Bank of Nova Scotia Business Model Canvas

Business Model Canvas snapshot: customer segments, revenue streams, competitive edge

Unlock the strategic blueprint behind Bank of Nova Scotia with our concise Business Model Canvas summary that highlights customer segments, revenue streams, and competitive advantages. This snapshot teases the actionable insights investors and strategists need. Purchase the full, editable Canvas to access every building block and drive smarter decisions.

Partnerships

Regulators & Central Banks

Close coordination with the Bank of Canada, OSFI and central banks across Latin America and the Caribbean secures compliance and systemic stability for Scotiabank, which reports over CAD 1.2 trillion in assets and operations in 30+ countries. These regulatory ties enable access to liquidity facilities and major payment rails and inform capital planning and risk practices through ongoing dialogue. Such partnerships underpin trust and Scotiabank's licence to operate.

Payment Networks & Fintechs

Scotiabank leverages Visa (TPV $14.9T in 2023), Mastercard ($8.6T in 2023) and Interac to power cards, wallets and embedded finance while partnering with fintechs to embed services across channels.

Open APIs and co-development accelerate digital features and improved client experience, cutting integration cycles and reducing time-to-market for innovations.

These partnerships extend Scotiabank’s reach into e-commerce and cross-border payments, unlocking new merchant and cross-border revenue streams.

Capital Markets Counterparties

Broker-dealers, exchanges and clearinghouses enable Scotiabank's trading, underwriting and market-making, with clearinghouses handling trillions in daily settlements globally. Syndicate partners expand distribution for debt and equity issues, increasing reach and placement success. ISDA counterparties facilitate standardized derivatives netting and collateral agreements. These relationships underpin liquidity, pricing transparency and timely client execution.

Technology & Cloud Providers

Technology and cloud providers — spanning cloud, core banking, cybersecurity and data vendors — underpin Scotiabank’s scalability and resilience, supporting ~25 million customers and roughly CA$1.2 trillion in assets in 2024; major cloud partnerships drive agility and cost efficiency while analytics and AI vendors improve risk models and personalization, and vendor ecosystems accelerate modernization across regions.

- Cloud partners: agility, cost efficiency

- Core banking: scalability & resilience

- Cybersecurity: fraud prevention & compliance

- Data/AI: enhanced risk models, personalization

Correspondent & Partner Banks

Global correspondent banks expand Scotiabank’s cross-border payments and trade finance reach, supporting clients across over 50 countries and serving about 25 million customers (2024), while local partner banks strengthen presence in smaller or restricted markets. Shared ATM and remittance networks improve accessibility and cost efficiency, enabling seamless international client service and faster settlement.

- Cross-border reach: >50 countries (2024)

- Customer base: ~25 million (2024)

- Shared ATM/remittance networks: improved accessibility and lower costs

Banking ecosystem unlocks CA$1.2T assets, ~25M customers, >50 countries

Scotiabank partners with central banks/OSFI for liquidity and compliance, supporting CA$1.2T assets and ~25M customers (2024). Card networks (Visa TPV US$14.9T 2023, Mastercard US$8.6T 2023) and fintechs drive payments and embedded finance. Cloud, core, cybersecurity and AI vendors accelerate digital scale and risk analytics. Correspondent banks extend cross-border reach to >50 countries.

| Metric | Value |

|---|---|

| Assets | CA$1.2T (2024) |

| Customers | ~25M (2024) |

| Cross-border | >50 countries |

What is included in the product

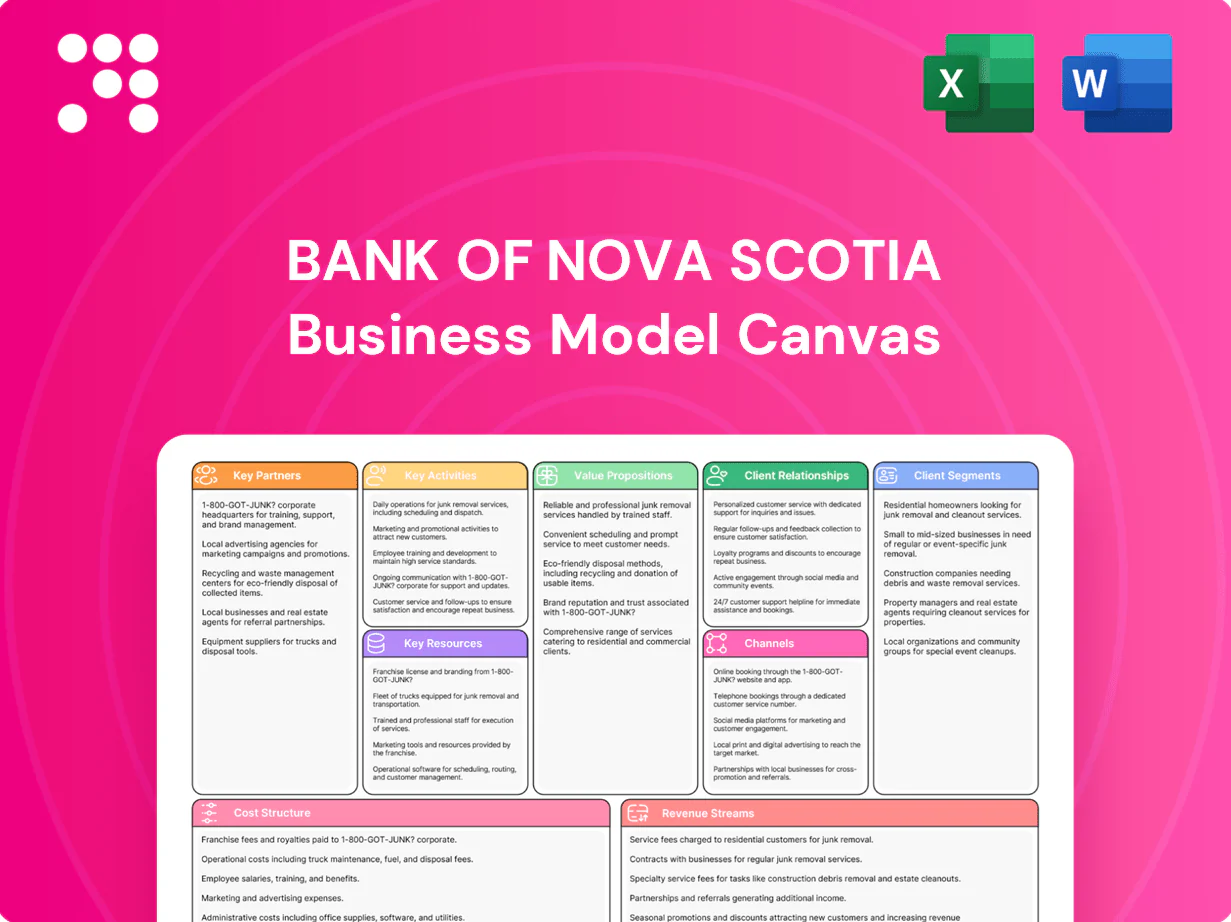

A comprehensive Business Model Canvas for Bank of Nova Scotia that maps customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks, reflecting real-world banking operations and strategic strengths. Ideal for presentations, investor discussions and analyst decision-making with linked SWOT insights and competitive analysis.

High-level view of Scotiabank’s business model with editable cells to quickly surface customer pain points, revenue and cost drivers, and operational bottlenecks for fast problem-solving and team collaboration.

Activities

Deposits & Lending

Originating, underwriting and servicing retail and commercial loans are core to Scotiabank’s intermediation, with FY2024 gross loans ~CAD 450 billion supporting net interest income.

Deposit gathering funds balance-sheet growth and liquidity, with FY2024 total deposits near CAD 550 billion, underpinning lending capacity.

Pricing and risk selection balance margin with credit quality while active portfolio management shifts exposures by cycle and geography to protect CET1 and returns.

Wealth & Advisory

Wealth & Advisory offers financial planning, asset management and private banking to affluent and mass affluent clients, supporting Scotiabank's Global Wealth Management which held about CAD 263 billion in assets under administration in 2024. Discretionary mandates and advisory services increase share of wallet and retention. Product manufacturing plus open architecture broaden investment choice. Fiduciary oversight and suitability remain core compliance pillars.

Capital Markets Services

Capital Markets Services delivers underwriting, M&A advisory, sales & trading and treasury solutions to corporates and institutions, supporting deal origination with research and market insights; in 2024 Scotiabank leveraged its 30+ country Americas footprint to execute cross-border mandates. Risk warehousing and distribution optimize capital use across balance sheet and syndicated channels. These capabilities target scalable corporate and institutional flow across the region.

Risk & Compliance Management

Credit, market, liquidity and operational risk frameworks at Bank of Nova Scotia underpin portfolio resilience and helped maintain a CET1 ratio near 12.3% in 2024; AML, sanctions and conduct controls preserve franchise value and limit regulatory loss exposure. Regular stress testing and ICAAP shape capital and funding plans, while data governance and model risk management ensure measurement reliability.

- Credit/Market/Liquidity/Operational risk: CET1 ~12.3% (2024)

- AML & sanctions controls: protect franchise value

- Stress testing & ICAAP: inform capital/funding

- Data governance & model risk: ensure reliability

Digital Product & Operations

Digital Product & Operations prioritizes mobile and online development to drive self-serve adoption, automating payments, onboarding and servicing for speed and scale; core modernization and cloud migration improve resilience while analytics and personalization lift engagement and retention. Scotiabank serves over 25 million customers globally (2024) and leverages cloud-native stacks to reduce outage risk and accelerate feature delivery.

- Mobile-first self-serve

- Automated payments & onboarding

- Core modernization & cloud migration

- Analytics-driven personalization

CAD450/550/263B loans/deposits/AUA

Originating, underwriting and servicing retail and commercial loans (gross loans ~CAD 450B in 2024) drive net interest income and balance-sheet intermediation. Deposit gathering (~CAD 550B deposits in 2024) funds lending and liquidity. Capital markets, wealth management (AUA ~CAD 263B in 2024) and digital operations scale fee income and reduce costs.

| Metric | 2024 |

|---|---|

| Gross loans | CAD 450B |

| Total deposits | CAD 550B |

| AUA | CAD 263B |

| CET1 ratio | ~12.3% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Bank of Nova Scotia Business Model Canvas you'll receive—it's not a mockup or sample. Upon purchase you'll get this exact, fully editable file with all sections intact and formatted for immediate use. No hidden content or altered layouts: what you see here is the complete deliverable, ready for presenting, editing, or sharing.

Business Model Canvas snapshot: customer segments, revenue streams, competitive edge

Unlock the strategic blueprint behind Bank of Nova Scotia with our concise Business Model Canvas summary that highlights customer segments, revenue streams, and competitive advantages. This snapshot teases the actionable insights investors and strategists need. Purchase the full, editable Canvas to access every building block and drive smarter decisions.

Partnerships

Regulators & Central Banks

Close coordination with the Bank of Canada, OSFI and central banks across Latin America and the Caribbean secures compliance and systemic stability for Scotiabank, which reports over CAD 1.2 trillion in assets and operations in 30+ countries. These regulatory ties enable access to liquidity facilities and major payment rails and inform capital planning and risk practices through ongoing dialogue. Such partnerships underpin trust and Scotiabank's licence to operate.

Payment Networks & Fintechs

Scotiabank leverages Visa (TPV $14.9T in 2023), Mastercard ($8.6T in 2023) and Interac to power cards, wallets and embedded finance while partnering with fintechs to embed services across channels.

Open APIs and co-development accelerate digital features and improved client experience, cutting integration cycles and reducing time-to-market for innovations.

These partnerships extend Scotiabank’s reach into e-commerce and cross-border payments, unlocking new merchant and cross-border revenue streams.

Capital Markets Counterparties

Broker-dealers, exchanges and clearinghouses enable Scotiabank's trading, underwriting and market-making, with clearinghouses handling trillions in daily settlements globally. Syndicate partners expand distribution for debt and equity issues, increasing reach and placement success. ISDA counterparties facilitate standardized derivatives netting and collateral agreements. These relationships underpin liquidity, pricing transparency and timely client execution.

Technology & Cloud Providers

Technology and cloud providers — spanning cloud, core banking, cybersecurity and data vendors — underpin Scotiabank’s scalability and resilience, supporting ~25 million customers and roughly CA$1.2 trillion in assets in 2024; major cloud partnerships drive agility and cost efficiency while analytics and AI vendors improve risk models and personalization, and vendor ecosystems accelerate modernization across regions.

- Cloud partners: agility, cost efficiency

- Core banking: scalability & resilience

- Cybersecurity: fraud prevention & compliance

- Data/AI: enhanced risk models, personalization

Correspondent & Partner Banks

Global correspondent banks expand Scotiabank’s cross-border payments and trade finance reach, supporting clients across over 50 countries and serving about 25 million customers (2024), while local partner banks strengthen presence in smaller or restricted markets. Shared ATM and remittance networks improve accessibility and cost efficiency, enabling seamless international client service and faster settlement.

- Cross-border reach: >50 countries (2024)

- Customer base: ~25 million (2024)

- Shared ATM/remittance networks: improved accessibility and lower costs

Banking ecosystem unlocks CA$1.2T assets, ~25M customers, >50 countries

Scotiabank partners with central banks/OSFI for liquidity and compliance, supporting CA$1.2T assets and ~25M customers (2024). Card networks (Visa TPV US$14.9T 2023, Mastercard US$8.6T 2023) and fintechs drive payments and embedded finance. Cloud, core, cybersecurity and AI vendors accelerate digital scale and risk analytics. Correspondent banks extend cross-border reach to >50 countries.

| Metric | Value |

|---|---|

| Assets | CA$1.2T (2024) |

| Customers | ~25M (2024) |

| Cross-border | >50 countries |

What is included in the product

A comprehensive Business Model Canvas for Bank of Nova Scotia that maps customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks, reflecting real-world banking operations and strategic strengths. Ideal for presentations, investor discussions and analyst decision-making with linked SWOT insights and competitive analysis.

High-level view of Scotiabank’s business model with editable cells to quickly surface customer pain points, revenue and cost drivers, and operational bottlenecks for fast problem-solving and team collaboration.

Activities

Deposits & Lending

Originating, underwriting and servicing retail and commercial loans are core to Scotiabank’s intermediation, with FY2024 gross loans ~CAD 450 billion supporting net interest income.

Deposit gathering funds balance-sheet growth and liquidity, with FY2024 total deposits near CAD 550 billion, underpinning lending capacity.

Pricing and risk selection balance margin with credit quality while active portfolio management shifts exposures by cycle and geography to protect CET1 and returns.

Wealth & Advisory

Wealth & Advisory offers financial planning, asset management and private banking to affluent and mass affluent clients, supporting Scotiabank's Global Wealth Management which held about CAD 263 billion in assets under administration in 2024. Discretionary mandates and advisory services increase share of wallet and retention. Product manufacturing plus open architecture broaden investment choice. Fiduciary oversight and suitability remain core compliance pillars.

Capital Markets Services

Capital Markets Services delivers underwriting, M&A advisory, sales & trading and treasury solutions to corporates and institutions, supporting deal origination with research and market insights; in 2024 Scotiabank leveraged its 30+ country Americas footprint to execute cross-border mandates. Risk warehousing and distribution optimize capital use across balance sheet and syndicated channels. These capabilities target scalable corporate and institutional flow across the region.

Risk & Compliance Management

Credit, market, liquidity and operational risk frameworks at Bank of Nova Scotia underpin portfolio resilience and helped maintain a CET1 ratio near 12.3% in 2024; AML, sanctions and conduct controls preserve franchise value and limit regulatory loss exposure. Regular stress testing and ICAAP shape capital and funding plans, while data governance and model risk management ensure measurement reliability.

- Credit/Market/Liquidity/Operational risk: CET1 ~12.3% (2024)

- AML & sanctions controls: protect franchise value

- Stress testing & ICAAP: inform capital/funding

- Data governance & model risk: ensure reliability

Digital Product & Operations

Digital Product & Operations prioritizes mobile and online development to drive self-serve adoption, automating payments, onboarding and servicing for speed and scale; core modernization and cloud migration improve resilience while analytics and personalization lift engagement and retention. Scotiabank serves over 25 million customers globally (2024) and leverages cloud-native stacks to reduce outage risk and accelerate feature delivery.

- Mobile-first self-serve

- Automated payments & onboarding

- Core modernization & cloud migration

- Analytics-driven personalization

CAD450/550/263B loans/deposits/AUA

Originating, underwriting and servicing retail and commercial loans (gross loans ~CAD 450B in 2024) drive net interest income and balance-sheet intermediation. Deposit gathering (~CAD 550B deposits in 2024) funds lending and liquidity. Capital markets, wealth management (AUA ~CAD 263B in 2024) and digital operations scale fee income and reduce costs.

| Metric | 2024 |

|---|---|

| Gross loans | CAD 450B |

| Total deposits | CAD 550B |

| AUA | CAD 263B |

| CET1 ratio | ~12.3% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Bank of Nova Scotia Business Model Canvas you'll receive—it's not a mockup or sample. Upon purchase you'll get this exact, fully editable file with all sections intact and formatted for immediate use. No hidden content or altered layouts: what you see here is the complete deliverable, ready for presenting, editing, or sharing.

Original: $10.00

-65%$10.00

$3.50Description

Business Model Canvas snapshot: customer segments, revenue streams, competitive edge

Unlock the strategic blueprint behind Bank of Nova Scotia with our concise Business Model Canvas summary that highlights customer segments, revenue streams, and competitive advantages. This snapshot teases the actionable insights investors and strategists need. Purchase the full, editable Canvas to access every building block and drive smarter decisions.

Partnerships

Regulators & Central Banks

Close coordination with the Bank of Canada, OSFI and central banks across Latin America and the Caribbean secures compliance and systemic stability for Scotiabank, which reports over CAD 1.2 trillion in assets and operations in 30+ countries. These regulatory ties enable access to liquidity facilities and major payment rails and inform capital planning and risk practices through ongoing dialogue. Such partnerships underpin trust and Scotiabank's licence to operate.

Payment Networks & Fintechs

Scotiabank leverages Visa (TPV $14.9T in 2023), Mastercard ($8.6T in 2023) and Interac to power cards, wallets and embedded finance while partnering with fintechs to embed services across channels.

Open APIs and co-development accelerate digital features and improved client experience, cutting integration cycles and reducing time-to-market for innovations.

These partnerships extend Scotiabank’s reach into e-commerce and cross-border payments, unlocking new merchant and cross-border revenue streams.

Capital Markets Counterparties

Broker-dealers, exchanges and clearinghouses enable Scotiabank's trading, underwriting and market-making, with clearinghouses handling trillions in daily settlements globally. Syndicate partners expand distribution for debt and equity issues, increasing reach and placement success. ISDA counterparties facilitate standardized derivatives netting and collateral agreements. These relationships underpin liquidity, pricing transparency and timely client execution.

Technology & Cloud Providers

Technology and cloud providers — spanning cloud, core banking, cybersecurity and data vendors — underpin Scotiabank’s scalability and resilience, supporting ~25 million customers and roughly CA$1.2 trillion in assets in 2024; major cloud partnerships drive agility and cost efficiency while analytics and AI vendors improve risk models and personalization, and vendor ecosystems accelerate modernization across regions.

- Cloud partners: agility, cost efficiency

- Core banking: scalability & resilience

- Cybersecurity: fraud prevention & compliance

- Data/AI: enhanced risk models, personalization

Correspondent & Partner Banks

Global correspondent banks expand Scotiabank’s cross-border payments and trade finance reach, supporting clients across over 50 countries and serving about 25 million customers (2024), while local partner banks strengthen presence in smaller or restricted markets. Shared ATM and remittance networks improve accessibility and cost efficiency, enabling seamless international client service and faster settlement.

- Cross-border reach: >50 countries (2024)

- Customer base: ~25 million (2024)

- Shared ATM/remittance networks: improved accessibility and lower costs

Banking ecosystem unlocks CA$1.2T assets, ~25M customers, >50 countries

Scotiabank partners with central banks/OSFI for liquidity and compliance, supporting CA$1.2T assets and ~25M customers (2024). Card networks (Visa TPV US$14.9T 2023, Mastercard US$8.6T 2023) and fintechs drive payments and embedded finance. Cloud, core, cybersecurity and AI vendors accelerate digital scale and risk analytics. Correspondent banks extend cross-border reach to >50 countries.

| Metric | Value |

|---|---|

| Assets | CA$1.2T (2024) |

| Customers | ~25M (2024) |

| Cross-border | >50 countries |

What is included in the product

A comprehensive Business Model Canvas for Bank of Nova Scotia that maps customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks, reflecting real-world banking operations and strategic strengths. Ideal for presentations, investor discussions and analyst decision-making with linked SWOT insights and competitive analysis.

High-level view of Scotiabank’s business model with editable cells to quickly surface customer pain points, revenue and cost drivers, and operational bottlenecks for fast problem-solving and team collaboration.

Activities

Deposits & Lending

Originating, underwriting and servicing retail and commercial loans are core to Scotiabank’s intermediation, with FY2024 gross loans ~CAD 450 billion supporting net interest income.

Deposit gathering funds balance-sheet growth and liquidity, with FY2024 total deposits near CAD 550 billion, underpinning lending capacity.

Pricing and risk selection balance margin with credit quality while active portfolio management shifts exposures by cycle and geography to protect CET1 and returns.

Wealth & Advisory

Wealth & Advisory offers financial planning, asset management and private banking to affluent and mass affluent clients, supporting Scotiabank's Global Wealth Management which held about CAD 263 billion in assets under administration in 2024. Discretionary mandates and advisory services increase share of wallet and retention. Product manufacturing plus open architecture broaden investment choice. Fiduciary oversight and suitability remain core compliance pillars.

Capital Markets Services

Capital Markets Services delivers underwriting, M&A advisory, sales & trading and treasury solutions to corporates and institutions, supporting deal origination with research and market insights; in 2024 Scotiabank leveraged its 30+ country Americas footprint to execute cross-border mandates. Risk warehousing and distribution optimize capital use across balance sheet and syndicated channels. These capabilities target scalable corporate and institutional flow across the region.

Risk & Compliance Management

Credit, market, liquidity and operational risk frameworks at Bank of Nova Scotia underpin portfolio resilience and helped maintain a CET1 ratio near 12.3% in 2024; AML, sanctions and conduct controls preserve franchise value and limit regulatory loss exposure. Regular stress testing and ICAAP shape capital and funding plans, while data governance and model risk management ensure measurement reliability.

- Credit/Market/Liquidity/Operational risk: CET1 ~12.3% (2024)

- AML & sanctions controls: protect franchise value

- Stress testing & ICAAP: inform capital/funding

- Data governance & model risk: ensure reliability

Digital Product & Operations

Digital Product & Operations prioritizes mobile and online development to drive self-serve adoption, automating payments, onboarding and servicing for speed and scale; core modernization and cloud migration improve resilience while analytics and personalization lift engagement and retention. Scotiabank serves over 25 million customers globally (2024) and leverages cloud-native stacks to reduce outage risk and accelerate feature delivery.

- Mobile-first self-serve

- Automated payments & onboarding

- Core modernization & cloud migration

- Analytics-driven personalization

CAD450/550/263B loans/deposits/AUA

Originating, underwriting and servicing retail and commercial loans (gross loans ~CAD 450B in 2024) drive net interest income and balance-sheet intermediation. Deposit gathering (~CAD 550B deposits in 2024) funds lending and liquidity. Capital markets, wealth management (AUA ~CAD 263B in 2024) and digital operations scale fee income and reduce costs.

| Metric | 2024 |

|---|---|

| Gross loans | CAD 450B |

| Total deposits | CAD 550B |

| AUA | CAD 263B |

| CET1 ratio | ~12.3% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Bank of Nova Scotia Business Model Canvas you'll receive—it's not a mockup or sample. Upon purchase you'll get this exact, fully editable file with all sections intact and formatted for immediate use. No hidden content or altered layouts: what you see here is the complete deliverable, ready for presenting, editing, or sharing.