Schindler Holding Porter's Five Forces Analysis

From Overview to Strategy Blueprint

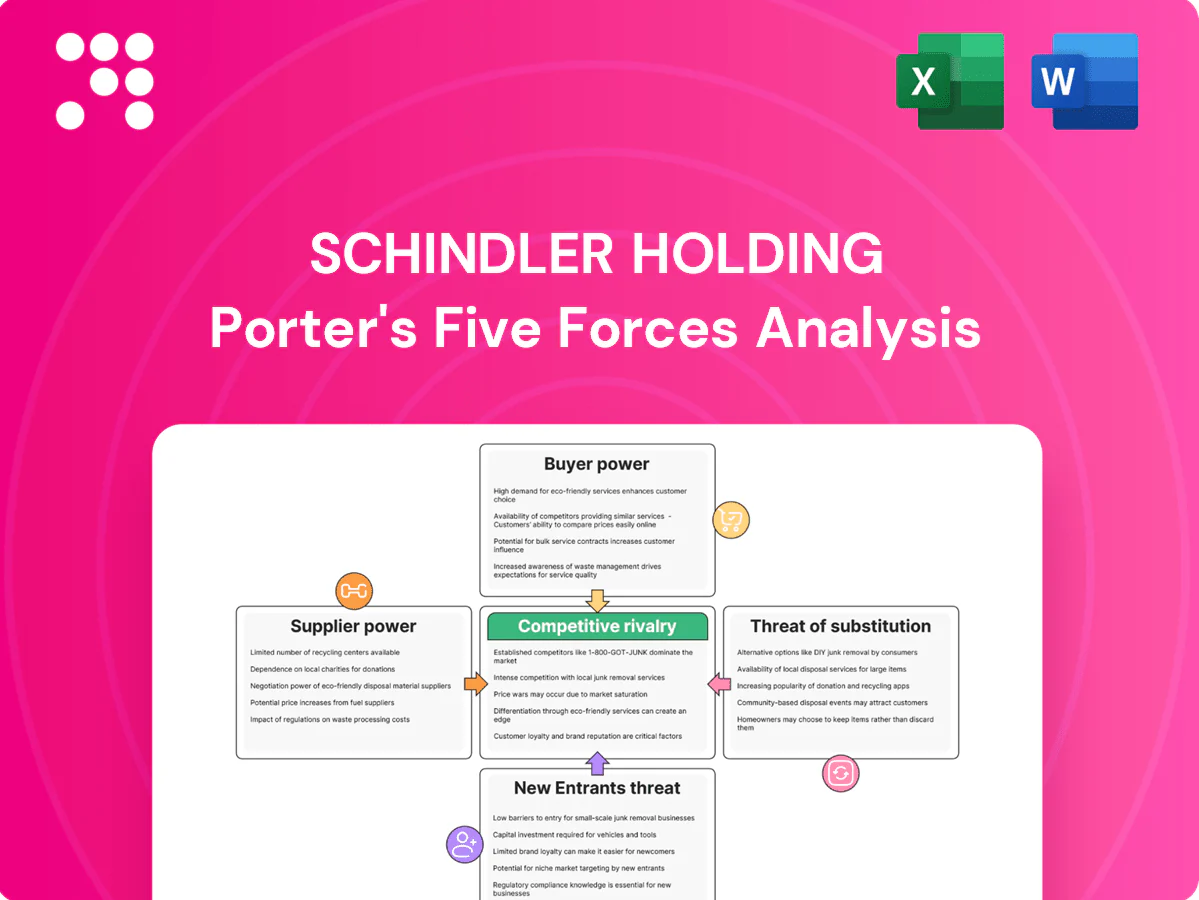

Schindler Holding faces moderate supplier power but high buyer expectations and intense rivalry across global elevator and escalator markets. Technological change and regulatory demands raise barriers yet enable differentiation, while threat of new entrants and substitutes remains manageable. This snapshot highlights key tensions shaping Schindler’s strategy. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated critical components

Advanced drives, controllers, door systems, ropes and safety gear come from a small pool of specialized suppliers, giving those vendors elevated leverage on pricing and lead times. Long safety qualification cycles make rapid substitution costly, so dual-sourcing is used where feasible but some items remain single or limited source. Consolidation in electronics suppliers can amplify this power during shortages, increasing procurement risk for Schindler.

Commodity and semiconductor volatility

Steel, copper and rare materials expose Schindler to cyclical cost swings, while global semiconductor sales of roughly $600 billion in 2024 highlight continued chip market tension that creates allocation risk and production disruptions. Schindler’s scale and hedging strategies mitigate shocks, yet cost pass-through to customers is often delayed. Extended component lead times raise inventories and working capital requirements.

Switching costs and qualification lock-in

Safety and compliance testing to standards EN 81 and ASME A17.1 create high requalification costs for alternative parts, often requiring months of validation. Tooling, software interfaces and firmware compatibility embed suppliers into platform designs, locking in value for incumbent suppliers, especially control systems. Schindler operates in over 100 countries, amplifying lock-in effects. Design-for-multi-sourcing and modularity partly counterbalance.

Aftermarket IP and proprietary parts

Aftermarket IP and proprietary parts tilt leverage toward Schindler when service kits use Schindler-owned modules, supported by an installed base of about 2.1 million units (2024) where service revenues represent roughly 60% of recurring sales; however upstream licensors and patent holders—often concentrated suppliers—retain bargaining power, notably where select makers supply long-tail parts comprising over 20% of replacement spend.

- Installed base: ~2.1M units (2024)

- Service share: ~60% recurring sales

- Long-tail supplier concentration: >20% spend

- Vertical integration: reduces exposure in key modules

Logistics and sustainability constraints

Logistics bottlenecks and stricter sustainability rules narrow Schindler’s supplier options: the EU CSRD extends to roughly 50,000 firms from 2024, increasing Scope 3 traceability demands, while IMO targets require major shipping decarbonization by 2050, pressuring carriers and component suppliers. Compliance and ESG audits shrink the vendor pool and can raise supplier leverage; regional nearshoring boosts resilience but reduces lowest-cost sourcing. Collaboration on supplier decarbonization becomes a commercial negotiating tool, potentially traded for price or long-term contracts.

- CSRD ~50,000 firms (2024) raises Scope 3 reporting

- IMO 2050 GHG reduction target tightens shipping suppliers

- Regionalization improves resilience, limits cheapest sourcing

- ESG audits narrow vendors, lifting supplier bargaining

Specialized elevator suppliers gain leverage; installed base 2.1M

Specialized elevator components and long safety qualifications give suppliers pricing and lead-time leverage; dual-sourcing limited. Schindler scale and vertical integration mitigate but exposure remains: installed base ~2.1M (2024), service ~60% recurring sales, semiconductor market ~$600B (2024). ESG/regulation (CSRD ~50,000 firms, IMO 2050) narrows vendor pool, raising supplier power.

| Metric | Value |

|---|---|

| Installed base | ~2.1M (2024) |

| Service share | ~60% |

| Chip market | $600B (2024) |

| CSRD scope | ~50,000 firms (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Schindler Holding, uncovering competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive technologies and market entry barriers to inform strategic decisions.

One-sheet Porter's Five Forces for Schindler Holding that instantly visualizes competitive pressure with a spider chart and customizable score inputs—ready to drop into pitch decks or board reports. No macros, editable labels, and seamless Excel integration for scenario testing.

Customers Bargaining Power

Professional buyers and tenders

Developers, contractors and transit authorities run competitive tenders that compress pricing and contractual terms, forcing Schindler to match aggressive bids. Standardized specifications make direct comparisons across top suppliers routine, increasing switching and reducing pricing power. Public-sector bids are significant: OECD estimated public procurement at about 12% of GDP in 2024, amplifying price transparency. Value engineering in new installs commonly trims supplier margins further.

High switching costs post-install

Once installed, proprietary controllers, certified safety ladders and software ecosystems make switching providers costly and risky, with modernization controller replacements typically costing €20,000–€100,000 and downtime in commercial buildings often valued at $1,000–$10,000 per hour (industry 2024 estimates). This materially reduces buyer power in maintenance and modernization phases and supports long-term service contracts that lock in annuity streams. Performance history and uptime KPIs (99%+ targets common) strongly influence renewal leverage.

Total cost of ownership focus

Buyers in 2024 evaluate lifecycle energy use, downtime and maintenance over capex alone, shifting negotiations toward total cost of ownership metrics. Remote monitoring, predictive maintenance and efficient drives allow Schindler to justify premium pricing based on reduced lifecycle costs. Schindler’s ability to quantify TCO savings weakens pure price bargaining. Penalties for SLA breaches keep pressure on delivery and uptime expectations above 99%.

Project cyclicality and timing

Construction cycles let buyers delay or bundle elevator orders to extract better terms, notably in years of weak construction demand; Schindler reported group sales of CHF 12.7bn in 2023, so large multi-building deals can materially shift negotiation leverage. Tight project schedules reduce buyer bargaining power as on-time delivery gains premium; change orders, common in retrofits, can erode margins if scope shifts late.

- Volume leverage: large projects increase buyer bargaining

- Timing risk: tight schedules reduce buyer power

- Bundling: cyclical slowdowns enable order delays

- Scope creep: change orders can claw back margins

Modernization alternatives

Owners often opt for partial modernization, third-party parts, or independent service providers to cut costs; interface openness and compatibility with existing control systems increase their leverage. Schindler defends pricing with OEM warranties, safety upgrades, and digital features like predictive maintenance, while demonstrated compliance and liability support frequently tip procurement toward OEM solutions.

- Levers: partial modernizations, third-party parts, independent servicers

- Key factors: interface openness, compatibility

- Schindler responses: OEM warranties, safety upgrades, digital services

- Decision drivers: compliance evidence, liability protection

Procurement pressure vs high switch costs: modernization €20k–€100k

Competitive tenders and standardized specs compress prices, but high switching costs for controllers and safety systems (modernization €20,000–€100,000; downtime $1,000–$10,000/hr, industry 2024) preserve Schindler’s service leverage; buyers shift to TCO and SLAs (99%+ uptime), while public procurement (≈12% GDP, OECD 2024) and CHF 12.7bn sales (Schindler 2023) shape negotiation dynamics.

| Metric | Value |

|---|---|

| Public procurement | ≈12% GDP (OECD 2024) |

| Schindler sales | CHF 12.7bn (2023) |

| Modernization cost | €20k–€100k (2024) |

| Downtime cost | $1k–$10k/hr (2024) |

| SLA target | 99%+ uptime |

Preview Before You Purchase

Schindler Holding Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Schindler Holding examines competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications with actionable recommendations. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

From Overview to Strategy Blueprint

Schindler Holding faces moderate supplier power but high buyer expectations and intense rivalry across global elevator and escalator markets. Technological change and regulatory demands raise barriers yet enable differentiation, while threat of new entrants and substitutes remains manageable. This snapshot highlights key tensions shaping Schindler’s strategy. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated critical components

Advanced drives, controllers, door systems, ropes and safety gear come from a small pool of specialized suppliers, giving those vendors elevated leverage on pricing and lead times. Long safety qualification cycles make rapid substitution costly, so dual-sourcing is used where feasible but some items remain single or limited source. Consolidation in electronics suppliers can amplify this power during shortages, increasing procurement risk for Schindler.

Commodity and semiconductor volatility

Steel, copper and rare materials expose Schindler to cyclical cost swings, while global semiconductor sales of roughly $600 billion in 2024 highlight continued chip market tension that creates allocation risk and production disruptions. Schindler’s scale and hedging strategies mitigate shocks, yet cost pass-through to customers is often delayed. Extended component lead times raise inventories and working capital requirements.

Switching costs and qualification lock-in

Safety and compliance testing to standards EN 81 and ASME A17.1 create high requalification costs for alternative parts, often requiring months of validation. Tooling, software interfaces and firmware compatibility embed suppliers into platform designs, locking in value for incumbent suppliers, especially control systems. Schindler operates in over 100 countries, amplifying lock-in effects. Design-for-multi-sourcing and modularity partly counterbalance.

Aftermarket IP and proprietary parts

Aftermarket IP and proprietary parts tilt leverage toward Schindler when service kits use Schindler-owned modules, supported by an installed base of about 2.1 million units (2024) where service revenues represent roughly 60% of recurring sales; however upstream licensors and patent holders—often concentrated suppliers—retain bargaining power, notably where select makers supply long-tail parts comprising over 20% of replacement spend.

- Installed base: ~2.1M units (2024)

- Service share: ~60% recurring sales

- Long-tail supplier concentration: >20% spend

- Vertical integration: reduces exposure in key modules

Logistics and sustainability constraints

Logistics bottlenecks and stricter sustainability rules narrow Schindler’s supplier options: the EU CSRD extends to roughly 50,000 firms from 2024, increasing Scope 3 traceability demands, while IMO targets require major shipping decarbonization by 2050, pressuring carriers and component suppliers. Compliance and ESG audits shrink the vendor pool and can raise supplier leverage; regional nearshoring boosts resilience but reduces lowest-cost sourcing. Collaboration on supplier decarbonization becomes a commercial negotiating tool, potentially traded for price or long-term contracts.

- CSRD ~50,000 firms (2024) raises Scope 3 reporting

- IMO 2050 GHG reduction target tightens shipping suppliers

- Regionalization improves resilience, limits cheapest sourcing

- ESG audits narrow vendors, lifting supplier bargaining

Specialized elevator suppliers gain leverage; installed base 2.1M

Specialized elevator components and long safety qualifications give suppliers pricing and lead-time leverage; dual-sourcing limited. Schindler scale and vertical integration mitigate but exposure remains: installed base ~2.1M (2024), service ~60% recurring sales, semiconductor market ~$600B (2024). ESG/regulation (CSRD ~50,000 firms, IMO 2050) narrows vendor pool, raising supplier power.

| Metric | Value |

|---|---|

| Installed base | ~2.1M (2024) |

| Service share | ~60% |

| Chip market | $600B (2024) |

| CSRD scope | ~50,000 firms (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Schindler Holding, uncovering competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive technologies and market entry barriers to inform strategic decisions.

One-sheet Porter's Five Forces for Schindler Holding that instantly visualizes competitive pressure with a spider chart and customizable score inputs—ready to drop into pitch decks or board reports. No macros, editable labels, and seamless Excel integration for scenario testing.

Customers Bargaining Power

Professional buyers and tenders

Developers, contractors and transit authorities run competitive tenders that compress pricing and contractual terms, forcing Schindler to match aggressive bids. Standardized specifications make direct comparisons across top suppliers routine, increasing switching and reducing pricing power. Public-sector bids are significant: OECD estimated public procurement at about 12% of GDP in 2024, amplifying price transparency. Value engineering in new installs commonly trims supplier margins further.

High switching costs post-install

Once installed, proprietary controllers, certified safety ladders and software ecosystems make switching providers costly and risky, with modernization controller replacements typically costing €20,000–€100,000 and downtime in commercial buildings often valued at $1,000–$10,000 per hour (industry 2024 estimates). This materially reduces buyer power in maintenance and modernization phases and supports long-term service contracts that lock in annuity streams. Performance history and uptime KPIs (99%+ targets common) strongly influence renewal leverage.

Total cost of ownership focus

Buyers in 2024 evaluate lifecycle energy use, downtime and maintenance over capex alone, shifting negotiations toward total cost of ownership metrics. Remote monitoring, predictive maintenance and efficient drives allow Schindler to justify premium pricing based on reduced lifecycle costs. Schindler’s ability to quantify TCO savings weakens pure price bargaining. Penalties for SLA breaches keep pressure on delivery and uptime expectations above 99%.

Project cyclicality and timing

Construction cycles let buyers delay or bundle elevator orders to extract better terms, notably in years of weak construction demand; Schindler reported group sales of CHF 12.7bn in 2023, so large multi-building deals can materially shift negotiation leverage. Tight project schedules reduce buyer bargaining power as on-time delivery gains premium; change orders, common in retrofits, can erode margins if scope shifts late.

- Volume leverage: large projects increase buyer bargaining

- Timing risk: tight schedules reduce buyer power

- Bundling: cyclical slowdowns enable order delays

- Scope creep: change orders can claw back margins

Modernization alternatives

Owners often opt for partial modernization, third-party parts, or independent service providers to cut costs; interface openness and compatibility with existing control systems increase their leverage. Schindler defends pricing with OEM warranties, safety upgrades, and digital features like predictive maintenance, while demonstrated compliance and liability support frequently tip procurement toward OEM solutions.

- Levers: partial modernizations, third-party parts, independent servicers

- Key factors: interface openness, compatibility

- Schindler responses: OEM warranties, safety upgrades, digital services

- Decision drivers: compliance evidence, liability protection

Procurement pressure vs high switch costs: modernization €20k–€100k

Competitive tenders and standardized specs compress prices, but high switching costs for controllers and safety systems (modernization €20,000–€100,000; downtime $1,000–$10,000/hr, industry 2024) preserve Schindler’s service leverage; buyers shift to TCO and SLAs (99%+ uptime), while public procurement (≈12% GDP, OECD 2024) and CHF 12.7bn sales (Schindler 2023) shape negotiation dynamics.

| Metric | Value |

|---|---|

| Public procurement | ≈12% GDP (OECD 2024) |

| Schindler sales | CHF 12.7bn (2023) |

| Modernization cost | €20k–€100k (2024) |

| Downtime cost | $1k–$10k/hr (2024) |

| SLA target | 99%+ uptime |

Preview Before You Purchase

Schindler Holding Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Schindler Holding examines competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications with actionable recommendations. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Description

From Overview to Strategy Blueprint

Schindler Holding faces moderate supplier power but high buyer expectations and intense rivalry across global elevator and escalator markets. Technological change and regulatory demands raise barriers yet enable differentiation, while threat of new entrants and substitutes remains manageable. This snapshot highlights key tensions shaping Schindler’s strategy. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated critical components

Advanced drives, controllers, door systems, ropes and safety gear come from a small pool of specialized suppliers, giving those vendors elevated leverage on pricing and lead times. Long safety qualification cycles make rapid substitution costly, so dual-sourcing is used where feasible but some items remain single or limited source. Consolidation in electronics suppliers can amplify this power during shortages, increasing procurement risk for Schindler.

Commodity and semiconductor volatility

Steel, copper and rare materials expose Schindler to cyclical cost swings, while global semiconductor sales of roughly $600 billion in 2024 highlight continued chip market tension that creates allocation risk and production disruptions. Schindler’s scale and hedging strategies mitigate shocks, yet cost pass-through to customers is often delayed. Extended component lead times raise inventories and working capital requirements.

Switching costs and qualification lock-in

Safety and compliance testing to standards EN 81 and ASME A17.1 create high requalification costs for alternative parts, often requiring months of validation. Tooling, software interfaces and firmware compatibility embed suppliers into platform designs, locking in value for incumbent suppliers, especially control systems. Schindler operates in over 100 countries, amplifying lock-in effects. Design-for-multi-sourcing and modularity partly counterbalance.

Aftermarket IP and proprietary parts

Aftermarket IP and proprietary parts tilt leverage toward Schindler when service kits use Schindler-owned modules, supported by an installed base of about 2.1 million units (2024) where service revenues represent roughly 60% of recurring sales; however upstream licensors and patent holders—often concentrated suppliers—retain bargaining power, notably where select makers supply long-tail parts comprising over 20% of replacement spend.

- Installed base: ~2.1M units (2024)

- Service share: ~60% recurring sales

- Long-tail supplier concentration: >20% spend

- Vertical integration: reduces exposure in key modules

Logistics and sustainability constraints

Logistics bottlenecks and stricter sustainability rules narrow Schindler’s supplier options: the EU CSRD extends to roughly 50,000 firms from 2024, increasing Scope 3 traceability demands, while IMO targets require major shipping decarbonization by 2050, pressuring carriers and component suppliers. Compliance and ESG audits shrink the vendor pool and can raise supplier leverage; regional nearshoring boosts resilience but reduces lowest-cost sourcing. Collaboration on supplier decarbonization becomes a commercial negotiating tool, potentially traded for price or long-term contracts.

- CSRD ~50,000 firms (2024) raises Scope 3 reporting

- IMO 2050 GHG reduction target tightens shipping suppliers

- Regionalization improves resilience, limits cheapest sourcing

- ESG audits narrow vendors, lifting supplier bargaining

Specialized elevator suppliers gain leverage; installed base 2.1M

Specialized elevator components and long safety qualifications give suppliers pricing and lead-time leverage; dual-sourcing limited. Schindler scale and vertical integration mitigate but exposure remains: installed base ~2.1M (2024), service ~60% recurring sales, semiconductor market ~$600B (2024). ESG/regulation (CSRD ~50,000 firms, IMO 2050) narrows vendor pool, raising supplier power.

| Metric | Value |

|---|---|

| Installed base | ~2.1M (2024) |

| Service share | ~60% |

| Chip market | $600B (2024) |

| CSRD scope | ~50,000 firms (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Schindler Holding, uncovering competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive technologies and market entry barriers to inform strategic decisions.

One-sheet Porter's Five Forces for Schindler Holding that instantly visualizes competitive pressure with a spider chart and customizable score inputs—ready to drop into pitch decks or board reports. No macros, editable labels, and seamless Excel integration for scenario testing.

Customers Bargaining Power

Professional buyers and tenders

Developers, contractors and transit authorities run competitive tenders that compress pricing and contractual terms, forcing Schindler to match aggressive bids. Standardized specifications make direct comparisons across top suppliers routine, increasing switching and reducing pricing power. Public-sector bids are significant: OECD estimated public procurement at about 12% of GDP in 2024, amplifying price transparency. Value engineering in new installs commonly trims supplier margins further.

High switching costs post-install

Once installed, proprietary controllers, certified safety ladders and software ecosystems make switching providers costly and risky, with modernization controller replacements typically costing €20,000–€100,000 and downtime in commercial buildings often valued at $1,000–$10,000 per hour (industry 2024 estimates). This materially reduces buyer power in maintenance and modernization phases and supports long-term service contracts that lock in annuity streams. Performance history and uptime KPIs (99%+ targets common) strongly influence renewal leverage.

Total cost of ownership focus

Buyers in 2024 evaluate lifecycle energy use, downtime and maintenance over capex alone, shifting negotiations toward total cost of ownership metrics. Remote monitoring, predictive maintenance and efficient drives allow Schindler to justify premium pricing based on reduced lifecycle costs. Schindler’s ability to quantify TCO savings weakens pure price bargaining. Penalties for SLA breaches keep pressure on delivery and uptime expectations above 99%.

Project cyclicality and timing

Construction cycles let buyers delay or bundle elevator orders to extract better terms, notably in years of weak construction demand; Schindler reported group sales of CHF 12.7bn in 2023, so large multi-building deals can materially shift negotiation leverage. Tight project schedules reduce buyer bargaining power as on-time delivery gains premium; change orders, common in retrofits, can erode margins if scope shifts late.

- Volume leverage: large projects increase buyer bargaining

- Timing risk: tight schedules reduce buyer power

- Bundling: cyclical slowdowns enable order delays

- Scope creep: change orders can claw back margins

Modernization alternatives

Owners often opt for partial modernization, third-party parts, or independent service providers to cut costs; interface openness and compatibility with existing control systems increase their leverage. Schindler defends pricing with OEM warranties, safety upgrades, and digital features like predictive maintenance, while demonstrated compliance and liability support frequently tip procurement toward OEM solutions.

- Levers: partial modernizations, third-party parts, independent servicers

- Key factors: interface openness, compatibility

- Schindler responses: OEM warranties, safety upgrades, digital services

- Decision drivers: compliance evidence, liability protection

Procurement pressure vs high switch costs: modernization €20k–€100k

Competitive tenders and standardized specs compress prices, but high switching costs for controllers and safety systems (modernization €20,000–€100,000; downtime $1,000–$10,000/hr, industry 2024) preserve Schindler’s service leverage; buyers shift to TCO and SLAs (99%+ uptime), while public procurement (≈12% GDP, OECD 2024) and CHF 12.7bn sales (Schindler 2023) shape negotiation dynamics.

| Metric | Value |

|---|---|

| Public procurement | ≈12% GDP (OECD 2024) |

| Schindler sales | CHF 12.7bn (2023) |

| Modernization cost | €20k–€100k (2024) |

| Downtime cost | $1k–$10k/hr (2024) |

| SLA target | 99%+ uptime |

Preview Before You Purchase

Schindler Holding Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Schindler Holding examines competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications with actionable recommendations. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.