Scandi Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

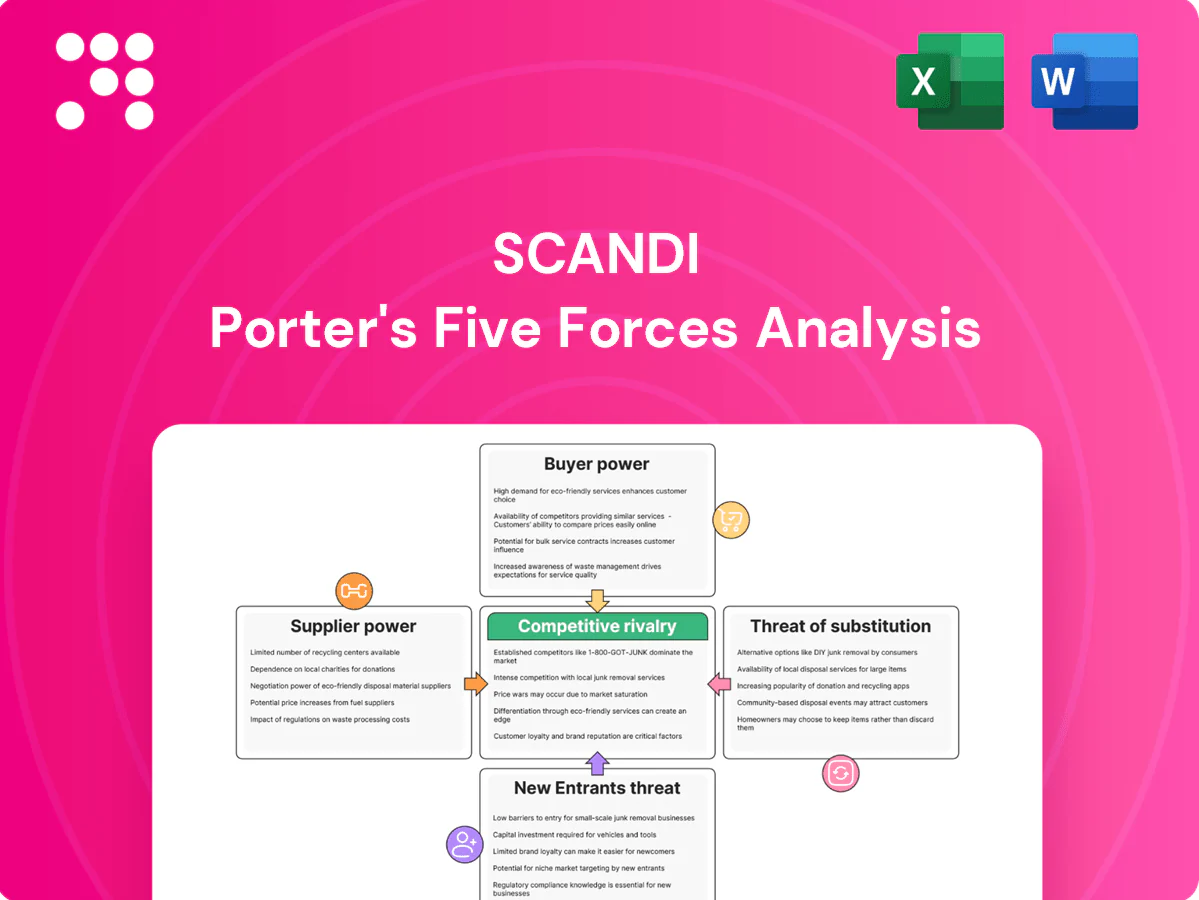

Scandi’s Porter’s Five Forces snapshot highlights supplier leverage, buyer bargaining trends, rivalry intensity and looming substitute and entrant risks — essential context for strategic moves. This brief teases key pressures; unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Scandi.

Suppliers Bargaining Power

Feed concentration

Feed is the largest input cost for Scandi, typically around 60% of production costs, and is tied to a concentrated global grain and soy supply where Brazil and the US account for roughly 80% of soybean exports in 2024. Commodity price spikes and currency swings during 2022–24 episodes increased supplier leverage. Hedging and multi-year contracts reduce but do not remove exposure. Weather shocks or trade disruptions can reprice inputs within weeks.

Breeder dependence

Access to day-old chicks depends on a handful of global genetics firms—top three suppliers account for roughly 80% of commercial broiler genetics in 2024, giving them structural bargaining power. Limited substitution and proprietary lines constrain buyers; breeder-level HPAI and other biosecurity events have repeatedly disrupted availability. Multi-sourcing and in-house hatching can reduce external purchases by c.25–30% but cannot eliminate dependence.

Contract farmers

Grow-out often relies on contract farmers with localized alternatives, and in Norway — the region's largest producer — farmed Atlantic salmon output was about 1.3 million tonnes in 2024, keeping supplier options fragmented. In tight labor or energy markets, farmer contract terms and energy cost pass-through can shift bargaining power, with industrial electricity prices and labor shortages amplifying leverage. Long-term partnerships and performance-based pay align incentives and cap opportunism, though regional consolidation of growers (fewer, larger contractors) raises their collective bargaining stance.

Energy and packaging

Energy hedges and efficiency capex reduced volatility exposure for processors in 2024, while sustainability-driven specifications (recycled/resin PCR) add cost layers suppliers can leverage.

Logistics exposure

Cold-chain capacity constraints pushed refrigerated carrier bargaining power higher, with peak utilization exceeding 80% in 2024 and spot premiums rising on key Nordic routes. Cross-border flows within the Nordics and EU add customs compliance and fuel surcharge volatility, while long-term lanes and backhaul optimization cap rate increases. Port disruptions and an EU truck driver shortfall estimated near 350,000 in 2024 can rapidly tighten supply.

- Peak cold-chain utilization >80% (2024)

- EU driver shortfall ~350,000 (2024)

- Long-term lanes/backhaul reduce spot-rate exposure

Supplier concentration and energy shocks squeeze margins and logistics capacity

Suppliers exert high leverage: feed ~60% of costs and Brazil+US ~80% of soybean exports (2024), so input shocks quickly raise prices. Genetics concentrated (top 3 ~80% broiler genetics, 2024), limiting substitution. Energy and resin tied to Brent ~ $85/bbl (2024); cold-chain utilization >80% with EU driver shortfall ~350,000, boosting logistics supplier power.

| Metric | 2024 |

|---|---|

| Feed share | ~60% |

| Soy export share (Brazil+US) | ~80% |

| Top-3 genetics | ~80% |

| Brent | $85/bbl |

| Cold-chain peak use | >80% |

| EU driver shortfall | ~350,000 |

What is included in the product

Uncovers key competitive drivers—rivalry, supplier and buyer power, threat of entrants and substitutes—tailored to Scandi’s market position. Identifies disruptive threats, pricing pressures and entry barriers, delivered in fully editable Word format for business plans, investor decks and strategic reports.

A concise one-sheet Scandi Porter's Five Forces summary that visualizes competitive pressure with an editable spider chart, lets you tweak force levels for shifting market trends or regulations, and copies cleanly into decks—no macros required.

Customers Bargaining Power

Retail consolidation

Nordic and Irish grocery sectors are highly consolidated, concentrating purchasing power: NorgesGruppen ≈43% in Norway, ICA ≈36% in Sweden and S‑Group ≈46% in Finland (2024), while Ireland’s top three grocers account for roughly 80% of the market. Large chains aggressively negotiate price, promotional funding and shelf space, leveraging scale to extract concessions. Suppliers become volume‑dependent, increasing exposure to a few accounts. Joint buying alliances further amplify retailer bargaining power.

Private label power

Private label penetration in Scandinavian poultry reached c.50% of retail volume in 2024, driving a largely price-led category where retailers use private brands to compress supplier margins. Retailers can threaten insourcing or shift to alternative co-packers, increasing supplier bargaining pressure and margin volatility. Branded value-adds (marinated, convenience) preserve premium pockets, but core cuts remain commoditized. Differentiation via higher welfare, certified origin, and sustainability claims can reduce price elasticity and defend premiums.

Foodservice tenders

QSRs and contract caterers allocate volumes via competitive tenders that often award millions in annual supply; contracts commonly run 3–5 years with renewal options (2024). Standardized specs and dual-sourcing keep switching costs low, enabling buyers to drive down prices. Menu price sensitivity—food costs typically 25–35% of sales—feeds tight procurement terms. Long contracts give volume visibility but restrict pricing flexibility.

Industrial buyers

Industrial buyers can pivot to alternative origins, using EU imports (~1.1 Mt in 2024) as a price benchmark that amplifies downward pressure; technical specs are strict but broadly achievable, shifting negotiation focus to reliability. Value is driven more by OTIF (industry targets >98% in 2024) and consistent supply than by lowest unit price alone.

- Benchmark: EU imports ~1.1 Mt (2024)

- OTIF: industry target >98% (2024)

- Specs: stringent but reachable

- Buyers leverage origin flexibility to pressure margins

Consumer frugality

End-demand is highly price elastic in staples; Kantar 2024 reports promotions drive roughly 35% of grocery volume, amplifying sensitivity to price cuts.

Promotions shift mix and velocity, prompting retailers to request category funding from suppliers to sustain shelf presence and turnover.

Premium convenience lines see down‑trading during weak macro cycles, while clear provenance and welfare claims preserve some pricing power.

- Elasticity: high in staples

- Promotions: ~35% grocery volume (Kantar 2024)

- Down‑trading: affects premium convenience

- Provenance/welfare: supports price retention

Retailer concentration and private labels squeeze poultry suppliers; promotions shift leverage

Retailer concentration and scale give buyers strong leverage (NorgesGruppen 43%, ICA 36%, S‑Group 46%, Ireland top3 ~80% in 2024), enabling aggressive price, promo funding and shelf terms. High private‑label share in poultry (~50% volume) and easy origin substitution (EU imports ~1.1 Mt) compress supplier margins; OTIF (>98%) and promotions (~35% grocery volume) shift negotiations toward reliability and funding. Premiums retain some defense via provenance/welfare claims.

| Metric | 2024 |

|---|---|

| NorgesGruppen share | ≈43% |

| ICA share | ≈36% |

| S‑Group share | ≈46% |

| Ireland top3 | ≈80% |

| Private‑label poultry | ≈50% vol |

| EU imports | ≈1.1 Mt |

| Promotions (Kantar) | ≈35% vol |

| OTIF target | >98% |

Preview Before You Purchase

Scandi Porter's Five Forces Analysis

This Scandi Porter's Five Forces Analysis provides a concise, professional assessment of competitive forces affecting Scandinavian markets, covering supplier and buyer power, rivalry, substitutes, and barriers to entry. The preview here is the exact document you’ll receive immediately after purchase—fully formatted and ready to use. No placeholders, no samples, just the final deliverable for instant download.

Go Beyond the Preview—Access the Full Strategic Report

Scandi’s Porter’s Five Forces snapshot highlights supplier leverage, buyer bargaining trends, rivalry intensity and looming substitute and entrant risks — essential context for strategic moves. This brief teases key pressures; unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Scandi.

Suppliers Bargaining Power

Feed concentration

Feed is the largest input cost for Scandi, typically around 60% of production costs, and is tied to a concentrated global grain and soy supply where Brazil and the US account for roughly 80% of soybean exports in 2024. Commodity price spikes and currency swings during 2022–24 episodes increased supplier leverage. Hedging and multi-year contracts reduce but do not remove exposure. Weather shocks or trade disruptions can reprice inputs within weeks.

Breeder dependence

Access to day-old chicks depends on a handful of global genetics firms—top three suppliers account for roughly 80% of commercial broiler genetics in 2024, giving them structural bargaining power. Limited substitution and proprietary lines constrain buyers; breeder-level HPAI and other biosecurity events have repeatedly disrupted availability. Multi-sourcing and in-house hatching can reduce external purchases by c.25–30% but cannot eliminate dependence.

Contract farmers

Grow-out often relies on contract farmers with localized alternatives, and in Norway — the region's largest producer — farmed Atlantic salmon output was about 1.3 million tonnes in 2024, keeping supplier options fragmented. In tight labor or energy markets, farmer contract terms and energy cost pass-through can shift bargaining power, with industrial electricity prices and labor shortages amplifying leverage. Long-term partnerships and performance-based pay align incentives and cap opportunism, though regional consolidation of growers (fewer, larger contractors) raises their collective bargaining stance.

Energy and packaging

Energy hedges and efficiency capex reduced volatility exposure for processors in 2024, while sustainability-driven specifications (recycled/resin PCR) add cost layers suppliers can leverage.

Logistics exposure

Cold-chain capacity constraints pushed refrigerated carrier bargaining power higher, with peak utilization exceeding 80% in 2024 and spot premiums rising on key Nordic routes. Cross-border flows within the Nordics and EU add customs compliance and fuel surcharge volatility, while long-term lanes and backhaul optimization cap rate increases. Port disruptions and an EU truck driver shortfall estimated near 350,000 in 2024 can rapidly tighten supply.

- Peak cold-chain utilization >80% (2024)

- EU driver shortfall ~350,000 (2024)

- Long-term lanes/backhaul reduce spot-rate exposure

Supplier concentration and energy shocks squeeze margins and logistics capacity

Suppliers exert high leverage: feed ~60% of costs and Brazil+US ~80% of soybean exports (2024), so input shocks quickly raise prices. Genetics concentrated (top 3 ~80% broiler genetics, 2024), limiting substitution. Energy and resin tied to Brent ~ $85/bbl (2024); cold-chain utilization >80% with EU driver shortfall ~350,000, boosting logistics supplier power.

| Metric | 2024 |

|---|---|

| Feed share | ~60% |

| Soy export share (Brazil+US) | ~80% |

| Top-3 genetics | ~80% |

| Brent | $85/bbl |

| Cold-chain peak use | >80% |

| EU driver shortfall | ~350,000 |

What is included in the product

Uncovers key competitive drivers—rivalry, supplier and buyer power, threat of entrants and substitutes—tailored to Scandi’s market position. Identifies disruptive threats, pricing pressures and entry barriers, delivered in fully editable Word format for business plans, investor decks and strategic reports.

A concise one-sheet Scandi Porter's Five Forces summary that visualizes competitive pressure with an editable spider chart, lets you tweak force levels for shifting market trends or regulations, and copies cleanly into decks—no macros required.

Customers Bargaining Power

Retail consolidation

Nordic and Irish grocery sectors are highly consolidated, concentrating purchasing power: NorgesGruppen ≈43% in Norway, ICA ≈36% in Sweden and S‑Group ≈46% in Finland (2024), while Ireland’s top three grocers account for roughly 80% of the market. Large chains aggressively negotiate price, promotional funding and shelf space, leveraging scale to extract concessions. Suppliers become volume‑dependent, increasing exposure to a few accounts. Joint buying alliances further amplify retailer bargaining power.

Private label power

Private label penetration in Scandinavian poultry reached c.50% of retail volume in 2024, driving a largely price-led category where retailers use private brands to compress supplier margins. Retailers can threaten insourcing or shift to alternative co-packers, increasing supplier bargaining pressure and margin volatility. Branded value-adds (marinated, convenience) preserve premium pockets, but core cuts remain commoditized. Differentiation via higher welfare, certified origin, and sustainability claims can reduce price elasticity and defend premiums.

Foodservice tenders

QSRs and contract caterers allocate volumes via competitive tenders that often award millions in annual supply; contracts commonly run 3–5 years with renewal options (2024). Standardized specs and dual-sourcing keep switching costs low, enabling buyers to drive down prices. Menu price sensitivity—food costs typically 25–35% of sales—feeds tight procurement terms. Long contracts give volume visibility but restrict pricing flexibility.

Industrial buyers

Industrial buyers can pivot to alternative origins, using EU imports (~1.1 Mt in 2024) as a price benchmark that amplifies downward pressure; technical specs are strict but broadly achievable, shifting negotiation focus to reliability. Value is driven more by OTIF (industry targets >98% in 2024) and consistent supply than by lowest unit price alone.

- Benchmark: EU imports ~1.1 Mt (2024)

- OTIF: industry target >98% (2024)

- Specs: stringent but reachable

- Buyers leverage origin flexibility to pressure margins

Consumer frugality

End-demand is highly price elastic in staples; Kantar 2024 reports promotions drive roughly 35% of grocery volume, amplifying sensitivity to price cuts.

Promotions shift mix and velocity, prompting retailers to request category funding from suppliers to sustain shelf presence and turnover.

Premium convenience lines see down‑trading during weak macro cycles, while clear provenance and welfare claims preserve some pricing power.

- Elasticity: high in staples

- Promotions: ~35% grocery volume (Kantar 2024)

- Down‑trading: affects premium convenience

- Provenance/welfare: supports price retention

Retailer concentration and private labels squeeze poultry suppliers; promotions shift leverage

Retailer concentration and scale give buyers strong leverage (NorgesGruppen 43%, ICA 36%, S‑Group 46%, Ireland top3 ~80% in 2024), enabling aggressive price, promo funding and shelf terms. High private‑label share in poultry (~50% volume) and easy origin substitution (EU imports ~1.1 Mt) compress supplier margins; OTIF (>98%) and promotions (~35% grocery volume) shift negotiations toward reliability and funding. Premiums retain some defense via provenance/welfare claims.

| Metric | 2024 |

|---|---|

| NorgesGruppen share | ≈43% |

| ICA share | ≈36% |

| S‑Group share | ≈46% |

| Ireland top3 | ≈80% |

| Private‑label poultry | ≈50% vol |

| EU imports | ≈1.1 Mt |

| Promotions (Kantar) | ≈35% vol |

| OTIF target | >98% |

Preview Before You Purchase

Scandi Porter's Five Forces Analysis

This Scandi Porter's Five Forces Analysis provides a concise, professional assessment of competitive forces affecting Scandinavian markets, covering supplier and buyer power, rivalry, substitutes, and barriers to entry. The preview here is the exact document you’ll receive immediately after purchase—fully formatted and ready to use. No placeholders, no samples, just the final deliverable for instant download.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Scandi’s Porter’s Five Forces snapshot highlights supplier leverage, buyer bargaining trends, rivalry intensity and looming substitute and entrant risks — essential context for strategic moves. This brief teases key pressures; unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Scandi.

Suppliers Bargaining Power

Feed concentration

Feed is the largest input cost for Scandi, typically around 60% of production costs, and is tied to a concentrated global grain and soy supply where Brazil and the US account for roughly 80% of soybean exports in 2024. Commodity price spikes and currency swings during 2022–24 episodes increased supplier leverage. Hedging and multi-year contracts reduce but do not remove exposure. Weather shocks or trade disruptions can reprice inputs within weeks.

Breeder dependence

Access to day-old chicks depends on a handful of global genetics firms—top three suppliers account for roughly 80% of commercial broiler genetics in 2024, giving them structural bargaining power. Limited substitution and proprietary lines constrain buyers; breeder-level HPAI and other biosecurity events have repeatedly disrupted availability. Multi-sourcing and in-house hatching can reduce external purchases by c.25–30% but cannot eliminate dependence.

Contract farmers

Grow-out often relies on contract farmers with localized alternatives, and in Norway — the region's largest producer — farmed Atlantic salmon output was about 1.3 million tonnes in 2024, keeping supplier options fragmented. In tight labor or energy markets, farmer contract terms and energy cost pass-through can shift bargaining power, with industrial electricity prices and labor shortages amplifying leverage. Long-term partnerships and performance-based pay align incentives and cap opportunism, though regional consolidation of growers (fewer, larger contractors) raises their collective bargaining stance.

Energy and packaging

Energy hedges and efficiency capex reduced volatility exposure for processors in 2024, while sustainability-driven specifications (recycled/resin PCR) add cost layers suppliers can leverage.

Logistics exposure

Cold-chain capacity constraints pushed refrigerated carrier bargaining power higher, with peak utilization exceeding 80% in 2024 and spot premiums rising on key Nordic routes. Cross-border flows within the Nordics and EU add customs compliance and fuel surcharge volatility, while long-term lanes and backhaul optimization cap rate increases. Port disruptions and an EU truck driver shortfall estimated near 350,000 in 2024 can rapidly tighten supply.

- Peak cold-chain utilization >80% (2024)

- EU driver shortfall ~350,000 (2024)

- Long-term lanes/backhaul reduce spot-rate exposure

Supplier concentration and energy shocks squeeze margins and logistics capacity

Suppliers exert high leverage: feed ~60% of costs and Brazil+US ~80% of soybean exports (2024), so input shocks quickly raise prices. Genetics concentrated (top 3 ~80% broiler genetics, 2024), limiting substitution. Energy and resin tied to Brent ~ $85/bbl (2024); cold-chain utilization >80% with EU driver shortfall ~350,000, boosting logistics supplier power.

| Metric | 2024 |

|---|---|

| Feed share | ~60% |

| Soy export share (Brazil+US) | ~80% |

| Top-3 genetics | ~80% |

| Brent | $85/bbl |

| Cold-chain peak use | >80% |

| EU driver shortfall | ~350,000 |

What is included in the product

Uncovers key competitive drivers—rivalry, supplier and buyer power, threat of entrants and substitutes—tailored to Scandi’s market position. Identifies disruptive threats, pricing pressures and entry barriers, delivered in fully editable Word format for business plans, investor decks and strategic reports.

A concise one-sheet Scandi Porter's Five Forces summary that visualizes competitive pressure with an editable spider chart, lets you tweak force levels for shifting market trends or regulations, and copies cleanly into decks—no macros required.

Customers Bargaining Power

Retail consolidation

Nordic and Irish grocery sectors are highly consolidated, concentrating purchasing power: NorgesGruppen ≈43% in Norway, ICA ≈36% in Sweden and S‑Group ≈46% in Finland (2024), while Ireland’s top three grocers account for roughly 80% of the market. Large chains aggressively negotiate price, promotional funding and shelf space, leveraging scale to extract concessions. Suppliers become volume‑dependent, increasing exposure to a few accounts. Joint buying alliances further amplify retailer bargaining power.

Private label power

Private label penetration in Scandinavian poultry reached c.50% of retail volume in 2024, driving a largely price-led category where retailers use private brands to compress supplier margins. Retailers can threaten insourcing or shift to alternative co-packers, increasing supplier bargaining pressure and margin volatility. Branded value-adds (marinated, convenience) preserve premium pockets, but core cuts remain commoditized. Differentiation via higher welfare, certified origin, and sustainability claims can reduce price elasticity and defend premiums.

Foodservice tenders

QSRs and contract caterers allocate volumes via competitive tenders that often award millions in annual supply; contracts commonly run 3–5 years with renewal options (2024). Standardized specs and dual-sourcing keep switching costs low, enabling buyers to drive down prices. Menu price sensitivity—food costs typically 25–35% of sales—feeds tight procurement terms. Long contracts give volume visibility but restrict pricing flexibility.

Industrial buyers

Industrial buyers can pivot to alternative origins, using EU imports (~1.1 Mt in 2024) as a price benchmark that amplifies downward pressure; technical specs are strict but broadly achievable, shifting negotiation focus to reliability. Value is driven more by OTIF (industry targets >98% in 2024) and consistent supply than by lowest unit price alone.

- Benchmark: EU imports ~1.1 Mt (2024)

- OTIF: industry target >98% (2024)

- Specs: stringent but reachable

- Buyers leverage origin flexibility to pressure margins

Consumer frugality

End-demand is highly price elastic in staples; Kantar 2024 reports promotions drive roughly 35% of grocery volume, amplifying sensitivity to price cuts.

Promotions shift mix and velocity, prompting retailers to request category funding from suppliers to sustain shelf presence and turnover.

Premium convenience lines see down‑trading during weak macro cycles, while clear provenance and welfare claims preserve some pricing power.

- Elasticity: high in staples

- Promotions: ~35% grocery volume (Kantar 2024)

- Down‑trading: affects premium convenience

- Provenance/welfare: supports price retention

Retailer concentration and private labels squeeze poultry suppliers; promotions shift leverage

Retailer concentration and scale give buyers strong leverage (NorgesGruppen 43%, ICA 36%, S‑Group 46%, Ireland top3 ~80% in 2024), enabling aggressive price, promo funding and shelf terms. High private‑label share in poultry (~50% volume) and easy origin substitution (EU imports ~1.1 Mt) compress supplier margins; OTIF (>98%) and promotions (~35% grocery volume) shift negotiations toward reliability and funding. Premiums retain some defense via provenance/welfare claims.

| Metric | 2024 |

|---|---|

| NorgesGruppen share | ≈43% |

| ICA share | ≈36% |

| S‑Group share | ≈46% |

| Ireland top3 | ≈80% |

| Private‑label poultry | ≈50% vol |

| EU imports | ≈1.1 Mt |

| Promotions (Kantar) | ≈35% vol |

| OTIF target | >98% |

Preview Before You Purchase

Scandi Porter's Five Forces Analysis

This Scandi Porter's Five Forces Analysis provides a concise, professional assessment of competitive forces affecting Scandinavian markets, covering supplier and buyer power, rivalry, substitutes, and barriers to entry. The preview here is the exact document you’ll receive immediately after purchase—fully formatted and ready to use. No placeholders, no samples, just the final deliverable for instant download.