Scana Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Scana's competitive landscape balances regulated utility dynamics with evolving energy markets, supplier concentration, buyer leverage, and emerging substitutes. This snapshot highlights key pressures but omits force-by-force ratings, trend data, and strategic implications. Unlock the full Porter's Five Forces Analysis for Scana to access detailed ratings, visuals, and actionable recommendations. Perfect for investors and strategists seeking a data-driven edge.

Suppliers Bargaining Power

Concentrated critical component vendors

Supplier bases for subsea, offshore wind and marine equipment remain concentrated in specialty steel, forgings, hydraulics and electronics; in 2024 this concentration continued to limit qualified vendors and certification holders. Limited vendor pools raise switching costs and exert upward pressure on lead times and pricing. Scana mitigates risk through multi-sourcing and portfolio-level volume aggregation to secure capacity and negotiate terms.

Skilled engineering and yard capacity

Access to specialized engineers, welders and certified yards is tightly constrained in Northern Europe, with yard utilization often above 80% in 2024, pushing up wage bills and schedule risk. Labor scarcity raises wage pressure and can delay projects, so Scana benefits from long-term framework agreements and training partnerships that stabilize supply. Counter-cyclical hiring during downturns secures talent at better terms.

OEM and technology licensors

Dependence on OEM interfaces, IP, and licenses creates lock-in, with licensor royalty rates commonly 1–5% and OEM approval cycles often adding 6–12 months to product timelines. Royalty structures and approval gates therefore increase cost and time-to-market. Co-development and modular designs cut dependency risk by enabling interface swaps. Building proprietary IP inside portfolio companies strengthens negotiating leverage and reduces recurring licensing spend.

Logistics and project services

Heavy-lift, offshore logistics and testing facilities are scarce and highly weather-dependent, and in 2024 weather-related delays remain a primary driver of EPC schedule slippage and penalty exposure. Bottlenecks in vessels or ports can cascade across projects, increasing costs and contract risk. Early booking and portfolio-level shared services lower per-project unit costs, while localizing supply near customers reduces transit risk and contingency needs.

- Limited heavy-lift assets → higher scheduling risk

- Weather-dependent windows → EPC penalty exposure

- Early booking/shared services → lower unit costs

- Local supply → reduced transit and schedule risk

Capital equipment and energy inputs

Capital equipment and energy inputs expose Scana to raw-material and power cost swings; after 2022 peaks steel and alloy prices eased into 2024, reducing margin pressure but volatility remains and suppliers can pass surcharges during upcycles. Hedging and indexed contracts used by Scana and suppliers damp volatility, while design-to-cost and material substitution mitigate spike impacts.

- 2024: steel/alloy prices down vs 2022 peaks, easing input-cost risk

- Suppliers can enact surcharges in upcycles

- Hedging/indexed contracts reduce short-term volatility

- Design-to-cost/material substitution offset price spikes

Supplier concentration and >80% yard utilization raise lead times; multi-sourcing advised

Supplier concentration in specialty steel, forgings and certified yards keeps switching costs high; yard utilization in Northern Europe exceeded 80% in 2024, raising lead times and wages. OEM lock-in (royalties 1–5%) and approval cycles (add 6–12 months) increase costs and time-to-market. Steel/alloy prices eased ~20% vs 2022 peaks in 2024, but volatility and surcharge risk persist; multi-sourcing, hedging and co-development mitigate exposure.

| Metric | 2024 value |

|---|---|

| Yard utilization | >80% |

| OEM royalty rates | 1–5% |

| OEM approval time | +6–12 months |

| Steel/alloy price change vs 2022 | ≈-20% |

What is included in the product

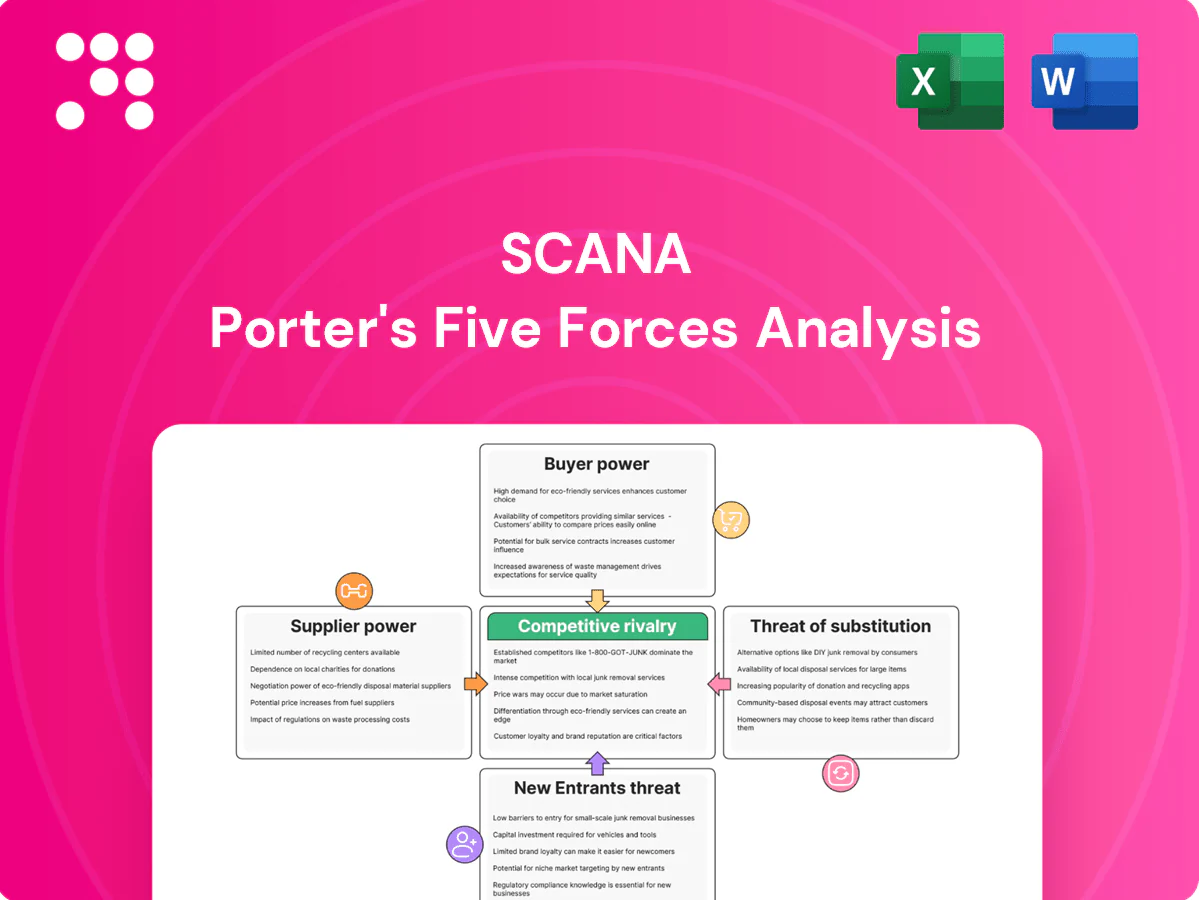

Uncovers competitive drivers, supplier and buyer power, threat of entrants and substitutes, and industry rivalry shaping Scana's profitability. Identifies disruptive threats and protective market dynamics with strategic commentary for integration into reports, investor decks, or internal strategy planning.

Scana Porter's Five Forces Analysis condenses competitive pressures into a single clear sheet for rapid strategic decisions. Customizable force levels, instant radar visualization and plug‑and‑play Excel layout make it easy to adapt to market shifts and drop directly into pitch decks.

Customers Bargaining Power

Highly concentrated blue-chip buyers

Highly concentrated blue-chip buyers—oil majors, major offshore wind developers, large shipowners and top aquaculture groups—purchase at scale and operate professional procurement and prequalification processes, forcing suppliers into framework tenders that prioritize price and lifetime cost; demonstrated 10+ year operational track records and reliability allow suppliers to justify premium pricing and win multi‑year contracts.

Project-based, long sales cycles

Customers commit through lengthy FEED and EPC phases that commonly span 2–5 years, giving buyers time to influence scope and specs early. Delays—common in large projects—shift bargaining power to buyers who control milestones and can renegotiate terms. Milestone payments are typically split across 4–6 stages and performance guarantees usually range 5–10% of contract value. Early engagement by buyers can effectively lock in long-term scope.

High switching costs but strict KPIs

Once integrated, switching is costly due to certification and interface risk, creating stickiness especially when clients embed Scana into operations with 99.9%+ SLA expectations. However, strict uptime and ESG KPIs—increasingly tied to penalties in 2024 contracts—give buyers leverage. Real‑time digital monitoring and strong service quality sustain lock‑in, while outcome‑based contracts align price with delivered value and reduce renegotiation risk.

Price sensitivity amid capex cycles

Price sensitivity for Scana shifts with capex cycles: downcycles drive 5–15% discount pressure and rebids as buyers seek cost cuts, while 2024 capex recovery saw customers prioritize delivery and availability over marginal price savings. Dynamic pricing and capacity allocation have captured upside during tight supply windows, and a diversified portfolio smooths cyclical demand swings.

- Downcycles: higher rebate/rebid activity

- Upcycles: delivery beats price

- Dynamic pricing: captures scarcity premium

- Portfolio diversity: reduces volatility

ESG and localization demands

Buyers demand low-carbon footprints and local content, with EU policy in 2024 enforcing Carbon Border Adjustment Mechanism coverage across five industrial sectors and an EU 2030 emissions reduction target of 55% driving procurement filters that can exclude non-compliant suppliers. Suppliers investing in greener processes and regional footprints strengthen bid competitiveness, while transparent ESG reporting enables premium pricing and access to regulated markets.

- CBAM coverage: 5 sectors (2024)

- EU 2030 target: −55% vs 1990

- Localization raises market access for regional suppliers

- Transparent reporting supports premium bids

FEED/EPC 2–5yr delivery; 5–10% guarantees; CBAM −55%/2030

Highly concentrated blue‑chip buyers drive framework tenders and price focus; FEED/EPC commitments span 2–5 years and performance guarantees run 5–10% of contract value. Switching costs and 99.9%+ SLA expectations create lock‑in, while 2024 capex recovery shifted buyer priority to delivery over marginal price, with downcycles producing 5–15% rebate pressure. EU 2024 policy: CBAM covers 5 sectors and 2030 target −55% vs 1990.

| Metric | 2024 Value |

|---|---|

| FEED/EPC duration | 2–5 yrs |

| Performance guarantees | 5–10% |

| Downcycle price pressure | 5–15% |

| CBAM coverage | 5 sectors |

| EU 2030 target | −55% vs 1990 |

Same Document Delivered

Scana Porter's Five Forces Analysis

This preview shows the exact Scana Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professional, and ready for download and use upon payment. You're viewing the final deliverable.

Don't Miss the Bigger Picture

Scana's competitive landscape balances regulated utility dynamics with evolving energy markets, supplier concentration, buyer leverage, and emerging substitutes. This snapshot highlights key pressures but omits force-by-force ratings, trend data, and strategic implications. Unlock the full Porter's Five Forces Analysis for Scana to access detailed ratings, visuals, and actionable recommendations. Perfect for investors and strategists seeking a data-driven edge.

Suppliers Bargaining Power

Concentrated critical component vendors

Supplier bases for subsea, offshore wind and marine equipment remain concentrated in specialty steel, forgings, hydraulics and electronics; in 2024 this concentration continued to limit qualified vendors and certification holders. Limited vendor pools raise switching costs and exert upward pressure on lead times and pricing. Scana mitigates risk through multi-sourcing and portfolio-level volume aggregation to secure capacity and negotiate terms.

Skilled engineering and yard capacity

Access to specialized engineers, welders and certified yards is tightly constrained in Northern Europe, with yard utilization often above 80% in 2024, pushing up wage bills and schedule risk. Labor scarcity raises wage pressure and can delay projects, so Scana benefits from long-term framework agreements and training partnerships that stabilize supply. Counter-cyclical hiring during downturns secures talent at better terms.

OEM and technology licensors

Dependence on OEM interfaces, IP, and licenses creates lock-in, with licensor royalty rates commonly 1–5% and OEM approval cycles often adding 6–12 months to product timelines. Royalty structures and approval gates therefore increase cost and time-to-market. Co-development and modular designs cut dependency risk by enabling interface swaps. Building proprietary IP inside portfolio companies strengthens negotiating leverage and reduces recurring licensing spend.

Logistics and project services

Heavy-lift, offshore logistics and testing facilities are scarce and highly weather-dependent, and in 2024 weather-related delays remain a primary driver of EPC schedule slippage and penalty exposure. Bottlenecks in vessels or ports can cascade across projects, increasing costs and contract risk. Early booking and portfolio-level shared services lower per-project unit costs, while localizing supply near customers reduces transit risk and contingency needs.

- Limited heavy-lift assets → higher scheduling risk

- Weather-dependent windows → EPC penalty exposure

- Early booking/shared services → lower unit costs

- Local supply → reduced transit and schedule risk

Capital equipment and energy inputs

Capital equipment and energy inputs expose Scana to raw-material and power cost swings; after 2022 peaks steel and alloy prices eased into 2024, reducing margin pressure but volatility remains and suppliers can pass surcharges during upcycles. Hedging and indexed contracts used by Scana and suppliers damp volatility, while design-to-cost and material substitution mitigate spike impacts.

- 2024: steel/alloy prices down vs 2022 peaks, easing input-cost risk

- Suppliers can enact surcharges in upcycles

- Hedging/indexed contracts reduce short-term volatility

- Design-to-cost/material substitution offset price spikes

Supplier concentration and >80% yard utilization raise lead times; multi-sourcing advised

Supplier concentration in specialty steel, forgings and certified yards keeps switching costs high; yard utilization in Northern Europe exceeded 80% in 2024, raising lead times and wages. OEM lock-in (royalties 1–5%) and approval cycles (add 6–12 months) increase costs and time-to-market. Steel/alloy prices eased ~20% vs 2022 peaks in 2024, but volatility and surcharge risk persist; multi-sourcing, hedging and co-development mitigate exposure.

| Metric | 2024 value |

|---|---|

| Yard utilization | >80% |

| OEM royalty rates | 1–5% |

| OEM approval time | +6–12 months |

| Steel/alloy price change vs 2022 | ≈-20% |

What is included in the product

Uncovers competitive drivers, supplier and buyer power, threat of entrants and substitutes, and industry rivalry shaping Scana's profitability. Identifies disruptive threats and protective market dynamics with strategic commentary for integration into reports, investor decks, or internal strategy planning.

Scana Porter's Five Forces Analysis condenses competitive pressures into a single clear sheet for rapid strategic decisions. Customizable force levels, instant radar visualization and plug‑and‑play Excel layout make it easy to adapt to market shifts and drop directly into pitch decks.

Customers Bargaining Power

Highly concentrated blue-chip buyers

Highly concentrated blue-chip buyers—oil majors, major offshore wind developers, large shipowners and top aquaculture groups—purchase at scale and operate professional procurement and prequalification processes, forcing suppliers into framework tenders that prioritize price and lifetime cost; demonstrated 10+ year operational track records and reliability allow suppliers to justify premium pricing and win multi‑year contracts.

Project-based, long sales cycles

Customers commit through lengthy FEED and EPC phases that commonly span 2–5 years, giving buyers time to influence scope and specs early. Delays—common in large projects—shift bargaining power to buyers who control milestones and can renegotiate terms. Milestone payments are typically split across 4–6 stages and performance guarantees usually range 5–10% of contract value. Early engagement by buyers can effectively lock in long-term scope.

High switching costs but strict KPIs

Once integrated, switching is costly due to certification and interface risk, creating stickiness especially when clients embed Scana into operations with 99.9%+ SLA expectations. However, strict uptime and ESG KPIs—increasingly tied to penalties in 2024 contracts—give buyers leverage. Real‑time digital monitoring and strong service quality sustain lock‑in, while outcome‑based contracts align price with delivered value and reduce renegotiation risk.

Price sensitivity amid capex cycles

Price sensitivity for Scana shifts with capex cycles: downcycles drive 5–15% discount pressure and rebids as buyers seek cost cuts, while 2024 capex recovery saw customers prioritize delivery and availability over marginal price savings. Dynamic pricing and capacity allocation have captured upside during tight supply windows, and a diversified portfolio smooths cyclical demand swings.

- Downcycles: higher rebate/rebid activity

- Upcycles: delivery beats price

- Dynamic pricing: captures scarcity premium

- Portfolio diversity: reduces volatility

ESG and localization demands

Buyers demand low-carbon footprints and local content, with EU policy in 2024 enforcing Carbon Border Adjustment Mechanism coverage across five industrial sectors and an EU 2030 emissions reduction target of 55% driving procurement filters that can exclude non-compliant suppliers. Suppliers investing in greener processes and regional footprints strengthen bid competitiveness, while transparent ESG reporting enables premium pricing and access to regulated markets.

- CBAM coverage: 5 sectors (2024)

- EU 2030 target: −55% vs 1990

- Localization raises market access for regional suppliers

- Transparent reporting supports premium bids

FEED/EPC 2–5yr delivery; 5–10% guarantees; CBAM −55%/2030

Highly concentrated blue‑chip buyers drive framework tenders and price focus; FEED/EPC commitments span 2–5 years and performance guarantees run 5–10% of contract value. Switching costs and 99.9%+ SLA expectations create lock‑in, while 2024 capex recovery shifted buyer priority to delivery over marginal price, with downcycles producing 5–15% rebate pressure. EU 2024 policy: CBAM covers 5 sectors and 2030 target −55% vs 1990.

| Metric | 2024 Value |

|---|---|

| FEED/EPC duration | 2–5 yrs |

| Performance guarantees | 5–10% |

| Downcycle price pressure | 5–15% |

| CBAM coverage | 5 sectors |

| EU 2030 target | −55% vs 1990 |

Same Document Delivered

Scana Porter's Five Forces Analysis

This preview shows the exact Scana Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professional, and ready for download and use upon payment. You're viewing the final deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Scana's competitive landscape balances regulated utility dynamics with evolving energy markets, supplier concentration, buyer leverage, and emerging substitutes. This snapshot highlights key pressures but omits force-by-force ratings, trend data, and strategic implications. Unlock the full Porter's Five Forces Analysis for Scana to access detailed ratings, visuals, and actionable recommendations. Perfect for investors and strategists seeking a data-driven edge.

Suppliers Bargaining Power

Concentrated critical component vendors

Supplier bases for subsea, offshore wind and marine equipment remain concentrated in specialty steel, forgings, hydraulics and electronics; in 2024 this concentration continued to limit qualified vendors and certification holders. Limited vendor pools raise switching costs and exert upward pressure on lead times and pricing. Scana mitigates risk through multi-sourcing and portfolio-level volume aggregation to secure capacity and negotiate terms.

Skilled engineering and yard capacity

Access to specialized engineers, welders and certified yards is tightly constrained in Northern Europe, with yard utilization often above 80% in 2024, pushing up wage bills and schedule risk. Labor scarcity raises wage pressure and can delay projects, so Scana benefits from long-term framework agreements and training partnerships that stabilize supply. Counter-cyclical hiring during downturns secures talent at better terms.

OEM and technology licensors

Dependence on OEM interfaces, IP, and licenses creates lock-in, with licensor royalty rates commonly 1–5% and OEM approval cycles often adding 6–12 months to product timelines. Royalty structures and approval gates therefore increase cost and time-to-market. Co-development and modular designs cut dependency risk by enabling interface swaps. Building proprietary IP inside portfolio companies strengthens negotiating leverage and reduces recurring licensing spend.

Logistics and project services

Heavy-lift, offshore logistics and testing facilities are scarce and highly weather-dependent, and in 2024 weather-related delays remain a primary driver of EPC schedule slippage and penalty exposure. Bottlenecks in vessels or ports can cascade across projects, increasing costs and contract risk. Early booking and portfolio-level shared services lower per-project unit costs, while localizing supply near customers reduces transit risk and contingency needs.

- Limited heavy-lift assets → higher scheduling risk

- Weather-dependent windows → EPC penalty exposure

- Early booking/shared services → lower unit costs

- Local supply → reduced transit and schedule risk

Capital equipment and energy inputs

Capital equipment and energy inputs expose Scana to raw-material and power cost swings; after 2022 peaks steel and alloy prices eased into 2024, reducing margin pressure but volatility remains and suppliers can pass surcharges during upcycles. Hedging and indexed contracts used by Scana and suppliers damp volatility, while design-to-cost and material substitution mitigate spike impacts.

- 2024: steel/alloy prices down vs 2022 peaks, easing input-cost risk

- Suppliers can enact surcharges in upcycles

- Hedging/indexed contracts reduce short-term volatility

- Design-to-cost/material substitution offset price spikes

Supplier concentration and >80% yard utilization raise lead times; multi-sourcing advised

Supplier concentration in specialty steel, forgings and certified yards keeps switching costs high; yard utilization in Northern Europe exceeded 80% in 2024, raising lead times and wages. OEM lock-in (royalties 1–5%) and approval cycles (add 6–12 months) increase costs and time-to-market. Steel/alloy prices eased ~20% vs 2022 peaks in 2024, but volatility and surcharge risk persist; multi-sourcing, hedging and co-development mitigate exposure.

| Metric | 2024 value |

|---|---|

| Yard utilization | >80% |

| OEM royalty rates | 1–5% |

| OEM approval time | +6–12 months |

| Steel/alloy price change vs 2022 | ≈-20% |

What is included in the product

Uncovers competitive drivers, supplier and buyer power, threat of entrants and substitutes, and industry rivalry shaping Scana's profitability. Identifies disruptive threats and protective market dynamics with strategic commentary for integration into reports, investor decks, or internal strategy planning.

Scana Porter's Five Forces Analysis condenses competitive pressures into a single clear sheet for rapid strategic decisions. Customizable force levels, instant radar visualization and plug‑and‑play Excel layout make it easy to adapt to market shifts and drop directly into pitch decks.

Customers Bargaining Power

Highly concentrated blue-chip buyers

Highly concentrated blue-chip buyers—oil majors, major offshore wind developers, large shipowners and top aquaculture groups—purchase at scale and operate professional procurement and prequalification processes, forcing suppliers into framework tenders that prioritize price and lifetime cost; demonstrated 10+ year operational track records and reliability allow suppliers to justify premium pricing and win multi‑year contracts.

Project-based, long sales cycles

Customers commit through lengthy FEED and EPC phases that commonly span 2–5 years, giving buyers time to influence scope and specs early. Delays—common in large projects—shift bargaining power to buyers who control milestones and can renegotiate terms. Milestone payments are typically split across 4–6 stages and performance guarantees usually range 5–10% of contract value. Early engagement by buyers can effectively lock in long-term scope.

High switching costs but strict KPIs

Once integrated, switching is costly due to certification and interface risk, creating stickiness especially when clients embed Scana into operations with 99.9%+ SLA expectations. However, strict uptime and ESG KPIs—increasingly tied to penalties in 2024 contracts—give buyers leverage. Real‑time digital monitoring and strong service quality sustain lock‑in, while outcome‑based contracts align price with delivered value and reduce renegotiation risk.

Price sensitivity amid capex cycles

Price sensitivity for Scana shifts with capex cycles: downcycles drive 5–15% discount pressure and rebids as buyers seek cost cuts, while 2024 capex recovery saw customers prioritize delivery and availability over marginal price savings. Dynamic pricing and capacity allocation have captured upside during tight supply windows, and a diversified portfolio smooths cyclical demand swings.

- Downcycles: higher rebate/rebid activity

- Upcycles: delivery beats price

- Dynamic pricing: captures scarcity premium

- Portfolio diversity: reduces volatility

ESG and localization demands

Buyers demand low-carbon footprints and local content, with EU policy in 2024 enforcing Carbon Border Adjustment Mechanism coverage across five industrial sectors and an EU 2030 emissions reduction target of 55% driving procurement filters that can exclude non-compliant suppliers. Suppliers investing in greener processes and regional footprints strengthen bid competitiveness, while transparent ESG reporting enables premium pricing and access to regulated markets.

- CBAM coverage: 5 sectors (2024)

- EU 2030 target: −55% vs 1990

- Localization raises market access for regional suppliers

- Transparent reporting supports premium bids

FEED/EPC 2–5yr delivery; 5–10% guarantees; CBAM −55%/2030

Highly concentrated blue‑chip buyers drive framework tenders and price focus; FEED/EPC commitments span 2–5 years and performance guarantees run 5–10% of contract value. Switching costs and 99.9%+ SLA expectations create lock‑in, while 2024 capex recovery shifted buyer priority to delivery over marginal price, with downcycles producing 5–15% rebate pressure. EU 2024 policy: CBAM covers 5 sectors and 2030 target −55% vs 1990.

| Metric | 2024 Value |

|---|---|

| FEED/EPC duration | 2–5 yrs |

| Performance guarantees | 5–10% |

| Downcycle price pressure | 5–15% |

| CBAM coverage | 5 sectors |

| EU 2030 target | −55% vs 1990 |

Same Document Delivered

Scana Porter's Five Forces Analysis

This preview shows the exact Scana Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professional, and ready for download and use upon payment. You're viewing the final deliverable.