Scandza AS PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain competitive insight with our PESTLE analysis of Scandza AS—revealing how political, economic, social, technological, legal and environmental forces shape strategy and risk. Ideal for investors, consultants and planners, it’s ready-to-use and fully sourced. Purchase the full report to access detailed, actionable intelligence and downloadable charts.

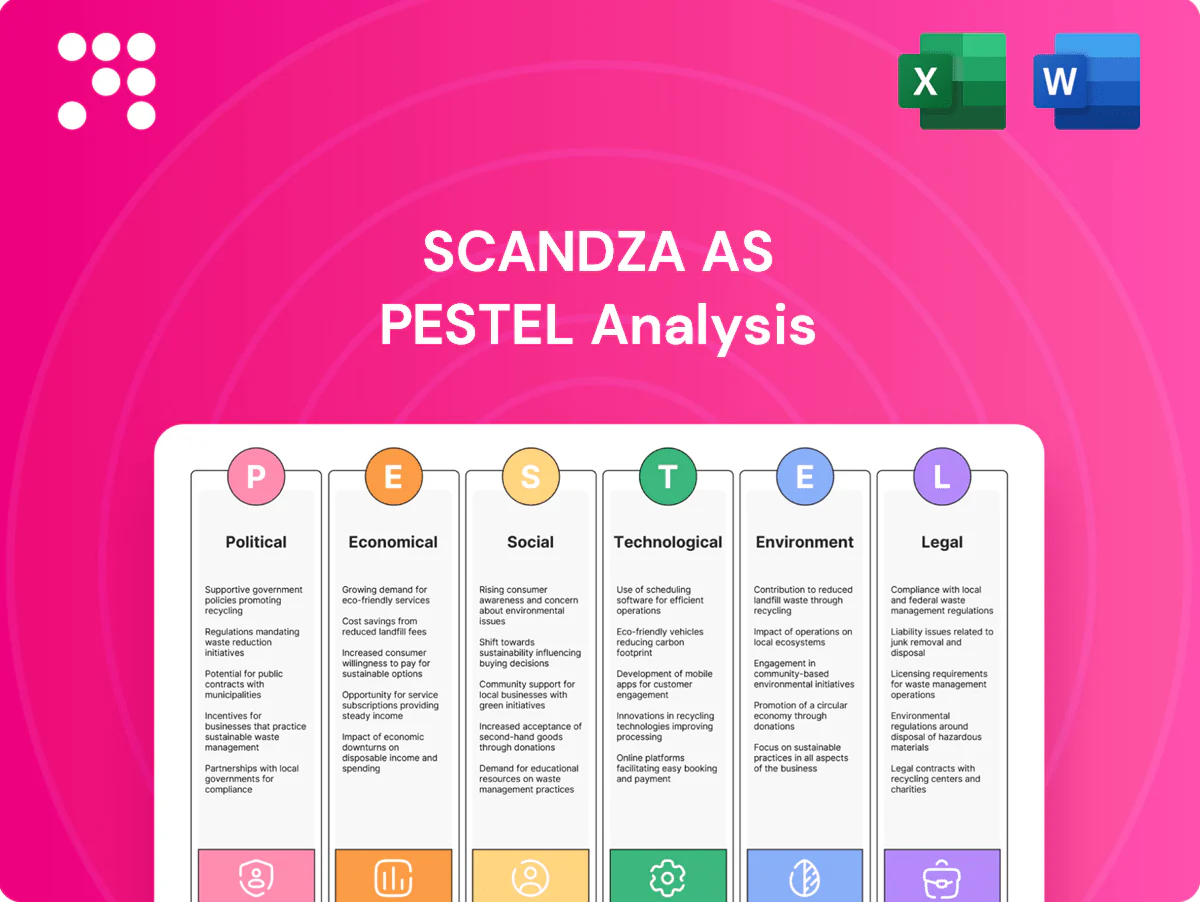

Political factors

Stable Nordic governance

Stable Nordic governance provides predictable policy environments that support long-term brand building; Transparency International CPI 2024 places Finland and Denmark among the top 5 (≈88–90), reflecting low corruption and policy continuity. Strong institutions reduce regulatory volatility for FMCG, allowing Scandza to plan capex, marketing and acquisitions with lower political risk. Regional coordination across Nordic markets eases cross-border portfolio management.

EEA/EU food policy alignment

Norway’s EEA alignment (EEA Agreement, 1994) brings EU food safety and labeling rules into scope, reducing multi-market compliance friction for Scandza and its brands. Harmonization simplifies cross-border sales but EU reforms can force reformulations or label changes; the EU Green Deal targets climate neutrality by 2050 and the Farm-to-Fork strategy includes a 50% reduction in chemical pesticide use by 2030. Scandza must track regulatory timelines and compliance costs.

Health taxation and sin levies

Several Nordic markets apply sugar or confectionery taxes, shifting price elasticity and category mix in beverages, snacks and sweets. WHO recommends fiscal measures that raise retail prices by roughly 20% to reduce consumption, so levies can materially affect demand. Scandza may need reformulation and pack-price architecture changes, and proactive stakeholder engagement can shape future levy design.

Agricultural and fisheries policy

Local agricultural and fisheries policies—including Norway's roughly NOK 18 billion in farm support and quota systems set by ICES/Norwegian authorities—directly affect input costs for dairy, grains and seafood; 2024 seafood exports near NOK 150 billion illustrate supplier importance. Policy shifts can rapidly alter supplier economics and availability, so Scandza leverages local sourcing narratives while hedging subsidy risk through supplier diversification and long-term contracts.

- Subsidies: ~NOK 18bn (2024)

- Seafood export scale: ~NOK 150bn (2024)

- Risk: quota/policy shifts affect costs

- Mitigation: local sourcing + diversified suppliers

Geopolitical supply chain risk

Baltic and broader European tensions risk disrupting energy, grain and logistics flows; the EU imported about 40% of its gas from Russia pre-2022 and Russian trade links have since sharply contracted, with EU goods exports to Russia down roughly 46% in 2022 (Eurostat). Sanctions and trade restrictions reroute shipments and raise costs, so Scandza must hold alternative suppliers and safety stocks. Scenario planning and stress tests support continuity of service under route and energy shocks.

- Supply diversification

- Maintain safety stock levels

- Run scenario stress tests

Nordic stability (CPI 88–90) vs EU green rules, levies and Russia risk

Stable Nordic governance (CPI 2024: Finland/Denmark ≈88–90) lowers political risk for Scandza while EEA/EU rules (Farm-to-Fork, Green Deal) raise compliance costs. Sugar/confectionery levies and regional agri/fish subsidies (Norway ~NOK 18bn; seafood exports ~NOK 150bn in 2024) affect input costs. Russia-related trade shifts (EU exports to Russia −46% in 2022) increase supply and energy risk.

| Indicator | Value/Year |

|---|---|

| CPI Nordic | ≈88–90 (2024) |

| Norway farm support | ~NOK 18bn (2024) |

| Norway seafood exports | ~NOK 150bn (2024) |

| EU→Russia exports | −46% (2022) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Scandza AS across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with region- and industry-specific data and trends. Designed for executives, consultants and investors, each section delivers detailed sub-points, forward-looking insights and clean formatting ready for business plans, pitch decks or internal reports.

A concise, visually segmented PESTLE summary of Scandza AS for quick reference in meetings and presentations, easily editable for local context and shareable across teams to streamline external risk discussion and strategic alignment.

Economic factors

Inflation and consumer trade-down

High food inflation (Eurozone ~8.5% y/y in 2024, Eurostat) drives private-label substitution and pack-size sensitivity, forcing Scandza to prioritize value offers. Scandza must balance price moves with clear value propositions to avoid brand deterioration. Active mix management and tighter promo efficiency (lower promo depth, higher ROI) become critical. Cost-productivity programs protect margins while preserving brand equity.

FX volatility in NOK/SEK/DKK/EUR

FX volatility in NOK/SEK/DKK/EUR (annualized volatility ~10% for NOK/SEK vs EUR 2022–24) directly shifts imported input costs and consolidated results, creating +/-10% profit swings in exposed segments. Natural hedging via local sourcing can cut currency exposure by up to 50%. Financial hedges (typically covering 60–80% of forecast flows) stabilize COGS and EBITDA. Pricing corridors should reflect realistic FX pass-through capacity of ~60%+.

Energy and logistics costs

Manufacturing and cold-chain energy costs materially compress margins for Scandza AS, with Nordic wholesale power averaging about €50–70/MWh in 2024 and industrial electricity/thermal consumption often representing 8–12% of food COGS. Fuel and freight volatility—EU diesel ~€1.50–1.70/L in 2024—directly affects distribution to Nordic retail networks. Energy-efficiency CAPEX (refrigeration upgrades, heat recovery) commonly yields 2–4 year paybacks. Network and routing optimization can cut logistics costs 10–20%, mitigating spikes.

Retailer consolidation and bargaining power

Nordic grocery concentration pressures trade terms and shelf space; ICA held about 36% of Sweden’s market in 2023 and NorgesGruppen roughly 48% in Norway in 2023, enabling chains to demand better margins and limited listings. Strong local brands can leverage sales data to secure premium visibility and joint business planning aligns promotions with measurable ROI. Expanding into convenience formats and e-commerce reduces dependency on a few dominant chains.

- Concentration: ICA 36% (SE 2023), NorgesGruppen ~48% (NO 2023)

- Negotiation: local brands win better shelf placement

- JBP: ties promotions to ROI

- Diversify: convenience + e-commerce to lower chain reliance

M&A cycle and valuations

Higher policy rates (Fed ~5.25–5.50% and ECB ~4.00% in 2024) compressed buyout multiples to roughly 8–9x EV/EBITDA on average in 2024, lowering valuations and slowing deal volume; tighter credit pushed deal activity down ~20% in Nordic markets in 2024, creating selective acquisition openings. Scandza’s platform model benefits from bolt-on M&A where synergies boost consolidated margins, and disciplined diligence preserves projected value creation.

- rate-impact: Fed/ECB 2024 ~5.25–5.50% / ~4.00%

- multiples: ~8–9x EV/EBITDA (2024)

- opportunity: Nordic deal volume down ~20% (2024)

Nordic stability (CPI 88–90) vs EU green rules, levies and Russia risk

High food inflation (Eurozone ~8.5% y/y 2024) plus NOK/SEK ~10% FX vol (2022–24) squeeze margins, forcing value packs and promo efficiency; energy (€50–70/MWh 2024) and diesel (€1.50–1.70/L 2024) raise COGS. Nordic retail concentration (ICA 36% SE 2023; NorgesGruppen 48% NO 2023) tightens terms. Higher rates (Fed ~5.25–5.5%, ECB ~4% 2024) cut multiples to ~8–9x; deal flow -20% (2024).

| Metric | Value |

|---|---|

| Food inflation | ~8.5% y/y (2024) |

| FX vol | ~10% (NOK/SEK vs EUR 2022–24) |

| Power | €50–70/MWh (2024) |

| Retail share | ICA 36% / NorgesGruppen 48% (2023) |

| Rates / multiples | Fed 5.25–5.5% • ECB ~4% • 8–9x EV/EBITDA (2024) |

Full Version Awaits

Scandza AS PESTLE Analysis

The preview shown here is the exact Scandza AS PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment with supporting data and insights. No placeholders or teasers; this is the final file available immediately after payment.

Plan Smarter. Present Sharper. Compete Stronger.

Gain competitive insight with our PESTLE analysis of Scandza AS—revealing how political, economic, social, technological, legal and environmental forces shape strategy and risk. Ideal for investors, consultants and planners, it’s ready-to-use and fully sourced. Purchase the full report to access detailed, actionable intelligence and downloadable charts.

Political factors

Stable Nordic governance

Stable Nordic governance provides predictable policy environments that support long-term brand building; Transparency International CPI 2024 places Finland and Denmark among the top 5 (≈88–90), reflecting low corruption and policy continuity. Strong institutions reduce regulatory volatility for FMCG, allowing Scandza to plan capex, marketing and acquisitions with lower political risk. Regional coordination across Nordic markets eases cross-border portfolio management.

EEA/EU food policy alignment

Norway’s EEA alignment (EEA Agreement, 1994) brings EU food safety and labeling rules into scope, reducing multi-market compliance friction for Scandza and its brands. Harmonization simplifies cross-border sales but EU reforms can force reformulations or label changes; the EU Green Deal targets climate neutrality by 2050 and the Farm-to-Fork strategy includes a 50% reduction in chemical pesticide use by 2030. Scandza must track regulatory timelines and compliance costs.

Health taxation and sin levies

Several Nordic markets apply sugar or confectionery taxes, shifting price elasticity and category mix in beverages, snacks and sweets. WHO recommends fiscal measures that raise retail prices by roughly 20% to reduce consumption, so levies can materially affect demand. Scandza may need reformulation and pack-price architecture changes, and proactive stakeholder engagement can shape future levy design.

Agricultural and fisheries policy

Local agricultural and fisheries policies—including Norway's roughly NOK 18 billion in farm support and quota systems set by ICES/Norwegian authorities—directly affect input costs for dairy, grains and seafood; 2024 seafood exports near NOK 150 billion illustrate supplier importance. Policy shifts can rapidly alter supplier economics and availability, so Scandza leverages local sourcing narratives while hedging subsidy risk through supplier diversification and long-term contracts.

- Subsidies: ~NOK 18bn (2024)

- Seafood export scale: ~NOK 150bn (2024)

- Risk: quota/policy shifts affect costs

- Mitigation: local sourcing + diversified suppliers

Geopolitical supply chain risk

Baltic and broader European tensions risk disrupting energy, grain and logistics flows; the EU imported about 40% of its gas from Russia pre-2022 and Russian trade links have since sharply contracted, with EU goods exports to Russia down roughly 46% in 2022 (Eurostat). Sanctions and trade restrictions reroute shipments and raise costs, so Scandza must hold alternative suppliers and safety stocks. Scenario planning and stress tests support continuity of service under route and energy shocks.

- Supply diversification

- Maintain safety stock levels

- Run scenario stress tests

Nordic stability (CPI 88–90) vs EU green rules, levies and Russia risk

Stable Nordic governance (CPI 2024: Finland/Denmark ≈88–90) lowers political risk for Scandza while EEA/EU rules (Farm-to-Fork, Green Deal) raise compliance costs. Sugar/confectionery levies and regional agri/fish subsidies (Norway ~NOK 18bn; seafood exports ~NOK 150bn in 2024) affect input costs. Russia-related trade shifts (EU exports to Russia −46% in 2022) increase supply and energy risk.

| Indicator | Value/Year |

|---|---|

| CPI Nordic | ≈88–90 (2024) |

| Norway farm support | ~NOK 18bn (2024) |

| Norway seafood exports | ~NOK 150bn (2024) |

| EU→Russia exports | −46% (2022) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Scandza AS across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with region- and industry-specific data and trends. Designed for executives, consultants and investors, each section delivers detailed sub-points, forward-looking insights and clean formatting ready for business plans, pitch decks or internal reports.

A concise, visually segmented PESTLE summary of Scandza AS for quick reference in meetings and presentations, easily editable for local context and shareable across teams to streamline external risk discussion and strategic alignment.

Economic factors

Inflation and consumer trade-down

High food inflation (Eurozone ~8.5% y/y in 2024, Eurostat) drives private-label substitution and pack-size sensitivity, forcing Scandza to prioritize value offers. Scandza must balance price moves with clear value propositions to avoid brand deterioration. Active mix management and tighter promo efficiency (lower promo depth, higher ROI) become critical. Cost-productivity programs protect margins while preserving brand equity.

FX volatility in NOK/SEK/DKK/EUR

FX volatility in NOK/SEK/DKK/EUR (annualized volatility ~10% for NOK/SEK vs EUR 2022–24) directly shifts imported input costs and consolidated results, creating +/-10% profit swings in exposed segments. Natural hedging via local sourcing can cut currency exposure by up to 50%. Financial hedges (typically covering 60–80% of forecast flows) stabilize COGS and EBITDA. Pricing corridors should reflect realistic FX pass-through capacity of ~60%+.

Energy and logistics costs

Manufacturing and cold-chain energy costs materially compress margins for Scandza AS, with Nordic wholesale power averaging about €50–70/MWh in 2024 and industrial electricity/thermal consumption often representing 8–12% of food COGS. Fuel and freight volatility—EU diesel ~€1.50–1.70/L in 2024—directly affects distribution to Nordic retail networks. Energy-efficiency CAPEX (refrigeration upgrades, heat recovery) commonly yields 2–4 year paybacks. Network and routing optimization can cut logistics costs 10–20%, mitigating spikes.

Retailer consolidation and bargaining power

Nordic grocery concentration pressures trade terms and shelf space; ICA held about 36% of Sweden’s market in 2023 and NorgesGruppen roughly 48% in Norway in 2023, enabling chains to demand better margins and limited listings. Strong local brands can leverage sales data to secure premium visibility and joint business planning aligns promotions with measurable ROI. Expanding into convenience formats and e-commerce reduces dependency on a few dominant chains.

- Concentration: ICA 36% (SE 2023), NorgesGruppen ~48% (NO 2023)

- Negotiation: local brands win better shelf placement

- JBP: ties promotions to ROI

- Diversify: convenience + e-commerce to lower chain reliance

M&A cycle and valuations

Higher policy rates (Fed ~5.25–5.50% and ECB ~4.00% in 2024) compressed buyout multiples to roughly 8–9x EV/EBITDA on average in 2024, lowering valuations and slowing deal volume; tighter credit pushed deal activity down ~20% in Nordic markets in 2024, creating selective acquisition openings. Scandza’s platform model benefits from bolt-on M&A where synergies boost consolidated margins, and disciplined diligence preserves projected value creation.

- rate-impact: Fed/ECB 2024 ~5.25–5.50% / ~4.00%

- multiples: ~8–9x EV/EBITDA (2024)

- opportunity: Nordic deal volume down ~20% (2024)

Nordic stability (CPI 88–90) vs EU green rules, levies and Russia risk

High food inflation (Eurozone ~8.5% y/y 2024) plus NOK/SEK ~10% FX vol (2022–24) squeeze margins, forcing value packs and promo efficiency; energy (€50–70/MWh 2024) and diesel (€1.50–1.70/L 2024) raise COGS. Nordic retail concentration (ICA 36% SE 2023; NorgesGruppen 48% NO 2023) tightens terms. Higher rates (Fed ~5.25–5.5%, ECB ~4% 2024) cut multiples to ~8–9x; deal flow -20% (2024).

| Metric | Value |

|---|---|

| Food inflation | ~8.5% y/y (2024) |

| FX vol | ~10% (NOK/SEK vs EUR 2022–24) |

| Power | €50–70/MWh (2024) |

| Retail share | ICA 36% / NorgesGruppen 48% (2023) |

| Rates / multiples | Fed 5.25–5.5% • ECB ~4% • 8–9x EV/EBITDA (2024) |

Full Version Awaits

Scandza AS PESTLE Analysis

The preview shown here is the exact Scandza AS PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment with supporting data and insights. No placeholders or teasers; this is the final file available immediately after payment.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain competitive insight with our PESTLE analysis of Scandza AS—revealing how political, economic, social, technological, legal and environmental forces shape strategy and risk. Ideal for investors, consultants and planners, it’s ready-to-use and fully sourced. Purchase the full report to access detailed, actionable intelligence and downloadable charts.

Political factors

Stable Nordic governance

Stable Nordic governance provides predictable policy environments that support long-term brand building; Transparency International CPI 2024 places Finland and Denmark among the top 5 (≈88–90), reflecting low corruption and policy continuity. Strong institutions reduce regulatory volatility for FMCG, allowing Scandza to plan capex, marketing and acquisitions with lower political risk. Regional coordination across Nordic markets eases cross-border portfolio management.

EEA/EU food policy alignment

Norway’s EEA alignment (EEA Agreement, 1994) brings EU food safety and labeling rules into scope, reducing multi-market compliance friction for Scandza and its brands. Harmonization simplifies cross-border sales but EU reforms can force reformulations or label changes; the EU Green Deal targets climate neutrality by 2050 and the Farm-to-Fork strategy includes a 50% reduction in chemical pesticide use by 2030. Scandza must track regulatory timelines and compliance costs.

Health taxation and sin levies

Several Nordic markets apply sugar or confectionery taxes, shifting price elasticity and category mix in beverages, snacks and sweets. WHO recommends fiscal measures that raise retail prices by roughly 20% to reduce consumption, so levies can materially affect demand. Scandza may need reformulation and pack-price architecture changes, and proactive stakeholder engagement can shape future levy design.

Agricultural and fisheries policy

Local agricultural and fisheries policies—including Norway's roughly NOK 18 billion in farm support and quota systems set by ICES/Norwegian authorities—directly affect input costs for dairy, grains and seafood; 2024 seafood exports near NOK 150 billion illustrate supplier importance. Policy shifts can rapidly alter supplier economics and availability, so Scandza leverages local sourcing narratives while hedging subsidy risk through supplier diversification and long-term contracts.

- Subsidies: ~NOK 18bn (2024)

- Seafood export scale: ~NOK 150bn (2024)

- Risk: quota/policy shifts affect costs

- Mitigation: local sourcing + diversified suppliers

Geopolitical supply chain risk

Baltic and broader European tensions risk disrupting energy, grain and logistics flows; the EU imported about 40% of its gas from Russia pre-2022 and Russian trade links have since sharply contracted, with EU goods exports to Russia down roughly 46% in 2022 (Eurostat). Sanctions and trade restrictions reroute shipments and raise costs, so Scandza must hold alternative suppliers and safety stocks. Scenario planning and stress tests support continuity of service under route and energy shocks.

- Supply diversification

- Maintain safety stock levels

- Run scenario stress tests

Nordic stability (CPI 88–90) vs EU green rules, levies and Russia risk

Stable Nordic governance (CPI 2024: Finland/Denmark ≈88–90) lowers political risk for Scandza while EEA/EU rules (Farm-to-Fork, Green Deal) raise compliance costs. Sugar/confectionery levies and regional agri/fish subsidies (Norway ~NOK 18bn; seafood exports ~NOK 150bn in 2024) affect input costs. Russia-related trade shifts (EU exports to Russia −46% in 2022) increase supply and energy risk.

| Indicator | Value/Year |

|---|---|

| CPI Nordic | ≈88–90 (2024) |

| Norway farm support | ~NOK 18bn (2024) |

| Norway seafood exports | ~NOK 150bn (2024) |

| EU→Russia exports | −46% (2022) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Scandza AS across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with region- and industry-specific data and trends. Designed for executives, consultants and investors, each section delivers detailed sub-points, forward-looking insights and clean formatting ready for business plans, pitch decks or internal reports.

A concise, visually segmented PESTLE summary of Scandza AS for quick reference in meetings and presentations, easily editable for local context and shareable across teams to streamline external risk discussion and strategic alignment.

Economic factors

Inflation and consumer trade-down

High food inflation (Eurozone ~8.5% y/y in 2024, Eurostat) drives private-label substitution and pack-size sensitivity, forcing Scandza to prioritize value offers. Scandza must balance price moves with clear value propositions to avoid brand deterioration. Active mix management and tighter promo efficiency (lower promo depth, higher ROI) become critical. Cost-productivity programs protect margins while preserving brand equity.

FX volatility in NOK/SEK/DKK/EUR

FX volatility in NOK/SEK/DKK/EUR (annualized volatility ~10% for NOK/SEK vs EUR 2022–24) directly shifts imported input costs and consolidated results, creating +/-10% profit swings in exposed segments. Natural hedging via local sourcing can cut currency exposure by up to 50%. Financial hedges (typically covering 60–80% of forecast flows) stabilize COGS and EBITDA. Pricing corridors should reflect realistic FX pass-through capacity of ~60%+.

Energy and logistics costs

Manufacturing and cold-chain energy costs materially compress margins for Scandza AS, with Nordic wholesale power averaging about €50–70/MWh in 2024 and industrial electricity/thermal consumption often representing 8–12% of food COGS. Fuel and freight volatility—EU diesel ~€1.50–1.70/L in 2024—directly affects distribution to Nordic retail networks. Energy-efficiency CAPEX (refrigeration upgrades, heat recovery) commonly yields 2–4 year paybacks. Network and routing optimization can cut logistics costs 10–20%, mitigating spikes.

Retailer consolidation and bargaining power

Nordic grocery concentration pressures trade terms and shelf space; ICA held about 36% of Sweden’s market in 2023 and NorgesGruppen roughly 48% in Norway in 2023, enabling chains to demand better margins and limited listings. Strong local brands can leverage sales data to secure premium visibility and joint business planning aligns promotions with measurable ROI. Expanding into convenience formats and e-commerce reduces dependency on a few dominant chains.

- Concentration: ICA 36% (SE 2023), NorgesGruppen ~48% (NO 2023)

- Negotiation: local brands win better shelf placement

- JBP: ties promotions to ROI

- Diversify: convenience + e-commerce to lower chain reliance

M&A cycle and valuations

Higher policy rates (Fed ~5.25–5.50% and ECB ~4.00% in 2024) compressed buyout multiples to roughly 8–9x EV/EBITDA on average in 2024, lowering valuations and slowing deal volume; tighter credit pushed deal activity down ~20% in Nordic markets in 2024, creating selective acquisition openings. Scandza’s platform model benefits from bolt-on M&A where synergies boost consolidated margins, and disciplined diligence preserves projected value creation.

- rate-impact: Fed/ECB 2024 ~5.25–5.50% / ~4.00%

- multiples: ~8–9x EV/EBITDA (2024)

- opportunity: Nordic deal volume down ~20% (2024)

Nordic stability (CPI 88–90) vs EU green rules, levies and Russia risk

High food inflation (Eurozone ~8.5% y/y 2024) plus NOK/SEK ~10% FX vol (2022–24) squeeze margins, forcing value packs and promo efficiency; energy (€50–70/MWh 2024) and diesel (€1.50–1.70/L 2024) raise COGS. Nordic retail concentration (ICA 36% SE 2023; NorgesGruppen 48% NO 2023) tightens terms. Higher rates (Fed ~5.25–5.5%, ECB ~4% 2024) cut multiples to ~8–9x; deal flow -20% (2024).

| Metric | Value |

|---|---|

| Food inflation | ~8.5% y/y (2024) |

| FX vol | ~10% (NOK/SEK vs EUR 2022–24) |

| Power | €50–70/MWh (2024) |

| Retail share | ICA 36% / NorgesGruppen 48% (2023) |

| Rates / multiples | Fed 5.25–5.5% • ECB ~4% • 8–9x EV/EBITDA (2024) |

Full Version Awaits

Scandza AS PESTLE Analysis

The preview shown here is the exact Scandza AS PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment with supporting data and insights. No placeholders or teasers; this is the final file available immediately after payment.