Scoular Porter's Five Forces Analysis

From Overview to Strategy Blueprint

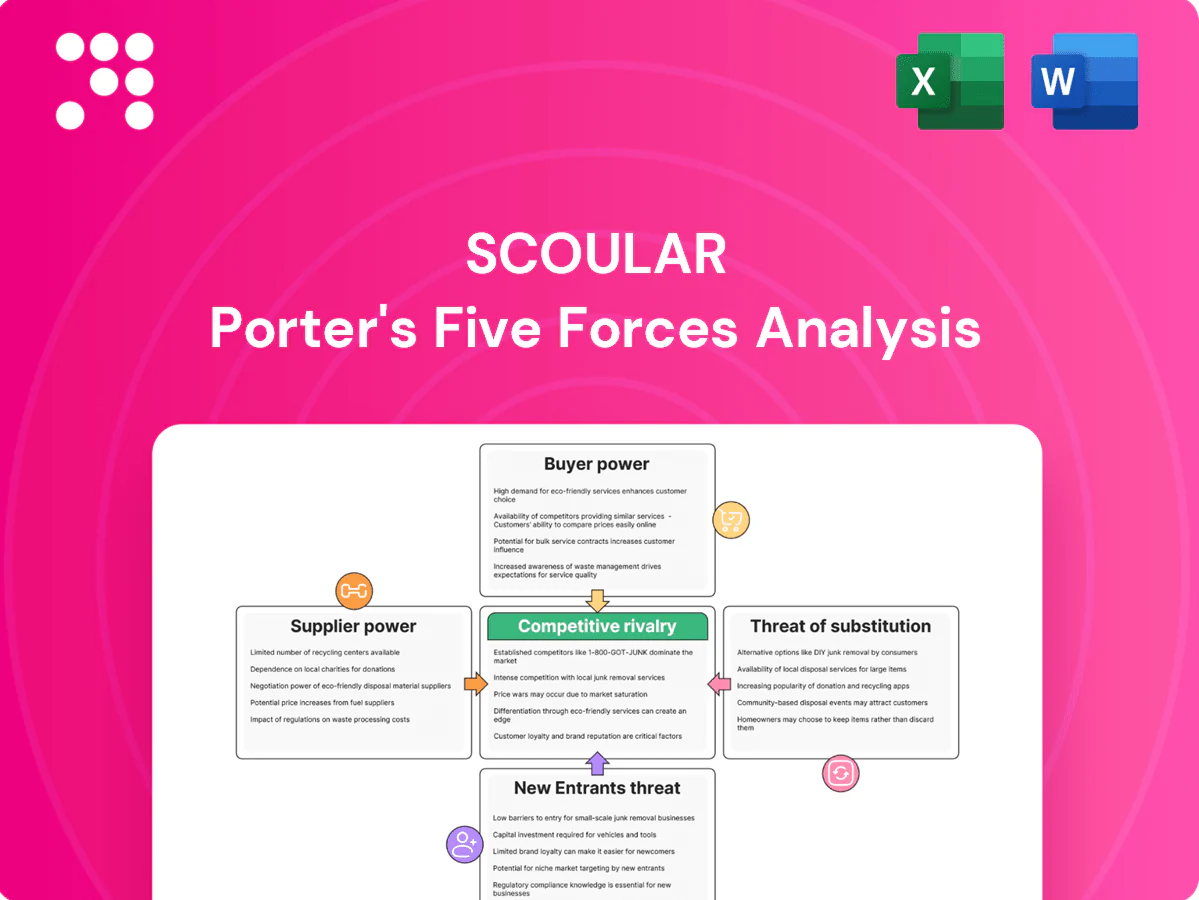

Scoular operates in a tightly contested agribusiness landscape where supplier leverage, buyer concentration, and substitute channels shape margins and strategic options. Our snapshot highlights key pressures—from commodity cyclicality to logistics bottlenecks—that influence Scoular’s competitive posture. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Scoular’s market dynamics and actionable insights in detail.

Suppliers Bargaining Power

Fragmented farm suppliers

Most crop suppliers are diversified, small-to-mid sized producers — the USDA estimated about 1.9 million US farms in 2024 — which limits collective leverage. Fragmentation allows Scoular to multi-source and balance volumes across regions. Co-ops and producer alliances can still secure stronger local terms. Seasonal gluts and harvest pressure further weaken supplier pricing power.

Regional concentration pockets

In certain corridors, a few large growers or co-ops can control more than 60% of origination, raising local supplier power. Limited rail spurs or river access—available at fewer than 30% of local sites—amplify that leverage. Scoular mitigates with a network of 100+ elevators and multi-modal options and secures committed flows through long-term origination programs.

Low switching costs for farmers

Producers can sell to multiple merchandisers with minimal friction, often switching on bid differentials of only $0.02–$0.10 per bushel; basis and freight advantages of a few cents per unit drive rapid movement. Scoular counters with faster inventory turns, transparent grading and value-added services, offering payment cycles typically around 30 days. Deep producer relationships and reliable payouts reduce churn.

Volatility and weather-driven leverage

Tight crops or quality shortfalls give suppliers pricing power, with farmgate premiums swinging up to 25-30% in stress years; bumper harvests can compress those premiums sharply. Scoular’s hedging and risk tools reduced realized margin volatility in 2024 versus 2022 but cannot eliminate weather-driven spikes. Diversified origination across 20+ crops and multiple geographies further dampens local shocks, supporting steadier supply and pricing.

- farmgate premium swings: up to 25-30%

- Scoular: hedging reduced realized margin volatility in 2024

- origination: 20+ crops, multiple geographies

Input traceability and specs

When buyers demand certified, identity-preserved, or sustainable crops in 2024, qualifying suppliers gain measurable leverage as compliant acreage remains limited; scarce compliant acres command observable premiums, and Scoular is expanding traceability programs to grow qualified supply. Data-sharing platforms and agronomy support increase supplier participation and reduce verification friction, shifting negotiating power toward certified growers.

- Certified demand up (2024)

- Scarce compliant acreage = premiums

- Scoular investing in traceability

- Data + agronomy expand supplier pool

Low supplier power amid 1.9M US farms, fragmented origination; premiums spike 25–30% in stress

Supplier power is generally low due to 1.9M US farms (2024) and fragmented origination, enabling Scoular's 100+ elevators and multi-source strategy; local co-ops can concentrate >60% in corridors. Seasonal gluts and easy seller switching (¢0.02–0.10/bu) compress leverage, but tight crops or certified-acre shortages can push farmgate premiums 25–30% in stress years.

| Metric | 2024 |

|---|---|

| US farms | 1.9M |

| Scoular elevators | 100+ |

| Rail/river access at sites | <30% |

| Farmgate premium swing | 25–30% |

| Certified demand | Up (2024) |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for Scoular, uncovering key drivers of competition, supplier and buyer power, substitutes, and entry barriers that shape pricing and profitability. Includes strategic commentary on disruptive threats and market dynamics, delivered in fully editable Word format for use in investor materials, strategy decks, or academic projects.

A concise Scoular Porter's Five Forces one-sheet that visualizes competitive pressure, lets you tweak force levels with real-time data, and exports clean charts for decks—so teams can quickly spot threats, test scenarios, and act without complex tools.

Customers Bargaining Power

Large industrial buyers

Feed mills, food manufacturers, ethanol plants and pet food firms buy at scale—U.S. ethanol plants alone consume roughly 40% of U.S. corn—giving buyers strong leverage. Commodity interchangeability and CBOT benchmark pricing increase price sensitivity. Scoular defends volumes via logistics reliability and tailored blends, while multi-year supply agreements and 2024 fixed-price collars help moderate short-term price squeezes.

Low switching costs among merchandisers

Low switching costs let buyers pivot between merchandisers on price, freight, and service, with basis spreads often settled in cents per bushel and transparent futures/basis markets making comparisons straightforward. Scoular differentiates through multimodal logistics and documented on-time delivery performance, turning speed into a competitive edge. Its embedded risk-management services can lock in margins and create switching frictions tied to cashflow and hedging complexity.

Quality, safety, and traceability demands

High-spec customers increasingly prioritize assured quality, safety, and full traceability over lowest price, shifting bargaining power toward service and certification requirements; Scoular’s processing plants and ISO/HACCP-aligned QA systems provide that assurance, increasing customer stickiness. Premium programs and value-added services further offset buyer price pressure by bundling traceability and supply-chain guarantees. Failure to meet standards risks regulatory penalties and customer churn.

Inventory and working-capital leverage

Buyers push for just-in-time delivery and extended payment terms (commonly 30–90 days), but Scoular’s balance sheet and 220+ storage locations (2024) absorb timing gaps and liquidity strain, shifting inventory risk onto the firm. Financing and vendor-managed inventory move value capture toward Scoular, though carrying costs (~1–2% annual inventory cost) and credit risk must be priced into margins.

- JIT pressure: 30–90 days

- Network: 220+ locations (2024)

- Carrying cost: ~1–2%/yr

- VMI/financing shifts value to Scoular

Global sourcing alternatives

- Import alternatives increase outside options

- Digital marketplaces boost visibility (2024)

- Scoular: ~25 trade lanes

- End-to-end logistics cut switching benefits

Buyers wield leverage; ethanol uses ~40% of US corn; logistics stick

Buyers (feed, ethanol, pet food) hold strong leverage—U.S. ethanol uses ~40% of U.S. corn—and can switch on price, freight and service; Scoular defends via logistics, hedging and multi-year deals. Digital marketplaces (2024) and low switching costs raise transparency; JIT (30–90 days) and extended terms pressure cashflow. Scoular’s 220+ locations (2024) and ~25 trade lanes create stickiness.

| Metric | Value |

|---|---|

| Ethanol corn share | ~40% |

| Storage locations (2024) | 220+ |

| Trade lanes | ~25 |

| Payment terms | 30–90 days |

| Carrying cost | ~1–2%/yr |

Full Version Awaits

Scoular Porter's Five Forces Analysis

This Scoular Porter’s Five Forces analysis provides a concise, actionable assessment of competitive dynamics, supplier and buyer power, threat of entrants and substitutes, and industry rivalry. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted and ready for immediate download and use.

From Overview to Strategy Blueprint

Scoular operates in a tightly contested agribusiness landscape where supplier leverage, buyer concentration, and substitute channels shape margins and strategic options. Our snapshot highlights key pressures—from commodity cyclicality to logistics bottlenecks—that influence Scoular’s competitive posture. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Scoular’s market dynamics and actionable insights in detail.

Suppliers Bargaining Power

Fragmented farm suppliers

Most crop suppliers are diversified, small-to-mid sized producers — the USDA estimated about 1.9 million US farms in 2024 — which limits collective leverage. Fragmentation allows Scoular to multi-source and balance volumes across regions. Co-ops and producer alliances can still secure stronger local terms. Seasonal gluts and harvest pressure further weaken supplier pricing power.

Regional concentration pockets

In certain corridors, a few large growers or co-ops can control more than 60% of origination, raising local supplier power. Limited rail spurs or river access—available at fewer than 30% of local sites—amplify that leverage. Scoular mitigates with a network of 100+ elevators and multi-modal options and secures committed flows through long-term origination programs.

Low switching costs for farmers

Producers can sell to multiple merchandisers with minimal friction, often switching on bid differentials of only $0.02–$0.10 per bushel; basis and freight advantages of a few cents per unit drive rapid movement. Scoular counters with faster inventory turns, transparent grading and value-added services, offering payment cycles typically around 30 days. Deep producer relationships and reliable payouts reduce churn.

Volatility and weather-driven leverage

Tight crops or quality shortfalls give suppliers pricing power, with farmgate premiums swinging up to 25-30% in stress years; bumper harvests can compress those premiums sharply. Scoular’s hedging and risk tools reduced realized margin volatility in 2024 versus 2022 but cannot eliminate weather-driven spikes. Diversified origination across 20+ crops and multiple geographies further dampens local shocks, supporting steadier supply and pricing.

- farmgate premium swings: up to 25-30%

- Scoular: hedging reduced realized margin volatility in 2024

- origination: 20+ crops, multiple geographies

Input traceability and specs

When buyers demand certified, identity-preserved, or sustainable crops in 2024, qualifying suppliers gain measurable leverage as compliant acreage remains limited; scarce compliant acres command observable premiums, and Scoular is expanding traceability programs to grow qualified supply. Data-sharing platforms and agronomy support increase supplier participation and reduce verification friction, shifting negotiating power toward certified growers.

- Certified demand up (2024)

- Scarce compliant acreage = premiums

- Scoular investing in traceability

- Data + agronomy expand supplier pool

Low supplier power amid 1.9M US farms, fragmented origination; premiums spike 25–30% in stress

Supplier power is generally low due to 1.9M US farms (2024) and fragmented origination, enabling Scoular's 100+ elevators and multi-source strategy; local co-ops can concentrate >60% in corridors. Seasonal gluts and easy seller switching (¢0.02–0.10/bu) compress leverage, but tight crops or certified-acre shortages can push farmgate premiums 25–30% in stress years.

| Metric | 2024 |

|---|---|

| US farms | 1.9M |

| Scoular elevators | 100+ |

| Rail/river access at sites | <30% |

| Farmgate premium swing | 25–30% |

| Certified demand | Up (2024) |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for Scoular, uncovering key drivers of competition, supplier and buyer power, substitutes, and entry barriers that shape pricing and profitability. Includes strategic commentary on disruptive threats and market dynamics, delivered in fully editable Word format for use in investor materials, strategy decks, or academic projects.

A concise Scoular Porter's Five Forces one-sheet that visualizes competitive pressure, lets you tweak force levels with real-time data, and exports clean charts for decks—so teams can quickly spot threats, test scenarios, and act without complex tools.

Customers Bargaining Power

Large industrial buyers

Feed mills, food manufacturers, ethanol plants and pet food firms buy at scale—U.S. ethanol plants alone consume roughly 40% of U.S. corn—giving buyers strong leverage. Commodity interchangeability and CBOT benchmark pricing increase price sensitivity. Scoular defends volumes via logistics reliability and tailored blends, while multi-year supply agreements and 2024 fixed-price collars help moderate short-term price squeezes.

Low switching costs among merchandisers

Low switching costs let buyers pivot between merchandisers on price, freight, and service, with basis spreads often settled in cents per bushel and transparent futures/basis markets making comparisons straightforward. Scoular differentiates through multimodal logistics and documented on-time delivery performance, turning speed into a competitive edge. Its embedded risk-management services can lock in margins and create switching frictions tied to cashflow and hedging complexity.

Quality, safety, and traceability demands

High-spec customers increasingly prioritize assured quality, safety, and full traceability over lowest price, shifting bargaining power toward service and certification requirements; Scoular’s processing plants and ISO/HACCP-aligned QA systems provide that assurance, increasing customer stickiness. Premium programs and value-added services further offset buyer price pressure by bundling traceability and supply-chain guarantees. Failure to meet standards risks regulatory penalties and customer churn.

Inventory and working-capital leverage

Buyers push for just-in-time delivery and extended payment terms (commonly 30–90 days), but Scoular’s balance sheet and 220+ storage locations (2024) absorb timing gaps and liquidity strain, shifting inventory risk onto the firm. Financing and vendor-managed inventory move value capture toward Scoular, though carrying costs (~1–2% annual inventory cost) and credit risk must be priced into margins.

- JIT pressure: 30–90 days

- Network: 220+ locations (2024)

- Carrying cost: ~1–2%/yr

- VMI/financing shifts value to Scoular

Global sourcing alternatives

- Import alternatives increase outside options

- Digital marketplaces boost visibility (2024)

- Scoular: ~25 trade lanes

- End-to-end logistics cut switching benefits

Buyers wield leverage; ethanol uses ~40% of US corn; logistics stick

Buyers (feed, ethanol, pet food) hold strong leverage—U.S. ethanol uses ~40% of U.S. corn—and can switch on price, freight and service; Scoular defends via logistics, hedging and multi-year deals. Digital marketplaces (2024) and low switching costs raise transparency; JIT (30–90 days) and extended terms pressure cashflow. Scoular’s 220+ locations (2024) and ~25 trade lanes create stickiness.

| Metric | Value |

|---|---|

| Ethanol corn share | ~40% |

| Storage locations (2024) | 220+ |

| Trade lanes | ~25 |

| Payment terms | 30–90 days |

| Carrying cost | ~1–2%/yr |

Full Version Awaits

Scoular Porter's Five Forces Analysis

This Scoular Porter’s Five Forces analysis provides a concise, actionable assessment of competitive dynamics, supplier and buyer power, threat of entrants and substitutes, and industry rivalry. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Scoular operates in a tightly contested agribusiness landscape where supplier leverage, buyer concentration, and substitute channels shape margins and strategic options. Our snapshot highlights key pressures—from commodity cyclicality to logistics bottlenecks—that influence Scoular’s competitive posture. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Scoular’s market dynamics and actionable insights in detail.

Suppliers Bargaining Power

Fragmented farm suppliers

Most crop suppliers are diversified, small-to-mid sized producers — the USDA estimated about 1.9 million US farms in 2024 — which limits collective leverage. Fragmentation allows Scoular to multi-source and balance volumes across regions. Co-ops and producer alliances can still secure stronger local terms. Seasonal gluts and harvest pressure further weaken supplier pricing power.

Regional concentration pockets

In certain corridors, a few large growers or co-ops can control more than 60% of origination, raising local supplier power. Limited rail spurs or river access—available at fewer than 30% of local sites—amplify that leverage. Scoular mitigates with a network of 100+ elevators and multi-modal options and secures committed flows through long-term origination programs.

Low switching costs for farmers

Producers can sell to multiple merchandisers with minimal friction, often switching on bid differentials of only $0.02–$0.10 per bushel; basis and freight advantages of a few cents per unit drive rapid movement. Scoular counters with faster inventory turns, transparent grading and value-added services, offering payment cycles typically around 30 days. Deep producer relationships and reliable payouts reduce churn.

Volatility and weather-driven leverage

Tight crops or quality shortfalls give suppliers pricing power, with farmgate premiums swinging up to 25-30% in stress years; bumper harvests can compress those premiums sharply. Scoular’s hedging and risk tools reduced realized margin volatility in 2024 versus 2022 but cannot eliminate weather-driven spikes. Diversified origination across 20+ crops and multiple geographies further dampens local shocks, supporting steadier supply and pricing.

- farmgate premium swings: up to 25-30%

- Scoular: hedging reduced realized margin volatility in 2024

- origination: 20+ crops, multiple geographies

Input traceability and specs

When buyers demand certified, identity-preserved, or sustainable crops in 2024, qualifying suppliers gain measurable leverage as compliant acreage remains limited; scarce compliant acres command observable premiums, and Scoular is expanding traceability programs to grow qualified supply. Data-sharing platforms and agronomy support increase supplier participation and reduce verification friction, shifting negotiating power toward certified growers.

- Certified demand up (2024)

- Scarce compliant acreage = premiums

- Scoular investing in traceability

- Data + agronomy expand supplier pool

Low supplier power amid 1.9M US farms, fragmented origination; premiums spike 25–30% in stress

Supplier power is generally low due to 1.9M US farms (2024) and fragmented origination, enabling Scoular's 100+ elevators and multi-source strategy; local co-ops can concentrate >60% in corridors. Seasonal gluts and easy seller switching (¢0.02–0.10/bu) compress leverage, but tight crops or certified-acre shortages can push farmgate premiums 25–30% in stress years.

| Metric | 2024 |

|---|---|

| US farms | 1.9M |

| Scoular elevators | 100+ |

| Rail/river access at sites | <30% |

| Farmgate premium swing | 25–30% |

| Certified demand | Up (2024) |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for Scoular, uncovering key drivers of competition, supplier and buyer power, substitutes, and entry barriers that shape pricing and profitability. Includes strategic commentary on disruptive threats and market dynamics, delivered in fully editable Word format for use in investor materials, strategy decks, or academic projects.

A concise Scoular Porter's Five Forces one-sheet that visualizes competitive pressure, lets you tweak force levels with real-time data, and exports clean charts for decks—so teams can quickly spot threats, test scenarios, and act without complex tools.

Customers Bargaining Power

Large industrial buyers

Feed mills, food manufacturers, ethanol plants and pet food firms buy at scale—U.S. ethanol plants alone consume roughly 40% of U.S. corn—giving buyers strong leverage. Commodity interchangeability and CBOT benchmark pricing increase price sensitivity. Scoular defends volumes via logistics reliability and tailored blends, while multi-year supply agreements and 2024 fixed-price collars help moderate short-term price squeezes.

Low switching costs among merchandisers

Low switching costs let buyers pivot between merchandisers on price, freight, and service, with basis spreads often settled in cents per bushel and transparent futures/basis markets making comparisons straightforward. Scoular differentiates through multimodal logistics and documented on-time delivery performance, turning speed into a competitive edge. Its embedded risk-management services can lock in margins and create switching frictions tied to cashflow and hedging complexity.

Quality, safety, and traceability demands

High-spec customers increasingly prioritize assured quality, safety, and full traceability over lowest price, shifting bargaining power toward service and certification requirements; Scoular’s processing plants and ISO/HACCP-aligned QA systems provide that assurance, increasing customer stickiness. Premium programs and value-added services further offset buyer price pressure by bundling traceability and supply-chain guarantees. Failure to meet standards risks regulatory penalties and customer churn.

Inventory and working-capital leverage

Buyers push for just-in-time delivery and extended payment terms (commonly 30–90 days), but Scoular’s balance sheet and 220+ storage locations (2024) absorb timing gaps and liquidity strain, shifting inventory risk onto the firm. Financing and vendor-managed inventory move value capture toward Scoular, though carrying costs (~1–2% annual inventory cost) and credit risk must be priced into margins.

- JIT pressure: 30–90 days

- Network: 220+ locations (2024)

- Carrying cost: ~1–2%/yr

- VMI/financing shifts value to Scoular

Global sourcing alternatives

- Import alternatives increase outside options

- Digital marketplaces boost visibility (2024)

- Scoular: ~25 trade lanes

- End-to-end logistics cut switching benefits

Buyers wield leverage; ethanol uses ~40% of US corn; logistics stick

Buyers (feed, ethanol, pet food) hold strong leverage—U.S. ethanol uses ~40% of U.S. corn—and can switch on price, freight and service; Scoular defends via logistics, hedging and multi-year deals. Digital marketplaces (2024) and low switching costs raise transparency; JIT (30–90 days) and extended terms pressure cashflow. Scoular’s 220+ locations (2024) and ~25 trade lanes create stickiness.

| Metric | Value |

|---|---|

| Ethanol corn share | ~40% |

| Storage locations (2024) | 220+ |

| Trade lanes | ~25 |

| Payment terms | 30–90 days |

| Carrying cost | ~1–2%/yr |

Full Version Awaits

Scoular Porter's Five Forces Analysis

This Scoular Porter’s Five Forces analysis provides a concise, actionable assessment of competitive dynamics, supplier and buyer power, threat of entrants and substitutes, and industry rivalry. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted and ready for immediate download and use.