Savencia Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

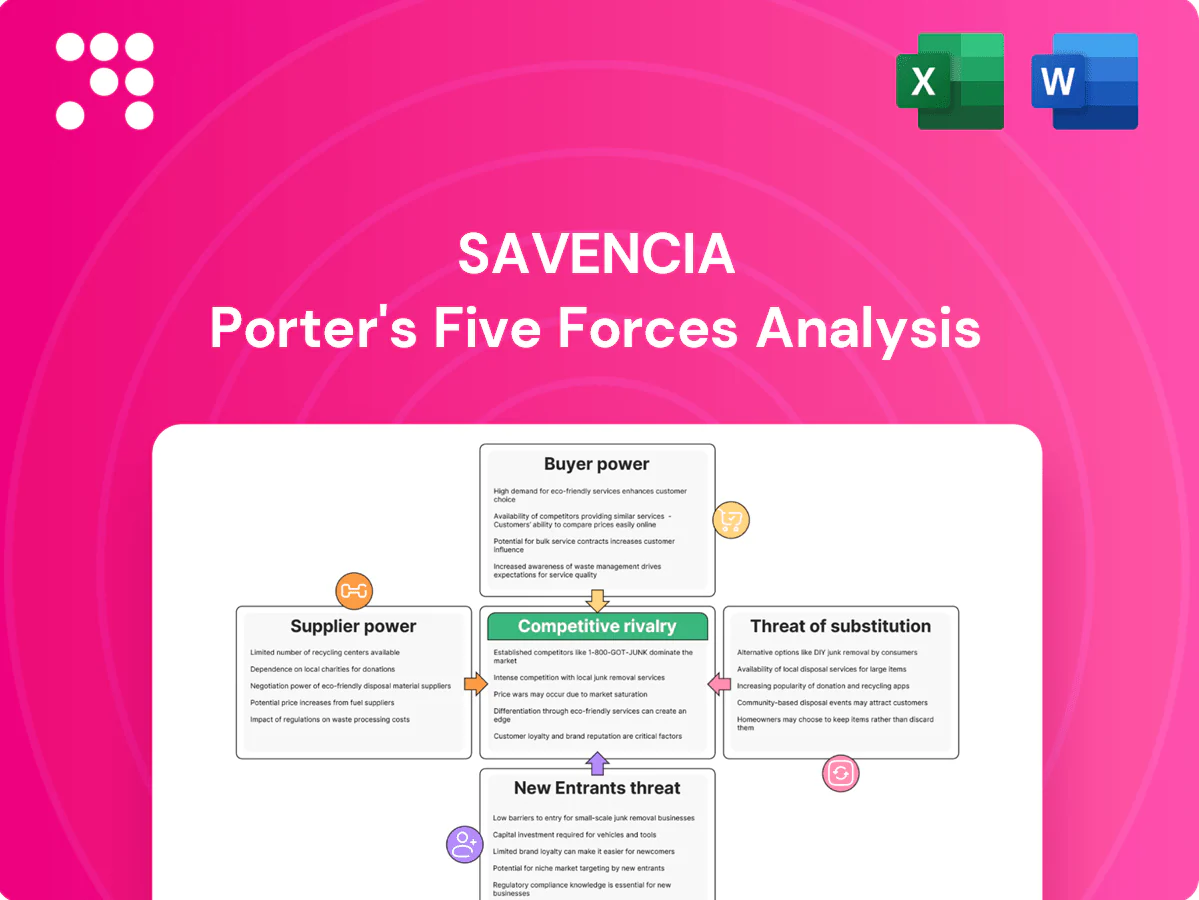

Savencia’s Porter's Five Forces snapshot highlights buyer power, supplier influence, competitive rivalry, substitute threats, and barriers to entry shaping its dairy and specialty cheese markets. Our concise review surfaces core pressures and strategic levers but leaves force-by-force ratings and implications brief. This preview only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable recommendations to guide investment or strategy.

Suppliers Bargaining Power

Concentrated milk supply in key regions

Milk sourcing is concentrated in regional farmer cooperatives—EU milk output remained around 150 million tonnes in 2023–24—allowing co-ops in tight basins to extract premiums or tougher terms. Savencia reduces supplier leverage via multi-country sourcing and long-term purchase contracts covering significant volumes. Nevertheless weather shocks, feed-cost spikes and herd-cycle lows can push farm-gate prices higher, strengthening supplier bargaining in constrained markets.

Volatile raw milk and feed input prices

Volatile raw milk and feed prices — EU farmgate milk averaged about €43/100kg in 2024 — shift bargaining power to suppliers during up-cycles, squeezing Savencia’s short-term margins. Hedging, formula pricing and product-mix adjustments damp volatility but do not remove it. Premium specialty cheeses allow partial pass-through, moderating supplier power.

Specialty inputs: cultures, enzymes, packaging

Savencia relies on a concentrated pool of suppliers for proprietary cultures, rennet and high-barrier packaging, giving vendors elevated leverage due to switching costs, QA and regulatory approvals. Dual qualification of suppliers and in-house fermentation expertise mitigate but do not eliminate dependence. Supply disruptions can directly reduce yields and consistency, affecting product availability and margins.

Energy and logistics as critical enablers

Cold-chain logistics and energy are essential for Savencia’s dairy processing and distribution, making transport and power suppliers structurally powerful when capacity tightens or prices spike. Price shocks in fuel or electricity quickly raise input costs and compress margins, increasing supplier leverage. Savencia’s geographic diversification and long-term contracts mitigate risk, but exposure in high-cost regions persists. Sustainability investments in on-site renewables and efficiency reduce dependency and long-term cost risk.

- Critical inputs: cold-chain energy and transport

- Risk: price spikes raise supplier power

- Mitigation: diversified footprint and contracts

- Long-term: renewables/efficiency lower dependency

Quality, animal welfare, and traceability requirements

Stricter quality, animal welfare, and traceability requirements narrow Savencia’s eligible supplier base, increasing leverage for compliant farmers and intermediaries while limiting sourcing flexibility; certification and traceability systems raise switching costs and operational complexity. Savencia gains brand differentiation from higher standards but must invest in collaborative programs to align incentives, stabilize supply and mitigate procurement risk.

- Certification increases supplier bargaining power

- Traceability raises switching costs

- Higher standards = tighter sourcing flexibility

- Collaborative programs stabilize supply

EU milk concentration increases leverage; multi-country sourcing and long contracts curb risk

Milk sourcing concentrated in regional co-ops (EU milk ~150 million tonnes 2023–24) and farm-gate spikes (EU farmgate ~€43/100kg in 2024) increase supplier leverage; Savencia limits this via multi-country sourcing and long-term contracts. High-barrier inputs (cultures, rennet, packaging) and certification raise switching costs; renewables and dual-sourcing mitigate risk.

| Metric | Value | Implication |

|---|---|---|

| EU milk output | ~150M t (2023–24) | Concentrated regional power |

| EU farmgate milk | ~€43/100kg (2024) | Price-driven supplier leverage |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, substitute threats and entry barriers tailored exclusively for Savencia, with detailed strategic commentary on disruptive forces and market dynamics to inform pricing, positioning and defensive strategies.

One-sheet Savencia Porter's Five Forces relieves decision-making pain by consolidating competitive pressures into a customizable, visual spider chart—easy to edit, copy into decks, and integrate with reports for clear, board-ready strategic insight.

Customers Bargaining Power

Large retailers and discounters

Grocers and discounters in Europe exert strong shelf-space control and pricing pressure, with discounters holding roughly 14% of grocery market share in 2024 and private label accounting for about 38% of Western European grocery sales in 2024, increasing buyer leverage over branded suppliers. Savencia’s specialty positioning limits some exposure, but heavy promotional reliance can compress margins and EBITDA. Joint category management and product differentiation can help rebalance power by driving premium placement and mix improvement.

Foodservice chains and industrial buyers

High-volume foodservice chains and industrial buyers can push on price, specs and lead times, using contractual tenders that intensified supplier competition in 2024; Savencia reported €3.9bn in sales that year, exposing scale-sensitive exposure. Savencia’s wide format range and technical support create customer stickiness, yet large concentrated bids concentrate risk and strengthen buyer leverage.

Consumers’ price sensitivity vs. premium niches

Mass-market cheese is highly price sensitive, with private-label penetration in EU grocery channels around 30–40%, empowering retailers to push down price points. In premium and specialty segments Savencia’s brands, origin claims and taste profiles markedly reduce elasticity, sustaining higher margins. Savencia’s portfolio mix lets it shift buyer power by channel, while recessions historically swing consumers back toward price-focused buyers.

International diversification and channel mix

- Global reach: present in 120+ countries (2024)

- Market structure: top chains dominate locally

- Emerging markets: growth with potential stronger local negotiators

- Channel mix: retail, e-commerce, foodservice dilutes single-buyer risk

Switching costs and product differentiation

In commoditized formats switching suppliers is easy, strengthening buyer power and compressing margins; Savencia 2024 sales ~€4.9bn support scale but not immunity. Specialty cheeses and functional ingredients create reformulation and taste frictions that reduce churn. PDO/PGI certifications and provenance anchor choices, while R&D and culinary support raise retention.

Retailer leverage: discounters ~14%, private label ~38%

Retailers hold strong leverage: discounters ~14% and private label ~38% of Western European grocery sales in 2024, pressuring branded pricing. Savencia’s €4.9bn 2024 sales and 120+ country footprint dilute but do not eliminate buyer power. Specialty brands, PDO/PGI and technical service increase stickiness and margin resilience.

| Metric | 2024 |

|---|---|

| Discounters share | ~14% |

| Private label W. Europe | ~38% |

| Savencia sales | €4.9bn |

| Countries | 120+ |

Preview Before You Purchase

Savencia Porter's Five Forces Analysis

This preview shows the exact Savencia Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy. You're looking at the actual file; once payment is complete you’ll get instant access to this identical deliverable.

Go Beyond the Preview—Access the Full Strategic Report

Savencia’s Porter's Five Forces snapshot highlights buyer power, supplier influence, competitive rivalry, substitute threats, and barriers to entry shaping its dairy and specialty cheese markets. Our concise review surfaces core pressures and strategic levers but leaves force-by-force ratings and implications brief. This preview only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable recommendations to guide investment or strategy.

Suppliers Bargaining Power

Concentrated milk supply in key regions

Milk sourcing is concentrated in regional farmer cooperatives—EU milk output remained around 150 million tonnes in 2023–24—allowing co-ops in tight basins to extract premiums or tougher terms. Savencia reduces supplier leverage via multi-country sourcing and long-term purchase contracts covering significant volumes. Nevertheless weather shocks, feed-cost spikes and herd-cycle lows can push farm-gate prices higher, strengthening supplier bargaining in constrained markets.

Volatile raw milk and feed input prices

Volatile raw milk and feed prices — EU farmgate milk averaged about €43/100kg in 2024 — shift bargaining power to suppliers during up-cycles, squeezing Savencia’s short-term margins. Hedging, formula pricing and product-mix adjustments damp volatility but do not remove it. Premium specialty cheeses allow partial pass-through, moderating supplier power.

Specialty inputs: cultures, enzymes, packaging

Savencia relies on a concentrated pool of suppliers for proprietary cultures, rennet and high-barrier packaging, giving vendors elevated leverage due to switching costs, QA and regulatory approvals. Dual qualification of suppliers and in-house fermentation expertise mitigate but do not eliminate dependence. Supply disruptions can directly reduce yields and consistency, affecting product availability and margins.

Energy and logistics as critical enablers

Cold-chain logistics and energy are essential for Savencia’s dairy processing and distribution, making transport and power suppliers structurally powerful when capacity tightens or prices spike. Price shocks in fuel or electricity quickly raise input costs and compress margins, increasing supplier leverage. Savencia’s geographic diversification and long-term contracts mitigate risk, but exposure in high-cost regions persists. Sustainability investments in on-site renewables and efficiency reduce dependency and long-term cost risk.

- Critical inputs: cold-chain energy and transport

- Risk: price spikes raise supplier power

- Mitigation: diversified footprint and contracts

- Long-term: renewables/efficiency lower dependency

Quality, animal welfare, and traceability requirements

Stricter quality, animal welfare, and traceability requirements narrow Savencia’s eligible supplier base, increasing leverage for compliant farmers and intermediaries while limiting sourcing flexibility; certification and traceability systems raise switching costs and operational complexity. Savencia gains brand differentiation from higher standards but must invest in collaborative programs to align incentives, stabilize supply and mitigate procurement risk.

- Certification increases supplier bargaining power

- Traceability raises switching costs

- Higher standards = tighter sourcing flexibility

- Collaborative programs stabilize supply

EU milk concentration increases leverage; multi-country sourcing and long contracts curb risk

Milk sourcing concentrated in regional co-ops (EU milk ~150 million tonnes 2023–24) and farm-gate spikes (EU farmgate ~€43/100kg in 2024) increase supplier leverage; Savencia limits this via multi-country sourcing and long-term contracts. High-barrier inputs (cultures, rennet, packaging) and certification raise switching costs; renewables and dual-sourcing mitigate risk.

| Metric | Value | Implication |

|---|---|---|

| EU milk output | ~150M t (2023–24) | Concentrated regional power |

| EU farmgate milk | ~€43/100kg (2024) | Price-driven supplier leverage |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, substitute threats and entry barriers tailored exclusively for Savencia, with detailed strategic commentary on disruptive forces and market dynamics to inform pricing, positioning and defensive strategies.

One-sheet Savencia Porter's Five Forces relieves decision-making pain by consolidating competitive pressures into a customizable, visual spider chart—easy to edit, copy into decks, and integrate with reports for clear, board-ready strategic insight.

Customers Bargaining Power

Large retailers and discounters

Grocers and discounters in Europe exert strong shelf-space control and pricing pressure, with discounters holding roughly 14% of grocery market share in 2024 and private label accounting for about 38% of Western European grocery sales in 2024, increasing buyer leverage over branded suppliers. Savencia’s specialty positioning limits some exposure, but heavy promotional reliance can compress margins and EBITDA. Joint category management and product differentiation can help rebalance power by driving premium placement and mix improvement.

Foodservice chains and industrial buyers

High-volume foodservice chains and industrial buyers can push on price, specs and lead times, using contractual tenders that intensified supplier competition in 2024; Savencia reported €3.9bn in sales that year, exposing scale-sensitive exposure. Savencia’s wide format range and technical support create customer stickiness, yet large concentrated bids concentrate risk and strengthen buyer leverage.

Consumers’ price sensitivity vs. premium niches

Mass-market cheese is highly price sensitive, with private-label penetration in EU grocery channels around 30–40%, empowering retailers to push down price points. In premium and specialty segments Savencia’s brands, origin claims and taste profiles markedly reduce elasticity, sustaining higher margins. Savencia’s portfolio mix lets it shift buyer power by channel, while recessions historically swing consumers back toward price-focused buyers.

International diversification and channel mix

- Global reach: present in 120+ countries (2024)

- Market structure: top chains dominate locally

- Emerging markets: growth with potential stronger local negotiators

- Channel mix: retail, e-commerce, foodservice dilutes single-buyer risk

Switching costs and product differentiation

In commoditized formats switching suppliers is easy, strengthening buyer power and compressing margins; Savencia 2024 sales ~€4.9bn support scale but not immunity. Specialty cheeses and functional ingredients create reformulation and taste frictions that reduce churn. PDO/PGI certifications and provenance anchor choices, while R&D and culinary support raise retention.

Retailer leverage: discounters ~14%, private label ~38%

Retailers hold strong leverage: discounters ~14% and private label ~38% of Western European grocery sales in 2024, pressuring branded pricing. Savencia’s €4.9bn 2024 sales and 120+ country footprint dilute but do not eliminate buyer power. Specialty brands, PDO/PGI and technical service increase stickiness and margin resilience.

| Metric | 2024 |

|---|---|

| Discounters share | ~14% |

| Private label W. Europe | ~38% |

| Savencia sales | €4.9bn |

| Countries | 120+ |

Preview Before You Purchase

Savencia Porter's Five Forces Analysis

This preview shows the exact Savencia Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy. You're looking at the actual file; once payment is complete you’ll get instant access to this identical deliverable.

Description

Go Beyond the Preview—Access the Full Strategic Report

Savencia’s Porter's Five Forces snapshot highlights buyer power, supplier influence, competitive rivalry, substitute threats, and barriers to entry shaping its dairy and specialty cheese markets. Our concise review surfaces core pressures and strategic levers but leaves force-by-force ratings and implications brief. This preview only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable recommendations to guide investment or strategy.

Suppliers Bargaining Power

Concentrated milk supply in key regions

Milk sourcing is concentrated in regional farmer cooperatives—EU milk output remained around 150 million tonnes in 2023–24—allowing co-ops in tight basins to extract premiums or tougher terms. Savencia reduces supplier leverage via multi-country sourcing and long-term purchase contracts covering significant volumes. Nevertheless weather shocks, feed-cost spikes and herd-cycle lows can push farm-gate prices higher, strengthening supplier bargaining in constrained markets.

Volatile raw milk and feed input prices

Volatile raw milk and feed prices — EU farmgate milk averaged about €43/100kg in 2024 — shift bargaining power to suppliers during up-cycles, squeezing Savencia’s short-term margins. Hedging, formula pricing and product-mix adjustments damp volatility but do not remove it. Premium specialty cheeses allow partial pass-through, moderating supplier power.

Specialty inputs: cultures, enzymes, packaging

Savencia relies on a concentrated pool of suppliers for proprietary cultures, rennet and high-barrier packaging, giving vendors elevated leverage due to switching costs, QA and regulatory approvals. Dual qualification of suppliers and in-house fermentation expertise mitigate but do not eliminate dependence. Supply disruptions can directly reduce yields and consistency, affecting product availability and margins.

Energy and logistics as critical enablers

Cold-chain logistics and energy are essential for Savencia’s dairy processing and distribution, making transport and power suppliers structurally powerful when capacity tightens or prices spike. Price shocks in fuel or electricity quickly raise input costs and compress margins, increasing supplier leverage. Savencia’s geographic diversification and long-term contracts mitigate risk, but exposure in high-cost regions persists. Sustainability investments in on-site renewables and efficiency reduce dependency and long-term cost risk.

- Critical inputs: cold-chain energy and transport

- Risk: price spikes raise supplier power

- Mitigation: diversified footprint and contracts

- Long-term: renewables/efficiency lower dependency

Quality, animal welfare, and traceability requirements

Stricter quality, animal welfare, and traceability requirements narrow Savencia’s eligible supplier base, increasing leverage for compliant farmers and intermediaries while limiting sourcing flexibility; certification and traceability systems raise switching costs and operational complexity. Savencia gains brand differentiation from higher standards but must invest in collaborative programs to align incentives, stabilize supply and mitigate procurement risk.

- Certification increases supplier bargaining power

- Traceability raises switching costs

- Higher standards = tighter sourcing flexibility

- Collaborative programs stabilize supply

EU milk concentration increases leverage; multi-country sourcing and long contracts curb risk

Milk sourcing concentrated in regional co-ops (EU milk ~150 million tonnes 2023–24) and farm-gate spikes (EU farmgate ~€43/100kg in 2024) increase supplier leverage; Savencia limits this via multi-country sourcing and long-term contracts. High-barrier inputs (cultures, rennet, packaging) and certification raise switching costs; renewables and dual-sourcing mitigate risk.

| Metric | Value | Implication |

|---|---|---|

| EU milk output | ~150M t (2023–24) | Concentrated regional power |

| EU farmgate milk | ~€43/100kg (2024) | Price-driven supplier leverage |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, substitute threats and entry barriers tailored exclusively for Savencia, with detailed strategic commentary on disruptive forces and market dynamics to inform pricing, positioning and defensive strategies.

One-sheet Savencia Porter's Five Forces relieves decision-making pain by consolidating competitive pressures into a customizable, visual spider chart—easy to edit, copy into decks, and integrate with reports for clear, board-ready strategic insight.

Customers Bargaining Power

Large retailers and discounters

Grocers and discounters in Europe exert strong shelf-space control and pricing pressure, with discounters holding roughly 14% of grocery market share in 2024 and private label accounting for about 38% of Western European grocery sales in 2024, increasing buyer leverage over branded suppliers. Savencia’s specialty positioning limits some exposure, but heavy promotional reliance can compress margins and EBITDA. Joint category management and product differentiation can help rebalance power by driving premium placement and mix improvement.

Foodservice chains and industrial buyers

High-volume foodservice chains and industrial buyers can push on price, specs and lead times, using contractual tenders that intensified supplier competition in 2024; Savencia reported €3.9bn in sales that year, exposing scale-sensitive exposure. Savencia’s wide format range and technical support create customer stickiness, yet large concentrated bids concentrate risk and strengthen buyer leverage.

Consumers’ price sensitivity vs. premium niches

Mass-market cheese is highly price sensitive, with private-label penetration in EU grocery channels around 30–40%, empowering retailers to push down price points. In premium and specialty segments Savencia’s brands, origin claims and taste profiles markedly reduce elasticity, sustaining higher margins. Savencia’s portfolio mix lets it shift buyer power by channel, while recessions historically swing consumers back toward price-focused buyers.

International diversification and channel mix

- Global reach: present in 120+ countries (2024)

- Market structure: top chains dominate locally

- Emerging markets: growth with potential stronger local negotiators

- Channel mix: retail, e-commerce, foodservice dilutes single-buyer risk

Switching costs and product differentiation

In commoditized formats switching suppliers is easy, strengthening buyer power and compressing margins; Savencia 2024 sales ~€4.9bn support scale but not immunity. Specialty cheeses and functional ingredients create reformulation and taste frictions that reduce churn. PDO/PGI certifications and provenance anchor choices, while R&D and culinary support raise retention.

Retailer leverage: discounters ~14%, private label ~38%

Retailers hold strong leverage: discounters ~14% and private label ~38% of Western European grocery sales in 2024, pressuring branded pricing. Savencia’s €4.9bn 2024 sales and 120+ country footprint dilute but do not eliminate buyer power. Specialty brands, PDO/PGI and technical service increase stickiness and margin resilience.

| Metric | 2024 |

|---|---|

| Discounters share | ~14% |

| Private label W. Europe | ~38% |

| Savencia sales | €4.9bn |

| Countries | 120+ |

Preview Before You Purchase

Savencia Porter's Five Forces Analysis

This preview shows the exact Savencia Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy. You're looking at the actual file; once payment is complete you’ll get instant access to this identical deliverable.