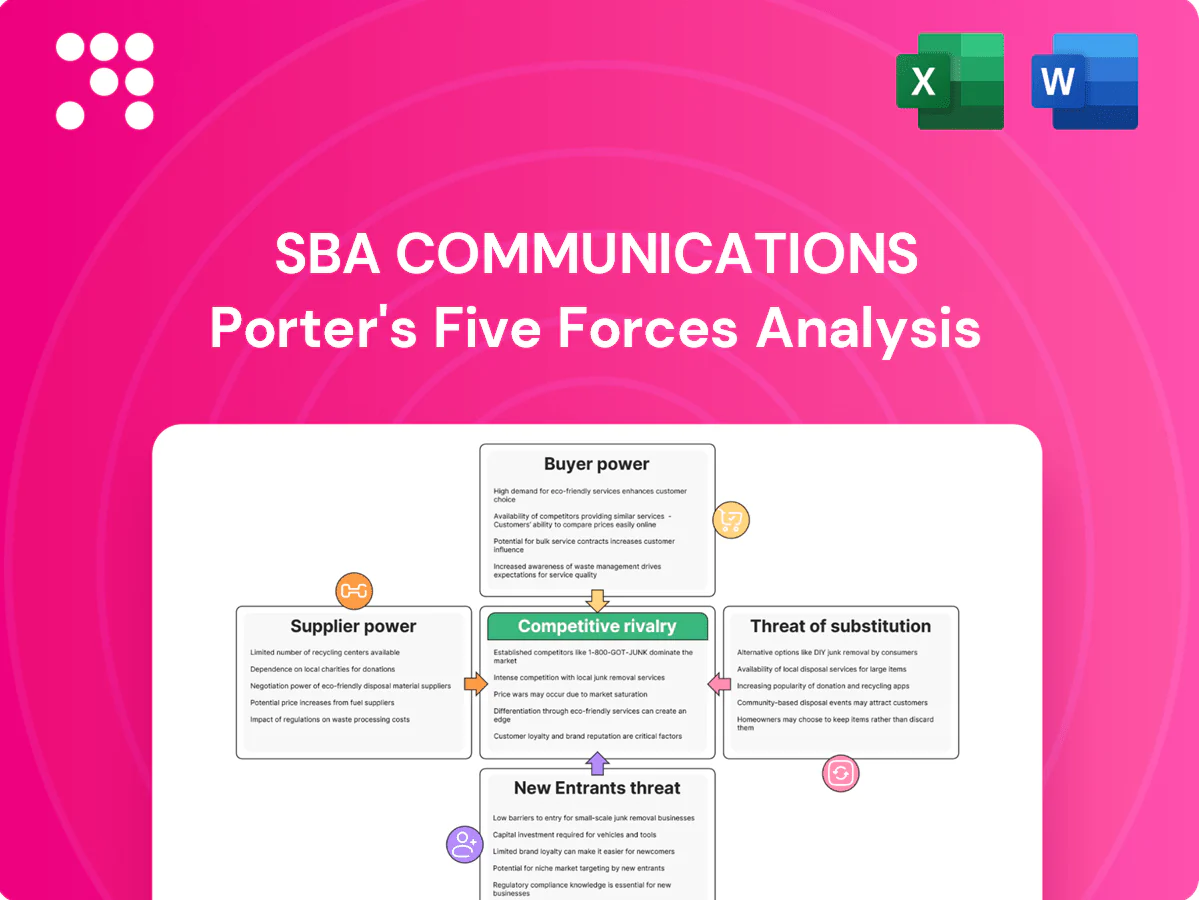

SBA Communications Porter's Five Forces Analysis

Don't Miss the Bigger Picture

SBA Communications faces intense buyer concentration, moderate supplier leverage, rising substitution risks from edge technologies, and barriers that temper new entrants—while rivalry among tower owners remains fierce. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore SBA Communications’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Landowners hold key leases

SBA often leases ground under its towers, making landowners critical suppliers with leverage at renewal or for premium locations. Long lease terms—commonly 25–30 years with extension options—mitigate but do not eliminate hold‑up risk. Portfolio diversification and rights of first refusal help contain rent escalations, which typically follow CPI or 1–3% annual steps. Unique parcels in dense urban areas still command materially higher rates.

Utilities and backhaul are essential

Power and fiber providers often act as local monopolies, giving them pricing and service leverage—industry data in 2024 shows average fiber interconnection lead times of 90–180 days and spot build fees commonly ranging from 50,000 to 250,000 USD per site. SLA reliability (targeting 99.99%+ uptime) directly affects tenant satisfaction and revenue. SBA mitigates risk through redundant feeds and standardized master services agreements, but extended interconnection timeframes and fees still lengthen build cycles and raise capital outlays.

Steel, equipment, and construction

Tower steel, antenna mounts and construction services are sourced from multiple vendors, keeping input pricing competitive. Volume purchasing and standardized designs lower per-site costs—SBA operates over 40,000 sites and reported roughly $3.2 billion revenue in 2024, reinforcing scale. Supply-chain tightness can temporarily raise lead times and prices. SBA’s scale improves bargaining terms versus smaller rivals.

Zoning, permitting, and consultants

Local permitting specialists and legal/zoning consultants materially affect approval speed, creating episodic supplier power as jurisdictions vary; in 2024 U.S. local zoning approvals commonly span from weeks to over a year depending on complexity. Jurisdictional complexity raises switching costs for specialized firms, while SBA Communications' framework agreements and internal permitting expertise reduce external dependency. Nonetheless, contentious municipalities can impose premium fees and multi-month delays.

- episodic supplier power: approval timelines vary widely

- switching costs: high for specialized local firms

- mitigation: framework agreements + internal teams

- risk: premium fees and months-long delays in contentious areas

Technology vendors and maintenance

SBA sources monitoring, lighting and safety systems from niche vendors, where differentiation is modest and pricing power is limited to low-single-digit uplifts; multi-year maintenance contracts (typically 3–5 years) stabilize costs and service levels, while obsolescence cycles (commonly 5–7 years) require periodic, but predictable, upgrades.

- Vendor differentiation: modest — limited pricing power

- Maintenance: multi-year contracts, 3–5 years

- Obsolescence: upgrade cycles ~5–7 years

Renewal landlord leverage; urban rents +20–50%, fiber delay 90–180 days

SBA faces landlord leverage at renewals despite 25–30yr leases; urban parcels can command 20–50% higher rents. Fiber/power have local monopolies: 2024 average fiber interconnect 90–180 days, build fees $50k–$250k. Tower materials competitive; scale (40,000+ sites, ~$3.2B revenue 2024) lowers supplier power.

| Metric | 2024 |

|---|---|

| Sites | 40,000+ |

| Revenue | $3.2B |

| Fiber lead time | 90–180 days |

| Fiber fees | $50k–$250k |

What is included in the product

Tailored Porter's Five Forces analysis for SBA Communications that uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging disruptive threats shaping its tower infrastructure advantage. Ready for investor decks, strategy reports, or academic use and editable for quick customization.

One-sheet Porter's Five Forces for SBA Communications that instantly visualizes strategic pressures with an editable spider chart—customize inputs, swap data or scenarios, and drop straight into pitch decks or Excel dashboards without macros for fast, board-ready decision-making.

Customers Bargaining Power

Carrier concentration is high

Major U.S. carriers—T‑Mobile ~36%, Verizon ~28%, AT&T ~26% of 2024 subscribers—represent a concentrated customer base that gives buyers leverage over SBA’s tower leasing. They commonly negotiate national master lease agreements with standardized economics and escalation terms. Limited alternative tower locations and site scarcity blunt the carriers’ ability to force deep rate cuts. Coverage obligations and speed‑to‑market frequently trump marginal price pressure.

Long-term, escalator leases

Multi-year leases with typical annual escalators of 2–3% blunt buyer leverage mid-term, while contractually stated early termination fees and relocation cost provisions materially raise churn costs. Co-location economics—industry average tenants per tower ~1.5–2—boost incremental cash flow and lock value as additional attachments dilute buyer bargaining. Observable concessions mainly occur at initial siting or during large amendment negotiations.

High switching and relocation costs

Moving antennas risks coverage gaps and network optimization costs; relocations in 2024 typically take weeks to months and often incur tens to hundreds of thousands of dollars in RF planning, re-permitting and crew work. These frictions shrink price sensitivity once a site is live, so carriers prioritize continuity and service quality over marginal rent savings, driving stickier tenant economics for SBA Communications.

Build-to-suit and volume deals

Large build-to-suit and volume commitments let carriers secure better pricing while SBA gains visibility and capital efficiency; in 2024 SBA reported roughly $3.1 billion in revenue and operated about 30,000 sites, underscoring scale in contract negotiation. Volume discounts are partially offset by multi-tenant upside over time as additional tenants raise site-level cash flows, keeping buyer power moderate rather than dominant.

- Carrier leverage: improved pricing via pipeline commitments

- SBA benefit: greater revenue visibility and capital efficiency

- Offset: multi-tenant rent growth reduces discount impact

- Net: buyer power = moderate

Alternative hosts are situational

Carriers can sometimes use rooftops, utility poles or competitor towers to bargain, but substitutes are unevenly available by market and height requirements; SBA owned and managed roughly 32,000 towers worldwide at year-end 2024, concentrating leverage where alternatives are scarce. In suburban and rural areas viable alternatives are sparse, limiting sustained buyer power and making siting constraints a key defense for tower operators.

- Roofs/poles: localized bargaining

- Height limits: reduce substitutes

- Suburban/rural: few alternatives

- 32,000 towers (SBA, 2024): concentrated leverage

Carrier concentration and site scarcity create moderate buyer leverage amid lease stickiness

Concentrated carrier base (T‑Mobile 36%, Verizon 28%, AT&T 26% of 2024 subscribers) gives buyers negotiating leverage but site scarcity, multi-year leases with 2–3% escalators, and relocation frictions limit deep cuts. Multi-tenant upside (avg 1.5–2 tenants/tower) and $3.1B 2024 revenue across ~32,000 towers keep buyer power moderate.

| Metric | 2024 |

|---|---|

| Major carrier share | T‑Mobile 36% / Verizon 28% / AT&T 26% |

| SBA revenue | $3.1B |

| Sites | ~32,000 |

| Tenants/tower | 1.5–2.0 |

What You See Is What You Get

SBA Communications Porter's Five Forces Analysis

This preview is the actual SBA Communications Porter's Five Forces analysis you'll receive—fully formatted and ready for immediate use. It covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. No placeholders or mockups; once you purchase, this exact document is available for instant download. Use it as-is in reports or presentations.

Don't Miss the Bigger Picture

SBA Communications faces intense buyer concentration, moderate supplier leverage, rising substitution risks from edge technologies, and barriers that temper new entrants—while rivalry among tower owners remains fierce. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore SBA Communications’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Landowners hold key leases

SBA often leases ground under its towers, making landowners critical suppliers with leverage at renewal or for premium locations. Long lease terms—commonly 25–30 years with extension options—mitigate but do not eliminate hold‑up risk. Portfolio diversification and rights of first refusal help contain rent escalations, which typically follow CPI or 1–3% annual steps. Unique parcels in dense urban areas still command materially higher rates.

Utilities and backhaul are essential

Power and fiber providers often act as local monopolies, giving them pricing and service leverage—industry data in 2024 shows average fiber interconnection lead times of 90–180 days and spot build fees commonly ranging from 50,000 to 250,000 USD per site. SLA reliability (targeting 99.99%+ uptime) directly affects tenant satisfaction and revenue. SBA mitigates risk through redundant feeds and standardized master services agreements, but extended interconnection timeframes and fees still lengthen build cycles and raise capital outlays.

Steel, equipment, and construction

Tower steel, antenna mounts and construction services are sourced from multiple vendors, keeping input pricing competitive. Volume purchasing and standardized designs lower per-site costs—SBA operates over 40,000 sites and reported roughly $3.2 billion revenue in 2024, reinforcing scale. Supply-chain tightness can temporarily raise lead times and prices. SBA’s scale improves bargaining terms versus smaller rivals.

Zoning, permitting, and consultants

Local permitting specialists and legal/zoning consultants materially affect approval speed, creating episodic supplier power as jurisdictions vary; in 2024 U.S. local zoning approvals commonly span from weeks to over a year depending on complexity. Jurisdictional complexity raises switching costs for specialized firms, while SBA Communications' framework agreements and internal permitting expertise reduce external dependency. Nonetheless, contentious municipalities can impose premium fees and multi-month delays.

- episodic supplier power: approval timelines vary widely

- switching costs: high for specialized local firms

- mitigation: framework agreements + internal teams

- risk: premium fees and months-long delays in contentious areas

Technology vendors and maintenance

SBA sources monitoring, lighting and safety systems from niche vendors, where differentiation is modest and pricing power is limited to low-single-digit uplifts; multi-year maintenance contracts (typically 3–5 years) stabilize costs and service levels, while obsolescence cycles (commonly 5–7 years) require periodic, but predictable, upgrades.

- Vendor differentiation: modest — limited pricing power

- Maintenance: multi-year contracts, 3–5 years

- Obsolescence: upgrade cycles ~5–7 years

Renewal landlord leverage; urban rents +20–50%, fiber delay 90–180 days

SBA faces landlord leverage at renewals despite 25–30yr leases; urban parcels can command 20–50% higher rents. Fiber/power have local monopolies: 2024 average fiber interconnect 90–180 days, build fees $50k–$250k. Tower materials competitive; scale (40,000+ sites, ~$3.2B revenue 2024) lowers supplier power.

| Metric | 2024 |

|---|---|

| Sites | 40,000+ |

| Revenue | $3.2B |

| Fiber lead time | 90–180 days |

| Fiber fees | $50k–$250k |

What is included in the product

Tailored Porter's Five Forces analysis for SBA Communications that uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging disruptive threats shaping its tower infrastructure advantage. Ready for investor decks, strategy reports, or academic use and editable for quick customization.

One-sheet Porter's Five Forces for SBA Communications that instantly visualizes strategic pressures with an editable spider chart—customize inputs, swap data or scenarios, and drop straight into pitch decks or Excel dashboards without macros for fast, board-ready decision-making.

Customers Bargaining Power

Carrier concentration is high

Major U.S. carriers—T‑Mobile ~36%, Verizon ~28%, AT&T ~26% of 2024 subscribers—represent a concentrated customer base that gives buyers leverage over SBA’s tower leasing. They commonly negotiate national master lease agreements with standardized economics and escalation terms. Limited alternative tower locations and site scarcity blunt the carriers’ ability to force deep rate cuts. Coverage obligations and speed‑to‑market frequently trump marginal price pressure.

Long-term, escalator leases

Multi-year leases with typical annual escalators of 2–3% blunt buyer leverage mid-term, while contractually stated early termination fees and relocation cost provisions materially raise churn costs. Co-location economics—industry average tenants per tower ~1.5–2—boost incremental cash flow and lock value as additional attachments dilute buyer bargaining. Observable concessions mainly occur at initial siting or during large amendment negotiations.

High switching and relocation costs

Moving antennas risks coverage gaps and network optimization costs; relocations in 2024 typically take weeks to months and often incur tens to hundreds of thousands of dollars in RF planning, re-permitting and crew work. These frictions shrink price sensitivity once a site is live, so carriers prioritize continuity and service quality over marginal rent savings, driving stickier tenant economics for SBA Communications.

Build-to-suit and volume deals

Large build-to-suit and volume commitments let carriers secure better pricing while SBA gains visibility and capital efficiency; in 2024 SBA reported roughly $3.1 billion in revenue and operated about 30,000 sites, underscoring scale in contract negotiation. Volume discounts are partially offset by multi-tenant upside over time as additional tenants raise site-level cash flows, keeping buyer power moderate rather than dominant.

- Carrier leverage: improved pricing via pipeline commitments

- SBA benefit: greater revenue visibility and capital efficiency

- Offset: multi-tenant rent growth reduces discount impact

- Net: buyer power = moderate

Alternative hosts are situational

Carriers can sometimes use rooftops, utility poles or competitor towers to bargain, but substitutes are unevenly available by market and height requirements; SBA owned and managed roughly 32,000 towers worldwide at year-end 2024, concentrating leverage where alternatives are scarce. In suburban and rural areas viable alternatives are sparse, limiting sustained buyer power and making siting constraints a key defense for tower operators.

- Roofs/poles: localized bargaining

- Height limits: reduce substitutes

- Suburban/rural: few alternatives

- 32,000 towers (SBA, 2024): concentrated leverage

Carrier concentration and site scarcity create moderate buyer leverage amid lease stickiness

Concentrated carrier base (T‑Mobile 36%, Verizon 28%, AT&T 26% of 2024 subscribers) gives buyers negotiating leverage but site scarcity, multi-year leases with 2–3% escalators, and relocation frictions limit deep cuts. Multi-tenant upside (avg 1.5–2 tenants/tower) and $3.1B 2024 revenue across ~32,000 towers keep buyer power moderate.

| Metric | 2024 |

|---|---|

| Major carrier share | T‑Mobile 36% / Verizon 28% / AT&T 26% |

| SBA revenue | $3.1B |

| Sites | ~32,000 |

| Tenants/tower | 1.5–2.0 |

What You See Is What You Get

SBA Communications Porter's Five Forces Analysis

This preview is the actual SBA Communications Porter's Five Forces analysis you'll receive—fully formatted and ready for immediate use. It covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. No placeholders or mockups; once you purchase, this exact document is available for instant download. Use it as-is in reports or presentations.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

SBA Communications faces intense buyer concentration, moderate supplier leverage, rising substitution risks from edge technologies, and barriers that temper new entrants—while rivalry among tower owners remains fierce. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore SBA Communications’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Landowners hold key leases

SBA often leases ground under its towers, making landowners critical suppliers with leverage at renewal or for premium locations. Long lease terms—commonly 25–30 years with extension options—mitigate but do not eliminate hold‑up risk. Portfolio diversification and rights of first refusal help contain rent escalations, which typically follow CPI or 1–3% annual steps. Unique parcels in dense urban areas still command materially higher rates.

Utilities and backhaul are essential

Power and fiber providers often act as local monopolies, giving them pricing and service leverage—industry data in 2024 shows average fiber interconnection lead times of 90–180 days and spot build fees commonly ranging from 50,000 to 250,000 USD per site. SLA reliability (targeting 99.99%+ uptime) directly affects tenant satisfaction and revenue. SBA mitigates risk through redundant feeds and standardized master services agreements, but extended interconnection timeframes and fees still lengthen build cycles and raise capital outlays.

Steel, equipment, and construction

Tower steel, antenna mounts and construction services are sourced from multiple vendors, keeping input pricing competitive. Volume purchasing and standardized designs lower per-site costs—SBA operates over 40,000 sites and reported roughly $3.2 billion revenue in 2024, reinforcing scale. Supply-chain tightness can temporarily raise lead times and prices. SBA’s scale improves bargaining terms versus smaller rivals.

Zoning, permitting, and consultants

Local permitting specialists and legal/zoning consultants materially affect approval speed, creating episodic supplier power as jurisdictions vary; in 2024 U.S. local zoning approvals commonly span from weeks to over a year depending on complexity. Jurisdictional complexity raises switching costs for specialized firms, while SBA Communications' framework agreements and internal permitting expertise reduce external dependency. Nonetheless, contentious municipalities can impose premium fees and multi-month delays.

- episodic supplier power: approval timelines vary widely

- switching costs: high for specialized local firms

- mitigation: framework agreements + internal teams

- risk: premium fees and months-long delays in contentious areas

Technology vendors and maintenance

SBA sources monitoring, lighting and safety systems from niche vendors, where differentiation is modest and pricing power is limited to low-single-digit uplifts; multi-year maintenance contracts (typically 3–5 years) stabilize costs and service levels, while obsolescence cycles (commonly 5–7 years) require periodic, but predictable, upgrades.

- Vendor differentiation: modest — limited pricing power

- Maintenance: multi-year contracts, 3–5 years

- Obsolescence: upgrade cycles ~5–7 years

Renewal landlord leverage; urban rents +20–50%, fiber delay 90–180 days

SBA faces landlord leverage at renewals despite 25–30yr leases; urban parcels can command 20–50% higher rents. Fiber/power have local monopolies: 2024 average fiber interconnect 90–180 days, build fees $50k–$250k. Tower materials competitive; scale (40,000+ sites, ~$3.2B revenue 2024) lowers supplier power.

| Metric | 2024 |

|---|---|

| Sites | 40,000+ |

| Revenue | $3.2B |

| Fiber lead time | 90–180 days |

| Fiber fees | $50k–$250k |

What is included in the product

Tailored Porter's Five Forces analysis for SBA Communications that uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging disruptive threats shaping its tower infrastructure advantage. Ready for investor decks, strategy reports, or academic use and editable for quick customization.

One-sheet Porter's Five Forces for SBA Communications that instantly visualizes strategic pressures with an editable spider chart—customize inputs, swap data or scenarios, and drop straight into pitch decks or Excel dashboards without macros for fast, board-ready decision-making.

Customers Bargaining Power

Carrier concentration is high

Major U.S. carriers—T‑Mobile ~36%, Verizon ~28%, AT&T ~26% of 2024 subscribers—represent a concentrated customer base that gives buyers leverage over SBA’s tower leasing. They commonly negotiate national master lease agreements with standardized economics and escalation terms. Limited alternative tower locations and site scarcity blunt the carriers’ ability to force deep rate cuts. Coverage obligations and speed‑to‑market frequently trump marginal price pressure.

Long-term, escalator leases

Multi-year leases with typical annual escalators of 2–3% blunt buyer leverage mid-term, while contractually stated early termination fees and relocation cost provisions materially raise churn costs. Co-location economics—industry average tenants per tower ~1.5–2—boost incremental cash flow and lock value as additional attachments dilute buyer bargaining. Observable concessions mainly occur at initial siting or during large amendment negotiations.

High switching and relocation costs

Moving antennas risks coverage gaps and network optimization costs; relocations in 2024 typically take weeks to months and often incur tens to hundreds of thousands of dollars in RF planning, re-permitting and crew work. These frictions shrink price sensitivity once a site is live, so carriers prioritize continuity and service quality over marginal rent savings, driving stickier tenant economics for SBA Communications.

Build-to-suit and volume deals

Large build-to-suit and volume commitments let carriers secure better pricing while SBA gains visibility and capital efficiency; in 2024 SBA reported roughly $3.1 billion in revenue and operated about 30,000 sites, underscoring scale in contract negotiation. Volume discounts are partially offset by multi-tenant upside over time as additional tenants raise site-level cash flows, keeping buyer power moderate rather than dominant.

- Carrier leverage: improved pricing via pipeline commitments

- SBA benefit: greater revenue visibility and capital efficiency

- Offset: multi-tenant rent growth reduces discount impact

- Net: buyer power = moderate

Alternative hosts are situational

Carriers can sometimes use rooftops, utility poles or competitor towers to bargain, but substitutes are unevenly available by market and height requirements; SBA owned and managed roughly 32,000 towers worldwide at year-end 2024, concentrating leverage where alternatives are scarce. In suburban and rural areas viable alternatives are sparse, limiting sustained buyer power and making siting constraints a key defense for tower operators.

- Roofs/poles: localized bargaining

- Height limits: reduce substitutes

- Suburban/rural: few alternatives

- 32,000 towers (SBA, 2024): concentrated leverage

Carrier concentration and site scarcity create moderate buyer leverage amid lease stickiness

Concentrated carrier base (T‑Mobile 36%, Verizon 28%, AT&T 26% of 2024 subscribers) gives buyers negotiating leverage but site scarcity, multi-year leases with 2–3% escalators, and relocation frictions limit deep cuts. Multi-tenant upside (avg 1.5–2 tenants/tower) and $3.1B 2024 revenue across ~32,000 towers keep buyer power moderate.

| Metric | 2024 |

|---|---|

| Major carrier share | T‑Mobile 36% / Verizon 28% / AT&T 26% |

| SBA revenue | $3.1B |

| Sites | ~32,000 |

| Tenants/tower | 1.5–2.0 |

What You See Is What You Get

SBA Communications Porter's Five Forces Analysis

This preview is the actual SBA Communications Porter's Five Forces analysis you'll receive—fully formatted and ready for immediate use. It covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. No placeholders or mockups; once you purchase, this exact document is available for instant download. Use it as-is in reports or presentations.