Schuler AG PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political, economic and technological forces shape Schuler AG's strategy and market position. Our PESTLE distills risks and opportunities into clear, actionable insights for investors and strategists. Buy the full analysis to access data-driven recommendations, editable deliverables and instant download.

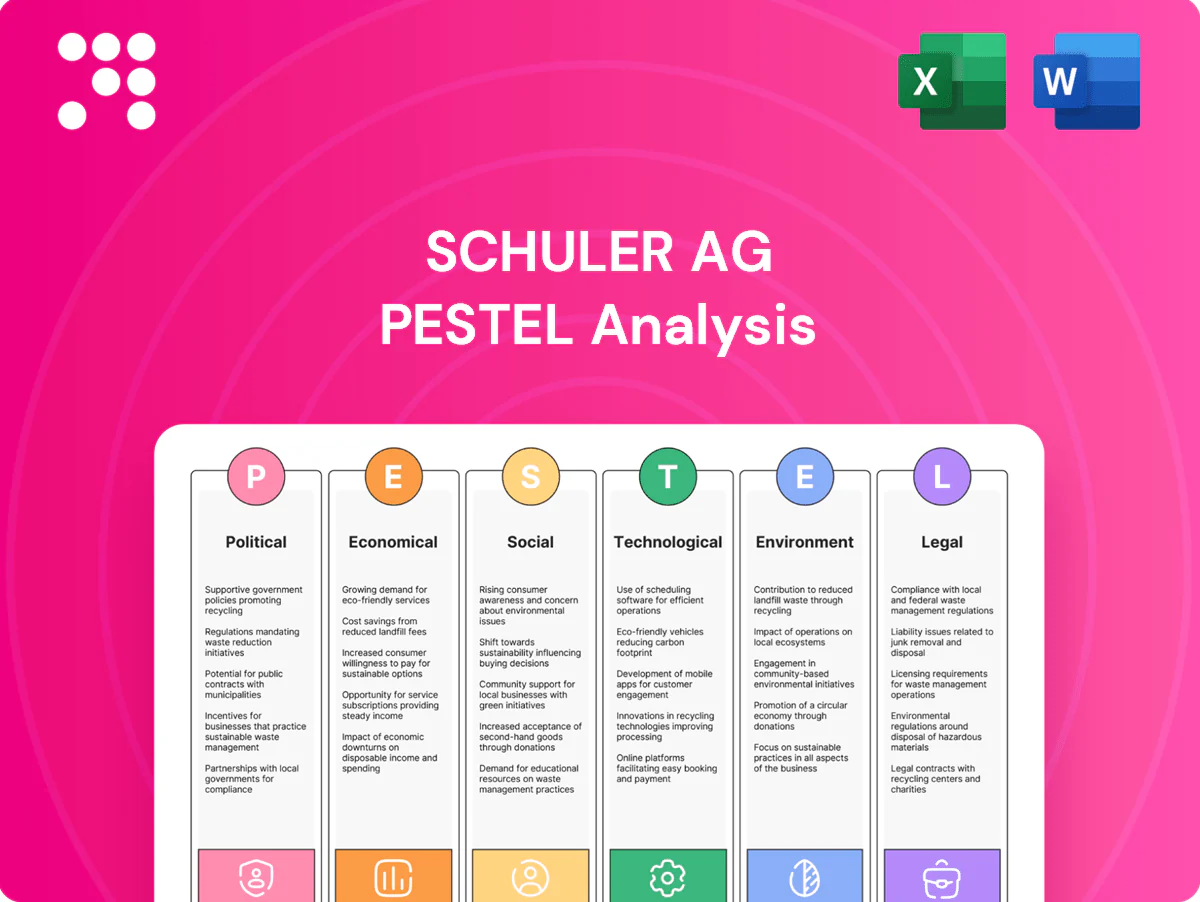

Political factors

Trade policy and tariffs

Schuler’s global sales of presses and dies are highly sensitive to tariffs on machinery and raw materials, with US steel/aluminum tariffs still at 25% under Section 232, directly raising landed costs and compressing pricing power. Shifts in EU, US and China trade relations can change landed costs rapidly; proactive localization and diversified sourcing reduce exposure. Continuous monitoring of WTO cases and regional FTAs is essential for planning.

Industrial policy and subsidies

EU NextGenerationEU recovery package of €723.8bn, the €43bn EU Chips Act and US CHIPS ($52bn) plus the $369bn IRA and EV tax credits up to $7,500 steer OEM capex toward reindustrialization, EVs and advanced manufacturing, accelerating orders for high-efficiency digital presses; aligning product specs with funded programs and public procurement (≈14% of EU GDP) boosts tender success and public-private initiative influence.

Geopolitical risks and sanctions

Sanctions regimes such as EU/US measures remaining in force in 2025 constrain Schuler AGs access to markets and partners, notably affecting trade with Russia and Iran and limiting sales of controlled technologies.

Geopolitical tensions have disrupted supply routes and service commitments, increasing lead times and logistics costs for industrial equipment suppliers since 2022.

Robust compliance screening and dual-use assessments reduce exposure, while redundancy in regional hubs preserves project continuity and aftersales service coverage.

Localization and content rules

Localization and content rules push Schuler AG to expand in-country assembly and service footprints to qualify for government-led automotive and infrastructure projects, improving procurement eligibility and shortening lead times while boosting aftersales resilience.

- Local assembly to meet procurement thresholds

- Regional service centers reduce lead times and downtime

- Partnerships with local firms satisfy policy requirements

Energy and infrastructure policy

Press shops are highly energy-intensive, so grid reliability and energy pricing policies materially affect customer TCO; incentives for energy-efficient presses strengthen Schuler’s value proposition. Policy-driven investments in hydrogen (EU target 10 Mt H2 by 2030) and Germany’s 10 GW electrolysis goal by 2030 will change forming requirements and create new demand—active policy engagement can position Schuler as a preferred technology partner.

- Energy intensity drives TCO

- Efficiency incentives increase sales appeal

- Hydrogen/green steel targets reshape demand

- Policy engagement = strategic advantage

Tariffs, stimulus and green targets drive localization and demand for efficient digital presses

Trade barriers (US 25% Section 232 steel/aluminum), sanctions and rising geopolitical risk since 2022 increase landed costs and lead times, pushing Schuler to localize sourcing and service. EU/US stimulus (NextGenerationEU €723.8bn, IRA $369bn, US CHIPS $52bn) and EV/green steel targets (EU H2 10 Mt by 2030; DE 10 GW electrolysis) shift OEM capex toward efficient, digital presses. Energy policy and procurement rules (public spend ≈14% EU GDP) favor energy-efficient, in‑country solutions.

| Factor | Key 2024/25 Data |

|---|---|

| Tariffs | US steel/aluminium 25% |

| Stimulus | EU €723.8bn; IRA $369bn; CHIPS $52bn |

| Green targets | EU H2 10 Mt; DE 10 GW electrolyzers by 2030 |

What is included in the product

Explains how macro-environmental factors—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Schuler AG, with data-backed trends, region- and industry-relevant insights, forward-looking scenarios, and practical implications to help executives, investors, and advisors identify risks, opportunities and strategic responses.

A concise, visually segmented PESTLE summary of Schuler AG that’s easily editable for local contexts and business lines, ideal for drop‑in slides, team alignment, and client reports to streamline risk discussions and strategic planning.

Economic factors

Automotive capex cycles

Automotive OEM and Tier-1 capex cycles remain the main driver of Schuler AG order intake, tied to model launches, platform shifts and EV programs that require new lines and dies. IEA reports 26 million electric cars in use and EVs reached ~14% of global new-car sales in 2023, sustaining tool demand. During downcycles Schuler shifts revenue mix to retrofit, spare parts and services. Diversification into appliances and electrical product lines cushions cyclicality.

Interest rates and financing

Rising interest rates—ECB deposit rate about 4.00% and 10y Bund near 2.6% in mid‑2024—raise hurdle rates and can delay large capex decisions for Schuler, increasing financing costs for press and line projects. Vendor financing and performance‑based contracts can unlock deals by shifting capex to Opex. Stable service and spare‑parts revenues hedge sales of rate‑sensitive equipment, while coordination with export credit agencies boosts competitiveness.

Commodity prices and input costs

Steel (HRC ~800 USD/t), aluminum (LME ~2,300 USD/t) and copper (LME ~9,500 USD/t) price swings—often 15–25% year-on-year in 2024–25—directly pressure Schuler AGs BOM and margins. Index-linked pricing and commodity hedges have been used to stabilize project economics and lock margins. Customer shifts toward aluminum or high-strength steel as prices change alter tooling specs, while transparent cost pass-through lowers dispute risk.

FX volatility and global footprint

Schuler AG’s multi-currency sales and procurement leave earnings exposed to FX moves; global FX daily turnover was about 7.5 trillion USD per BIS 2022, underlining market volatility. Local sourcing and production provide natural hedges that limit P&L swings, while currency clauses and selective hedges are used on large, long-duration projects; strict pricing discipline is critical in high-volatility markets.

- Multi-currency exposure

- Natural hedging via local production

- Currency clauses/selective hedges

- Pricing discipline essential

Emerging market industrialization

Rising middle classes and expanding manufacturing bases across Asia, MENA and LATAM are enlarging Schuler AGs installed base; IMF data show emerging market growth around 4.0% in 2024, supporting capital equipment demand. Localized, modular lines gain traction amid skills and infrastructure limits, driving tiered portfolios and higher-margin aftermarket services as fleets mature.

- Installed-base growth: EM GDP ~4.0% (IMF 2024)

- Modular lines: address local skills/infrastructure

- Tiered portfolios: capture price-performance tiers

- Aftermarket: recurring revenue from maturing fleets

Tariffs, stimulus and green targets drive localization and demand for efficient digital presses

OEM capex cycles and EV rollout (IEA: 26m EVs; 14% new‑car sales 2023) drive Schuler order demand; EM GDP ~4.0% (IMF 2024) supports aftermarket growth. ECB deposit ~4.0% and 10y Bund ~2.6% (mid‑2024) raise financing costs; vendor financing shifts capex to opex. Commodities HRC ~800 USD/t, Al ~2,300 USD/t, Cu ~9,500 USD/t pressure margins; FX daily turnover ~7.5T USD (BIS 2022).

| Metric | Value |

|---|---|

| EVs (IEA) | 26M / 14% new sales 2023 |

| ECB depo / 10y Bund | ~4.0% / ~2.6% |

| HRC / Al / Cu | 800 / 2,300 / 9,500 USD/t |

| EM GDP (IMF 2024) | ~4.0% |

| FX turnover (BIS 2022) | ~7.5T USD/day |

Full Version Awaits

Schuler AG PESTLE Analysis

This Schuler AG PESTLE Analysis preview is the exact, fully formatted document you’ll receive after purchase. The layout, content, and structure shown here are professional and final—no placeholders or teasers. After checkout you’ll download this same ready-to-use file.

Your Competitive Advantage Starts with This Report

Discover how political, economic and technological forces shape Schuler AG's strategy and market position. Our PESTLE distills risks and opportunities into clear, actionable insights for investors and strategists. Buy the full analysis to access data-driven recommendations, editable deliverables and instant download.

Political factors

Trade policy and tariffs

Schuler’s global sales of presses and dies are highly sensitive to tariffs on machinery and raw materials, with US steel/aluminum tariffs still at 25% under Section 232, directly raising landed costs and compressing pricing power. Shifts in EU, US and China trade relations can change landed costs rapidly; proactive localization and diversified sourcing reduce exposure. Continuous monitoring of WTO cases and regional FTAs is essential for planning.

Industrial policy and subsidies

EU NextGenerationEU recovery package of €723.8bn, the €43bn EU Chips Act and US CHIPS ($52bn) plus the $369bn IRA and EV tax credits up to $7,500 steer OEM capex toward reindustrialization, EVs and advanced manufacturing, accelerating orders for high-efficiency digital presses; aligning product specs with funded programs and public procurement (≈14% of EU GDP) boosts tender success and public-private initiative influence.

Geopolitical risks and sanctions

Sanctions regimes such as EU/US measures remaining in force in 2025 constrain Schuler AGs access to markets and partners, notably affecting trade with Russia and Iran and limiting sales of controlled technologies.

Geopolitical tensions have disrupted supply routes and service commitments, increasing lead times and logistics costs for industrial equipment suppliers since 2022.

Robust compliance screening and dual-use assessments reduce exposure, while redundancy in regional hubs preserves project continuity and aftersales service coverage.

Localization and content rules

Localization and content rules push Schuler AG to expand in-country assembly and service footprints to qualify for government-led automotive and infrastructure projects, improving procurement eligibility and shortening lead times while boosting aftersales resilience.

- Local assembly to meet procurement thresholds

- Regional service centers reduce lead times and downtime

- Partnerships with local firms satisfy policy requirements

Energy and infrastructure policy

Press shops are highly energy-intensive, so grid reliability and energy pricing policies materially affect customer TCO; incentives for energy-efficient presses strengthen Schuler’s value proposition. Policy-driven investments in hydrogen (EU target 10 Mt H2 by 2030) and Germany’s 10 GW electrolysis goal by 2030 will change forming requirements and create new demand—active policy engagement can position Schuler as a preferred technology partner.

- Energy intensity drives TCO

- Efficiency incentives increase sales appeal

- Hydrogen/green steel targets reshape demand

- Policy engagement = strategic advantage

Tariffs, stimulus and green targets drive localization and demand for efficient digital presses

Trade barriers (US 25% Section 232 steel/aluminum), sanctions and rising geopolitical risk since 2022 increase landed costs and lead times, pushing Schuler to localize sourcing and service. EU/US stimulus (NextGenerationEU €723.8bn, IRA $369bn, US CHIPS $52bn) and EV/green steel targets (EU H2 10 Mt by 2030; DE 10 GW electrolysis) shift OEM capex toward efficient, digital presses. Energy policy and procurement rules (public spend ≈14% EU GDP) favor energy-efficient, in‑country solutions.

| Factor | Key 2024/25 Data |

|---|---|

| Tariffs | US steel/aluminium 25% |

| Stimulus | EU €723.8bn; IRA $369bn; CHIPS $52bn |

| Green targets | EU H2 10 Mt; DE 10 GW electrolyzers by 2030 |

What is included in the product

Explains how macro-environmental factors—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Schuler AG, with data-backed trends, region- and industry-relevant insights, forward-looking scenarios, and practical implications to help executives, investors, and advisors identify risks, opportunities and strategic responses.

A concise, visually segmented PESTLE summary of Schuler AG that’s easily editable for local contexts and business lines, ideal for drop‑in slides, team alignment, and client reports to streamline risk discussions and strategic planning.

Economic factors

Automotive capex cycles

Automotive OEM and Tier-1 capex cycles remain the main driver of Schuler AG order intake, tied to model launches, platform shifts and EV programs that require new lines and dies. IEA reports 26 million electric cars in use and EVs reached ~14% of global new-car sales in 2023, sustaining tool demand. During downcycles Schuler shifts revenue mix to retrofit, spare parts and services. Diversification into appliances and electrical product lines cushions cyclicality.

Interest rates and financing

Rising interest rates—ECB deposit rate about 4.00% and 10y Bund near 2.6% in mid‑2024—raise hurdle rates and can delay large capex decisions for Schuler, increasing financing costs for press and line projects. Vendor financing and performance‑based contracts can unlock deals by shifting capex to Opex. Stable service and spare‑parts revenues hedge sales of rate‑sensitive equipment, while coordination with export credit agencies boosts competitiveness.

Commodity prices and input costs

Steel (HRC ~800 USD/t), aluminum (LME ~2,300 USD/t) and copper (LME ~9,500 USD/t) price swings—often 15–25% year-on-year in 2024–25—directly pressure Schuler AGs BOM and margins. Index-linked pricing and commodity hedges have been used to stabilize project economics and lock margins. Customer shifts toward aluminum or high-strength steel as prices change alter tooling specs, while transparent cost pass-through lowers dispute risk.

FX volatility and global footprint

Schuler AG’s multi-currency sales and procurement leave earnings exposed to FX moves; global FX daily turnover was about 7.5 trillion USD per BIS 2022, underlining market volatility. Local sourcing and production provide natural hedges that limit P&L swings, while currency clauses and selective hedges are used on large, long-duration projects; strict pricing discipline is critical in high-volatility markets.

- Multi-currency exposure

- Natural hedging via local production

- Currency clauses/selective hedges

- Pricing discipline essential

Emerging market industrialization

Rising middle classes and expanding manufacturing bases across Asia, MENA and LATAM are enlarging Schuler AGs installed base; IMF data show emerging market growth around 4.0% in 2024, supporting capital equipment demand. Localized, modular lines gain traction amid skills and infrastructure limits, driving tiered portfolios and higher-margin aftermarket services as fleets mature.

- Installed-base growth: EM GDP ~4.0% (IMF 2024)

- Modular lines: address local skills/infrastructure

- Tiered portfolios: capture price-performance tiers

- Aftermarket: recurring revenue from maturing fleets

Tariffs, stimulus and green targets drive localization and demand for efficient digital presses

OEM capex cycles and EV rollout (IEA: 26m EVs; 14% new‑car sales 2023) drive Schuler order demand; EM GDP ~4.0% (IMF 2024) supports aftermarket growth. ECB deposit ~4.0% and 10y Bund ~2.6% (mid‑2024) raise financing costs; vendor financing shifts capex to opex. Commodities HRC ~800 USD/t, Al ~2,300 USD/t, Cu ~9,500 USD/t pressure margins; FX daily turnover ~7.5T USD (BIS 2022).

| Metric | Value |

|---|---|

| EVs (IEA) | 26M / 14% new sales 2023 |

| ECB depo / 10y Bund | ~4.0% / ~2.6% |

| HRC / Al / Cu | 800 / 2,300 / 9,500 USD/t |

| EM GDP (IMF 2024) | ~4.0% |

| FX turnover (BIS 2022) | ~7.5T USD/day |

Full Version Awaits

Schuler AG PESTLE Analysis

This Schuler AG PESTLE Analysis preview is the exact, fully formatted document you’ll receive after purchase. The layout, content, and structure shown here are professional and final—no placeholders or teasers. After checkout you’ll download this same ready-to-use file.

Description

Your Competitive Advantage Starts with This Report

Discover how political, economic and technological forces shape Schuler AG's strategy and market position. Our PESTLE distills risks and opportunities into clear, actionable insights for investors and strategists. Buy the full analysis to access data-driven recommendations, editable deliverables and instant download.

Political factors

Trade policy and tariffs

Schuler’s global sales of presses and dies are highly sensitive to tariffs on machinery and raw materials, with US steel/aluminum tariffs still at 25% under Section 232, directly raising landed costs and compressing pricing power. Shifts in EU, US and China trade relations can change landed costs rapidly; proactive localization and diversified sourcing reduce exposure. Continuous monitoring of WTO cases and regional FTAs is essential for planning.

Industrial policy and subsidies

EU NextGenerationEU recovery package of €723.8bn, the €43bn EU Chips Act and US CHIPS ($52bn) plus the $369bn IRA and EV tax credits up to $7,500 steer OEM capex toward reindustrialization, EVs and advanced manufacturing, accelerating orders for high-efficiency digital presses; aligning product specs with funded programs and public procurement (≈14% of EU GDP) boosts tender success and public-private initiative influence.

Geopolitical risks and sanctions

Sanctions regimes such as EU/US measures remaining in force in 2025 constrain Schuler AGs access to markets and partners, notably affecting trade with Russia and Iran and limiting sales of controlled technologies.

Geopolitical tensions have disrupted supply routes and service commitments, increasing lead times and logistics costs for industrial equipment suppliers since 2022.

Robust compliance screening and dual-use assessments reduce exposure, while redundancy in regional hubs preserves project continuity and aftersales service coverage.

Localization and content rules

Localization and content rules push Schuler AG to expand in-country assembly and service footprints to qualify for government-led automotive and infrastructure projects, improving procurement eligibility and shortening lead times while boosting aftersales resilience.

- Local assembly to meet procurement thresholds

- Regional service centers reduce lead times and downtime

- Partnerships with local firms satisfy policy requirements

Energy and infrastructure policy

Press shops are highly energy-intensive, so grid reliability and energy pricing policies materially affect customer TCO; incentives for energy-efficient presses strengthen Schuler’s value proposition. Policy-driven investments in hydrogen (EU target 10 Mt H2 by 2030) and Germany’s 10 GW electrolysis goal by 2030 will change forming requirements and create new demand—active policy engagement can position Schuler as a preferred technology partner.

- Energy intensity drives TCO

- Efficiency incentives increase sales appeal

- Hydrogen/green steel targets reshape demand

- Policy engagement = strategic advantage

Tariffs, stimulus and green targets drive localization and demand for efficient digital presses

Trade barriers (US 25% Section 232 steel/aluminum), sanctions and rising geopolitical risk since 2022 increase landed costs and lead times, pushing Schuler to localize sourcing and service. EU/US stimulus (NextGenerationEU €723.8bn, IRA $369bn, US CHIPS $52bn) and EV/green steel targets (EU H2 10 Mt by 2030; DE 10 GW electrolysis) shift OEM capex toward efficient, digital presses. Energy policy and procurement rules (public spend ≈14% EU GDP) favor energy-efficient, in‑country solutions.

| Factor | Key 2024/25 Data |

|---|---|

| Tariffs | US steel/aluminium 25% |

| Stimulus | EU €723.8bn; IRA $369bn; CHIPS $52bn |

| Green targets | EU H2 10 Mt; DE 10 GW electrolyzers by 2030 |

What is included in the product

Explains how macro-environmental factors—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Schuler AG, with data-backed trends, region- and industry-relevant insights, forward-looking scenarios, and practical implications to help executives, investors, and advisors identify risks, opportunities and strategic responses.

A concise, visually segmented PESTLE summary of Schuler AG that’s easily editable for local contexts and business lines, ideal for drop‑in slides, team alignment, and client reports to streamline risk discussions and strategic planning.

Economic factors

Automotive capex cycles

Automotive OEM and Tier-1 capex cycles remain the main driver of Schuler AG order intake, tied to model launches, platform shifts and EV programs that require new lines and dies. IEA reports 26 million electric cars in use and EVs reached ~14% of global new-car sales in 2023, sustaining tool demand. During downcycles Schuler shifts revenue mix to retrofit, spare parts and services. Diversification into appliances and electrical product lines cushions cyclicality.

Interest rates and financing

Rising interest rates—ECB deposit rate about 4.00% and 10y Bund near 2.6% in mid‑2024—raise hurdle rates and can delay large capex decisions for Schuler, increasing financing costs for press and line projects. Vendor financing and performance‑based contracts can unlock deals by shifting capex to Opex. Stable service and spare‑parts revenues hedge sales of rate‑sensitive equipment, while coordination with export credit agencies boosts competitiveness.

Commodity prices and input costs

Steel (HRC ~800 USD/t), aluminum (LME ~2,300 USD/t) and copper (LME ~9,500 USD/t) price swings—often 15–25% year-on-year in 2024–25—directly pressure Schuler AGs BOM and margins. Index-linked pricing and commodity hedges have been used to stabilize project economics and lock margins. Customer shifts toward aluminum or high-strength steel as prices change alter tooling specs, while transparent cost pass-through lowers dispute risk.

FX volatility and global footprint

Schuler AG’s multi-currency sales and procurement leave earnings exposed to FX moves; global FX daily turnover was about 7.5 trillion USD per BIS 2022, underlining market volatility. Local sourcing and production provide natural hedges that limit P&L swings, while currency clauses and selective hedges are used on large, long-duration projects; strict pricing discipline is critical in high-volatility markets.

- Multi-currency exposure

- Natural hedging via local production

- Currency clauses/selective hedges

- Pricing discipline essential

Emerging market industrialization

Rising middle classes and expanding manufacturing bases across Asia, MENA and LATAM are enlarging Schuler AGs installed base; IMF data show emerging market growth around 4.0% in 2024, supporting capital equipment demand. Localized, modular lines gain traction amid skills and infrastructure limits, driving tiered portfolios and higher-margin aftermarket services as fleets mature.

- Installed-base growth: EM GDP ~4.0% (IMF 2024)

- Modular lines: address local skills/infrastructure

- Tiered portfolios: capture price-performance tiers

- Aftermarket: recurring revenue from maturing fleets

Tariffs, stimulus and green targets drive localization and demand for efficient digital presses

OEM capex cycles and EV rollout (IEA: 26m EVs; 14% new‑car sales 2023) drive Schuler order demand; EM GDP ~4.0% (IMF 2024) supports aftermarket growth. ECB deposit ~4.0% and 10y Bund ~2.6% (mid‑2024) raise financing costs; vendor financing shifts capex to opex. Commodities HRC ~800 USD/t, Al ~2,300 USD/t, Cu ~9,500 USD/t pressure margins; FX daily turnover ~7.5T USD (BIS 2022).

| Metric | Value |

|---|---|

| EVs (IEA) | 26M / 14% new sales 2023 |

| ECB depo / 10y Bund | ~4.0% / ~2.6% |

| HRC / Al / Cu | 800 / 2,300 / 9,500 USD/t |

| EM GDP (IMF 2024) | ~4.0% |

| FX turnover (BIS 2022) | ~7.5T USD/day |

Full Version Awaits

Schuler AG PESTLE Analysis

This Schuler AG PESTLE Analysis preview is the exact, fully formatted document you’ll receive after purchase. The layout, content, and structure shown here are professional and final—no placeholders or teasers. After checkout you’ll download this same ready-to-use file.