Shanghai Construction Porter's Five Forces Analysis

From Overview to Strategy Blueprint

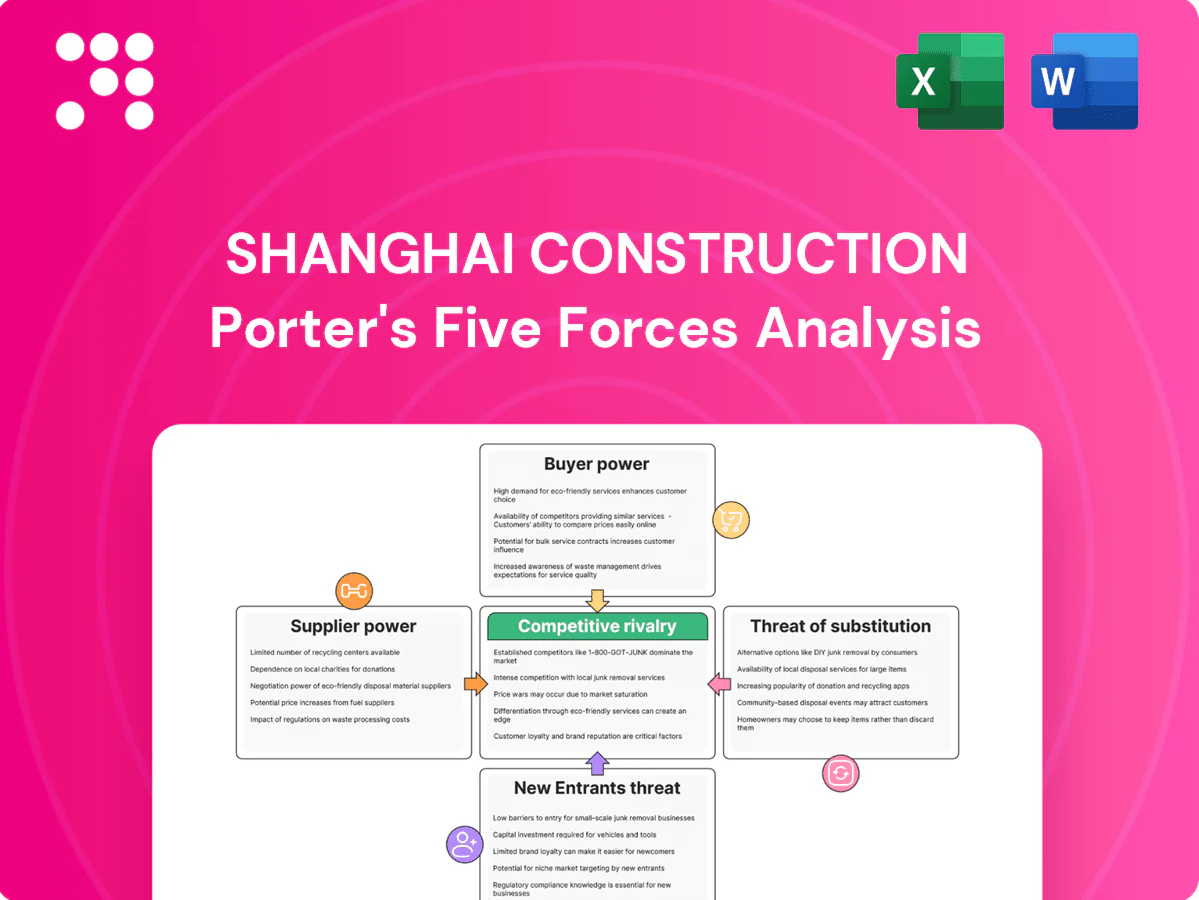

Shanghai Construction faces moderate supplier power, strong buyer bargaining in public contracts, elevated competitive rivalry, and material threats from low-cost entrants and offsite construction substitutes. This snapshot highlights strategic pressure points and operational risks that matter for investors. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Shanghai Construction.

Suppliers Bargaining Power

Concentrated core materials

Steel, cement and glass are largely supplied by a few giant, often state-linked firms—China supplies about 60% of global cement production (2023)—giving suppliers concentrated bargaining power. Volatile commodity pricing has squeezed margins on fixed-price contracts. Long-term volume contracts and financial hedges reduce exposure. SCG’s scale boosts leverage but cannot fully neutralize commodity cycles.

Specialized equipment scarcity

Specialized TBMs, heavy cranes and niche MEP systems remain concentrated among few global vendors, so as of 2024 lead times often exceed 18 months and switching costs on mega-projects are substantial. Supplier service quality directly shifts schedule risk and can trigger liquidated damages running into millions of USD per month on delayed sections. Strategic alliances and multi-vendor frameworks are used to dilute single-point dependency and shorten contingency lead times.

Skilled labor and subcontractors

Specialized trades and reputable subcontractors can command premiums in tight Shanghai markets, with 2024 industry surveys reporting up to 20% cost uplifts for scarce skills; labor mobility constraints and stricter safety compliance further add measurable overheads and schedule risk. SCG’s preferred subcontractor networks stabilize rates and quality across projects. Ongoing workforce development and increased self-perform capacity moderate supplier power.

Logistics and imported inputs

International projects depend on imported materials exposed to tariffs, FX swings and port congestion; Port of Shanghai throughput was about 43 million TEU in 2023 (SIPG), concentrating supplier leverage and delay risks that can spike mid-project. Early procurement and near-shoring reduce FX/tariff exposure, while logistics bottlenecks elevate supplier bargaining power during execution.

- Multi-sourcing

- Buffer inventories

- Early procurement

- Near-shoring

Countervailing scale and integration

In 2024 Shanghai Construction Group leverages large-scale centralized purchasing, standardized specs and e-procurement to secure better pricing and delivery terms, while partial vertical integration in design and selected fabrication reduces supplier dependence. Performance-based contracts shift quality and schedule risk back to suppliers, leaving supplier power moderate but highly project-specific.

- procurement scale: centralized sourcing, e-procurement

- integration: in-house design/fabrication reduces reliance

- contracting: performance-based risk transfer

- assessment: moderate supplier power, varies by project

Concentrated suppliers, long lead times and skilled-trade premiums tighten construction margins

Suppliers of steel/cement/glass are concentrated (China ~60% of global cement production, 2023) and commodity volatility squeezes margins; TBM/crane lead times >18 months (2024) raise switching costs; scarce trades command up to 20% premiums (2024). SCG central procurement, partial vertical integration and performance contracts keep supplier power moderate and project-specific.

| Metric | Value |

|---|---|

| Cement share (China, 2023) | ~60% |

| Port of Shanghai throughput (2023) | ~43M TEU |

| TBM/crane lead times (2024) | >18 months |

| Skilled trade premium (2024) | up to 20% |

What is included in the product

Comprehensive Porter's Five Forces assessment for Shanghai Construction, evaluating competitive rivalry, supplier and buyer power, entry barriers, and substitute threats to reveal strategic vulnerabilities, pricing pressures, and emerging disruptors shaping its profitability and market positioning.

A concise, one-sheet Porter’s Five Forces for Shanghai Construction that pinpoints competitive pain—ready to drop into decks or model scenarios, customize pressure levels with new data, compare pre/post regulation impacts, and integrate into wider reports without macros for non-finance users.

Customers Bargaining Power

Government tender dominance

In 2024 public owners in Shanghai run highly transparent, price-competitive tenders with strict prequalification barriers that filter bidders and favor lowest-compliant offers.

Lowest-compliant bids and tight KPIs — focused on safety, schedule and quality — compress margins and elevate cost-to-win pressures for contractors.

Political and social objectives frequently reshape scope and timelines, raising change-order risk; however strong reputation and documented past performance still secure value-based awards despite price competition.

Large developers and SOEs

Large private developers and SOEs buy at scale—often awarding single pipelines exceeding RMB 1 billion—so they demand favorable pricing and extended payment terms. Multi-city bundling in 2024 lets them extract deeper volume discounts and leverage procurement across provinces. Payment schedules and retention clauses (commonly 5–10%) squeeze contractor cash flow, while value engineering and EPC bundling are used to trade price reductions for narrower scope.

Payment risk and financing

Extended receivables and milestone payments—commonly stretching beyond 180 days in 2024—shift working-capital burden to contractors and elevate payment risk. Buyers with financing constraints increasingly push for deferred terms, raising bargaining power. SCG’s strong balance sheet, state-backed guarantees and PPP track record mitigate this pressure. Use of factoring and project-finance rings reduces buyer leverage and shortens cash cycles.

Quality, safety, ESG standards

Owners increasingly require green materials, BIM and safety certifications, raising compliance costs but allowing developers to differentiate; by 2024 many Tier-1 projects in China mandated BIM for design and construction coordination.

Buyers can benchmark performance against global standards and ESG metrics, pressuring contractors on quality and safety; SCG’s advanced design capability enables delivery of performance-based specs and capture of premium pricing.

- Tier-1 BIM mandate 2024: widespread on major Chinese projects

- Compliance raises costs but supports premium bids

- ESG/safety benchmarking strengthens buyer bargaining

- SCG design capability: enables premium, spec-driven wins

International and MDB clients

International and MDB clients exert high bargaining power: in 2024 multilateral banks and overseas governments reinforced strict compliance and local‑content requirements, competitive international tenders broaden bidder pools, and currency, legal and dispute frameworks favor sophisticated buyers while Shanghai Construction's cross‑border EPC experience helps rebalance terms.

- Compliance focus: stronger local‑content clauses in 2024

- Procurement: wider bidder pools via international tenders

- Legal/currency: advantage to sophisticated buyers

- Experience: cross‑border EPCs improve contract leverage

Shanghai 2024 tenders: >RMB1bn, 5–10% retention

In 2024 Shanghai owners run transparent, price‑competitive tenders (single awards often >RMB1bn) with tight KPIs, 5–10% retention and receivables commonly >180 days, compressing contractor margins. Tier‑1 BIM mandates and ESG benchmarks raise compliance costs but enable premium, spec‑driven wins; MDBs widen bidder pools and increase buyer leverage.

| Metric | 2024 |

|---|---|

| Avg single award | RMB>1bn |

| Retention | 5–10% |

| Receivables | >180 days |

Same Document Delivered

Shanghai Construction Porter's Five Forces Analysis

This preview shows the exact Shanghai Construction Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted and ready for use. The document provides a professional assessment of competitive rivalry, supplier and buyer power, and threats of new entrants and substitutes, with clear strategic implications. No placeholders or samples; instant download upon payment.

From Overview to Strategy Blueprint

Shanghai Construction faces moderate supplier power, strong buyer bargaining in public contracts, elevated competitive rivalry, and material threats from low-cost entrants and offsite construction substitutes. This snapshot highlights strategic pressure points and operational risks that matter for investors. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Shanghai Construction.

Suppliers Bargaining Power

Concentrated core materials

Steel, cement and glass are largely supplied by a few giant, often state-linked firms—China supplies about 60% of global cement production (2023)—giving suppliers concentrated bargaining power. Volatile commodity pricing has squeezed margins on fixed-price contracts. Long-term volume contracts and financial hedges reduce exposure. SCG’s scale boosts leverage but cannot fully neutralize commodity cycles.

Specialized equipment scarcity

Specialized TBMs, heavy cranes and niche MEP systems remain concentrated among few global vendors, so as of 2024 lead times often exceed 18 months and switching costs on mega-projects are substantial. Supplier service quality directly shifts schedule risk and can trigger liquidated damages running into millions of USD per month on delayed sections. Strategic alliances and multi-vendor frameworks are used to dilute single-point dependency and shorten contingency lead times.

Skilled labor and subcontractors

Specialized trades and reputable subcontractors can command premiums in tight Shanghai markets, with 2024 industry surveys reporting up to 20% cost uplifts for scarce skills; labor mobility constraints and stricter safety compliance further add measurable overheads and schedule risk. SCG’s preferred subcontractor networks stabilize rates and quality across projects. Ongoing workforce development and increased self-perform capacity moderate supplier power.

Logistics and imported inputs

International projects depend on imported materials exposed to tariffs, FX swings and port congestion; Port of Shanghai throughput was about 43 million TEU in 2023 (SIPG), concentrating supplier leverage and delay risks that can spike mid-project. Early procurement and near-shoring reduce FX/tariff exposure, while logistics bottlenecks elevate supplier bargaining power during execution.

- Multi-sourcing

- Buffer inventories

- Early procurement

- Near-shoring

Countervailing scale and integration

In 2024 Shanghai Construction Group leverages large-scale centralized purchasing, standardized specs and e-procurement to secure better pricing and delivery terms, while partial vertical integration in design and selected fabrication reduces supplier dependence. Performance-based contracts shift quality and schedule risk back to suppliers, leaving supplier power moderate but highly project-specific.

- procurement scale: centralized sourcing, e-procurement

- integration: in-house design/fabrication reduces reliance

- contracting: performance-based risk transfer

- assessment: moderate supplier power, varies by project

Concentrated suppliers, long lead times and skilled-trade premiums tighten construction margins

Suppliers of steel/cement/glass are concentrated (China ~60% of global cement production, 2023) and commodity volatility squeezes margins; TBM/crane lead times >18 months (2024) raise switching costs; scarce trades command up to 20% premiums (2024). SCG central procurement, partial vertical integration and performance contracts keep supplier power moderate and project-specific.

| Metric | Value |

|---|---|

| Cement share (China, 2023) | ~60% |

| Port of Shanghai throughput (2023) | ~43M TEU |

| TBM/crane lead times (2024) | >18 months |

| Skilled trade premium (2024) | up to 20% |

What is included in the product

Comprehensive Porter's Five Forces assessment for Shanghai Construction, evaluating competitive rivalry, supplier and buyer power, entry barriers, and substitute threats to reveal strategic vulnerabilities, pricing pressures, and emerging disruptors shaping its profitability and market positioning.

A concise, one-sheet Porter’s Five Forces for Shanghai Construction that pinpoints competitive pain—ready to drop into decks or model scenarios, customize pressure levels with new data, compare pre/post regulation impacts, and integrate into wider reports without macros for non-finance users.

Customers Bargaining Power

Government tender dominance

In 2024 public owners in Shanghai run highly transparent, price-competitive tenders with strict prequalification barriers that filter bidders and favor lowest-compliant offers.

Lowest-compliant bids and tight KPIs — focused on safety, schedule and quality — compress margins and elevate cost-to-win pressures for contractors.

Political and social objectives frequently reshape scope and timelines, raising change-order risk; however strong reputation and documented past performance still secure value-based awards despite price competition.

Large developers and SOEs

Large private developers and SOEs buy at scale—often awarding single pipelines exceeding RMB 1 billion—so they demand favorable pricing and extended payment terms. Multi-city bundling in 2024 lets them extract deeper volume discounts and leverage procurement across provinces. Payment schedules and retention clauses (commonly 5–10%) squeeze contractor cash flow, while value engineering and EPC bundling are used to trade price reductions for narrower scope.

Payment risk and financing

Extended receivables and milestone payments—commonly stretching beyond 180 days in 2024—shift working-capital burden to contractors and elevate payment risk. Buyers with financing constraints increasingly push for deferred terms, raising bargaining power. SCG’s strong balance sheet, state-backed guarantees and PPP track record mitigate this pressure. Use of factoring and project-finance rings reduces buyer leverage and shortens cash cycles.

Quality, safety, ESG standards

Owners increasingly require green materials, BIM and safety certifications, raising compliance costs but allowing developers to differentiate; by 2024 many Tier-1 projects in China mandated BIM for design and construction coordination.

Buyers can benchmark performance against global standards and ESG metrics, pressuring contractors on quality and safety; SCG’s advanced design capability enables delivery of performance-based specs and capture of premium pricing.

- Tier-1 BIM mandate 2024: widespread on major Chinese projects

- Compliance raises costs but supports premium bids

- ESG/safety benchmarking strengthens buyer bargaining

- SCG design capability: enables premium, spec-driven wins

International and MDB clients

International and MDB clients exert high bargaining power: in 2024 multilateral banks and overseas governments reinforced strict compliance and local‑content requirements, competitive international tenders broaden bidder pools, and currency, legal and dispute frameworks favor sophisticated buyers while Shanghai Construction's cross‑border EPC experience helps rebalance terms.

- Compliance focus: stronger local‑content clauses in 2024

- Procurement: wider bidder pools via international tenders

- Legal/currency: advantage to sophisticated buyers

- Experience: cross‑border EPCs improve contract leverage

Shanghai 2024 tenders: >RMB1bn, 5–10% retention

In 2024 Shanghai owners run transparent, price‑competitive tenders (single awards often >RMB1bn) with tight KPIs, 5–10% retention and receivables commonly >180 days, compressing contractor margins. Tier‑1 BIM mandates and ESG benchmarks raise compliance costs but enable premium, spec‑driven wins; MDBs widen bidder pools and increase buyer leverage.

| Metric | 2024 |

|---|---|

| Avg single award | RMB>1bn |

| Retention | 5–10% |

| Receivables | >180 days |

Same Document Delivered

Shanghai Construction Porter's Five Forces Analysis

This preview shows the exact Shanghai Construction Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted and ready for use. The document provides a professional assessment of competitive rivalry, supplier and buyer power, and threats of new entrants and substitutes, with clear strategic implications. No placeholders or samples; instant download upon payment.

Description

From Overview to Strategy Blueprint

Shanghai Construction faces moderate supplier power, strong buyer bargaining in public contracts, elevated competitive rivalry, and material threats from low-cost entrants and offsite construction substitutes. This snapshot highlights strategic pressure points and operational risks that matter for investors. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Shanghai Construction.

Suppliers Bargaining Power

Concentrated core materials

Steel, cement and glass are largely supplied by a few giant, often state-linked firms—China supplies about 60% of global cement production (2023)—giving suppliers concentrated bargaining power. Volatile commodity pricing has squeezed margins on fixed-price contracts. Long-term volume contracts and financial hedges reduce exposure. SCG’s scale boosts leverage but cannot fully neutralize commodity cycles.

Specialized equipment scarcity

Specialized TBMs, heavy cranes and niche MEP systems remain concentrated among few global vendors, so as of 2024 lead times often exceed 18 months and switching costs on mega-projects are substantial. Supplier service quality directly shifts schedule risk and can trigger liquidated damages running into millions of USD per month on delayed sections. Strategic alliances and multi-vendor frameworks are used to dilute single-point dependency and shorten contingency lead times.

Skilled labor and subcontractors

Specialized trades and reputable subcontractors can command premiums in tight Shanghai markets, with 2024 industry surveys reporting up to 20% cost uplifts for scarce skills; labor mobility constraints and stricter safety compliance further add measurable overheads and schedule risk. SCG’s preferred subcontractor networks stabilize rates and quality across projects. Ongoing workforce development and increased self-perform capacity moderate supplier power.

Logistics and imported inputs

International projects depend on imported materials exposed to tariffs, FX swings and port congestion; Port of Shanghai throughput was about 43 million TEU in 2023 (SIPG), concentrating supplier leverage and delay risks that can spike mid-project. Early procurement and near-shoring reduce FX/tariff exposure, while logistics bottlenecks elevate supplier bargaining power during execution.

- Multi-sourcing

- Buffer inventories

- Early procurement

- Near-shoring

Countervailing scale and integration

In 2024 Shanghai Construction Group leverages large-scale centralized purchasing, standardized specs and e-procurement to secure better pricing and delivery terms, while partial vertical integration in design and selected fabrication reduces supplier dependence. Performance-based contracts shift quality and schedule risk back to suppliers, leaving supplier power moderate but highly project-specific.

- procurement scale: centralized sourcing, e-procurement

- integration: in-house design/fabrication reduces reliance

- contracting: performance-based risk transfer

- assessment: moderate supplier power, varies by project

Concentrated suppliers, long lead times and skilled-trade premiums tighten construction margins

Suppliers of steel/cement/glass are concentrated (China ~60% of global cement production, 2023) and commodity volatility squeezes margins; TBM/crane lead times >18 months (2024) raise switching costs; scarce trades command up to 20% premiums (2024). SCG central procurement, partial vertical integration and performance contracts keep supplier power moderate and project-specific.

| Metric | Value |

|---|---|

| Cement share (China, 2023) | ~60% |

| Port of Shanghai throughput (2023) | ~43M TEU |

| TBM/crane lead times (2024) | >18 months |

| Skilled trade premium (2024) | up to 20% |

What is included in the product

Comprehensive Porter's Five Forces assessment for Shanghai Construction, evaluating competitive rivalry, supplier and buyer power, entry barriers, and substitute threats to reveal strategic vulnerabilities, pricing pressures, and emerging disruptors shaping its profitability and market positioning.

A concise, one-sheet Porter’s Five Forces for Shanghai Construction that pinpoints competitive pain—ready to drop into decks or model scenarios, customize pressure levels with new data, compare pre/post regulation impacts, and integrate into wider reports without macros for non-finance users.

Customers Bargaining Power

Government tender dominance

In 2024 public owners in Shanghai run highly transparent, price-competitive tenders with strict prequalification barriers that filter bidders and favor lowest-compliant offers.

Lowest-compliant bids and tight KPIs — focused on safety, schedule and quality — compress margins and elevate cost-to-win pressures for contractors.

Political and social objectives frequently reshape scope and timelines, raising change-order risk; however strong reputation and documented past performance still secure value-based awards despite price competition.

Large developers and SOEs

Large private developers and SOEs buy at scale—often awarding single pipelines exceeding RMB 1 billion—so they demand favorable pricing and extended payment terms. Multi-city bundling in 2024 lets them extract deeper volume discounts and leverage procurement across provinces. Payment schedules and retention clauses (commonly 5–10%) squeeze contractor cash flow, while value engineering and EPC bundling are used to trade price reductions for narrower scope.

Payment risk and financing

Extended receivables and milestone payments—commonly stretching beyond 180 days in 2024—shift working-capital burden to contractors and elevate payment risk. Buyers with financing constraints increasingly push for deferred terms, raising bargaining power. SCG’s strong balance sheet, state-backed guarantees and PPP track record mitigate this pressure. Use of factoring and project-finance rings reduces buyer leverage and shortens cash cycles.

Quality, safety, ESG standards

Owners increasingly require green materials, BIM and safety certifications, raising compliance costs but allowing developers to differentiate; by 2024 many Tier-1 projects in China mandated BIM for design and construction coordination.

Buyers can benchmark performance against global standards and ESG metrics, pressuring contractors on quality and safety; SCG’s advanced design capability enables delivery of performance-based specs and capture of premium pricing.

- Tier-1 BIM mandate 2024: widespread on major Chinese projects

- Compliance raises costs but supports premium bids

- ESG/safety benchmarking strengthens buyer bargaining

- SCG design capability: enables premium, spec-driven wins

International and MDB clients

International and MDB clients exert high bargaining power: in 2024 multilateral banks and overseas governments reinforced strict compliance and local‑content requirements, competitive international tenders broaden bidder pools, and currency, legal and dispute frameworks favor sophisticated buyers while Shanghai Construction's cross‑border EPC experience helps rebalance terms.

- Compliance focus: stronger local‑content clauses in 2024

- Procurement: wider bidder pools via international tenders

- Legal/currency: advantage to sophisticated buyers

- Experience: cross‑border EPCs improve contract leverage

Shanghai 2024 tenders: >RMB1bn, 5–10% retention

In 2024 Shanghai owners run transparent, price‑competitive tenders (single awards often >RMB1bn) with tight KPIs, 5–10% retention and receivables commonly >180 days, compressing contractor margins. Tier‑1 BIM mandates and ESG benchmarks raise compliance costs but enable premium, spec‑driven wins; MDBs widen bidder pools and increase buyer leverage.

| Metric | 2024 |

|---|---|

| Avg single award | RMB>1bn |

| Retention | 5–10% |

| Receivables | >180 days |

Same Document Delivered

Shanghai Construction Porter's Five Forces Analysis

This preview shows the exact Shanghai Construction Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted and ready for use. The document provides a professional assessment of competitive rivalry, supplier and buyer power, and threats of new entrants and substitutes, with clear strategic implications. No placeholders or samples; instant download upon payment.