Scandi PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our Scandi PESTLE Analysis—three to five concise insights into political, economic, social, technological, legal, and environmental forces shaping the company's future. Ideal for investors and strategists, it highlights risks and growth levers you can act on today. Purchase the full report for the complete, ready-to-use breakdown and immediate download.

Political factors

EU agri-food and trade policy

Common EU agri-food rules (CAP 2021-27 budget ~EUR 387bn) shape tariffs, subsidies and veterinary standards across Scandi Standard’s markets. CAP reforms and import quotas directly affect input costs and competitive dynamics for processors and farmers. Shifts in trade with non-EU feed exporters—EU soy imports ~15 Mt in 2023—can quickly ripple through feed and meat pricing. The firm must sustain lobbying and compliance alignment across Sweden, Denmark, Ireland, Lithuania, Finland and EEA-linked Norway.

Animal welfare agenda

Nordic and Irish politics prioritize high animal welfare, shaping stocking densities, approved stunning methods and transport rules. Tightening standards can raise compliance costs while supporting premium pricing and market access. Public funding under the CAP 2021-27 budget (€387bn) can subsidize welfare upgrades. Proactive engagement with authorities reduces risk of abrupt regulatory shocks.

Food security and self-sufficiency

Post-crisis policy across Scandinavia emphasizes resilient domestic protein supply, with governments promoting local sourcing, strategic stocks and protection of slaughter and processing as critical infrastructure; Norway and Sweden increased contingency budgets in 2024 (combined ~NOK/SEK 2.5bn) to support these measures.

Energy and climate policy support

State incentives for electrification, heat recovery and renewables in Scandinavia cut processing emissions and lower upfront barriers while Norway already sources over 90% of power from renewables. The EU ETS carbon price averaged about €90/tCO2 in 2024 and energy taxes materially shift plant-level economics. Access to green grants boosts margins and brand equity; stable policy steers long-term capex.

- EU ETS ~€90/tCO2 (2024)

- Norway >90% renewable power

- Grants improve margins & reputation

- Policy stability required for capex planning

Geopolitical risk and sanctions

War and sanctions have disrupted grain, fertilizer and logistics flows—Russia and Ukraine together supplied about 25% of global wheat exports pre-2022—pushing feed and energy costs and causing fertilizer prices to spike up to 200–300% in 2022–23. Governments may impose export controls or emergency measures; procurement must use political-risk hedging and contractual protections. Diversified sourcing and buffer inventories materially cut exposure and price volatility.

- Tag: grain_supply_risk

- Tag: fertilizer_price_shock

- Tag: export_controls

- Tag: political_hedging

- Tag: sourcing_diversification

Nordic agri risks: EU CAP, ETS and trade shocks reshaping costs and market access

Political drivers—CAP (2021–27 budget €387bn) plus national welfare laws and green incentives shape costs, margins and market access across Sweden, Denmark, Ireland, Finland, Lithuania and Norway. Trade shocks (EU soy ~15 Mt 2023; Russia/Ukraine ~25% pre‑2022 wheat) and sanctions raised feed/fertilizer volatility, prompting contingency budgets (~NOK/SEK 2.5bn in 2024). EU ETS ~€90/tCO2 (2024) and renewables (>90% Norway) affect capex and operating costs.

| Indicator | Value |

|---|---|

| CAP budget | €387bn |

| EU ETS (2024) | €90/tCO2 |

| EU soy imports (2023) | ~15 Mt |

What is included in the product

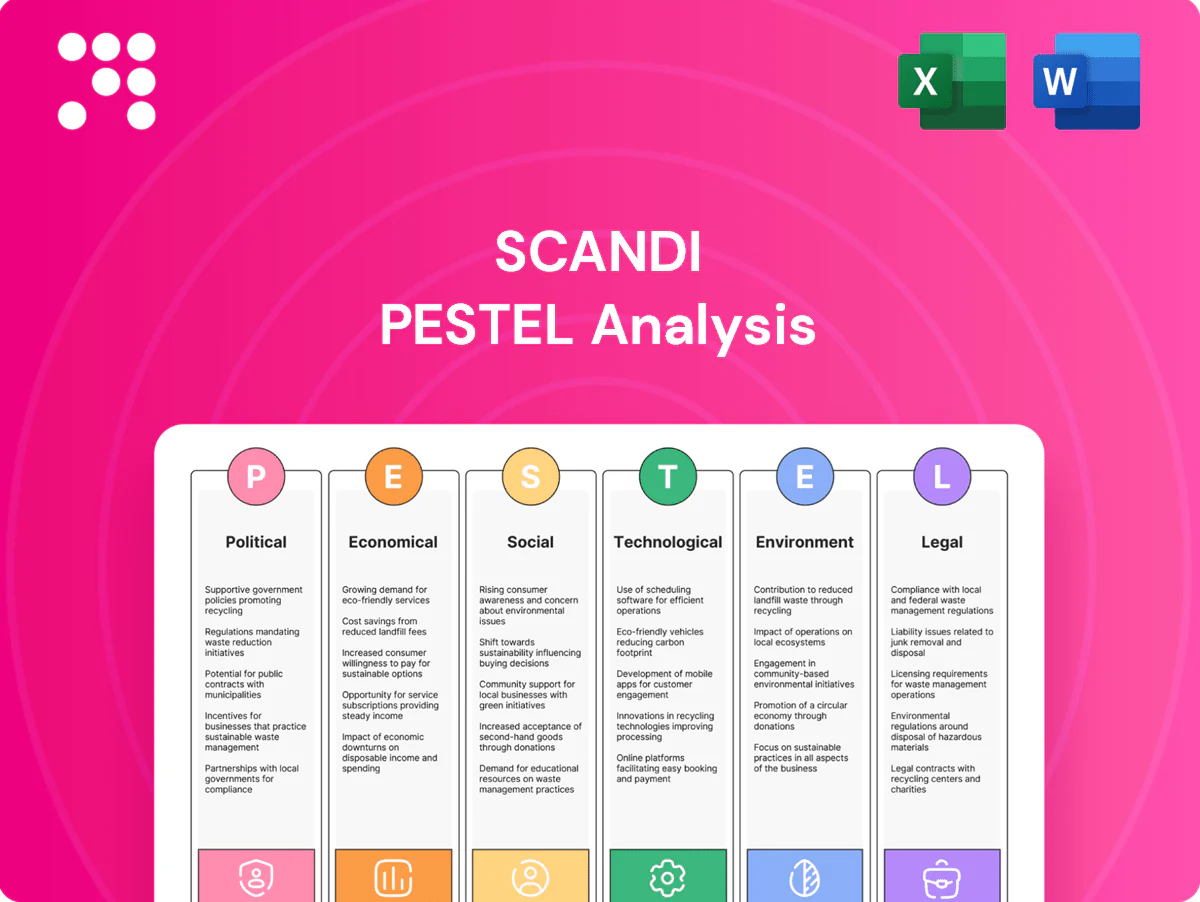

Explores how external macro-environmental factors uniquely affect Scandi across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and detailed subpoints tailored to the business; designed for executives, consultants and investors, it delivers forward-looking insights for scenario planning, risk mitigation and opportunity capture, formatted for direct use in plans and decks.

A concise, visually segmented Scandi PESTLE summary that’s editable and shareable, enabling quick alignment across teams and clear communication of external risks and market positioning during planning sessions.

Economic factors

Feed and input cost volatility

Feed accounts for about 65% of broiler cost of goods, with corn and soymeal the primary cost drivers; spikes in these commodities directly compress margins. Hedging via futures and long-term supply contracts is therefore essential for integrators. Fertilizer and energy price shocks (fertilizer rose >50% in 2021–22) amplify input volatility. Improving feed conversion ratio remains a core profit lever.

Consumer inflation and trading down

High food inflation in Scandi markets (around 6% average in 2024 per Nordic statistics) is shifting shoppers from premium to value SKUs, boosting private-label penetration. Poultry typically gains share versus red meat in downturns, supporting protein affordability. Balanced mix across retail, foodservice and industry cushions volume swings. Promotional intensity and smaller pack sizes become decisive for retaining price-sensitive consumers.

Currency exposure (SEK, NOK, DKK, EUR)

Multi-currency operations across SEK, NOK, DKK and EUR create both translation and transaction risk that can materially affect reported margins. Many inputs are EUR-priced while sales remain in Nordic currencies, so hedging strategies must match exposure timing; DKK remains pegged to EUR at 7.46038 DKK per EUR. FX moves can quickly alter competitiveness versus imports, so treasury policy must align with procurement/payment cycles and tenor.

Labor availability and wages

Tight Nordic labor markets in 2024 pushed processing and logistics costs higher as firms faced low vacancy buffers and average wage growth near 3–5% year-on-year; automation investments offset wage inflation but require significant CAPEX and 2–5 year payback horizons. Migrant labor policy changes altered plant staffing flexibility, while targeted training and retention cut overtime and quality variance.

- Wage growth 2024 ~3–5%

- Automation CAPEX with 2–5y payback

- Migrant-policy affects staffing flexibility

- Training reduces OT and quality variance

Interest rates and capex cycles

- Higher policy rates: Riksbank ~4.0%, Norges ~4.25%

- Stricter payback: favor <3–5 year projects

- Cash-flow focus: maintenance over expansion

- Green finance: −20–40 bps cheaper

Nordic agri risks: EU CAP, ETS and trade shocks reshaping costs and market access

Feed ~65% of COGS; corn/soy spikes compress margins. Food inflation ~6% (2024) shifts shoppers to value; poultry gains share. Wages 3–5% (2024); automation CAPEX 2–5y payback. Policy rates mid‑2025: Riksbank ~4.0%, Norges ~4.25%; green loans −20–40bps.

| Metric | Value |

|---|---|

| Feed share | ~65% |

| Food inflation | ~6% (2024) |

| Wage growth | 3–5% (2024) |

| Policy rates | Riksbank 4.0% / Norges 4.25% (mid‑2025) |

Preview Before You Purchase

Scandi PESTLE Analysis

The preview shown is the exact Scandi PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It includes the complete political, economic, social, technological, legal, and environmental assessments for the Scandinavian region with no placeholders or teasers. After payment you’ll instantly download this same final file, structured and professionally presented for immediate application.

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our Scandi PESTLE Analysis—three to five concise insights into political, economic, social, technological, legal, and environmental forces shaping the company's future. Ideal for investors and strategists, it highlights risks and growth levers you can act on today. Purchase the full report for the complete, ready-to-use breakdown and immediate download.

Political factors

EU agri-food and trade policy

Common EU agri-food rules (CAP 2021-27 budget ~EUR 387bn) shape tariffs, subsidies and veterinary standards across Scandi Standard’s markets. CAP reforms and import quotas directly affect input costs and competitive dynamics for processors and farmers. Shifts in trade with non-EU feed exporters—EU soy imports ~15 Mt in 2023—can quickly ripple through feed and meat pricing. The firm must sustain lobbying and compliance alignment across Sweden, Denmark, Ireland, Lithuania, Finland and EEA-linked Norway.

Animal welfare agenda

Nordic and Irish politics prioritize high animal welfare, shaping stocking densities, approved stunning methods and transport rules. Tightening standards can raise compliance costs while supporting premium pricing and market access. Public funding under the CAP 2021-27 budget (€387bn) can subsidize welfare upgrades. Proactive engagement with authorities reduces risk of abrupt regulatory shocks.

Food security and self-sufficiency

Post-crisis policy across Scandinavia emphasizes resilient domestic protein supply, with governments promoting local sourcing, strategic stocks and protection of slaughter and processing as critical infrastructure; Norway and Sweden increased contingency budgets in 2024 (combined ~NOK/SEK 2.5bn) to support these measures.

Energy and climate policy support

State incentives for electrification, heat recovery and renewables in Scandinavia cut processing emissions and lower upfront barriers while Norway already sources over 90% of power from renewables. The EU ETS carbon price averaged about €90/tCO2 in 2024 and energy taxes materially shift plant-level economics. Access to green grants boosts margins and brand equity; stable policy steers long-term capex.

- EU ETS ~€90/tCO2 (2024)

- Norway >90% renewable power

- Grants improve margins & reputation

- Policy stability required for capex planning

Geopolitical risk and sanctions

War and sanctions have disrupted grain, fertilizer and logistics flows—Russia and Ukraine together supplied about 25% of global wheat exports pre-2022—pushing feed and energy costs and causing fertilizer prices to spike up to 200–300% in 2022–23. Governments may impose export controls or emergency measures; procurement must use political-risk hedging and contractual protections. Diversified sourcing and buffer inventories materially cut exposure and price volatility.

- Tag: grain_supply_risk

- Tag: fertilizer_price_shock

- Tag: export_controls

- Tag: political_hedging

- Tag: sourcing_diversification

Nordic agri risks: EU CAP, ETS and trade shocks reshaping costs and market access

Political drivers—CAP (2021–27 budget €387bn) plus national welfare laws and green incentives shape costs, margins and market access across Sweden, Denmark, Ireland, Finland, Lithuania and Norway. Trade shocks (EU soy ~15 Mt 2023; Russia/Ukraine ~25% pre‑2022 wheat) and sanctions raised feed/fertilizer volatility, prompting contingency budgets (~NOK/SEK 2.5bn in 2024). EU ETS ~€90/tCO2 (2024) and renewables (>90% Norway) affect capex and operating costs.

| Indicator | Value |

|---|---|

| CAP budget | €387bn |

| EU ETS (2024) | €90/tCO2 |

| EU soy imports (2023) | ~15 Mt |

What is included in the product

Explores how external macro-environmental factors uniquely affect Scandi across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and detailed subpoints tailored to the business; designed for executives, consultants and investors, it delivers forward-looking insights for scenario planning, risk mitigation and opportunity capture, formatted for direct use in plans and decks.

A concise, visually segmented Scandi PESTLE summary that’s editable and shareable, enabling quick alignment across teams and clear communication of external risks and market positioning during planning sessions.

Economic factors

Feed and input cost volatility

Feed accounts for about 65% of broiler cost of goods, with corn and soymeal the primary cost drivers; spikes in these commodities directly compress margins. Hedging via futures and long-term supply contracts is therefore essential for integrators. Fertilizer and energy price shocks (fertilizer rose >50% in 2021–22) amplify input volatility. Improving feed conversion ratio remains a core profit lever.

Consumer inflation and trading down

High food inflation in Scandi markets (around 6% average in 2024 per Nordic statistics) is shifting shoppers from premium to value SKUs, boosting private-label penetration. Poultry typically gains share versus red meat in downturns, supporting protein affordability. Balanced mix across retail, foodservice and industry cushions volume swings. Promotional intensity and smaller pack sizes become decisive for retaining price-sensitive consumers.

Currency exposure (SEK, NOK, DKK, EUR)

Multi-currency operations across SEK, NOK, DKK and EUR create both translation and transaction risk that can materially affect reported margins. Many inputs are EUR-priced while sales remain in Nordic currencies, so hedging strategies must match exposure timing; DKK remains pegged to EUR at 7.46038 DKK per EUR. FX moves can quickly alter competitiveness versus imports, so treasury policy must align with procurement/payment cycles and tenor.

Labor availability and wages

Tight Nordic labor markets in 2024 pushed processing and logistics costs higher as firms faced low vacancy buffers and average wage growth near 3–5% year-on-year; automation investments offset wage inflation but require significant CAPEX and 2–5 year payback horizons. Migrant labor policy changes altered plant staffing flexibility, while targeted training and retention cut overtime and quality variance.

- Wage growth 2024 ~3–5%

- Automation CAPEX with 2–5y payback

- Migrant-policy affects staffing flexibility

- Training reduces OT and quality variance

Interest rates and capex cycles

- Higher policy rates: Riksbank ~4.0%, Norges ~4.25%

- Stricter payback: favor <3–5 year projects

- Cash-flow focus: maintenance over expansion

- Green finance: −20–40 bps cheaper

Nordic agri risks: EU CAP, ETS and trade shocks reshaping costs and market access

Feed ~65% of COGS; corn/soy spikes compress margins. Food inflation ~6% (2024) shifts shoppers to value; poultry gains share. Wages 3–5% (2024); automation CAPEX 2–5y payback. Policy rates mid‑2025: Riksbank ~4.0%, Norges ~4.25%; green loans −20–40bps.

| Metric | Value |

|---|---|

| Feed share | ~65% |

| Food inflation | ~6% (2024) |

| Wage growth | 3–5% (2024) |

| Policy rates | Riksbank 4.0% / Norges 4.25% (mid‑2025) |

Preview Before You Purchase

Scandi PESTLE Analysis

The preview shown is the exact Scandi PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It includes the complete political, economic, social, technological, legal, and environmental assessments for the Scandinavian region with no placeholders or teasers. After payment you’ll instantly download this same final file, structured and professionally presented for immediate application.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our Scandi PESTLE Analysis—three to five concise insights into political, economic, social, technological, legal, and environmental forces shaping the company's future. Ideal for investors and strategists, it highlights risks and growth levers you can act on today. Purchase the full report for the complete, ready-to-use breakdown and immediate download.

Political factors

EU agri-food and trade policy

Common EU agri-food rules (CAP 2021-27 budget ~EUR 387bn) shape tariffs, subsidies and veterinary standards across Scandi Standard’s markets. CAP reforms and import quotas directly affect input costs and competitive dynamics for processors and farmers. Shifts in trade with non-EU feed exporters—EU soy imports ~15 Mt in 2023—can quickly ripple through feed and meat pricing. The firm must sustain lobbying and compliance alignment across Sweden, Denmark, Ireland, Lithuania, Finland and EEA-linked Norway.

Animal welfare agenda

Nordic and Irish politics prioritize high animal welfare, shaping stocking densities, approved stunning methods and transport rules. Tightening standards can raise compliance costs while supporting premium pricing and market access. Public funding under the CAP 2021-27 budget (€387bn) can subsidize welfare upgrades. Proactive engagement with authorities reduces risk of abrupt regulatory shocks.

Food security and self-sufficiency

Post-crisis policy across Scandinavia emphasizes resilient domestic protein supply, with governments promoting local sourcing, strategic stocks and protection of slaughter and processing as critical infrastructure; Norway and Sweden increased contingency budgets in 2024 (combined ~NOK/SEK 2.5bn) to support these measures.

Energy and climate policy support

State incentives for electrification, heat recovery and renewables in Scandinavia cut processing emissions and lower upfront barriers while Norway already sources over 90% of power from renewables. The EU ETS carbon price averaged about €90/tCO2 in 2024 and energy taxes materially shift plant-level economics. Access to green grants boosts margins and brand equity; stable policy steers long-term capex.

- EU ETS ~€90/tCO2 (2024)

- Norway >90% renewable power

- Grants improve margins & reputation

- Policy stability required for capex planning

Geopolitical risk and sanctions

War and sanctions have disrupted grain, fertilizer and logistics flows—Russia and Ukraine together supplied about 25% of global wheat exports pre-2022—pushing feed and energy costs and causing fertilizer prices to spike up to 200–300% in 2022–23. Governments may impose export controls or emergency measures; procurement must use political-risk hedging and contractual protections. Diversified sourcing and buffer inventories materially cut exposure and price volatility.

- Tag: grain_supply_risk

- Tag: fertilizer_price_shock

- Tag: export_controls

- Tag: political_hedging

- Tag: sourcing_diversification

Nordic agri risks: EU CAP, ETS and trade shocks reshaping costs and market access

Political drivers—CAP (2021–27 budget €387bn) plus national welfare laws and green incentives shape costs, margins and market access across Sweden, Denmark, Ireland, Finland, Lithuania and Norway. Trade shocks (EU soy ~15 Mt 2023; Russia/Ukraine ~25% pre‑2022 wheat) and sanctions raised feed/fertilizer volatility, prompting contingency budgets (~NOK/SEK 2.5bn in 2024). EU ETS ~€90/tCO2 (2024) and renewables (>90% Norway) affect capex and operating costs.

| Indicator | Value |

|---|---|

| CAP budget | €387bn |

| EU ETS (2024) | €90/tCO2 |

| EU soy imports (2023) | ~15 Mt |

What is included in the product

Explores how external macro-environmental factors uniquely affect Scandi across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and detailed subpoints tailored to the business; designed for executives, consultants and investors, it delivers forward-looking insights for scenario planning, risk mitigation and opportunity capture, formatted for direct use in plans and decks.

A concise, visually segmented Scandi PESTLE summary that’s editable and shareable, enabling quick alignment across teams and clear communication of external risks and market positioning during planning sessions.

Economic factors

Feed and input cost volatility

Feed accounts for about 65% of broiler cost of goods, with corn and soymeal the primary cost drivers; spikes in these commodities directly compress margins. Hedging via futures and long-term supply contracts is therefore essential for integrators. Fertilizer and energy price shocks (fertilizer rose >50% in 2021–22) amplify input volatility. Improving feed conversion ratio remains a core profit lever.

Consumer inflation and trading down

High food inflation in Scandi markets (around 6% average in 2024 per Nordic statistics) is shifting shoppers from premium to value SKUs, boosting private-label penetration. Poultry typically gains share versus red meat in downturns, supporting protein affordability. Balanced mix across retail, foodservice and industry cushions volume swings. Promotional intensity and smaller pack sizes become decisive for retaining price-sensitive consumers.

Currency exposure (SEK, NOK, DKK, EUR)

Multi-currency operations across SEK, NOK, DKK and EUR create both translation and transaction risk that can materially affect reported margins. Many inputs are EUR-priced while sales remain in Nordic currencies, so hedging strategies must match exposure timing; DKK remains pegged to EUR at 7.46038 DKK per EUR. FX moves can quickly alter competitiveness versus imports, so treasury policy must align with procurement/payment cycles and tenor.

Labor availability and wages

Tight Nordic labor markets in 2024 pushed processing and logistics costs higher as firms faced low vacancy buffers and average wage growth near 3–5% year-on-year; automation investments offset wage inflation but require significant CAPEX and 2–5 year payback horizons. Migrant labor policy changes altered plant staffing flexibility, while targeted training and retention cut overtime and quality variance.

- Wage growth 2024 ~3–5%

- Automation CAPEX with 2–5y payback

- Migrant-policy affects staffing flexibility

- Training reduces OT and quality variance

Interest rates and capex cycles

- Higher policy rates: Riksbank ~4.0%, Norges ~4.25%

- Stricter payback: favor <3–5 year projects

- Cash-flow focus: maintenance over expansion

- Green finance: −20–40 bps cheaper

Nordic agri risks: EU CAP, ETS and trade shocks reshaping costs and market access

Feed ~65% of COGS; corn/soy spikes compress margins. Food inflation ~6% (2024) shifts shoppers to value; poultry gains share. Wages 3–5% (2024); automation CAPEX 2–5y payback. Policy rates mid‑2025: Riksbank ~4.0%, Norges ~4.25%; green loans −20–40bps.

| Metric | Value |

|---|---|

| Feed share | ~65% |

| Food inflation | ~6% (2024) |

| Wage growth | 3–5% (2024) |

| Policy rates | Riksbank 4.0% / Norges 4.25% (mid‑2025) |

Preview Before You Purchase

Scandi PESTLE Analysis

The preview shown is the exact Scandi PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It includes the complete political, economic, social, technological, legal, and environmental assessments for the Scandinavian region with no placeholders or teasers. After payment you’ll instantly download this same final file, structured and professionally presented for immediate application.