Schaeffler Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

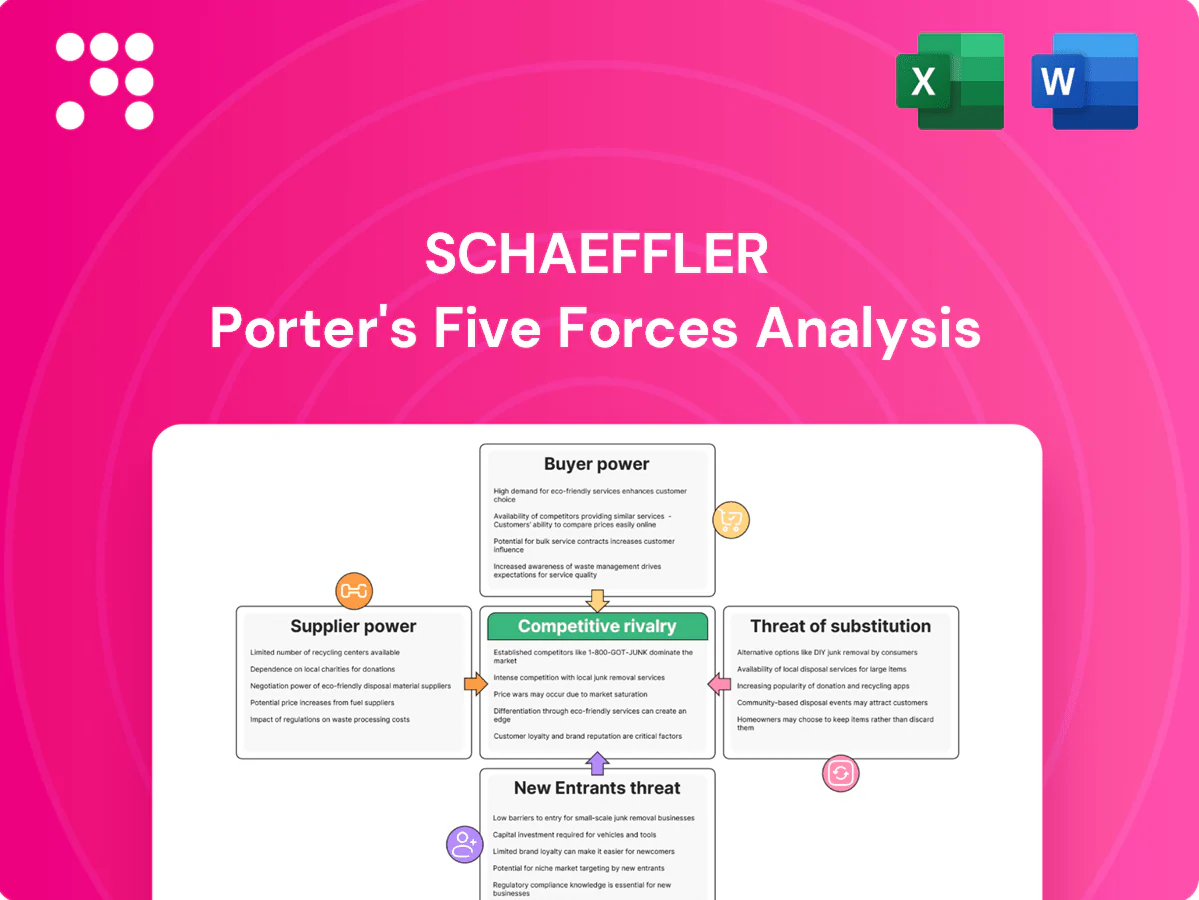

Schaeffler faces intense competitive rivalry, shifting supplier dynamics, and mounting substitute threats amid electrification and supply-chain shifts, while buyer power and entry barriers shape margin pressure and strategic choices. This snapshot highlights key tensions and tactical levers—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications for investment or strategy.

Suppliers Bargaining Power

Specialized materials and semiconductors

Precision steel, advanced alloys, rare-earth magnets and semiconductors are critical for bearings and e-mobility; China controls roughly 85–90% of rare-earth processing, concentrating magnet supply and boosting supplier leverage. Semiconductor tightness has pushed lead times above 20 weeks in peak cycles, and long qualification times hamper quick substitution; Schaeffler offsets risk via multi-sourcing, elevated inventories and closer supplier collaboration.

High switching costs and qualification

Automotive-grade inputs require rigorous PPAP and validation, often taking 6–18 months and effectively locking suppliers in for years. Switching carries real risks of line stoppages and warranty exposure, increasing supplier leverage. Dual-qualification lowers dependency but typically raises sourcing costs and program complexity. Long-term agreements trade price stability for firm volume commitments and supply security.

Logistics and energy sensitivity

Bearings and metal-intensive parts are highly energy- and logistics-sensitive, with global container freight rates down roughly 80% from 2021 peaks to 2024 levels, transmitting through to input costs. Energy price spikes and freight bottlenecks directly pressure margins unless inputs are indexed or hedged. European energy volatility remains elevated versus pre‑crisis levels, so indexed contracts matter. Nearshoring and local-for-local production materially dampen this pass-through.

Supplier innovation and co-development

Material science and electronics suppliers co-develop EV, Industry 4.0 and lightweighting solutions with Schaeffler, bringing proprietary IP and process know-how that can create quasi-sole-source positions; Schaeffler’s early supplier involvement secures access to these innovations but often concedes margin to align roadmaps on cost-downs and performance.

- Co-development: secures tech access

- Unique IP: raises supplier power

- Early involvement: margin trade-off

- Joint roadmaps: align cost and performance

ESG and compliance requirements

Traceability requirements for conflict minerals and CO2 footprints narrow Schaeffler’s approved supplier pool, enabling suppliers with scarce certifications to demand higher prices and push compliance costs up; non-compliance risks customer penalties and lost program awards, while certified suppliers lower disruption and reputational risk.

- Traceability narrows pool

- Certified suppliers command premiums

- Non-compliance = penalties/lost awards

- Strategic certified partnerships reduce disruption

China controls 85–90% rare-earths; semiconductors >20w lead times

Supplier power is high: China controls 85–90% of rare-earth processing, semiconductors see peak lead times >20 weeks, and PPAP/validation takes 6–18 months, limiting quick substitution. Freight fell ~80% from 2021 to 2024, easing cost pass-through but energy volatility keeps input risk. Certified suppliers command pricing and access advantages, reinforcing supplier leverage.

| Metric | 2024 | Impact |

|---|---|---|

| Rare-earth processing | 85–90% China | High concentration |

| Semiconductor lead time | >20 weeks | Switching difficulty |

| Container rates vs 2021 | -~80% | Lower logistics cost |

| PPAP/validation | 6–18 months | Lock-in |

What is included in the product

Tailored Porter’s Five Forces analysis for Schaeffler uncovering competitive intensity, supplier and buyer power, entry barriers, substitute threats, and strategic implications for profitability and market positioning.

One-sheet Porter's Five Forces for Schaeffler that condenses competitive pressure into an editable spider chart—customize scores, swap data, and drop straight into pitch decks or boardroom slides for fast strategic decisions.

Customers Bargaining Power

Concentrated OEM customers

Concentrated OEM customers—global automakers and Tier‑1s—buy at scale and negotiate aggressively, putting sustained price pressure on suppliers; Schaeffler reported group revenue of about €14.4bn in 2023, underlining OEM importance. Platform sourcing and global RFQs amplify this pressure, and losing a platform can reduce volumes and revenue materially. Schaeffler mitigates risk via multi‑year awards and diversified industrial clients outside automotive.

Design-in reduces switching

Design-in of bearings and chassis into OEM platforms—OEM platform lifecycles averaging ~10 years in 2024—raises switching costs as validation and tooling involve multi-million-euro investments, tempering buyer power. Buyers still leverage future platform awards to extract program-level cost reductions, commonly targeting mid-single-digit percentage savings. Consequently, Schaeffler relies on performance, quality, and on-time delivery as primary retention levers.

EV transition repricing

Shift from ICE to EV reshapes BOMs and resets supplier rosters; with global EV share of new car sales at about 14% in 2023 (IEA), buyers rebid content and increasingly favor integrated e-axle/system providers. Incumbency in ICE is less protective, raising buyer power. Schaeffler’s expanding e-mobility portfolio aims to defend content and value.

Aftermarket and industrial diversification

Aftermarket and industrial diversification dilute OEM concentration risk: independent aftermarket accounted for roughly one-third of Schaeffler group sales in 2024, lowering reliance on vehicle OEM cycles. These buyers are fragmented with varied margins and service needs, shifting buying power away from pure price competition. Growth in value-added services (predictive maintenance, digital monitoring) and active mix management supported overall pricing power in 2024.

- aftermarket ~33% of 2024 sales

- fragmented buyers = lower price pressure

- digital services = higher margin mix

- mix mgmt strengthens pricing

Quality, warranty, and delivery clauses

Strict PPAP and common 2024 OEM PPM expectations (typically ≤100 ppm) plus warranty backstops give buyers leverage; penalties and chargebacks can reclaim margins when quality or delivery fail. JIT/lean schedules amplify exposure as delivery deviations often trigger financial deductions. Robust quality systems and S&OP discipline are essential to defend pricing and limit clawbacks.

- PPAP enforcement

- PPM ≤100 ppm (2024 OEM norm)

- Warranty backstops/chargebacks

- JIT penalties for delivery variance

- Need: quality systems + S&OP

OEM buyers tighten margins; 33% aftermarket and EV rebids boost buyer leverage

Concentrated OEM buyers drive sustained price pressure despite Schaeffler’s ~€14.4bn 2023 revenue and ~33% aftermarket share in 2024, reducing OEM reliance. Ten-year OEM platform cycles and high design‑in costs limit switching, but EV rebidding (global EV ~14% of new sales in 2023) raises buyer leverage. Rigorous PPAP/PPM ≤100 ppm, JIT penalties and warranty clauses further shift power to buyers.

| Metric | 2023/24 |

|---|---|

| Group revenue | €14.4bn (2023) |

| Aftermarket | ~33% (2024) |

| EV share | ~14% (2023) |

What You See Is What You Get

Schaeffler Porter's Five Forces Analysis

This Porter's Five Forces analysis of Schaeffler evaluates competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and strategic implications for profitability and positioning. It includes sourced insights and actionable recommendations. The document shown is the exact file you’ll receive immediately after purchase—no surprises.

A Must-Have Tool for Decision-Makers

Schaeffler faces intense competitive rivalry, shifting supplier dynamics, and mounting substitute threats amid electrification and supply-chain shifts, while buyer power and entry barriers shape margin pressure and strategic choices. This snapshot highlights key tensions and tactical levers—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications for investment or strategy.

Suppliers Bargaining Power

Specialized materials and semiconductors

Precision steel, advanced alloys, rare-earth magnets and semiconductors are critical for bearings and e-mobility; China controls roughly 85–90% of rare-earth processing, concentrating magnet supply and boosting supplier leverage. Semiconductor tightness has pushed lead times above 20 weeks in peak cycles, and long qualification times hamper quick substitution; Schaeffler offsets risk via multi-sourcing, elevated inventories and closer supplier collaboration.

High switching costs and qualification

Automotive-grade inputs require rigorous PPAP and validation, often taking 6–18 months and effectively locking suppliers in for years. Switching carries real risks of line stoppages and warranty exposure, increasing supplier leverage. Dual-qualification lowers dependency but typically raises sourcing costs and program complexity. Long-term agreements trade price stability for firm volume commitments and supply security.

Logistics and energy sensitivity

Bearings and metal-intensive parts are highly energy- and logistics-sensitive, with global container freight rates down roughly 80% from 2021 peaks to 2024 levels, transmitting through to input costs. Energy price spikes and freight bottlenecks directly pressure margins unless inputs are indexed or hedged. European energy volatility remains elevated versus pre‑crisis levels, so indexed contracts matter. Nearshoring and local-for-local production materially dampen this pass-through.

Supplier innovation and co-development

Material science and electronics suppliers co-develop EV, Industry 4.0 and lightweighting solutions with Schaeffler, bringing proprietary IP and process know-how that can create quasi-sole-source positions; Schaeffler’s early supplier involvement secures access to these innovations but often concedes margin to align roadmaps on cost-downs and performance.

- Co-development: secures tech access

- Unique IP: raises supplier power

- Early involvement: margin trade-off

- Joint roadmaps: align cost and performance

ESG and compliance requirements

Traceability requirements for conflict minerals and CO2 footprints narrow Schaeffler’s approved supplier pool, enabling suppliers with scarce certifications to demand higher prices and push compliance costs up; non-compliance risks customer penalties and lost program awards, while certified suppliers lower disruption and reputational risk.

- Traceability narrows pool

- Certified suppliers command premiums

- Non-compliance = penalties/lost awards

- Strategic certified partnerships reduce disruption

China controls 85–90% rare-earths; semiconductors >20w lead times

Supplier power is high: China controls 85–90% of rare-earth processing, semiconductors see peak lead times >20 weeks, and PPAP/validation takes 6–18 months, limiting quick substitution. Freight fell ~80% from 2021 to 2024, easing cost pass-through but energy volatility keeps input risk. Certified suppliers command pricing and access advantages, reinforcing supplier leverage.

| Metric | 2024 | Impact |

|---|---|---|

| Rare-earth processing | 85–90% China | High concentration |

| Semiconductor lead time | >20 weeks | Switching difficulty |

| Container rates vs 2021 | -~80% | Lower logistics cost |

| PPAP/validation | 6–18 months | Lock-in |

What is included in the product

Tailored Porter’s Five Forces analysis for Schaeffler uncovering competitive intensity, supplier and buyer power, entry barriers, substitute threats, and strategic implications for profitability and market positioning.

One-sheet Porter's Five Forces for Schaeffler that condenses competitive pressure into an editable spider chart—customize scores, swap data, and drop straight into pitch decks or boardroom slides for fast strategic decisions.

Customers Bargaining Power

Concentrated OEM customers

Concentrated OEM customers—global automakers and Tier‑1s—buy at scale and negotiate aggressively, putting sustained price pressure on suppliers; Schaeffler reported group revenue of about €14.4bn in 2023, underlining OEM importance. Platform sourcing and global RFQs amplify this pressure, and losing a platform can reduce volumes and revenue materially. Schaeffler mitigates risk via multi‑year awards and diversified industrial clients outside automotive.

Design-in reduces switching

Design-in of bearings and chassis into OEM platforms—OEM platform lifecycles averaging ~10 years in 2024—raises switching costs as validation and tooling involve multi-million-euro investments, tempering buyer power. Buyers still leverage future platform awards to extract program-level cost reductions, commonly targeting mid-single-digit percentage savings. Consequently, Schaeffler relies on performance, quality, and on-time delivery as primary retention levers.

EV transition repricing

Shift from ICE to EV reshapes BOMs and resets supplier rosters; with global EV share of new car sales at about 14% in 2023 (IEA), buyers rebid content and increasingly favor integrated e-axle/system providers. Incumbency in ICE is less protective, raising buyer power. Schaeffler’s expanding e-mobility portfolio aims to defend content and value.

Aftermarket and industrial diversification

Aftermarket and industrial diversification dilute OEM concentration risk: independent aftermarket accounted for roughly one-third of Schaeffler group sales in 2024, lowering reliance on vehicle OEM cycles. These buyers are fragmented with varied margins and service needs, shifting buying power away from pure price competition. Growth in value-added services (predictive maintenance, digital monitoring) and active mix management supported overall pricing power in 2024.

- aftermarket ~33% of 2024 sales

- fragmented buyers = lower price pressure

- digital services = higher margin mix

- mix mgmt strengthens pricing

Quality, warranty, and delivery clauses

Strict PPAP and common 2024 OEM PPM expectations (typically ≤100 ppm) plus warranty backstops give buyers leverage; penalties and chargebacks can reclaim margins when quality or delivery fail. JIT/lean schedules amplify exposure as delivery deviations often trigger financial deductions. Robust quality systems and S&OP discipline are essential to defend pricing and limit clawbacks.

- PPAP enforcement

- PPM ≤100 ppm (2024 OEM norm)

- Warranty backstops/chargebacks

- JIT penalties for delivery variance

- Need: quality systems + S&OP

OEM buyers tighten margins; 33% aftermarket and EV rebids boost buyer leverage

Concentrated OEM buyers drive sustained price pressure despite Schaeffler’s ~€14.4bn 2023 revenue and ~33% aftermarket share in 2024, reducing OEM reliance. Ten-year OEM platform cycles and high design‑in costs limit switching, but EV rebidding (global EV ~14% of new sales in 2023) raises buyer leverage. Rigorous PPAP/PPM ≤100 ppm, JIT penalties and warranty clauses further shift power to buyers.

| Metric | 2023/24 |

|---|---|

| Group revenue | €14.4bn (2023) |

| Aftermarket | ~33% (2024) |

| EV share | ~14% (2023) |

What You See Is What You Get

Schaeffler Porter's Five Forces Analysis

This Porter's Five Forces analysis of Schaeffler evaluates competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and strategic implications for profitability and positioning. It includes sourced insights and actionable recommendations. The document shown is the exact file you’ll receive immediately after purchase—no surprises.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Schaeffler faces intense competitive rivalry, shifting supplier dynamics, and mounting substitute threats amid electrification and supply-chain shifts, while buyer power and entry barriers shape margin pressure and strategic choices. This snapshot highlights key tensions and tactical levers—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications for investment or strategy.

Suppliers Bargaining Power

Specialized materials and semiconductors

Precision steel, advanced alloys, rare-earth magnets and semiconductors are critical for bearings and e-mobility; China controls roughly 85–90% of rare-earth processing, concentrating magnet supply and boosting supplier leverage. Semiconductor tightness has pushed lead times above 20 weeks in peak cycles, and long qualification times hamper quick substitution; Schaeffler offsets risk via multi-sourcing, elevated inventories and closer supplier collaboration.

High switching costs and qualification

Automotive-grade inputs require rigorous PPAP and validation, often taking 6–18 months and effectively locking suppliers in for years. Switching carries real risks of line stoppages and warranty exposure, increasing supplier leverage. Dual-qualification lowers dependency but typically raises sourcing costs and program complexity. Long-term agreements trade price stability for firm volume commitments and supply security.

Logistics and energy sensitivity

Bearings and metal-intensive parts are highly energy- and logistics-sensitive, with global container freight rates down roughly 80% from 2021 peaks to 2024 levels, transmitting through to input costs. Energy price spikes and freight bottlenecks directly pressure margins unless inputs are indexed or hedged. European energy volatility remains elevated versus pre‑crisis levels, so indexed contracts matter. Nearshoring and local-for-local production materially dampen this pass-through.

Supplier innovation and co-development

Material science and electronics suppliers co-develop EV, Industry 4.0 and lightweighting solutions with Schaeffler, bringing proprietary IP and process know-how that can create quasi-sole-source positions; Schaeffler’s early supplier involvement secures access to these innovations but often concedes margin to align roadmaps on cost-downs and performance.

- Co-development: secures tech access

- Unique IP: raises supplier power

- Early involvement: margin trade-off

- Joint roadmaps: align cost and performance

ESG and compliance requirements

Traceability requirements for conflict minerals and CO2 footprints narrow Schaeffler’s approved supplier pool, enabling suppliers with scarce certifications to demand higher prices and push compliance costs up; non-compliance risks customer penalties and lost program awards, while certified suppliers lower disruption and reputational risk.

- Traceability narrows pool

- Certified suppliers command premiums

- Non-compliance = penalties/lost awards

- Strategic certified partnerships reduce disruption

China controls 85–90% rare-earths; semiconductors >20w lead times

Supplier power is high: China controls 85–90% of rare-earth processing, semiconductors see peak lead times >20 weeks, and PPAP/validation takes 6–18 months, limiting quick substitution. Freight fell ~80% from 2021 to 2024, easing cost pass-through but energy volatility keeps input risk. Certified suppliers command pricing and access advantages, reinforcing supplier leverage.

| Metric | 2024 | Impact |

|---|---|---|

| Rare-earth processing | 85–90% China | High concentration |

| Semiconductor lead time | >20 weeks | Switching difficulty |

| Container rates vs 2021 | -~80% | Lower logistics cost |

| PPAP/validation | 6–18 months | Lock-in |

What is included in the product

Tailored Porter’s Five Forces analysis for Schaeffler uncovering competitive intensity, supplier and buyer power, entry barriers, substitute threats, and strategic implications for profitability and market positioning.

One-sheet Porter's Five Forces for Schaeffler that condenses competitive pressure into an editable spider chart—customize scores, swap data, and drop straight into pitch decks or boardroom slides for fast strategic decisions.

Customers Bargaining Power

Concentrated OEM customers

Concentrated OEM customers—global automakers and Tier‑1s—buy at scale and negotiate aggressively, putting sustained price pressure on suppliers; Schaeffler reported group revenue of about €14.4bn in 2023, underlining OEM importance. Platform sourcing and global RFQs amplify this pressure, and losing a platform can reduce volumes and revenue materially. Schaeffler mitigates risk via multi‑year awards and diversified industrial clients outside automotive.

Design-in reduces switching

Design-in of bearings and chassis into OEM platforms—OEM platform lifecycles averaging ~10 years in 2024—raises switching costs as validation and tooling involve multi-million-euro investments, tempering buyer power. Buyers still leverage future platform awards to extract program-level cost reductions, commonly targeting mid-single-digit percentage savings. Consequently, Schaeffler relies on performance, quality, and on-time delivery as primary retention levers.

EV transition repricing

Shift from ICE to EV reshapes BOMs and resets supplier rosters; with global EV share of new car sales at about 14% in 2023 (IEA), buyers rebid content and increasingly favor integrated e-axle/system providers. Incumbency in ICE is less protective, raising buyer power. Schaeffler’s expanding e-mobility portfolio aims to defend content and value.

Aftermarket and industrial diversification

Aftermarket and industrial diversification dilute OEM concentration risk: independent aftermarket accounted for roughly one-third of Schaeffler group sales in 2024, lowering reliance on vehicle OEM cycles. These buyers are fragmented with varied margins and service needs, shifting buying power away from pure price competition. Growth in value-added services (predictive maintenance, digital monitoring) and active mix management supported overall pricing power in 2024.

- aftermarket ~33% of 2024 sales

- fragmented buyers = lower price pressure

- digital services = higher margin mix

- mix mgmt strengthens pricing

Quality, warranty, and delivery clauses

Strict PPAP and common 2024 OEM PPM expectations (typically ≤100 ppm) plus warranty backstops give buyers leverage; penalties and chargebacks can reclaim margins when quality or delivery fail. JIT/lean schedules amplify exposure as delivery deviations often trigger financial deductions. Robust quality systems and S&OP discipline are essential to defend pricing and limit clawbacks.

- PPAP enforcement

- PPM ≤100 ppm (2024 OEM norm)

- Warranty backstops/chargebacks

- JIT penalties for delivery variance

- Need: quality systems + S&OP

OEM buyers tighten margins; 33% aftermarket and EV rebids boost buyer leverage

Concentrated OEM buyers drive sustained price pressure despite Schaeffler’s ~€14.4bn 2023 revenue and ~33% aftermarket share in 2024, reducing OEM reliance. Ten-year OEM platform cycles and high design‑in costs limit switching, but EV rebidding (global EV ~14% of new sales in 2023) raises buyer leverage. Rigorous PPAP/PPM ≤100 ppm, JIT penalties and warranty clauses further shift power to buyers.

| Metric | 2023/24 |

|---|---|

| Group revenue | €14.4bn (2023) |

| Aftermarket | ~33% (2024) |

| EV share | ~14% (2023) |

What You See Is What You Get

Schaeffler Porter's Five Forces Analysis

This Porter's Five Forces analysis of Schaeffler evaluates competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and strategic implications for profitability and positioning. It includes sourced insights and actionable recommendations. The document shown is the exact file you’ll receive immediately after purchase—no surprises.