Standard Chartered Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Standard Chartered’s Porter’s Five Forces snapshot highlights competitive intensity, regulatory pressures, supplier and buyer leverage, and substitute threats shaping its banking model. This concise view flags strategic strengths and vulnerabilities for investors and managers. Ready to move beyond the basics? Unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Diverse funding base limits single-source leverage

Standard Chartered funds itself via retail deposits, corporates, wholesale markets and central bank facilities, with customer deposits historically forming over half of funding; this diversification curbs single-source supplier leverage. In stressed markets wholesale providers can push spreads wider, but the bank’s liquidity buffers and ALM—with LCR c.130% in 2024—limit episodic price power.

Technology and data vendors exert switching frictions

Mission-critical core banking, cloud, cybersecurity and data providers exert bargaining power due to deep integration complexity and long implementation cycles that materially raise switching costs.

Top three cloud providers held about 70% of global IaaS market share in 2024 and the RegTech market approached $19bn in 2024, letting vendors with differentiated AML, risk and payments capabilities command premium pricing.

Standard Chartered reduces concentration risk through multi-vendor sourcing and targeted in-house builds.

Skilled talent as a scarce input

Skilled risk, compliance, digital and markets talent is concentrated in hubs like London, Singapore and Hong Kong, creating supplier power as firms compete for scarce specialists. Compensation inflation—around 6% in 2024 for financial services—plus rising demand for regulatory expertise amplifies labor bargaining leverage. Retention costs spike during growth or remediation phases, while Standard Chartered’s global footprint enables internal mobility to rebalance pressure.

Correspondent and clearing banks enable cross-border reach

Correspondent and clearing banks underpin Standard Chartered’s cross‑border flows: USD and EUR accounted for roughly 40% and 32% of global cross‑border payment value in 2024, making access to their clearing rails essential. Major correspondents can set pricing and service terms, raising supplier bargaining power. Heightened sanctions and AML regimes since 2022 have increased compliance costs and operational demands, so building bilateral depth and multi‑corridor options reduces dependence.

- Access: USD/EUR clearing ~40%/32% (2024)

- Pricing power: key correspondents set fees and SLAs

- Compliance: sanctions/AML raise costs and due diligence

- Mitigation: bilateral depth + multi‑corridor routing

Regulators and central banks shape license and liquidity access

Regulators and central banks effectively quasi-supply licenses, emergency liquidity facilities and policy frameworks; non‑compliance can prompt stricter covenants or withdrawal, raising funding costs. Macroprudential rules — e.g., Basel III CET1 minimum 4.5% plus buffers and LCR >=100% — force balance sheet and funding mix adjustments. Proactive supervisory engagement reduces regulators' bargaining leverage and limits punitive tightening.

- Licenses: regulatory approval dictates market access and ongoing conditions

- Liquidity: central bank facilities set tail‑risk pricing and availability

- Policy: CET1 4.5% + buffers, LCR >=100% shape capital/funding

- Engagement: proactive dialogue lowers probability of punitive measures

Supplier power moderate; tech & RegTech strong; deposits >50%, LCR ~130%

Supplier power is moderate: diversified funding (customer deposits >50% historically; LCR ~130% in 2024) limits funding leverage. Technology, RegTech and specialist talent exert strong power (top3 cloud ~70% IaaS share 2024; RegTech ~19bn USD 2024; financial services pay inflation ~6% 2024). Correspondent banks and regulators retain high leverage for cross‑border rails and licenses; multi‑vendor sourcing and bilateral depth mitigate.

| Item | Metric (2024) |

|---|---|

| Customer deposits | >50% |

| LCR | ~130% |

| Top3 cloud IaaS | ~70% |

| RegTech market | ~19bn USD |

| Comp inflation (FS) | ~6% |

| USD/EUR clearing | ~40%/~32% |

What is included in the product

Comprehensive Porter's Five Forces assessment for Standard Chartered, revealing competitive intensity, customer and supplier bargaining power, entry barriers, substitute threats, and strategic positioning within global banking markets to inform risk mitigation and growth strategies.

A concise one-sheet Porter's Five Forces for Standard Chartered that visualizes competitive pressure with an instant spider chart, customizable by scenario and data, export-ready for decks and boardrooms—no macros or finance expertise required.

Customers Bargaining Power

Large corporates and institutions negotiate hard on price

Large corporates multi-bank and benchmark fees across global peers, with the top c.20% of clients commanding disproportionate negotiating power and pressuring spreads in 2024.

They leverage volume and ancillary wallet — deposits, treasury and trade flows — to extract tighter pricing, while deep integrated relationships and bespoke solutions can defend margins.

Cross-sell into FX, cash management and trade finance in 2024 drove the majority of CIB fee improvement, improving economics per client.

Retail and affluent segments show moderate switching costs

Digital onboarding and portability of payments reduce barriers to switch, reinforced by 2024 trends showing about 4.5 billion mobile banking users driving easier account mobility. However, trust in advice, bundled wealth and corporate products create stickiness for retail and affluent clients. Loyalty benefits and ecosystem partnerships (cards, platforms) improve retention, though service outages or rate gaps still trigger churn.

Transaction banking clients prioritize reliability over price

Cash management and trade clients prioritize uptime, network reach and compliance strength—Standard Chartered's presence in 59 markets and ISO 20022-led API standardization reinforce this, reducing pure price sensitivity when operational risk is high. Standardized SLAs and APIs increase transparency of performance and enable benchmarking, while differentiated service and guaranteed reliability allow banks to sustain pricing premia.

Sovereigns and public entities exert procedural power

Tenders and policy objectives drive sovereign procurement and pricing, with public procurement estimated at about 12% of global GDP (World Bank, 2024). Compliance, ESG and localization demands raise transaction complexity and due-diligence costs. Winning mandates often needs multi-year commitments and co-investment while competitive bidding tightens margins.

- Procurement scale: 12% GDP (World Bank, 2024)

- Higher compliance and ESG cost

- Multi-year / co-investment required

- Competitive bidding compresses margins

Wealth clients seek bespoke solutions and open architecture

- Choice & transparency: higher expectations

- Performance & private markets: key leverage

- Advisory + risk mgmt: loyalty drivers

- Platform breadth: cushions fees

Corporates squeeze fees; CIB cross-sell lifts economics; 4.5bn mobile users

Large corporates (top c.20% of clients) exert outsized fee pressure, leveraging deposits and trade flows; CIB cross-sell lifted per-client economics in 2024. Digital portability (≈4.5bn mobile users) increases switching, while trust, advisory and platform breadth (59 markets) sustain stickiness. Sovereign tenders (≈12% GDP) and private banking AUM (~27tn USD) raise procurement complexity and bargaining power.

| Metric | 2024 |

|---|---|

| Top client share | c.20% |

| Mobile users | 4.5bn |

| Markets | 59 |

| Public procurement | ≈12% GDP |

| Private banking AUM | ≈27tn USD |

Preview Before You Purchase

Standard Chartered Porter's Five Forces Analysis

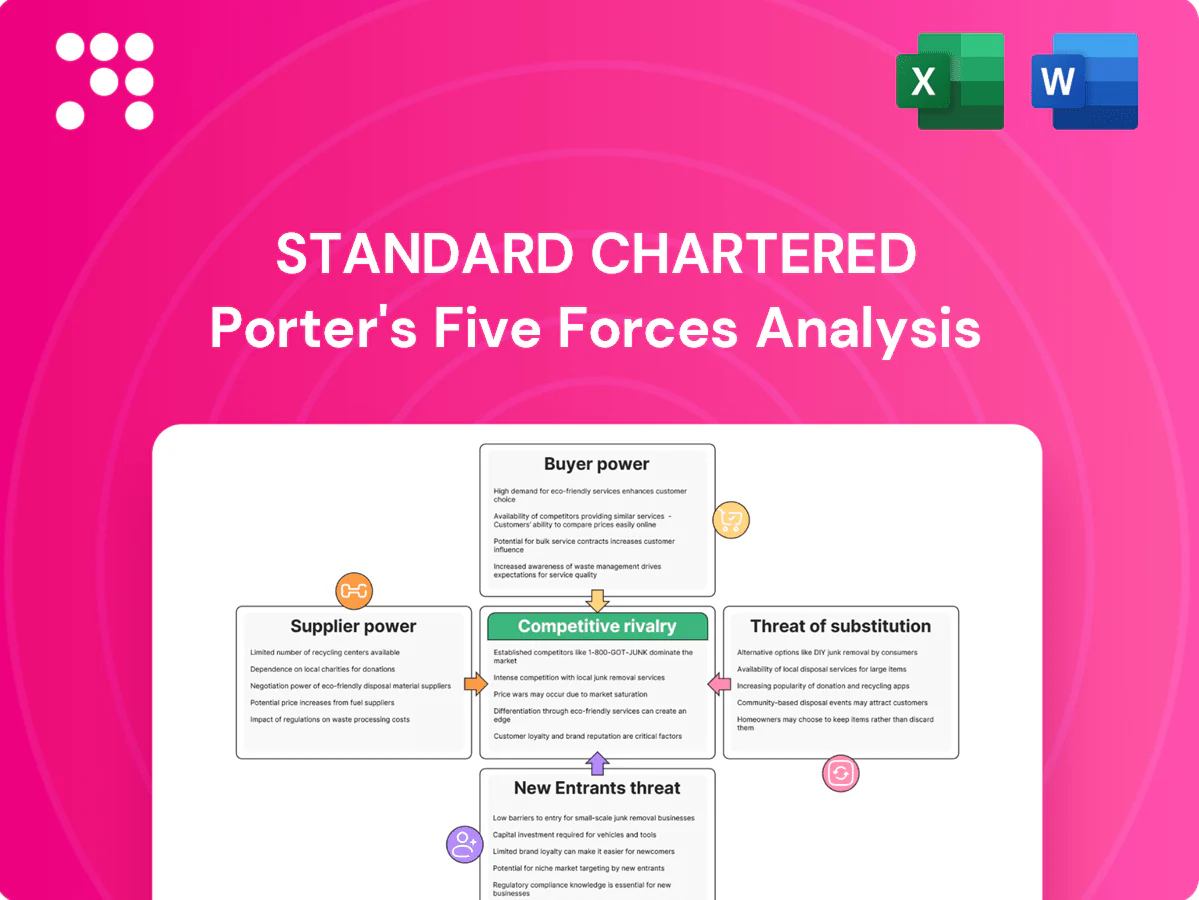

This preview is the complete Porter's Five Forces analysis of Standard Chartered—detailing competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and substitute threats. The document shown is the exact, professionally formatted file you'll receive instantly after purchase. No placeholders, no samples—ready for download and use.

Don't Miss the Bigger Picture

Standard Chartered’s Porter’s Five Forces snapshot highlights competitive intensity, regulatory pressures, supplier and buyer leverage, and substitute threats shaping its banking model. This concise view flags strategic strengths and vulnerabilities for investors and managers. Ready to move beyond the basics? Unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Diverse funding base limits single-source leverage

Standard Chartered funds itself via retail deposits, corporates, wholesale markets and central bank facilities, with customer deposits historically forming over half of funding; this diversification curbs single-source supplier leverage. In stressed markets wholesale providers can push spreads wider, but the bank’s liquidity buffers and ALM—with LCR c.130% in 2024—limit episodic price power.

Technology and data vendors exert switching frictions

Mission-critical core banking, cloud, cybersecurity and data providers exert bargaining power due to deep integration complexity and long implementation cycles that materially raise switching costs.

Top three cloud providers held about 70% of global IaaS market share in 2024 and the RegTech market approached $19bn in 2024, letting vendors with differentiated AML, risk and payments capabilities command premium pricing.

Standard Chartered reduces concentration risk through multi-vendor sourcing and targeted in-house builds.

Skilled talent as a scarce input

Skilled risk, compliance, digital and markets talent is concentrated in hubs like London, Singapore and Hong Kong, creating supplier power as firms compete for scarce specialists. Compensation inflation—around 6% in 2024 for financial services—plus rising demand for regulatory expertise amplifies labor bargaining leverage. Retention costs spike during growth or remediation phases, while Standard Chartered’s global footprint enables internal mobility to rebalance pressure.

Correspondent and clearing banks enable cross-border reach

Correspondent and clearing banks underpin Standard Chartered’s cross‑border flows: USD and EUR accounted for roughly 40% and 32% of global cross‑border payment value in 2024, making access to their clearing rails essential. Major correspondents can set pricing and service terms, raising supplier bargaining power. Heightened sanctions and AML regimes since 2022 have increased compliance costs and operational demands, so building bilateral depth and multi‑corridor options reduces dependence.

- Access: USD/EUR clearing ~40%/32% (2024)

- Pricing power: key correspondents set fees and SLAs

- Compliance: sanctions/AML raise costs and due diligence

- Mitigation: bilateral depth + multi‑corridor routing

Regulators and central banks shape license and liquidity access

Regulators and central banks effectively quasi-supply licenses, emergency liquidity facilities and policy frameworks; non‑compliance can prompt stricter covenants or withdrawal, raising funding costs. Macroprudential rules — e.g., Basel III CET1 minimum 4.5% plus buffers and LCR >=100% — force balance sheet and funding mix adjustments. Proactive supervisory engagement reduces regulators' bargaining leverage and limits punitive tightening.

- Licenses: regulatory approval dictates market access and ongoing conditions

- Liquidity: central bank facilities set tail‑risk pricing and availability

- Policy: CET1 4.5% + buffers, LCR >=100% shape capital/funding

- Engagement: proactive dialogue lowers probability of punitive measures

Supplier power moderate; tech & RegTech strong; deposits >50%, LCR ~130%

Supplier power is moderate: diversified funding (customer deposits >50% historically; LCR ~130% in 2024) limits funding leverage. Technology, RegTech and specialist talent exert strong power (top3 cloud ~70% IaaS share 2024; RegTech ~19bn USD 2024; financial services pay inflation ~6% 2024). Correspondent banks and regulators retain high leverage for cross‑border rails and licenses; multi‑vendor sourcing and bilateral depth mitigate.

| Item | Metric (2024) |

|---|---|

| Customer deposits | >50% |

| LCR | ~130% |

| Top3 cloud IaaS | ~70% |

| RegTech market | ~19bn USD |

| Comp inflation (FS) | ~6% |

| USD/EUR clearing | ~40%/~32% |

What is included in the product

Comprehensive Porter's Five Forces assessment for Standard Chartered, revealing competitive intensity, customer and supplier bargaining power, entry barriers, substitute threats, and strategic positioning within global banking markets to inform risk mitigation and growth strategies.

A concise one-sheet Porter's Five Forces for Standard Chartered that visualizes competitive pressure with an instant spider chart, customizable by scenario and data, export-ready for decks and boardrooms—no macros or finance expertise required.

Customers Bargaining Power

Large corporates and institutions negotiate hard on price

Large corporates multi-bank and benchmark fees across global peers, with the top c.20% of clients commanding disproportionate negotiating power and pressuring spreads in 2024.

They leverage volume and ancillary wallet — deposits, treasury and trade flows — to extract tighter pricing, while deep integrated relationships and bespoke solutions can defend margins.

Cross-sell into FX, cash management and trade finance in 2024 drove the majority of CIB fee improvement, improving economics per client.

Retail and affluent segments show moderate switching costs

Digital onboarding and portability of payments reduce barriers to switch, reinforced by 2024 trends showing about 4.5 billion mobile banking users driving easier account mobility. However, trust in advice, bundled wealth and corporate products create stickiness for retail and affluent clients. Loyalty benefits and ecosystem partnerships (cards, platforms) improve retention, though service outages or rate gaps still trigger churn.

Transaction banking clients prioritize reliability over price

Cash management and trade clients prioritize uptime, network reach and compliance strength—Standard Chartered's presence in 59 markets and ISO 20022-led API standardization reinforce this, reducing pure price sensitivity when operational risk is high. Standardized SLAs and APIs increase transparency of performance and enable benchmarking, while differentiated service and guaranteed reliability allow banks to sustain pricing premia.

Sovereigns and public entities exert procedural power

Tenders and policy objectives drive sovereign procurement and pricing, with public procurement estimated at about 12% of global GDP (World Bank, 2024). Compliance, ESG and localization demands raise transaction complexity and due-diligence costs. Winning mandates often needs multi-year commitments and co-investment while competitive bidding tightens margins.

- Procurement scale: 12% GDP (World Bank, 2024)

- Higher compliance and ESG cost

- Multi-year / co-investment required

- Competitive bidding compresses margins

Wealth clients seek bespoke solutions and open architecture

- Choice & transparency: higher expectations

- Performance & private markets: key leverage

- Advisory + risk mgmt: loyalty drivers

- Platform breadth: cushions fees

Corporates squeeze fees; CIB cross-sell lifts economics; 4.5bn mobile users

Large corporates (top c.20% of clients) exert outsized fee pressure, leveraging deposits and trade flows; CIB cross-sell lifted per-client economics in 2024. Digital portability (≈4.5bn mobile users) increases switching, while trust, advisory and platform breadth (59 markets) sustain stickiness. Sovereign tenders (≈12% GDP) and private banking AUM (~27tn USD) raise procurement complexity and bargaining power.

| Metric | 2024 |

|---|---|

| Top client share | c.20% |

| Mobile users | 4.5bn |

| Markets | 59 |

| Public procurement | ≈12% GDP |

| Private banking AUM | ≈27tn USD |

Preview Before You Purchase

Standard Chartered Porter's Five Forces Analysis

This preview is the complete Porter's Five Forces analysis of Standard Chartered—detailing competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and substitute threats. The document shown is the exact, professionally formatted file you'll receive instantly after purchase. No placeholders, no samples—ready for download and use.

Description

Don't Miss the Bigger Picture

Standard Chartered’s Porter’s Five Forces snapshot highlights competitive intensity, regulatory pressures, supplier and buyer leverage, and substitute threats shaping its banking model. This concise view flags strategic strengths and vulnerabilities for investors and managers. Ready to move beyond the basics? Unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Diverse funding base limits single-source leverage

Standard Chartered funds itself via retail deposits, corporates, wholesale markets and central bank facilities, with customer deposits historically forming over half of funding; this diversification curbs single-source supplier leverage. In stressed markets wholesale providers can push spreads wider, but the bank’s liquidity buffers and ALM—with LCR c.130% in 2024—limit episodic price power.

Technology and data vendors exert switching frictions

Mission-critical core banking, cloud, cybersecurity and data providers exert bargaining power due to deep integration complexity and long implementation cycles that materially raise switching costs.

Top three cloud providers held about 70% of global IaaS market share in 2024 and the RegTech market approached $19bn in 2024, letting vendors with differentiated AML, risk and payments capabilities command premium pricing.

Standard Chartered reduces concentration risk through multi-vendor sourcing and targeted in-house builds.

Skilled talent as a scarce input

Skilled risk, compliance, digital and markets talent is concentrated in hubs like London, Singapore and Hong Kong, creating supplier power as firms compete for scarce specialists. Compensation inflation—around 6% in 2024 for financial services—plus rising demand for regulatory expertise amplifies labor bargaining leverage. Retention costs spike during growth or remediation phases, while Standard Chartered’s global footprint enables internal mobility to rebalance pressure.

Correspondent and clearing banks enable cross-border reach

Correspondent and clearing banks underpin Standard Chartered’s cross‑border flows: USD and EUR accounted for roughly 40% and 32% of global cross‑border payment value in 2024, making access to their clearing rails essential. Major correspondents can set pricing and service terms, raising supplier bargaining power. Heightened sanctions and AML regimes since 2022 have increased compliance costs and operational demands, so building bilateral depth and multi‑corridor options reduces dependence.

- Access: USD/EUR clearing ~40%/32% (2024)

- Pricing power: key correspondents set fees and SLAs

- Compliance: sanctions/AML raise costs and due diligence

- Mitigation: bilateral depth + multi‑corridor routing

Regulators and central banks shape license and liquidity access

Regulators and central banks effectively quasi-supply licenses, emergency liquidity facilities and policy frameworks; non‑compliance can prompt stricter covenants or withdrawal, raising funding costs. Macroprudential rules — e.g., Basel III CET1 minimum 4.5% plus buffers and LCR >=100% — force balance sheet and funding mix adjustments. Proactive supervisory engagement reduces regulators' bargaining leverage and limits punitive tightening.

- Licenses: regulatory approval dictates market access and ongoing conditions

- Liquidity: central bank facilities set tail‑risk pricing and availability

- Policy: CET1 4.5% + buffers, LCR >=100% shape capital/funding

- Engagement: proactive dialogue lowers probability of punitive measures

Supplier power moderate; tech & RegTech strong; deposits >50%, LCR ~130%

Supplier power is moderate: diversified funding (customer deposits >50% historically; LCR ~130% in 2024) limits funding leverage. Technology, RegTech and specialist talent exert strong power (top3 cloud ~70% IaaS share 2024; RegTech ~19bn USD 2024; financial services pay inflation ~6% 2024). Correspondent banks and regulators retain high leverage for cross‑border rails and licenses; multi‑vendor sourcing and bilateral depth mitigate.

| Item | Metric (2024) |

|---|---|

| Customer deposits | >50% |

| LCR | ~130% |

| Top3 cloud IaaS | ~70% |

| RegTech market | ~19bn USD |

| Comp inflation (FS) | ~6% |

| USD/EUR clearing | ~40%/~32% |

What is included in the product

Comprehensive Porter's Five Forces assessment for Standard Chartered, revealing competitive intensity, customer and supplier bargaining power, entry barriers, substitute threats, and strategic positioning within global banking markets to inform risk mitigation and growth strategies.

A concise one-sheet Porter's Five Forces for Standard Chartered that visualizes competitive pressure with an instant spider chart, customizable by scenario and data, export-ready for decks and boardrooms—no macros or finance expertise required.

Customers Bargaining Power

Large corporates and institutions negotiate hard on price

Large corporates multi-bank and benchmark fees across global peers, with the top c.20% of clients commanding disproportionate negotiating power and pressuring spreads in 2024.

They leverage volume and ancillary wallet — deposits, treasury and trade flows — to extract tighter pricing, while deep integrated relationships and bespoke solutions can defend margins.

Cross-sell into FX, cash management and trade finance in 2024 drove the majority of CIB fee improvement, improving economics per client.

Retail and affluent segments show moderate switching costs

Digital onboarding and portability of payments reduce barriers to switch, reinforced by 2024 trends showing about 4.5 billion mobile banking users driving easier account mobility. However, trust in advice, bundled wealth and corporate products create stickiness for retail and affluent clients. Loyalty benefits and ecosystem partnerships (cards, platforms) improve retention, though service outages or rate gaps still trigger churn.

Transaction banking clients prioritize reliability over price

Cash management and trade clients prioritize uptime, network reach and compliance strength—Standard Chartered's presence in 59 markets and ISO 20022-led API standardization reinforce this, reducing pure price sensitivity when operational risk is high. Standardized SLAs and APIs increase transparency of performance and enable benchmarking, while differentiated service and guaranteed reliability allow banks to sustain pricing premia.

Sovereigns and public entities exert procedural power

Tenders and policy objectives drive sovereign procurement and pricing, with public procurement estimated at about 12% of global GDP (World Bank, 2024). Compliance, ESG and localization demands raise transaction complexity and due-diligence costs. Winning mandates often needs multi-year commitments and co-investment while competitive bidding tightens margins.

- Procurement scale: 12% GDP (World Bank, 2024)

- Higher compliance and ESG cost

- Multi-year / co-investment required

- Competitive bidding compresses margins

Wealth clients seek bespoke solutions and open architecture

- Choice & transparency: higher expectations

- Performance & private markets: key leverage

- Advisory + risk mgmt: loyalty drivers

- Platform breadth: cushions fees

Corporates squeeze fees; CIB cross-sell lifts economics; 4.5bn mobile users

Large corporates (top c.20% of clients) exert outsized fee pressure, leveraging deposits and trade flows; CIB cross-sell lifted per-client economics in 2024. Digital portability (≈4.5bn mobile users) increases switching, while trust, advisory and platform breadth (59 markets) sustain stickiness. Sovereign tenders (≈12% GDP) and private banking AUM (~27tn USD) raise procurement complexity and bargaining power.

| Metric | 2024 |

|---|---|

| Top client share | c.20% |

| Mobile users | 4.5bn |

| Markets | 59 |

| Public procurement | ≈12% GDP |

| Private banking AUM | ≈27tn USD |

Preview Before You Purchase

Standard Chartered Porter's Five Forces Analysis

This preview is the complete Porter's Five Forces analysis of Standard Chartered—detailing competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and substitute threats. The document shown is the exact, professionally formatted file you'll receive instantly after purchase. No placeholders, no samples—ready for download and use.