SBI ARUHI Porter's Five Forces Analysis

From Overview to Strategy Blueprint

SBI ARUHI navigates a competitive landscape shaped by moderate buyer power and the persistent threat of substitutes in the housing loan market. Understanding the intensity of these forces is crucial for strategic planning.

The full report reveals the real forces shaping SBI ARUHI’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Funding Sources and Cost of Capital

SBI ARUHI's reliance on the Japan Housing Finance Agency (JHF) for its Flat 35 mortgages significantly shapes supplier bargaining power. The JHF's role as a primary funding source and risk absorber means its terms and conditions directly influence SBI ARUHI's cost of capital for this core product.

The Bank of Japan's monetary policy, especially the anticipated interest rate hikes in 2024 and 2025, exerts considerable influence. These policy shifts impact the overall cost of funds for financial institutions, including SBI ARUHI, affecting their pricing strategies and profitability on loans.

The increasing trend of major banks raising their short-term prime rates in 2024 also contributes to higher funding costs for variable-rate products across the financial sector, indirectly impacting SBI ARUHI's cost of capital.

Technology and Digital Infrastructure Providers

The mortgage sector's growing dependence on advanced digital lending platforms, data analytics, and robust cybersecurity solutions significantly bolsters the bargaining power of technology and digital infrastructure providers. These suppliers are critical for enhancing operational efficiency, improving customer interactions, and ensuring regulatory compliance in an increasingly digitalized environment.

Companies like SBI ARUHI, which adopt a multi-channel strategy, necessitate dependable online services, making their relationships with reliable technology partners indispensable. For instance, the global digital lending market was valued at approximately $10.5 billion in 2023 and is projected to grow substantially, underscoring the critical role and thus the power of its technology enablers.

Data and Information Providers

Data and information providers hold significant bargaining power in the housing finance sector, particularly for companies like SBI ARUHI. Access to accurate and timely data, including credit information, property valuations, and market trends, is absolutely critical for effective risk assessment and strategic decision-making. In 2024, the reliance on sophisticated data analytics for loan underwriting and market analysis only intensified, making these specialized suppliers indispensable.

Specialized data providers and credit bureaus often possess unique or exceptionally comprehensive data sets, which grants them considerable leverage. The quality and accessibility of this information directly influence SBI ARUHI's ability to perform thorough loan underwriting and conduct insightful market analysis. For example, the cost of accessing reliable property valuation data or granular credit scoring information can be a significant input cost, and suppliers with superior data can command higher prices.

Human Capital and Specialized Expertise

The bargaining power of suppliers in the context of human capital is significant for SBI ARUHI, especially given the specialized nature of the housing loan market. Skilled professionals in finance, technology, risk management, and customer service are essential for maintaining operational efficiency and delivering high-quality services. For instance, a shortage of experienced personnel in areas like advanced fintech solutions, which are increasingly important for loan processing and customer engagement, can empower these individuals and increase their leverage.

The availability of specialized talent, particularly in niche segments like Flat 35 loans, directly impacts SBI ARUHI's ability to innovate and compete. If there's a limited pool of professionals with proven track records in these specific areas, their ability to command higher salaries and better benefits grows. This was evident in early 2024, where reports indicated a heightened demand for cybersecurity experts within the financial sector, leading to salary increases of up to 15% for those with specialized skills.

- Talent Scarcity: Shortages in critical skill sets, such as data analytics and AI specialists in finance, can significantly boost supplier (employee) bargaining power.

- Industry Demand: High demand for financial professionals with expertise in areas like mortgage-backed securities or regulatory compliance can lead to increased wage pressures.

- Specialized Knowledge: Employees possessing unique knowledge of specific housing loan products or regulatory frameworks, like Flat 35 in Japan, hold considerable leverage.

- Employee Retention: Companies like SBI ARUHI face increased costs and operational disruption if they cannot retain key talent, further strengthening employee bargaining power.

Regulatory Bodies and Policy Makers

Regulatory bodies and policymakers exert significant influence over SBI ARUHI, acting as de facto suppliers by shaping the environment for its core business, particularly Flat 35 loans. Agencies like the Japan Housing Finance Agency and the Ministry of Land, Infrastructure, Transport and Tourism, alongside the Bank of Japan, set the operational parameters and product guidelines that SBI ARUHI must adhere to. For instance, policy shifts concerning preferential interest rates for energy-efficient housing directly impact the attractiveness and viability of specific loan products.

These entities' mandates can drastically alter market dynamics and SBI ARUHI's competitive standing. Changes in lending requirements or the introduction of new governmental housing initiatives can necessitate rapid adaptation of business models and product portfolios. The Bank of Japan's monetary policy, including interest rate decisions, is a critical factor influencing the cost of funds and, consequently, the pricing of mortgages offered by SBI ARUHI.

- Governmental influence: The Japan Housing Finance Agency and the Ministry of Land, Infrastructure, Transport and Tourism dictate product standards and market access for mortgage providers like SBI ARUHI.

- Policy impact on products: Regulatory changes, such as incentives for energy-efficient homes, directly affect the design and competitiveness of mortgage offerings.

- Monetary policy relevance: The Bank of Japan's interest rate decisions significantly influence SBI ARUHI's funding costs and lending rates.

Supplier Power Shapes Mortgage Lender's Future

The bargaining power of suppliers for SBI ARUHI is significantly influenced by its reliance on the Japan Housing Finance Agency (JHF) for Flat 35 mortgages, as the JHF dictates crucial terms and funding conditions. Furthermore, the Bank of Japan's monetary policy, including anticipated interest rate hikes in 2024 and 2025, directly impacts SBI ARUHI's cost of capital and lending rates.

Technology and data providers hold substantial sway due to the increasing digitalization of the mortgage sector, where advanced platforms and accurate data are vital for operational efficiency and risk assessment. Specialized talent in finance and technology also commands significant leverage, especially when specific expertise, like in fintech or cybersecurity, is scarce, leading to higher recruitment and retention costs for SBI ARUHI.

| Supplier Type | Influence on SBI ARUHI | Key Factors |

|---|---|---|

| Japan Housing Finance Agency (JHF) | High | Funding source, product terms for Flat 35 |

| Bank of Japan | High | Monetary policy, interest rates, cost of funds |

| Technology Providers | Medium to High | Digital platforms, data analytics, cybersecurity |

| Data & Information Providers | High | Credit data, property valuations, market trends |

| Specialized Talent | Medium to High | Fintech, risk management, cybersecurity expertise |

What is included in the product

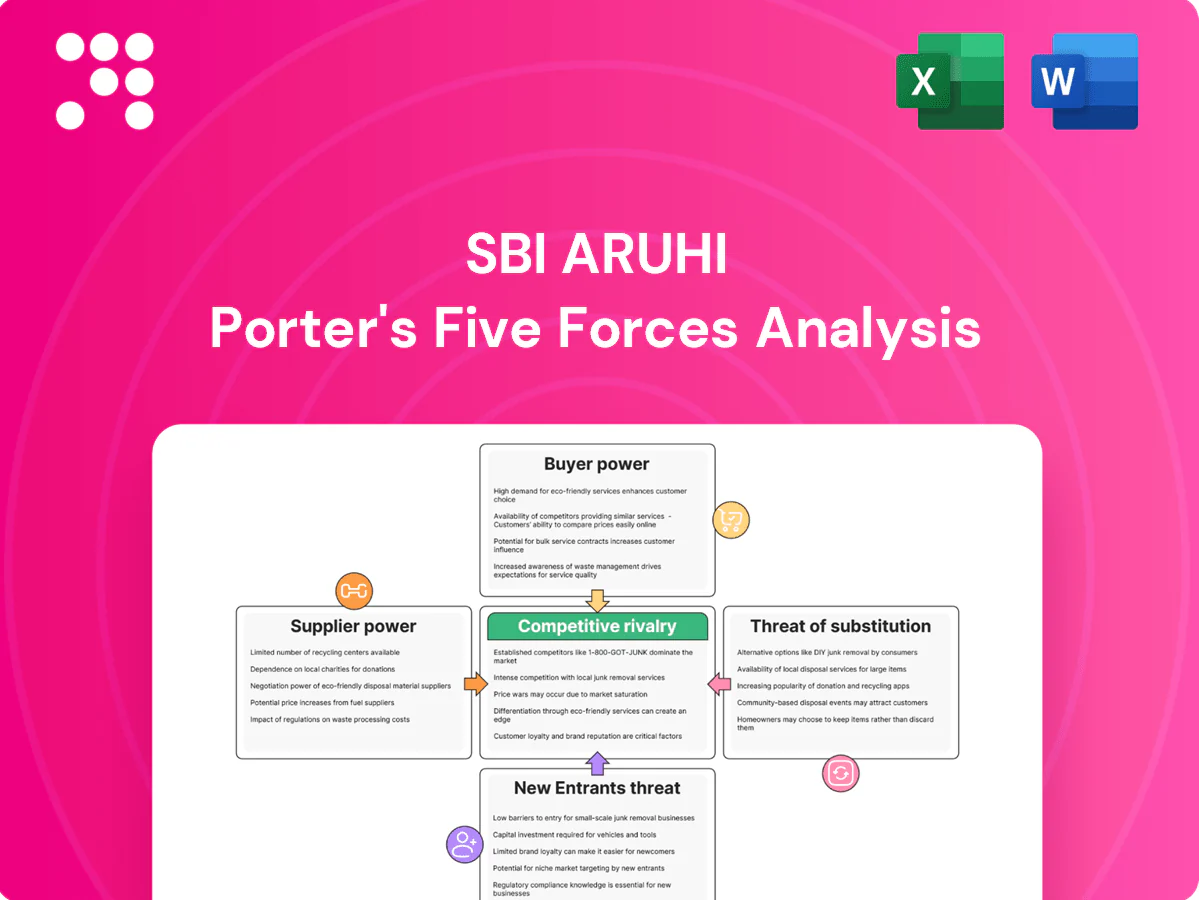

Tailored exclusively for SBI ARUHI, this analysis dissects the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes on its market position.

Instantly visualize the competitive landscape for SBI ARUHI with a dynamic Porter's Five Forces analysis, simplifying complex market pressures for strategic clarity.

Customers Bargaining Power

High Price Sensitivity and Interest Rate Awareness

Japanese mortgage customers, particularly with the Bank of Japan's recent interest rate adjustments, are acutely aware of loan interest rate fluctuations. This heightened sensitivity means they actively compare offerings, looking for the best deals. For instance, in early 2024, as fixed rates for products like Flat 35 began to climb, many borrowers explored alternatives to secure predictable payments.

The prevalence of floating-rate mortgages in Japan amplifies this customer power. When interest rates rise, borrowers on these plans face increased monthly payments, making them more inclined to refinance or switch lenders if a better fixed-rate option emerges. This dynamic forces lenders to remain competitive to retain their customer base.

Abundance of Alternatives and Low Switching Costs

The Japanese mortgage market presents customers with a wide array of choices. Major banks, regional institutions, credit unions, and online lenders all compete, offering diverse mortgage products. This abundance means borrowers can readily find options that suit their needs.

Switching lenders, often through refinancing, incurs some administrative fees. However, these costs are generally minor when weighed against the potential savings from securing a lower interest rate. For instance, a 0.5% reduction on a ¥30 million mortgage over 30 years could save a borrower millions of yen over the loan's life.

This ease of comparison and relatively low switching cost significantly bolsters customer bargaining power. Borrowers can leverage the competitive landscape to negotiate better terms or simply move to a provider offering a more attractive deal, putting pressure on lenders to maintain competitive pricing and service.

Increased Information Transparency

Increased information transparency significantly bolsters customer bargaining power. Online platforms and mortgage brokers now provide readily available comparisons of interest rates, fees, and loan terms from various lenders. This accessibility empowers customers, reducing the traditional information gap and enabling them to identify the most favorable offers.

In 2024, the digital mortgage market continued its expansion, with an increasing percentage of consumers utilizing online tools for initial research and comparison. For instance, data from industry reports indicated that over 60% of mortgage shoppers actively researched rates online before engaging with a lender. This trend directly pressures lenders like SBI ARUHI to maintain competitive pricing and transparent fee structures to attract and retain customers.

Demographic Shifts and Evolving Needs

Changes in borrower demographics are significantly impacting the housing loan market. For instance, an aging population in Japan, where SBI ARUHI operates, is showing increased interest in financial products like reverse mortgages to supplement retirement income. Concurrently, younger demographics are increasingly demanding digital-first experiences, prioritizing streamlined online application processes for home loans.

SBI ARUHI's strategic focus on products like Flat 35, a government-backed housing loan scheme, and its multi-channel service approach, which includes both physical branches and online platforms, are crucial for adapting to these shifts. The company must remain agile to cater to these evolving customer preferences, ensuring it can maintain and grow its market share in a dynamic environment.

- Aging Population: Japan's population is aging rapidly, with the proportion of those aged 65 and over projected to reach 31.3% by 2025, increasing demand for financial solutions tailored to seniors.

- Digital Adoption: A growing segment of the population, particularly those under 40, prefers digital channels for financial transactions, including loan applications, with mobile banking usage rising steadily.

- Housing Preferences: There's a noticeable trend towards purchasing existing homes rather than custom-built properties, which can influence the types of mortgage products and associated services customers seek.

Government Incentives and Programs

Government initiatives, such as tax incentives for energy-efficient homes and preferential interest rate measures like those for Flat 35, significantly bolster customer bargaining power. These programs effectively lower the overall cost of homeownership for eligible buyers, making them more discerning about loan terms and property features. For instance, in 2024, the Japanese government continued to support housing market stability through various subsidies and tax breaks, directly impacting affordability and consumer choice.

These government programs can directly influence customer choice by making certain loan types or housing features more attractive. When borrowers can access lower interest rates or receive tax credits, their overall financial burden is reduced, thereby increasing their leverage in negotiations with lenders and developers. This enhanced financial capacity allows customers to demand more favorable terms, potentially driving down prices or improving service quality.

The impact of these incentives is evident in the increased demand for specific housing segments. For example, a rise in government subsidies for green building technologies in 2024 likely led to a surge in demand for eco-friendly homes, giving buyers in that segment greater negotiating power. Customers who qualify for these benefits, such as preferential interest rates on mortgages, are empowered to seek out the best deals, knowing they have a financial advantage.

- Government Support: Initiatives like tax incentives for energy-efficient homes and preferential interest rates for programs such as Flat 35 empower customers.

- Influence on Choice: These programs can sway customer decisions towards specific loan types or housing features, increasing demand.

- Increased Leverage: Borrowers meeting specific criteria often receive lower rates, enhancing their bargaining position with financial institutions.

- Market Impact: In 2024, continued government support for housing affordability in markets like Japan directly influenced consumer spending and negotiation power.

Japanese Mortgage Borrowers Wield Significant Bargaining Power

Customers in the Japanese mortgage market possess significant bargaining power, largely driven by heightened price sensitivity and the availability of numerous competing lenders. The ease with which borrowers can compare offerings, especially with the proliferation of online tools and information transparency, allows them to readily identify and pursue the most advantageous loan terms. This competitive environment, coupled with relatively low switching costs, compels financial institutions to offer attractive rates and services to retain their clientele.

The prevalence of floating-rate mortgages in Japan means that borrowers are keenly aware of interest rate shifts, actively seeking to refinance or switch to more favorable fixed-rate options when rates rise. For instance, in early 2024, as fixed rates for products like Flat 35 saw increases, many borrowers explored alternative lenders to secure predictable payments, demonstrating their power to influence market pricing.

Government incentives, such as tax breaks for energy-efficient homes and preferential interest rates for programs like Flat 35, further empower customers. These initiatives reduce the overall cost of homeownership, enabling buyers to be more selective and negotiate better terms, as seen in 2024 when continued government support for housing affordability directly impacted consumer negotiation power.

| Factor | Impact on Customer Bargaining Power | 2024 Data/Trend Example |

|---|---|---|

| Price Sensitivity & Rate Awareness | High; customers actively seek lower interest rates. | Increased comparison of Flat 35 rates in early 2024 due to upward rate adjustments. |

| Availability of Lenders & Product Variety | High; numerous banks, credit unions, and online lenders offer diverse mortgage products. | Continued expansion of digital mortgage platforms offering wide comparisons. |

| Information Transparency & Digital Tools | High; online platforms provide easy comparison of rates and fees. | Over 60% of mortgage shoppers researched rates online in 2024 before engaging lenders. |

| Switching Costs | Low; administrative fees are generally minor compared to potential savings. | Potential savings of millions of yen on a ¥30 million mortgage for a 0.5% rate reduction. |

| Government Incentives (e.g., Flat 35) | High; subsidies and tax breaks lower overall cost, increasing leverage. | Continued government support for housing affordability in 2024 boosted consumer negotiation power. |

Preview Before You Purchase

SBI ARUHI Porter's Five Forces Analysis

The document you see is your deliverable. It’s ready for immediate use—no customization or setup required. This comprehensive Porter's Five Forces analysis of SBI ARUHI delves into the competitive landscape, evaluating the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the industry. Understanding these forces is crucial for strategic decision-making and identifying opportunities for SBI ARUHI to enhance its competitive position.

From Overview to Strategy Blueprint

SBI ARUHI navigates a competitive landscape shaped by moderate buyer power and the persistent threat of substitutes in the housing loan market. Understanding the intensity of these forces is crucial for strategic planning.

The full report reveals the real forces shaping SBI ARUHI’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Funding Sources and Cost of Capital

SBI ARUHI's reliance on the Japan Housing Finance Agency (JHF) for its Flat 35 mortgages significantly shapes supplier bargaining power. The JHF's role as a primary funding source and risk absorber means its terms and conditions directly influence SBI ARUHI's cost of capital for this core product.

The Bank of Japan's monetary policy, especially the anticipated interest rate hikes in 2024 and 2025, exerts considerable influence. These policy shifts impact the overall cost of funds for financial institutions, including SBI ARUHI, affecting their pricing strategies and profitability on loans.

The increasing trend of major banks raising their short-term prime rates in 2024 also contributes to higher funding costs for variable-rate products across the financial sector, indirectly impacting SBI ARUHI's cost of capital.

Technology and Digital Infrastructure Providers

The mortgage sector's growing dependence on advanced digital lending platforms, data analytics, and robust cybersecurity solutions significantly bolsters the bargaining power of technology and digital infrastructure providers. These suppliers are critical for enhancing operational efficiency, improving customer interactions, and ensuring regulatory compliance in an increasingly digitalized environment.

Companies like SBI ARUHI, which adopt a multi-channel strategy, necessitate dependable online services, making their relationships with reliable technology partners indispensable. For instance, the global digital lending market was valued at approximately $10.5 billion in 2023 and is projected to grow substantially, underscoring the critical role and thus the power of its technology enablers.

Data and Information Providers

Data and information providers hold significant bargaining power in the housing finance sector, particularly for companies like SBI ARUHI. Access to accurate and timely data, including credit information, property valuations, and market trends, is absolutely critical for effective risk assessment and strategic decision-making. In 2024, the reliance on sophisticated data analytics for loan underwriting and market analysis only intensified, making these specialized suppliers indispensable.

Specialized data providers and credit bureaus often possess unique or exceptionally comprehensive data sets, which grants them considerable leverage. The quality and accessibility of this information directly influence SBI ARUHI's ability to perform thorough loan underwriting and conduct insightful market analysis. For example, the cost of accessing reliable property valuation data or granular credit scoring information can be a significant input cost, and suppliers with superior data can command higher prices.

Human Capital and Specialized Expertise

The bargaining power of suppliers in the context of human capital is significant for SBI ARUHI, especially given the specialized nature of the housing loan market. Skilled professionals in finance, technology, risk management, and customer service are essential for maintaining operational efficiency and delivering high-quality services. For instance, a shortage of experienced personnel in areas like advanced fintech solutions, which are increasingly important for loan processing and customer engagement, can empower these individuals and increase their leverage.

The availability of specialized talent, particularly in niche segments like Flat 35 loans, directly impacts SBI ARUHI's ability to innovate and compete. If there's a limited pool of professionals with proven track records in these specific areas, their ability to command higher salaries and better benefits grows. This was evident in early 2024, where reports indicated a heightened demand for cybersecurity experts within the financial sector, leading to salary increases of up to 15% for those with specialized skills.

- Talent Scarcity: Shortages in critical skill sets, such as data analytics and AI specialists in finance, can significantly boost supplier (employee) bargaining power.

- Industry Demand: High demand for financial professionals with expertise in areas like mortgage-backed securities or regulatory compliance can lead to increased wage pressures.

- Specialized Knowledge: Employees possessing unique knowledge of specific housing loan products or regulatory frameworks, like Flat 35 in Japan, hold considerable leverage.

- Employee Retention: Companies like SBI ARUHI face increased costs and operational disruption if they cannot retain key talent, further strengthening employee bargaining power.

Regulatory Bodies and Policy Makers

Regulatory bodies and policymakers exert significant influence over SBI ARUHI, acting as de facto suppliers by shaping the environment for its core business, particularly Flat 35 loans. Agencies like the Japan Housing Finance Agency and the Ministry of Land, Infrastructure, Transport and Tourism, alongside the Bank of Japan, set the operational parameters and product guidelines that SBI ARUHI must adhere to. For instance, policy shifts concerning preferential interest rates for energy-efficient housing directly impact the attractiveness and viability of specific loan products.

These entities' mandates can drastically alter market dynamics and SBI ARUHI's competitive standing. Changes in lending requirements or the introduction of new governmental housing initiatives can necessitate rapid adaptation of business models and product portfolios. The Bank of Japan's monetary policy, including interest rate decisions, is a critical factor influencing the cost of funds and, consequently, the pricing of mortgages offered by SBI ARUHI.

- Governmental influence: The Japan Housing Finance Agency and the Ministry of Land, Infrastructure, Transport and Tourism dictate product standards and market access for mortgage providers like SBI ARUHI.

- Policy impact on products: Regulatory changes, such as incentives for energy-efficient homes, directly affect the design and competitiveness of mortgage offerings.

- Monetary policy relevance: The Bank of Japan's interest rate decisions significantly influence SBI ARUHI's funding costs and lending rates.

Supplier Power Shapes Mortgage Lender's Future

The bargaining power of suppliers for SBI ARUHI is significantly influenced by its reliance on the Japan Housing Finance Agency (JHF) for Flat 35 mortgages, as the JHF dictates crucial terms and funding conditions. Furthermore, the Bank of Japan's monetary policy, including anticipated interest rate hikes in 2024 and 2025, directly impacts SBI ARUHI's cost of capital and lending rates.

Technology and data providers hold substantial sway due to the increasing digitalization of the mortgage sector, where advanced platforms and accurate data are vital for operational efficiency and risk assessment. Specialized talent in finance and technology also commands significant leverage, especially when specific expertise, like in fintech or cybersecurity, is scarce, leading to higher recruitment and retention costs for SBI ARUHI.

| Supplier Type | Influence on SBI ARUHI | Key Factors |

|---|---|---|

| Japan Housing Finance Agency (JHF) | High | Funding source, product terms for Flat 35 |

| Bank of Japan | High | Monetary policy, interest rates, cost of funds |

| Technology Providers | Medium to High | Digital platforms, data analytics, cybersecurity |

| Data & Information Providers | High | Credit data, property valuations, market trends |

| Specialized Talent | Medium to High | Fintech, risk management, cybersecurity expertise |

What is included in the product

Tailored exclusively for SBI ARUHI, this analysis dissects the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes on its market position.

Instantly visualize the competitive landscape for SBI ARUHI with a dynamic Porter's Five Forces analysis, simplifying complex market pressures for strategic clarity.

Customers Bargaining Power

High Price Sensitivity and Interest Rate Awareness

Japanese mortgage customers, particularly with the Bank of Japan's recent interest rate adjustments, are acutely aware of loan interest rate fluctuations. This heightened sensitivity means they actively compare offerings, looking for the best deals. For instance, in early 2024, as fixed rates for products like Flat 35 began to climb, many borrowers explored alternatives to secure predictable payments.

The prevalence of floating-rate mortgages in Japan amplifies this customer power. When interest rates rise, borrowers on these plans face increased monthly payments, making them more inclined to refinance or switch lenders if a better fixed-rate option emerges. This dynamic forces lenders to remain competitive to retain their customer base.

Abundance of Alternatives and Low Switching Costs

The Japanese mortgage market presents customers with a wide array of choices. Major banks, regional institutions, credit unions, and online lenders all compete, offering diverse mortgage products. This abundance means borrowers can readily find options that suit their needs.

Switching lenders, often through refinancing, incurs some administrative fees. However, these costs are generally minor when weighed against the potential savings from securing a lower interest rate. For instance, a 0.5% reduction on a ¥30 million mortgage over 30 years could save a borrower millions of yen over the loan's life.

This ease of comparison and relatively low switching cost significantly bolsters customer bargaining power. Borrowers can leverage the competitive landscape to negotiate better terms or simply move to a provider offering a more attractive deal, putting pressure on lenders to maintain competitive pricing and service.

Increased Information Transparency

Increased information transparency significantly bolsters customer bargaining power. Online platforms and mortgage brokers now provide readily available comparisons of interest rates, fees, and loan terms from various lenders. This accessibility empowers customers, reducing the traditional information gap and enabling them to identify the most favorable offers.

In 2024, the digital mortgage market continued its expansion, with an increasing percentage of consumers utilizing online tools for initial research and comparison. For instance, data from industry reports indicated that over 60% of mortgage shoppers actively researched rates online before engaging with a lender. This trend directly pressures lenders like SBI ARUHI to maintain competitive pricing and transparent fee structures to attract and retain customers.

Demographic Shifts and Evolving Needs

Changes in borrower demographics are significantly impacting the housing loan market. For instance, an aging population in Japan, where SBI ARUHI operates, is showing increased interest in financial products like reverse mortgages to supplement retirement income. Concurrently, younger demographics are increasingly demanding digital-first experiences, prioritizing streamlined online application processes for home loans.

SBI ARUHI's strategic focus on products like Flat 35, a government-backed housing loan scheme, and its multi-channel service approach, which includes both physical branches and online platforms, are crucial for adapting to these shifts. The company must remain agile to cater to these evolving customer preferences, ensuring it can maintain and grow its market share in a dynamic environment.

- Aging Population: Japan's population is aging rapidly, with the proportion of those aged 65 and over projected to reach 31.3% by 2025, increasing demand for financial solutions tailored to seniors.

- Digital Adoption: A growing segment of the population, particularly those under 40, prefers digital channels for financial transactions, including loan applications, with mobile banking usage rising steadily.

- Housing Preferences: There's a noticeable trend towards purchasing existing homes rather than custom-built properties, which can influence the types of mortgage products and associated services customers seek.

Government Incentives and Programs

Government initiatives, such as tax incentives for energy-efficient homes and preferential interest rate measures like those for Flat 35, significantly bolster customer bargaining power. These programs effectively lower the overall cost of homeownership for eligible buyers, making them more discerning about loan terms and property features. For instance, in 2024, the Japanese government continued to support housing market stability through various subsidies and tax breaks, directly impacting affordability and consumer choice.

These government programs can directly influence customer choice by making certain loan types or housing features more attractive. When borrowers can access lower interest rates or receive tax credits, their overall financial burden is reduced, thereby increasing their leverage in negotiations with lenders and developers. This enhanced financial capacity allows customers to demand more favorable terms, potentially driving down prices or improving service quality.

The impact of these incentives is evident in the increased demand for specific housing segments. For example, a rise in government subsidies for green building technologies in 2024 likely led to a surge in demand for eco-friendly homes, giving buyers in that segment greater negotiating power. Customers who qualify for these benefits, such as preferential interest rates on mortgages, are empowered to seek out the best deals, knowing they have a financial advantage.

- Government Support: Initiatives like tax incentives for energy-efficient homes and preferential interest rates for programs such as Flat 35 empower customers.

- Influence on Choice: These programs can sway customer decisions towards specific loan types or housing features, increasing demand.

- Increased Leverage: Borrowers meeting specific criteria often receive lower rates, enhancing their bargaining position with financial institutions.

- Market Impact: In 2024, continued government support for housing affordability in markets like Japan directly influenced consumer spending and negotiation power.

Japanese Mortgage Borrowers Wield Significant Bargaining Power

Customers in the Japanese mortgage market possess significant bargaining power, largely driven by heightened price sensitivity and the availability of numerous competing lenders. The ease with which borrowers can compare offerings, especially with the proliferation of online tools and information transparency, allows them to readily identify and pursue the most advantageous loan terms. This competitive environment, coupled with relatively low switching costs, compels financial institutions to offer attractive rates and services to retain their clientele.

The prevalence of floating-rate mortgages in Japan means that borrowers are keenly aware of interest rate shifts, actively seeking to refinance or switch to more favorable fixed-rate options when rates rise. For instance, in early 2024, as fixed rates for products like Flat 35 saw increases, many borrowers explored alternative lenders to secure predictable payments, demonstrating their power to influence market pricing.

Government incentives, such as tax breaks for energy-efficient homes and preferential interest rates for programs like Flat 35, further empower customers. These initiatives reduce the overall cost of homeownership, enabling buyers to be more selective and negotiate better terms, as seen in 2024 when continued government support for housing affordability directly impacted consumer negotiation power.

| Factor | Impact on Customer Bargaining Power | 2024 Data/Trend Example |

|---|---|---|

| Price Sensitivity & Rate Awareness | High; customers actively seek lower interest rates. | Increased comparison of Flat 35 rates in early 2024 due to upward rate adjustments. |

| Availability of Lenders & Product Variety | High; numerous banks, credit unions, and online lenders offer diverse mortgage products. | Continued expansion of digital mortgage platforms offering wide comparisons. |

| Information Transparency & Digital Tools | High; online platforms provide easy comparison of rates and fees. | Over 60% of mortgage shoppers researched rates online in 2024 before engaging lenders. |

| Switching Costs | Low; administrative fees are generally minor compared to potential savings. | Potential savings of millions of yen on a ¥30 million mortgage for a 0.5% rate reduction. |

| Government Incentives (e.g., Flat 35) | High; subsidies and tax breaks lower overall cost, increasing leverage. | Continued government support for housing affordability in 2024 boosted consumer negotiation power. |

Preview Before You Purchase

SBI ARUHI Porter's Five Forces Analysis

The document you see is your deliverable. It’s ready for immediate use—no customization or setup required. This comprehensive Porter's Five Forces analysis of SBI ARUHI delves into the competitive landscape, evaluating the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the industry. Understanding these forces is crucial for strategic decision-making and identifying opportunities for SBI ARUHI to enhance its competitive position.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

SBI ARUHI navigates a competitive landscape shaped by moderate buyer power and the persistent threat of substitutes in the housing loan market. Understanding the intensity of these forces is crucial for strategic planning.

The full report reveals the real forces shaping SBI ARUHI’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Funding Sources and Cost of Capital

SBI ARUHI's reliance on the Japan Housing Finance Agency (JHF) for its Flat 35 mortgages significantly shapes supplier bargaining power. The JHF's role as a primary funding source and risk absorber means its terms and conditions directly influence SBI ARUHI's cost of capital for this core product.

The Bank of Japan's monetary policy, especially the anticipated interest rate hikes in 2024 and 2025, exerts considerable influence. These policy shifts impact the overall cost of funds for financial institutions, including SBI ARUHI, affecting their pricing strategies and profitability on loans.

The increasing trend of major banks raising their short-term prime rates in 2024 also contributes to higher funding costs for variable-rate products across the financial sector, indirectly impacting SBI ARUHI's cost of capital.

Technology and Digital Infrastructure Providers

The mortgage sector's growing dependence on advanced digital lending platforms, data analytics, and robust cybersecurity solutions significantly bolsters the bargaining power of technology and digital infrastructure providers. These suppliers are critical for enhancing operational efficiency, improving customer interactions, and ensuring regulatory compliance in an increasingly digitalized environment.

Companies like SBI ARUHI, which adopt a multi-channel strategy, necessitate dependable online services, making their relationships with reliable technology partners indispensable. For instance, the global digital lending market was valued at approximately $10.5 billion in 2023 and is projected to grow substantially, underscoring the critical role and thus the power of its technology enablers.

Data and Information Providers

Data and information providers hold significant bargaining power in the housing finance sector, particularly for companies like SBI ARUHI. Access to accurate and timely data, including credit information, property valuations, and market trends, is absolutely critical for effective risk assessment and strategic decision-making. In 2024, the reliance on sophisticated data analytics for loan underwriting and market analysis only intensified, making these specialized suppliers indispensable.

Specialized data providers and credit bureaus often possess unique or exceptionally comprehensive data sets, which grants them considerable leverage. The quality and accessibility of this information directly influence SBI ARUHI's ability to perform thorough loan underwriting and conduct insightful market analysis. For example, the cost of accessing reliable property valuation data or granular credit scoring information can be a significant input cost, and suppliers with superior data can command higher prices.

Human Capital and Specialized Expertise

The bargaining power of suppliers in the context of human capital is significant for SBI ARUHI, especially given the specialized nature of the housing loan market. Skilled professionals in finance, technology, risk management, and customer service are essential for maintaining operational efficiency and delivering high-quality services. For instance, a shortage of experienced personnel in areas like advanced fintech solutions, which are increasingly important for loan processing and customer engagement, can empower these individuals and increase their leverage.

The availability of specialized talent, particularly in niche segments like Flat 35 loans, directly impacts SBI ARUHI's ability to innovate and compete. If there's a limited pool of professionals with proven track records in these specific areas, their ability to command higher salaries and better benefits grows. This was evident in early 2024, where reports indicated a heightened demand for cybersecurity experts within the financial sector, leading to salary increases of up to 15% for those with specialized skills.

- Talent Scarcity: Shortages in critical skill sets, such as data analytics and AI specialists in finance, can significantly boost supplier (employee) bargaining power.

- Industry Demand: High demand for financial professionals with expertise in areas like mortgage-backed securities or regulatory compliance can lead to increased wage pressures.

- Specialized Knowledge: Employees possessing unique knowledge of specific housing loan products or regulatory frameworks, like Flat 35 in Japan, hold considerable leverage.

- Employee Retention: Companies like SBI ARUHI face increased costs and operational disruption if they cannot retain key talent, further strengthening employee bargaining power.

Regulatory Bodies and Policy Makers

Regulatory bodies and policymakers exert significant influence over SBI ARUHI, acting as de facto suppliers by shaping the environment for its core business, particularly Flat 35 loans. Agencies like the Japan Housing Finance Agency and the Ministry of Land, Infrastructure, Transport and Tourism, alongside the Bank of Japan, set the operational parameters and product guidelines that SBI ARUHI must adhere to. For instance, policy shifts concerning preferential interest rates for energy-efficient housing directly impact the attractiveness and viability of specific loan products.

These entities' mandates can drastically alter market dynamics and SBI ARUHI's competitive standing. Changes in lending requirements or the introduction of new governmental housing initiatives can necessitate rapid adaptation of business models and product portfolios. The Bank of Japan's monetary policy, including interest rate decisions, is a critical factor influencing the cost of funds and, consequently, the pricing of mortgages offered by SBI ARUHI.

- Governmental influence: The Japan Housing Finance Agency and the Ministry of Land, Infrastructure, Transport and Tourism dictate product standards and market access for mortgage providers like SBI ARUHI.

- Policy impact on products: Regulatory changes, such as incentives for energy-efficient homes, directly affect the design and competitiveness of mortgage offerings.

- Monetary policy relevance: The Bank of Japan's interest rate decisions significantly influence SBI ARUHI's funding costs and lending rates.

Supplier Power Shapes Mortgage Lender's Future

The bargaining power of suppliers for SBI ARUHI is significantly influenced by its reliance on the Japan Housing Finance Agency (JHF) for Flat 35 mortgages, as the JHF dictates crucial terms and funding conditions. Furthermore, the Bank of Japan's monetary policy, including anticipated interest rate hikes in 2024 and 2025, directly impacts SBI ARUHI's cost of capital and lending rates.

Technology and data providers hold substantial sway due to the increasing digitalization of the mortgage sector, where advanced platforms and accurate data are vital for operational efficiency and risk assessment. Specialized talent in finance and technology also commands significant leverage, especially when specific expertise, like in fintech or cybersecurity, is scarce, leading to higher recruitment and retention costs for SBI ARUHI.

| Supplier Type | Influence on SBI ARUHI | Key Factors |

|---|---|---|

| Japan Housing Finance Agency (JHF) | High | Funding source, product terms for Flat 35 |

| Bank of Japan | High | Monetary policy, interest rates, cost of funds |

| Technology Providers | Medium to High | Digital platforms, data analytics, cybersecurity |

| Data & Information Providers | High | Credit data, property valuations, market trends |

| Specialized Talent | Medium to High | Fintech, risk management, cybersecurity expertise |

What is included in the product

Tailored exclusively for SBI ARUHI, this analysis dissects the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes on its market position.

Instantly visualize the competitive landscape for SBI ARUHI with a dynamic Porter's Five Forces analysis, simplifying complex market pressures for strategic clarity.

Customers Bargaining Power

High Price Sensitivity and Interest Rate Awareness

Japanese mortgage customers, particularly with the Bank of Japan's recent interest rate adjustments, are acutely aware of loan interest rate fluctuations. This heightened sensitivity means they actively compare offerings, looking for the best deals. For instance, in early 2024, as fixed rates for products like Flat 35 began to climb, many borrowers explored alternatives to secure predictable payments.

The prevalence of floating-rate mortgages in Japan amplifies this customer power. When interest rates rise, borrowers on these plans face increased monthly payments, making them more inclined to refinance or switch lenders if a better fixed-rate option emerges. This dynamic forces lenders to remain competitive to retain their customer base.

Abundance of Alternatives and Low Switching Costs

The Japanese mortgage market presents customers with a wide array of choices. Major banks, regional institutions, credit unions, and online lenders all compete, offering diverse mortgage products. This abundance means borrowers can readily find options that suit their needs.

Switching lenders, often through refinancing, incurs some administrative fees. However, these costs are generally minor when weighed against the potential savings from securing a lower interest rate. For instance, a 0.5% reduction on a ¥30 million mortgage over 30 years could save a borrower millions of yen over the loan's life.

This ease of comparison and relatively low switching cost significantly bolsters customer bargaining power. Borrowers can leverage the competitive landscape to negotiate better terms or simply move to a provider offering a more attractive deal, putting pressure on lenders to maintain competitive pricing and service.

Increased Information Transparency

Increased information transparency significantly bolsters customer bargaining power. Online platforms and mortgage brokers now provide readily available comparisons of interest rates, fees, and loan terms from various lenders. This accessibility empowers customers, reducing the traditional information gap and enabling them to identify the most favorable offers.

In 2024, the digital mortgage market continued its expansion, with an increasing percentage of consumers utilizing online tools for initial research and comparison. For instance, data from industry reports indicated that over 60% of mortgage shoppers actively researched rates online before engaging with a lender. This trend directly pressures lenders like SBI ARUHI to maintain competitive pricing and transparent fee structures to attract and retain customers.

Demographic Shifts and Evolving Needs

Changes in borrower demographics are significantly impacting the housing loan market. For instance, an aging population in Japan, where SBI ARUHI operates, is showing increased interest in financial products like reverse mortgages to supplement retirement income. Concurrently, younger demographics are increasingly demanding digital-first experiences, prioritizing streamlined online application processes for home loans.

SBI ARUHI's strategic focus on products like Flat 35, a government-backed housing loan scheme, and its multi-channel service approach, which includes both physical branches and online platforms, are crucial for adapting to these shifts. The company must remain agile to cater to these evolving customer preferences, ensuring it can maintain and grow its market share in a dynamic environment.

- Aging Population: Japan's population is aging rapidly, with the proportion of those aged 65 and over projected to reach 31.3% by 2025, increasing demand for financial solutions tailored to seniors.

- Digital Adoption: A growing segment of the population, particularly those under 40, prefers digital channels for financial transactions, including loan applications, with mobile banking usage rising steadily.

- Housing Preferences: There's a noticeable trend towards purchasing existing homes rather than custom-built properties, which can influence the types of mortgage products and associated services customers seek.

Government Incentives and Programs

Government initiatives, such as tax incentives for energy-efficient homes and preferential interest rate measures like those for Flat 35, significantly bolster customer bargaining power. These programs effectively lower the overall cost of homeownership for eligible buyers, making them more discerning about loan terms and property features. For instance, in 2024, the Japanese government continued to support housing market stability through various subsidies and tax breaks, directly impacting affordability and consumer choice.

These government programs can directly influence customer choice by making certain loan types or housing features more attractive. When borrowers can access lower interest rates or receive tax credits, their overall financial burden is reduced, thereby increasing their leverage in negotiations with lenders and developers. This enhanced financial capacity allows customers to demand more favorable terms, potentially driving down prices or improving service quality.

The impact of these incentives is evident in the increased demand for specific housing segments. For example, a rise in government subsidies for green building technologies in 2024 likely led to a surge in demand for eco-friendly homes, giving buyers in that segment greater negotiating power. Customers who qualify for these benefits, such as preferential interest rates on mortgages, are empowered to seek out the best deals, knowing they have a financial advantage.

- Government Support: Initiatives like tax incentives for energy-efficient homes and preferential interest rates for programs such as Flat 35 empower customers.

- Influence on Choice: These programs can sway customer decisions towards specific loan types or housing features, increasing demand.

- Increased Leverage: Borrowers meeting specific criteria often receive lower rates, enhancing their bargaining position with financial institutions.

- Market Impact: In 2024, continued government support for housing affordability in markets like Japan directly influenced consumer spending and negotiation power.

Japanese Mortgage Borrowers Wield Significant Bargaining Power

Customers in the Japanese mortgage market possess significant bargaining power, largely driven by heightened price sensitivity and the availability of numerous competing lenders. The ease with which borrowers can compare offerings, especially with the proliferation of online tools and information transparency, allows them to readily identify and pursue the most advantageous loan terms. This competitive environment, coupled with relatively low switching costs, compels financial institutions to offer attractive rates and services to retain their clientele.

The prevalence of floating-rate mortgages in Japan means that borrowers are keenly aware of interest rate shifts, actively seeking to refinance or switch to more favorable fixed-rate options when rates rise. For instance, in early 2024, as fixed rates for products like Flat 35 saw increases, many borrowers explored alternative lenders to secure predictable payments, demonstrating their power to influence market pricing.

Government incentives, such as tax breaks for energy-efficient homes and preferential interest rates for programs like Flat 35, further empower customers. These initiatives reduce the overall cost of homeownership, enabling buyers to be more selective and negotiate better terms, as seen in 2024 when continued government support for housing affordability directly impacted consumer negotiation power.

| Factor | Impact on Customer Bargaining Power | 2024 Data/Trend Example |

|---|---|---|

| Price Sensitivity & Rate Awareness | High; customers actively seek lower interest rates. | Increased comparison of Flat 35 rates in early 2024 due to upward rate adjustments. |

| Availability of Lenders & Product Variety | High; numerous banks, credit unions, and online lenders offer diverse mortgage products. | Continued expansion of digital mortgage platforms offering wide comparisons. |

| Information Transparency & Digital Tools | High; online platforms provide easy comparison of rates and fees. | Over 60% of mortgage shoppers researched rates online in 2024 before engaging lenders. |

| Switching Costs | Low; administrative fees are generally minor compared to potential savings. | Potential savings of millions of yen on a ¥30 million mortgage for a 0.5% rate reduction. |

| Government Incentives (e.g., Flat 35) | High; subsidies and tax breaks lower overall cost, increasing leverage. | Continued government support for housing affordability in 2024 boosted consumer negotiation power. |

Preview Before You Purchase

SBI ARUHI Porter's Five Forces Analysis

The document you see is your deliverable. It’s ready for immediate use—no customization or setup required. This comprehensive Porter's Five Forces analysis of SBI ARUHI delves into the competitive landscape, evaluating the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the industry. Understanding these forces is crucial for strategic decision-making and identifying opportunities for SBI ARUHI to enhance its competitive position.