snapshot. This analysis highlights risks and opportunities for investors and strategists. Purchase the full PESTLE for the complete, actionable breakdown and downloadable templates.

Political factors

Regulatory stability in host nations

Operations depend on consistent energy policies and licensing regimes across the three African jurisdictions where Savannah Energy operates; policy reversals or fiscal term changes—seen regionally in 2024—can materially alter project economics and extend timelines by months or years. Proactive government engagement and continuous policy monitoring mitigate risk, and multi-country diversification reduces exposure to single-state volatility.

Resource nationalism and fiscal terms

Shifts in royalties, profit-oil splits and windfall taxes materially alter Savannah Energy cash flows; with Brent averaging about $86/bbl in 2024, fiscal take can jump sharply during upcycles. Governments in West Africa have signalled higher state participation when prices rise, pressuring margins. Robust PSC design and stabilization clauses protect project value, while transparent benefit-sharing and local content reporting improve host-state relations.

Security and geopolitical risk

Onshore assets and transmission corridors face insurgency, militancy and theft risks that have in some African basins caused production losses of up to 30% and forced capex schedule delays. Disruptions reduce uptime and raise remediation costs. Robust security protocols and community partnerships are essential. Political risk insurance complements measures; MIGA's gross exposure reached $24.8bn in FY2023.

Energy transition policy incentives

National plans increasingly support utility-scale solar and wind via competitive PPAs and fiscal incentives in 2024, and alignment with grid expansion agendas has sped approval timelines for large projects; participation in regional power pools (e.g., WAPP/ECOWAS) strengthens offtake certainty, while perceived policy credibility directly influences financing terms for renewables.

- PPAs growth in 2024: strengthened market signals

- Grid alignment: faster approvals for utility projects

- Regional pools: improved offtake certainty

- Policy credibility: key driver of financing spreads

Local content and government relations

Local content laws, notably Nigeria's 2010 Nigerian Content Act which targets c.70% domestic participation, shape Savannah Energy procurement, workforce composition and vendor selection, increasing onshore supplier spend and local hiring. Strong compliance builds political goodwill and operational resilience, reducing permit delays and fiscal disruptions. Long-term MoUs with ministries and capacity-building programs streamline project delivery and sustain partnerships.

- Local content target: c.70% (Nigerian Content Act 2010)

- Compliance reduces permitting risk

- MoUs accelerate approvals and CAPEX deployment

- Capacity-building secures local supply chains

Policy risk squeezes West Africa margins; Brent $86/bbl

Operations hinge on stable energy policy and licensing; 2024 Brent averaged $86/bbl and fiscal reversals can shift project NPV materially. Royalties, windfall taxes and rising state participation in West Africa compress margins. Security-related losses have reached c.30% in some basins, while Nigerian Content targets c.70% domestic participation. MIGA gross exposure was $24.8bn (FY2023).

| Metric | Value |

|---|---|

| Brent 2024 average | $86/bbl |

| Max reported production losses | c.30% |

| Nigerian Content target | c.70% |

| MIGA gross exposure FY2023 | $24.8bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Savannah Energy across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it provides forward-looking insights to identify risks, opportunities and strategic actions.

A concise, visually segmented PESTLE summary for Savannah Energy that distills regulatory, geopolitical, economic and environmental risks into an easily shareable format for quick alignment across teams and seamless inclusion in presentations or client reports.

Economic factors

Commodity price exposure

Revenues at Savannah are highly sensitive to Brent, which traded around $84/bbl in mid‑2025, and gas‑linked contracts, creating substantial cash‑flow volatility when prices swing. Active hedging of marketed volumes has been used to stabilise near‑term budgets and cap downside. A mixed oil, gas and renewables portfolio reduces cyclicality by smoothing commodity exposures. Maintaining conservative leverage metrics protects against prolonged downturns.

Power demand growth

African power demand growth underpins gas-to-power and renewables: Nigeria, where Savannah operates, has ~13 GW installed but only ~4–5 GW typically available in 2024, highlighting latent demand for firm capacity. Industrialization and urbanization (Africa urbanization projected toward ~60% by 2050) support multi-year load growth. Long-dated PPAs (typically 15–20 years) improve bankability, while persistent grid bottlenecks can constrain near-term monetization.

Currency and inflation risks

Revenue billed in USD while many expenses are in local currencies exposes Savannah to FX translation and liquidity risk; Nigeria headline inflation was 22.3% in Dec 2024 (NBS), boosting EPC and O&M unit costs. Natural FX hedges from dollar-linked offtake and indexed tariffs can offset volatility. Prudent treasury—forward cover and multicurrency cash pools—preserves margins.

Access to project finance

Capital intensity in Savannah Energy projects aligns with the global infrastructure investment gap—OECD/G20 estimate of about $15 trillion to 2040—driving need for blended finance from DFIs, export credit agencies and commercial banks.

Strong ESG credentials and de-risked PPAs materially improve access and can narrow funding spreads, while local capital market depth varies across West and Central African jurisdictions.

Phased development is used to reduce upfront funding strain and stage drawdowns to match offtake and cashflow milestones.

- DFIs/ECA/banks: blended finance required

- OECD/G20: $15 trillion infrastructure gap to 2040

- ESG + PPAs: lower cost of capital

- Local markets: depth varies by country

- Phased development: reduces funding strain

Infrastructure and logistics costs

Remote project sites raise transport, import and construction costs for Savannah Energy, increasing logistics premiums and contributing to multi-million-dollar uplift in project budgets and schedule risk.

Limited pipeline, road and port capacity in operating regions constrains throughput and can delay commissioning; co-developing enabling infrastructure has unlocked value in prior West African projects by improving time-to-first-gas and reducing unit costs.

Robust maintenance planning is essential to maximize uptime and control OPEX, where proactive asset management materially lowers unplanned shutdown costs and preserves revenue streams.

- Logistics premium: multi-million-dollar budget uplifts

- Capacity constraints: pipeline/port bottlenecks increase schedule risk

- Co-development: enables faster delivery and lower unit costs

- Maintenance focus: reduces unplanned downtime and OPEX

Policy risk squeezes West Africa margins; Brent $86/bbl

Revenues tied to Brent (~$84/bbl mid‑2025) and gas contracts drive cash‑flow volatility; active hedging and mixed oil/gas/renewables reduce cyclicality. Nigeria demand gap (13 GW installed, 4–5 GW available in 2024) supports gas‑to‑power; Dec‑2024 inflation 22.3% raises costs. Blended DFI/ECA finance narrows spreads; $15tn infrastructure gap to 2040 sustains capital needs.

| Metric | Value |

|---|---|

| Brent (mid‑2025) | $84/bbl |

| Nigeria available capacity (2024) | 4–5 GW |

| Nigeria inflation (Dec‑2024) | 22.3% |

| Infra gap | $15tn to 2040 |

Same Document Delivered

Savannah Energy PESTLE Analysis

The preview of the Savannah Energy PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the same content, structure and professional layout you’ll download immediately after payment. No placeholders or teasers—this is the real, final file.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, regional economics, and environmental regulations are shaping Savannah Energy’s prospects in our concise PESTLE snapshot. This analysis highlights risks and opportunities for investors and strategists. Purchase the full PESTLE for the complete, actionable breakdown and downloadable templates.

Political factors

Regulatory stability in host nations

Operations depend on consistent energy policies and licensing regimes across the three African jurisdictions where Savannah Energy operates; policy reversals or fiscal term changes—seen regionally in 2024—can materially alter project economics and extend timelines by months or years. Proactive government engagement and continuous policy monitoring mitigate risk, and multi-country diversification reduces exposure to single-state volatility.

Resource nationalism and fiscal terms

Shifts in royalties, profit-oil splits and windfall taxes materially alter Savannah Energy cash flows; with Brent averaging about $86/bbl in 2024, fiscal take can jump sharply during upcycles. Governments in West Africa have signalled higher state participation when prices rise, pressuring margins. Robust PSC design and stabilization clauses protect project value, while transparent benefit-sharing and local content reporting improve host-state relations.

Security and geopolitical risk

Onshore assets and transmission corridors face insurgency, militancy and theft risks that have in some African basins caused production losses of up to 30% and forced capex schedule delays. Disruptions reduce uptime and raise remediation costs. Robust security protocols and community partnerships are essential. Political risk insurance complements measures; MIGA's gross exposure reached $24.8bn in FY2023.

Energy transition policy incentives

National plans increasingly support utility-scale solar and wind via competitive PPAs and fiscal incentives in 2024, and alignment with grid expansion agendas has sped approval timelines for large projects; participation in regional power pools (e.g., WAPP/ECOWAS) strengthens offtake certainty, while perceived policy credibility directly influences financing terms for renewables.

- PPAs growth in 2024: strengthened market signals

- Grid alignment: faster approvals for utility projects

- Regional pools: improved offtake certainty

- Policy credibility: key driver of financing spreads

Local content and government relations

Local content laws, notably Nigeria's 2010 Nigerian Content Act which targets c.70% domestic participation, shape Savannah Energy procurement, workforce composition and vendor selection, increasing onshore supplier spend and local hiring. Strong compliance builds political goodwill and operational resilience, reducing permit delays and fiscal disruptions. Long-term MoUs with ministries and capacity-building programs streamline project delivery and sustain partnerships.

- Local content target: c.70% (Nigerian Content Act 2010)

- Compliance reduces permitting risk

- MoUs accelerate approvals and CAPEX deployment

- Capacity-building secures local supply chains

Policy risk squeezes West Africa margins; Brent $86/bbl

Operations hinge on stable energy policy and licensing; 2024 Brent averaged $86/bbl and fiscal reversals can shift project NPV materially. Royalties, windfall taxes and rising state participation in West Africa compress margins. Security-related losses have reached c.30% in some basins, while Nigerian Content targets c.70% domestic participation. MIGA gross exposure was $24.8bn (FY2023).

| Metric | Value |

|---|---|

| Brent 2024 average | $86/bbl |

| Max reported production losses | c.30% |

| Nigerian Content target | c.70% |

| MIGA gross exposure FY2023 | $24.8bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Savannah Energy across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it provides forward-looking insights to identify risks, opportunities and strategic actions.

A concise, visually segmented PESTLE summary for Savannah Energy that distills regulatory, geopolitical, economic and environmental risks into an easily shareable format for quick alignment across teams and seamless inclusion in presentations or client reports.

Economic factors

Commodity price exposure

Revenues at Savannah are highly sensitive to Brent, which traded around $84/bbl in mid‑2025, and gas‑linked contracts, creating substantial cash‑flow volatility when prices swing. Active hedging of marketed volumes has been used to stabilise near‑term budgets and cap downside. A mixed oil, gas and renewables portfolio reduces cyclicality by smoothing commodity exposures. Maintaining conservative leverage metrics protects against prolonged downturns.

Power demand growth

African power demand growth underpins gas-to-power and renewables: Nigeria, where Savannah operates, has ~13 GW installed but only ~4–5 GW typically available in 2024, highlighting latent demand for firm capacity. Industrialization and urbanization (Africa urbanization projected toward ~60% by 2050) support multi-year load growth. Long-dated PPAs (typically 15–20 years) improve bankability, while persistent grid bottlenecks can constrain near-term monetization.

Currency and inflation risks

Revenue billed in USD while many expenses are in local currencies exposes Savannah to FX translation and liquidity risk; Nigeria headline inflation was 22.3% in Dec 2024 (NBS), boosting EPC and O&M unit costs. Natural FX hedges from dollar-linked offtake and indexed tariffs can offset volatility. Prudent treasury—forward cover and multicurrency cash pools—preserves margins.

Access to project finance

Capital intensity in Savannah Energy projects aligns with the global infrastructure investment gap—OECD/G20 estimate of about $15 trillion to 2040—driving need for blended finance from DFIs, export credit agencies and commercial banks.

Strong ESG credentials and de-risked PPAs materially improve access and can narrow funding spreads, while local capital market depth varies across West and Central African jurisdictions.

Phased development is used to reduce upfront funding strain and stage drawdowns to match offtake and cashflow milestones.

- DFIs/ECA/banks: blended finance required

- OECD/G20: $15 trillion infrastructure gap to 2040

- ESG + PPAs: lower cost of capital

- Local markets: depth varies by country

- Phased development: reduces funding strain

Infrastructure and logistics costs

Remote project sites raise transport, import and construction costs for Savannah Energy, increasing logistics premiums and contributing to multi-million-dollar uplift in project budgets and schedule risk.

Limited pipeline, road and port capacity in operating regions constrains throughput and can delay commissioning; co-developing enabling infrastructure has unlocked value in prior West African projects by improving time-to-first-gas and reducing unit costs.

Robust maintenance planning is essential to maximize uptime and control OPEX, where proactive asset management materially lowers unplanned shutdown costs and preserves revenue streams.

- Logistics premium: multi-million-dollar budget uplifts

- Capacity constraints: pipeline/port bottlenecks increase schedule risk

- Co-development: enables faster delivery and lower unit costs

- Maintenance focus: reduces unplanned downtime and OPEX

Policy risk squeezes West Africa margins; Brent $86/bbl

Revenues tied to Brent (~$84/bbl mid‑2025) and gas contracts drive cash‑flow volatility; active hedging and mixed oil/gas/renewables reduce cyclicality. Nigeria demand gap (13 GW installed, 4–5 GW available in 2024) supports gas‑to‑power; Dec‑2024 inflation 22.3% raises costs. Blended DFI/ECA finance narrows spreads; $15tn infrastructure gap to 2040 sustains capital needs.

| Metric | Value |

|---|---|

| Brent (mid‑2025) | $84/bbl |

| Nigeria available capacity (2024) | 4–5 GW |

| Nigeria inflation (Dec‑2024) | 22.3% |

| Infra gap | $15tn to 2040 |

Same Document Delivered

Savannah Energy PESTLE Analysis

The preview of the Savannah Energy PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the same content, structure and professional layout you’ll download immediately after payment. No placeholders or teasers—this is the real, final file.