Schreiber Foods Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

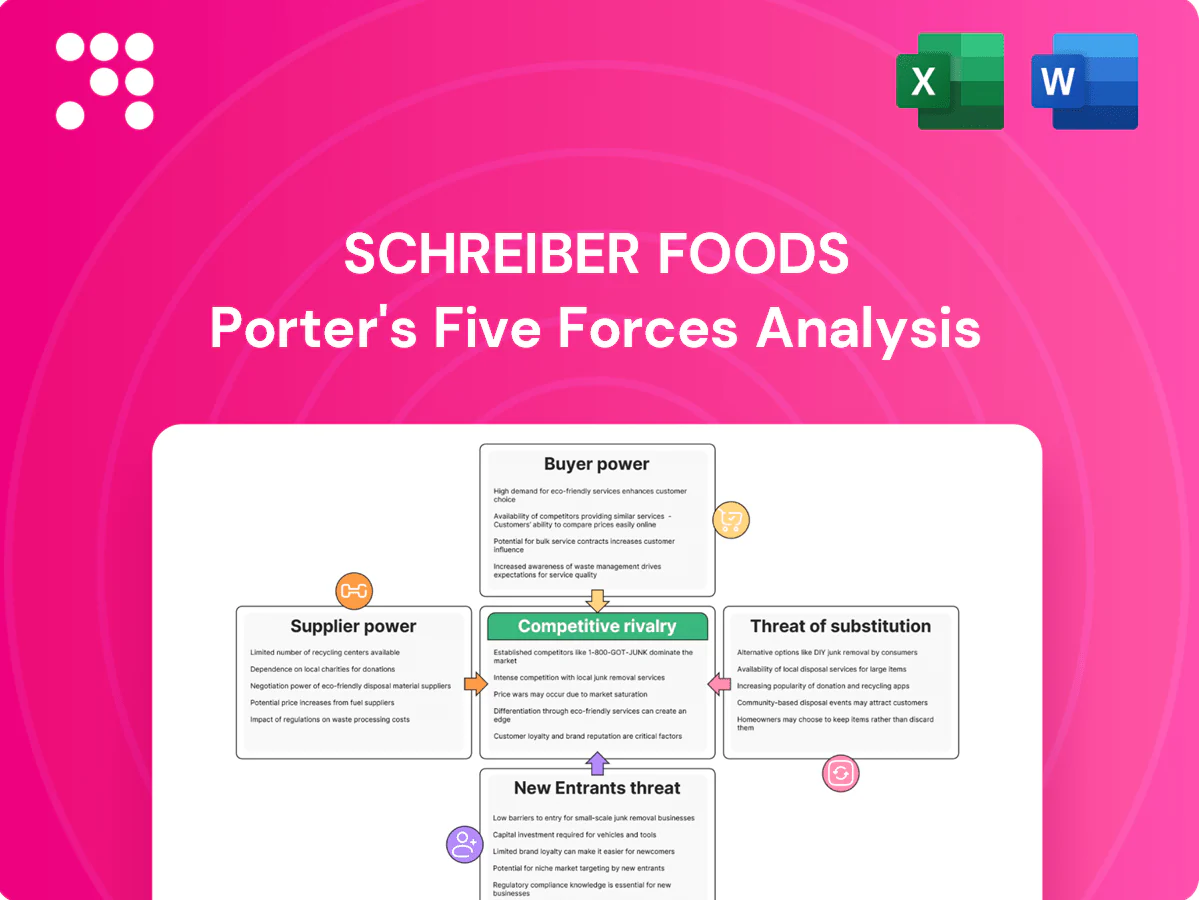

Schreiber Foods faces moderate supplier power, high buyer sensitivity, steady rivalry, limited new-entrant threat, and growing substitute risks as value-added dairy trends shift margins. This snapshot highlights key strategic pressures shaping performance and margins. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Concentrated milk supply regions

Raw milk sourcing is highly concentrated, with major cooperatives like Dairy Farmers of America handling about 20% of U.S. milk volumes, giving them leverage on pricing and volumes. Schreiber’s global footprint across multiple countries diversifies origin risk, but transport costs and perishability limit long-haul flexibility. Seasonal swings and weather-driven production drops can tighten regional supply. Supplier power rises sharply in tight markets.

Input price volatility

Feed, energy and transport costs flow through to farm-gate milk prices, pushing U.S. all-milk value up to about $25.90 per cwt in 2024 and amplifying input pass-through to processors like Schreiber Foods. Volatility in Class prices and international powder markets (SMP/MP) pressured margins through 2024; hedging reduced but did not eliminate swings. Suppliers gain clout when prices spike rapidly, constraining negotiating leverage.

Quality and compliance requirements

Food safety, animal welfare and sustainability standards shrink interchangeable suppliers: organic/third-party certified milk was about 3% of US production in 2024 and certified pools often command 15–25% price premiums. Traceability systems and GFSI-style audits (commonly $5k–15k annually) raise switching costs and documentation burdens, increasing supplier bargaining leverage for Schreiber Foods.

Alternative ingredient options

- Commodity substitutability: moderating

- Global whey market 2024: ~USD 7B

- Specialized cultures/emulsifiers: concentrated suppliers

- Net effect: reduced but persistent supplier power

Long-term contracts and co-op relationships

Long-term multi-year contracts stabilize Schreiber Foods’ input volumes but often embed price-escalators that shift cost risk back to the buyer; cooperative suppliers negotiating collectively increase supplier leverage. Schreiber’s scale and diversified footprint provide countervailing power in negotiations, but balance hinges on market cycle and specific contract clauses. In 2024 dairy cooperatives marketed about 80% of U.S. milk, reinforcing collective bargaining strength.

- Contracts: multi-year stability vs embedded escalators

- Co-ops: ~80% U.S. milk marketed in 2024

- Schreiber scale: countervailing bargaining power

- Outcome: depends on cycle and contract structure

Co-op control 80% drives supplier leverage; organic small, whey USD 7B

Supplier power is moderate-to-high: U.S. cooperatives marketed ~80% of milk in 2024, concentrating negotiating leverage. All-milk value averaged about $25.90 per cwt in 2024 and spikes tighten supply bargaining; organic/third-party milk ~3% of U.S. production with 15–25% premiums. Commodity whey market (~USD 7B in 2024) and substitutable inputs dilute but specialized cultures/emulsifiers keep pockets of supplier power.

| Metric | 2024 Value |

|---|---|

| U.S. milk marketed by co-ops | ~80% |

| All-milk value | $25.90 per cwt |

| Organic milk share | ~3% |

| Organic premium | 15–25% |

| Global whey market | ~USD 7B |

What is included in the product

Tailored Porter's Five Forces analysis for Schreiber Foods that uncovers key drivers of competition, buyer and supplier bargaining power, and market entry risks specific to dairy and cheese value chains. Evaluates disruptive substitutes, emerging threats, and structural barriers that influence Schreiber's pricing power and profitability.

A concise, one-sheet Porter's Five Forces for Schreiber Foods—instantly reveal supplier, buyer, rivalry, entrant, and substitute pressures with customizable scenario sliders and a radar chart for rapid strategic decisions.

Customers Bargaining Power

Large retail and foodservice chains

Major grocers and QSRs buy at scale—Walmart (~25% US grocery share in 2024) and Kroger (~10%) negotiate aggressively with suppliers, pressuring margins. Rising private-label penetration (≈18% of US grocery sales in 2024) intensifies price and service demands on Schreiber Foods. Large buyers commonly dual-source ingredients to maintain leverage, and their purchasing scale translates into strong bargaining power.

Price transparency in commodities

Widespread visibility of CME 40-lb block cheese (avg ~$1.85/lb in 2024) and Class III milk futures (avg ~$17.50/cwt in 2024) anchors buyer expectations and compresses negotiation room. Cost-plus contracting with formulae tied to these indices caps upside on Schreiber Foods margins. Buyers demand faster pass-throughs when reference prices fall than when they rise, and this transparency amplifies buyer leverage in pricing talks.

Switching and qualification costs

While audits, trials and spec qualifications create formal barriers, experienced food-industry buyers routinely manage vendor transitions through standardized protocols and supplier scorecards. Multi-plant suppliers offering redundant capacity reduce supply-risk and therefore slightly lower perceived switching costs. For custom formulations with unique processing parameters, switching remains time-consuming due to revalidation and pilot runs. Net buyer power is high but meaningfully tempered by these technical frictions.

Service and logistics expectations

Buyers demand OTIF 95%+ performance, reliable cold-chain integrity and 24–48 hour rapid replenishment as table stakes; breaches invite penalties and scorecards that extract concessions. Penalty regimes and retailer scorecards (used widely by major grocers) convert service metrics into bargaining leverage. Offering value-added services (co-packing, category management) helps defend pricing but raises operating complexity and cost.

- OTIF target: 95%+

- Cold-chain uptime critical for dairy shelf-life

- Rapid replenishment: 24–48 hours

- Penalties/scorecards used to force concessions

- Value-added services = price defense but +operational complexity

Private label vs. branded dynamics

Private label growth (about 18% of US grocery sales in 2024) heightens price sensitivity and commoditization, pressuring margins. Branded customers value consistency and may pay a premium, yet they still negotiate hard on contract manufacturing. Schreiber’s limited consumer brand pull constrains pricing power, leaving buyers with the upper hand.

- Private label share ~18% (2024)

- Contract manufacturing faces aggressive buyer negotiation

- Limited brand pull reduces Schreiber pricing leverage

Top grocers' scale, private label rise and commodity indices squeeze supplier margins

Buyers wield high bargaining power: Walmart (~25% US grocery share 2024) and Kroger (~10%) force pricing/terms; private label ~18% of US grocery sales in 2024 increases pressure. Price indices (CME block ~$1.85/lb; Class III milk ~$17.50/cwt in 2024) anchor contracts and compress margins. Service metrics (OTIF 95%+) and penalties further shift leverage to buyers.

| Metric | 2024 |

|---|---|

| Walmart share | ~25% |

| Kroger share | ~10% |

| Private label | ~18% |

| CME block | $1.85/lb |

| Class III milk | $17.50/cwt |

| OTIF target | 95%+ |

Full Version Awaits

Schreiber Foods Porter's Five Forces Analysis

This Schreiber Foods Porter's Five Forces Analysis preview is the exact, professionally written document you’ll receive immediately after purchase—no samples or placeholders. It contains the full competitive assessment, formatted and ready for download and use upon payment. What you see is what you get.

A Must-Have Tool for Decision-Makers

Schreiber Foods faces moderate supplier power, high buyer sensitivity, steady rivalry, limited new-entrant threat, and growing substitute risks as value-added dairy trends shift margins. This snapshot highlights key strategic pressures shaping performance and margins. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Concentrated milk supply regions

Raw milk sourcing is highly concentrated, with major cooperatives like Dairy Farmers of America handling about 20% of U.S. milk volumes, giving them leverage on pricing and volumes. Schreiber’s global footprint across multiple countries diversifies origin risk, but transport costs and perishability limit long-haul flexibility. Seasonal swings and weather-driven production drops can tighten regional supply. Supplier power rises sharply in tight markets.

Input price volatility

Feed, energy and transport costs flow through to farm-gate milk prices, pushing U.S. all-milk value up to about $25.90 per cwt in 2024 and amplifying input pass-through to processors like Schreiber Foods. Volatility in Class prices and international powder markets (SMP/MP) pressured margins through 2024; hedging reduced but did not eliminate swings. Suppliers gain clout when prices spike rapidly, constraining negotiating leverage.

Quality and compliance requirements

Food safety, animal welfare and sustainability standards shrink interchangeable suppliers: organic/third-party certified milk was about 3% of US production in 2024 and certified pools often command 15–25% price premiums. Traceability systems and GFSI-style audits (commonly $5k–15k annually) raise switching costs and documentation burdens, increasing supplier bargaining leverage for Schreiber Foods.

Alternative ingredient options

- Commodity substitutability: moderating

- Global whey market 2024: ~USD 7B

- Specialized cultures/emulsifiers: concentrated suppliers

- Net effect: reduced but persistent supplier power

Long-term contracts and co-op relationships

Long-term multi-year contracts stabilize Schreiber Foods’ input volumes but often embed price-escalators that shift cost risk back to the buyer; cooperative suppliers negotiating collectively increase supplier leverage. Schreiber’s scale and diversified footprint provide countervailing power in negotiations, but balance hinges on market cycle and specific contract clauses. In 2024 dairy cooperatives marketed about 80% of U.S. milk, reinforcing collective bargaining strength.

- Contracts: multi-year stability vs embedded escalators

- Co-ops: ~80% U.S. milk marketed in 2024

- Schreiber scale: countervailing bargaining power

- Outcome: depends on cycle and contract structure

Co-op control 80% drives supplier leverage; organic small, whey USD 7B

Supplier power is moderate-to-high: U.S. cooperatives marketed ~80% of milk in 2024, concentrating negotiating leverage. All-milk value averaged about $25.90 per cwt in 2024 and spikes tighten supply bargaining; organic/third-party milk ~3% of U.S. production with 15–25% premiums. Commodity whey market (~USD 7B in 2024) and substitutable inputs dilute but specialized cultures/emulsifiers keep pockets of supplier power.

| Metric | 2024 Value |

|---|---|

| U.S. milk marketed by co-ops | ~80% |

| All-milk value | $25.90 per cwt |

| Organic milk share | ~3% |

| Organic premium | 15–25% |

| Global whey market | ~USD 7B |

What is included in the product

Tailored Porter's Five Forces analysis for Schreiber Foods that uncovers key drivers of competition, buyer and supplier bargaining power, and market entry risks specific to dairy and cheese value chains. Evaluates disruptive substitutes, emerging threats, and structural barriers that influence Schreiber's pricing power and profitability.

A concise, one-sheet Porter's Five Forces for Schreiber Foods—instantly reveal supplier, buyer, rivalry, entrant, and substitute pressures with customizable scenario sliders and a radar chart for rapid strategic decisions.

Customers Bargaining Power

Large retail and foodservice chains

Major grocers and QSRs buy at scale—Walmart (~25% US grocery share in 2024) and Kroger (~10%) negotiate aggressively with suppliers, pressuring margins. Rising private-label penetration (≈18% of US grocery sales in 2024) intensifies price and service demands on Schreiber Foods. Large buyers commonly dual-source ingredients to maintain leverage, and their purchasing scale translates into strong bargaining power.

Price transparency in commodities

Widespread visibility of CME 40-lb block cheese (avg ~$1.85/lb in 2024) and Class III milk futures (avg ~$17.50/cwt in 2024) anchors buyer expectations and compresses negotiation room. Cost-plus contracting with formulae tied to these indices caps upside on Schreiber Foods margins. Buyers demand faster pass-throughs when reference prices fall than when they rise, and this transparency amplifies buyer leverage in pricing talks.

Switching and qualification costs

While audits, trials and spec qualifications create formal barriers, experienced food-industry buyers routinely manage vendor transitions through standardized protocols and supplier scorecards. Multi-plant suppliers offering redundant capacity reduce supply-risk and therefore slightly lower perceived switching costs. For custom formulations with unique processing parameters, switching remains time-consuming due to revalidation and pilot runs. Net buyer power is high but meaningfully tempered by these technical frictions.

Service and logistics expectations

Buyers demand OTIF 95%+ performance, reliable cold-chain integrity and 24–48 hour rapid replenishment as table stakes; breaches invite penalties and scorecards that extract concessions. Penalty regimes and retailer scorecards (used widely by major grocers) convert service metrics into bargaining leverage. Offering value-added services (co-packing, category management) helps defend pricing but raises operating complexity and cost.

- OTIF target: 95%+

- Cold-chain uptime critical for dairy shelf-life

- Rapid replenishment: 24–48 hours

- Penalties/scorecards used to force concessions

- Value-added services = price defense but +operational complexity

Private label vs. branded dynamics

Private label growth (about 18% of US grocery sales in 2024) heightens price sensitivity and commoditization, pressuring margins. Branded customers value consistency and may pay a premium, yet they still negotiate hard on contract manufacturing. Schreiber’s limited consumer brand pull constrains pricing power, leaving buyers with the upper hand.

- Private label share ~18% (2024)

- Contract manufacturing faces aggressive buyer negotiation

- Limited brand pull reduces Schreiber pricing leverage

Top grocers' scale, private label rise and commodity indices squeeze supplier margins

Buyers wield high bargaining power: Walmart (~25% US grocery share 2024) and Kroger (~10%) force pricing/terms; private label ~18% of US grocery sales in 2024 increases pressure. Price indices (CME block ~$1.85/lb; Class III milk ~$17.50/cwt in 2024) anchor contracts and compress margins. Service metrics (OTIF 95%+) and penalties further shift leverage to buyers.

| Metric | 2024 |

|---|---|

| Walmart share | ~25% |

| Kroger share | ~10% |

| Private label | ~18% |

| CME block | $1.85/lb |

| Class III milk | $17.50/cwt |

| OTIF target | 95%+ |

Full Version Awaits

Schreiber Foods Porter's Five Forces Analysis

This Schreiber Foods Porter's Five Forces Analysis preview is the exact, professionally written document you’ll receive immediately after purchase—no samples or placeholders. It contains the full competitive assessment, formatted and ready for download and use upon payment. What you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Schreiber Foods faces moderate supplier power, high buyer sensitivity, steady rivalry, limited new-entrant threat, and growing substitute risks as value-added dairy trends shift margins. This snapshot highlights key strategic pressures shaping performance and margins. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Concentrated milk supply regions

Raw milk sourcing is highly concentrated, with major cooperatives like Dairy Farmers of America handling about 20% of U.S. milk volumes, giving them leverage on pricing and volumes. Schreiber’s global footprint across multiple countries diversifies origin risk, but transport costs and perishability limit long-haul flexibility. Seasonal swings and weather-driven production drops can tighten regional supply. Supplier power rises sharply in tight markets.

Input price volatility

Feed, energy and transport costs flow through to farm-gate milk prices, pushing U.S. all-milk value up to about $25.90 per cwt in 2024 and amplifying input pass-through to processors like Schreiber Foods. Volatility in Class prices and international powder markets (SMP/MP) pressured margins through 2024; hedging reduced but did not eliminate swings. Suppliers gain clout when prices spike rapidly, constraining negotiating leverage.

Quality and compliance requirements

Food safety, animal welfare and sustainability standards shrink interchangeable suppliers: organic/third-party certified milk was about 3% of US production in 2024 and certified pools often command 15–25% price premiums. Traceability systems and GFSI-style audits (commonly $5k–15k annually) raise switching costs and documentation burdens, increasing supplier bargaining leverage for Schreiber Foods.

Alternative ingredient options

- Commodity substitutability: moderating

- Global whey market 2024: ~USD 7B

- Specialized cultures/emulsifiers: concentrated suppliers

- Net effect: reduced but persistent supplier power

Long-term contracts and co-op relationships

Long-term multi-year contracts stabilize Schreiber Foods’ input volumes but often embed price-escalators that shift cost risk back to the buyer; cooperative suppliers negotiating collectively increase supplier leverage. Schreiber’s scale and diversified footprint provide countervailing power in negotiations, but balance hinges on market cycle and specific contract clauses. In 2024 dairy cooperatives marketed about 80% of U.S. milk, reinforcing collective bargaining strength.

- Contracts: multi-year stability vs embedded escalators

- Co-ops: ~80% U.S. milk marketed in 2024

- Schreiber scale: countervailing bargaining power

- Outcome: depends on cycle and contract structure

Co-op control 80% drives supplier leverage; organic small, whey USD 7B

Supplier power is moderate-to-high: U.S. cooperatives marketed ~80% of milk in 2024, concentrating negotiating leverage. All-milk value averaged about $25.90 per cwt in 2024 and spikes tighten supply bargaining; organic/third-party milk ~3% of U.S. production with 15–25% premiums. Commodity whey market (~USD 7B in 2024) and substitutable inputs dilute but specialized cultures/emulsifiers keep pockets of supplier power.

| Metric | 2024 Value |

|---|---|

| U.S. milk marketed by co-ops | ~80% |

| All-milk value | $25.90 per cwt |

| Organic milk share | ~3% |

| Organic premium | 15–25% |

| Global whey market | ~USD 7B |

What is included in the product

Tailored Porter's Five Forces analysis for Schreiber Foods that uncovers key drivers of competition, buyer and supplier bargaining power, and market entry risks specific to dairy and cheese value chains. Evaluates disruptive substitutes, emerging threats, and structural barriers that influence Schreiber's pricing power and profitability.

A concise, one-sheet Porter's Five Forces for Schreiber Foods—instantly reveal supplier, buyer, rivalry, entrant, and substitute pressures with customizable scenario sliders and a radar chart for rapid strategic decisions.

Customers Bargaining Power

Large retail and foodservice chains

Major grocers and QSRs buy at scale—Walmart (~25% US grocery share in 2024) and Kroger (~10%) negotiate aggressively with suppliers, pressuring margins. Rising private-label penetration (≈18% of US grocery sales in 2024) intensifies price and service demands on Schreiber Foods. Large buyers commonly dual-source ingredients to maintain leverage, and their purchasing scale translates into strong bargaining power.

Price transparency in commodities

Widespread visibility of CME 40-lb block cheese (avg ~$1.85/lb in 2024) and Class III milk futures (avg ~$17.50/cwt in 2024) anchors buyer expectations and compresses negotiation room. Cost-plus contracting with formulae tied to these indices caps upside on Schreiber Foods margins. Buyers demand faster pass-throughs when reference prices fall than when they rise, and this transparency amplifies buyer leverage in pricing talks.

Switching and qualification costs

While audits, trials and spec qualifications create formal barriers, experienced food-industry buyers routinely manage vendor transitions through standardized protocols and supplier scorecards. Multi-plant suppliers offering redundant capacity reduce supply-risk and therefore slightly lower perceived switching costs. For custom formulations with unique processing parameters, switching remains time-consuming due to revalidation and pilot runs. Net buyer power is high but meaningfully tempered by these technical frictions.

Service and logistics expectations

Buyers demand OTIF 95%+ performance, reliable cold-chain integrity and 24–48 hour rapid replenishment as table stakes; breaches invite penalties and scorecards that extract concessions. Penalty regimes and retailer scorecards (used widely by major grocers) convert service metrics into bargaining leverage. Offering value-added services (co-packing, category management) helps defend pricing but raises operating complexity and cost.

- OTIF target: 95%+

- Cold-chain uptime critical for dairy shelf-life

- Rapid replenishment: 24–48 hours

- Penalties/scorecards used to force concessions

- Value-added services = price defense but +operational complexity

Private label vs. branded dynamics

Private label growth (about 18% of US grocery sales in 2024) heightens price sensitivity and commoditization, pressuring margins. Branded customers value consistency and may pay a premium, yet they still negotiate hard on contract manufacturing. Schreiber’s limited consumer brand pull constrains pricing power, leaving buyers with the upper hand.

- Private label share ~18% (2024)

- Contract manufacturing faces aggressive buyer negotiation

- Limited brand pull reduces Schreiber pricing leverage

Top grocers' scale, private label rise and commodity indices squeeze supplier margins

Buyers wield high bargaining power: Walmart (~25% US grocery share 2024) and Kroger (~10%) force pricing/terms; private label ~18% of US grocery sales in 2024 increases pressure. Price indices (CME block ~$1.85/lb; Class III milk ~$17.50/cwt in 2024) anchor contracts and compress margins. Service metrics (OTIF 95%+) and penalties further shift leverage to buyers.

| Metric | 2024 |

|---|---|

| Walmart share | ~25% |

| Kroger share | ~10% |

| Private label | ~18% |

| CME block | $1.85/lb |

| Class III milk | $17.50/cwt |

| OTIF target | 95%+ |

Full Version Awaits

Schreiber Foods Porter's Five Forces Analysis

This Schreiber Foods Porter's Five Forces Analysis preview is the exact, professionally written document you’ll receive immediately after purchase—no samples or placeholders. It contains the full competitive assessment, formatted and ready for download and use upon payment. What you see is what you get.