Scoular SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Scoular’s SWOT highlights strengths in integrated grain origination and logistics, exposure to commodity volatility, and opportunities in digital supply-chain services; it also flags regulatory and climate-related risks. Want the full picture with actionable strategy and financial context? Purchase the complete SWOT to get a professionally written, editable Word report plus an Excel matrix for planning and investment decisions.

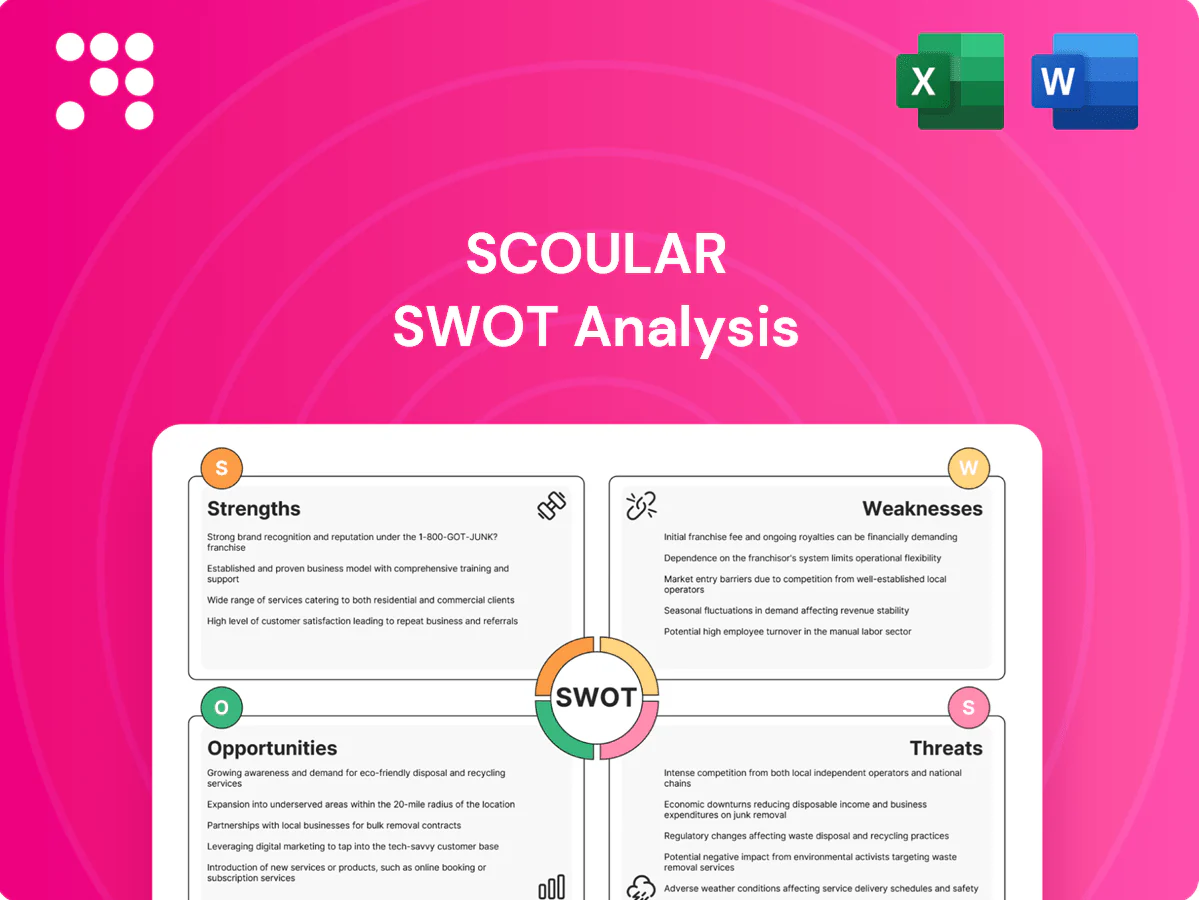

Strengths

Integrated supply chain footprint

Scoular, founded in 1892, operates end-to-end across sourcing, processing, storage and transportation, reducing handoffs and cycle times while optimizing cost and quality; integrated capacity management across grain elevators, feed ingredient facilities and processing plants supports reliable global service for producers and end-users.

Employee-owned culture

Scoular's employee-owned structure aligns incentives with long-term customer and supplier relationships and, per NCEO data (about 6,500 ESOP companies and ~14 million participants in 2023), is linked to stronger retention and accountability. In asset-heavy, low-margin grain logistics this ownership model boosts operational execution and faster decision-making focused on sustainable growth. The culture underpins continuous improvement and service reliability.

Logistics and risk management expertise

Scoular leverages 130+ years of experience to offer comprehensive logistics that smooth seasonality, regional imbalances and cross-border flows. Execution across rail, barge, truck and port coordination enhances reliability and throughput. Deep expertise in hedging and basis dynamics helps stabilize margins and customer pricing. This integrated capability differentiates Scoular in volatile commodity markets.

Diverse product and customer mix

Serving grain, feed and food ingredients gives Scoular diversified revenue and lowers segment concentration; U.S. corn production was about 13.9 billion bushels in 2024 (USDA), underpinning feed and ingredient flows. Exposure to upstream producers and downstream end-users reduces reliance on any single market and allows shifting volumes among products to maintain utilization and resilience across commodity cycles.

- Diversified revenue streams

- Balanced producer and end-user exposure

- Operational flexibility to shift volumes

- Stronger resilience through commodity cycles

Global market connectivity

Scoular's global market connectivity expands origination and demand options, linking producers and consumers across 100+ markets and enabling arbitrage for niche ingredients in regional price pockets.

International reach supports scalable traceability and quality-spec programs for emerging customers, and enhances bargaining power with carriers and suppliers, lowering logistics costs.

- 100+ markets reached

- Supports traceability and quality specs

- Enables niche-ingredient arbitrage

- Stronger carrier/supplier leverage

130+ Years of Global Grain Expertise: ESOP-Aligned Supply Chain Efficiency

Scoular (founded 1892) provides end-to-end sourcing, processing and logistics across rail, barge, truck and ports, reducing cycle times and optimizing cost. Employee-owned alignment (NCEO: ~6,500 ESOP firms; ~14M participants in 2023) supports retention and long-term customer focus. Global reach (100+ markets) and 130+ years of commodity expertise enable resiliency in volatile grain/feed cycles.

| Metric | Value |

|---|---|

| Founded | 1892 |

| Markets | 100+ |

| ESOP context | 6,500 firms; ~14M participants (2023) |

| U.S. corn 2024 | 13.9B bushels (USDA) |

What is included in the product

Provides a strategic overview of Scoular’s internal strengths and weaknesses and external opportunities and threats, highlighting competitive position, growth drivers, operational gaps, and market risks shaping its future.

Provides a concise Scoular-focused SWOT matrix for fast, visual strategy alignment and risk mitigation across supply chain and grain merchandising operations.

Weaknesses

Exposure to commodity margin compression

Grain and ingredient handling often yields thin, volatile margins, leaving Scoular exposed to commodity margin compression. Basis swings and widening freight spreads can erode profitability even when volumes remain strong. Hedging programs mitigate but do not eliminate market risk, and prolonged low volatility environments compress trading income.

High capital intensity

Scoular's grain elevators, storage, and processing assets demand continuous maintenance and safety investments, driving high fixed and variable costs. Returns hinge on throughput and utilization, so idle capacity quickly erodes margins. Large capex cycles for upgrades or expansions can strain cash flow during commodity downturns. The heavy asset footprint is less agile than asset-light logistics or brokerage models.

Operational complexity

Coordinating multi-modal logistics, quality specs, and regulatory compliance across regions increases Scoular’s operational complexity and execution risk, especially given the US agricultural export market totaled about $178 billion in FY2023 (USDA), amplifying volume and regulatory oversight.

Process variability drives losses through shrink, demurrage, and quality claims; industry demurrage exposures can reach thousands per shipment, raising cost volatility for grain handlers.

Systems integration across facilities and partners is resource intensive, requiring continuous investment in IT and compliance to avoid elevated execution and regulatory penalties.

Scale disadvantage vs. global majors

Competing with mega-players like Cargill (~165 billion annual sales 2023), ADM (~79 billion 2024) and Bunge (~60 billion 2024) limits Scoulars pricing power; these incumbents secure preferential freight, insurance and cheaper financing and invest heavily in ports, digital tools and sustainability, pressuring margins in contested corridors.

- Scale gap vs majors

- Preferential logistics/finance

- Higher tech & sustainability spend

- Margin pressure in key corridors

Concentration in agricultural cycles

Scoular's results remain tightly linked to crop yields, plantings and feed demand, so seasonal swings and agronomic outcomes drive revenue and margin variability. Weather shocks or disease outbreaks can rapidly shift volumes and commodity mixes, while concentration in grains and oilseeds raises earnings volatility and limits non‑agricultural diversification.

- Exposure: grain/oilseed handling dominant

- Risk drivers: yield, plantings, feed demand

- Shock sensitivity: weather, disease

- Limited diversification outside ag

Thin, volatile commodity margins and heavy assets raise execution and capex risk in US ag exports

Thin, volatile commodity margins and hedging limits leave Scoular exposed to prolonged low volatility and freight/basis swings. Heavy asset base raises fixed costs and capex risk, reducing agility versus asset-light peers. Complex multi-modal operations and compliance increase execution risk amid a $178B US ag export market (USDA 2023).

| Metric | Figure |

|---|---|

| US ag exports 2023 | $178B |

| Cargill revenue 2023 | $165B |

| ADM revenue 2024 | $79B |

Full Version Awaits

Scoular SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in‑depth version. You’re viewing a live excerpt of the editable file that becomes available after checkout.

Elevate Your Analysis with the Complete SWOT Report

Scoular’s SWOT highlights strengths in integrated grain origination and logistics, exposure to commodity volatility, and opportunities in digital supply-chain services; it also flags regulatory and climate-related risks. Want the full picture with actionable strategy and financial context? Purchase the complete SWOT to get a professionally written, editable Word report plus an Excel matrix for planning and investment decisions.

Strengths

Integrated supply chain footprint

Scoular, founded in 1892, operates end-to-end across sourcing, processing, storage and transportation, reducing handoffs and cycle times while optimizing cost and quality; integrated capacity management across grain elevators, feed ingredient facilities and processing plants supports reliable global service for producers and end-users.

Employee-owned culture

Scoular's employee-owned structure aligns incentives with long-term customer and supplier relationships and, per NCEO data (about 6,500 ESOP companies and ~14 million participants in 2023), is linked to stronger retention and accountability. In asset-heavy, low-margin grain logistics this ownership model boosts operational execution and faster decision-making focused on sustainable growth. The culture underpins continuous improvement and service reliability.

Logistics and risk management expertise

Scoular leverages 130+ years of experience to offer comprehensive logistics that smooth seasonality, regional imbalances and cross-border flows. Execution across rail, barge, truck and port coordination enhances reliability and throughput. Deep expertise in hedging and basis dynamics helps stabilize margins and customer pricing. This integrated capability differentiates Scoular in volatile commodity markets.

Diverse product and customer mix

Serving grain, feed and food ingredients gives Scoular diversified revenue and lowers segment concentration; U.S. corn production was about 13.9 billion bushels in 2024 (USDA), underpinning feed and ingredient flows. Exposure to upstream producers and downstream end-users reduces reliance on any single market and allows shifting volumes among products to maintain utilization and resilience across commodity cycles.

- Diversified revenue streams

- Balanced producer and end-user exposure

- Operational flexibility to shift volumes

- Stronger resilience through commodity cycles

Global market connectivity

Scoular's global market connectivity expands origination and demand options, linking producers and consumers across 100+ markets and enabling arbitrage for niche ingredients in regional price pockets.

International reach supports scalable traceability and quality-spec programs for emerging customers, and enhances bargaining power with carriers and suppliers, lowering logistics costs.

- 100+ markets reached

- Supports traceability and quality specs

- Enables niche-ingredient arbitrage

- Stronger carrier/supplier leverage

130+ Years of Global Grain Expertise: ESOP-Aligned Supply Chain Efficiency

Scoular (founded 1892) provides end-to-end sourcing, processing and logistics across rail, barge, truck and ports, reducing cycle times and optimizing cost. Employee-owned alignment (NCEO: ~6,500 ESOP firms; ~14M participants in 2023) supports retention and long-term customer focus. Global reach (100+ markets) and 130+ years of commodity expertise enable resiliency in volatile grain/feed cycles.

| Metric | Value |

|---|---|

| Founded | 1892 |

| Markets | 100+ |

| ESOP context | 6,500 firms; ~14M participants (2023) |

| U.S. corn 2024 | 13.9B bushels (USDA) |

What is included in the product

Provides a strategic overview of Scoular’s internal strengths and weaknesses and external opportunities and threats, highlighting competitive position, growth drivers, operational gaps, and market risks shaping its future.

Provides a concise Scoular-focused SWOT matrix for fast, visual strategy alignment and risk mitigation across supply chain and grain merchandising operations.

Weaknesses

Exposure to commodity margin compression

Grain and ingredient handling often yields thin, volatile margins, leaving Scoular exposed to commodity margin compression. Basis swings and widening freight spreads can erode profitability even when volumes remain strong. Hedging programs mitigate but do not eliminate market risk, and prolonged low volatility environments compress trading income.

High capital intensity

Scoular's grain elevators, storage, and processing assets demand continuous maintenance and safety investments, driving high fixed and variable costs. Returns hinge on throughput and utilization, so idle capacity quickly erodes margins. Large capex cycles for upgrades or expansions can strain cash flow during commodity downturns. The heavy asset footprint is less agile than asset-light logistics or brokerage models.

Operational complexity

Coordinating multi-modal logistics, quality specs, and regulatory compliance across regions increases Scoular’s operational complexity and execution risk, especially given the US agricultural export market totaled about $178 billion in FY2023 (USDA), amplifying volume and regulatory oversight.

Process variability drives losses through shrink, demurrage, and quality claims; industry demurrage exposures can reach thousands per shipment, raising cost volatility for grain handlers.

Systems integration across facilities and partners is resource intensive, requiring continuous investment in IT and compliance to avoid elevated execution and regulatory penalties.

Scale disadvantage vs. global majors

Competing with mega-players like Cargill (~165 billion annual sales 2023), ADM (~79 billion 2024) and Bunge (~60 billion 2024) limits Scoulars pricing power; these incumbents secure preferential freight, insurance and cheaper financing and invest heavily in ports, digital tools and sustainability, pressuring margins in contested corridors.

- Scale gap vs majors

- Preferential logistics/finance

- Higher tech & sustainability spend

- Margin pressure in key corridors

Concentration in agricultural cycles

Scoular's results remain tightly linked to crop yields, plantings and feed demand, so seasonal swings and agronomic outcomes drive revenue and margin variability. Weather shocks or disease outbreaks can rapidly shift volumes and commodity mixes, while concentration in grains and oilseeds raises earnings volatility and limits non‑agricultural diversification.

- Exposure: grain/oilseed handling dominant

- Risk drivers: yield, plantings, feed demand

- Shock sensitivity: weather, disease

- Limited diversification outside ag

Thin, volatile commodity margins and heavy assets raise execution and capex risk in US ag exports

Thin, volatile commodity margins and hedging limits leave Scoular exposed to prolonged low volatility and freight/basis swings. Heavy asset base raises fixed costs and capex risk, reducing agility versus asset-light peers. Complex multi-modal operations and compliance increase execution risk amid a $178B US ag export market (USDA 2023).

| Metric | Figure |

|---|---|

| US ag exports 2023 | $178B |

| Cargill revenue 2023 | $165B |

| ADM revenue 2024 | $79B |

Full Version Awaits

Scoular SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in‑depth version. You’re viewing a live excerpt of the editable file that becomes available after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

Scoular’s SWOT highlights strengths in integrated grain origination and logistics, exposure to commodity volatility, and opportunities in digital supply-chain services; it also flags regulatory and climate-related risks. Want the full picture with actionable strategy and financial context? Purchase the complete SWOT to get a professionally written, editable Word report plus an Excel matrix for planning and investment decisions.

Strengths

Integrated supply chain footprint

Scoular, founded in 1892, operates end-to-end across sourcing, processing, storage and transportation, reducing handoffs and cycle times while optimizing cost and quality; integrated capacity management across grain elevators, feed ingredient facilities and processing plants supports reliable global service for producers and end-users.

Employee-owned culture

Scoular's employee-owned structure aligns incentives with long-term customer and supplier relationships and, per NCEO data (about 6,500 ESOP companies and ~14 million participants in 2023), is linked to stronger retention and accountability. In asset-heavy, low-margin grain logistics this ownership model boosts operational execution and faster decision-making focused on sustainable growth. The culture underpins continuous improvement and service reliability.

Logistics and risk management expertise

Scoular leverages 130+ years of experience to offer comprehensive logistics that smooth seasonality, regional imbalances and cross-border flows. Execution across rail, barge, truck and port coordination enhances reliability and throughput. Deep expertise in hedging and basis dynamics helps stabilize margins and customer pricing. This integrated capability differentiates Scoular in volatile commodity markets.

Diverse product and customer mix

Serving grain, feed and food ingredients gives Scoular diversified revenue and lowers segment concentration; U.S. corn production was about 13.9 billion bushels in 2024 (USDA), underpinning feed and ingredient flows. Exposure to upstream producers and downstream end-users reduces reliance on any single market and allows shifting volumes among products to maintain utilization and resilience across commodity cycles.

- Diversified revenue streams

- Balanced producer and end-user exposure

- Operational flexibility to shift volumes

- Stronger resilience through commodity cycles

Global market connectivity

Scoular's global market connectivity expands origination and demand options, linking producers and consumers across 100+ markets and enabling arbitrage for niche ingredients in regional price pockets.

International reach supports scalable traceability and quality-spec programs for emerging customers, and enhances bargaining power with carriers and suppliers, lowering logistics costs.

- 100+ markets reached

- Supports traceability and quality specs

- Enables niche-ingredient arbitrage

- Stronger carrier/supplier leverage

130+ Years of Global Grain Expertise: ESOP-Aligned Supply Chain Efficiency

Scoular (founded 1892) provides end-to-end sourcing, processing and logistics across rail, barge, truck and ports, reducing cycle times and optimizing cost. Employee-owned alignment (NCEO: ~6,500 ESOP firms; ~14M participants in 2023) supports retention and long-term customer focus. Global reach (100+ markets) and 130+ years of commodity expertise enable resiliency in volatile grain/feed cycles.

| Metric | Value |

|---|---|

| Founded | 1892 |

| Markets | 100+ |

| ESOP context | 6,500 firms; ~14M participants (2023) |

| U.S. corn 2024 | 13.9B bushels (USDA) |

What is included in the product

Provides a strategic overview of Scoular’s internal strengths and weaknesses and external opportunities and threats, highlighting competitive position, growth drivers, operational gaps, and market risks shaping its future.

Provides a concise Scoular-focused SWOT matrix for fast, visual strategy alignment and risk mitigation across supply chain and grain merchandising operations.

Weaknesses

Exposure to commodity margin compression

Grain and ingredient handling often yields thin, volatile margins, leaving Scoular exposed to commodity margin compression. Basis swings and widening freight spreads can erode profitability even when volumes remain strong. Hedging programs mitigate but do not eliminate market risk, and prolonged low volatility environments compress trading income.

High capital intensity

Scoular's grain elevators, storage, and processing assets demand continuous maintenance and safety investments, driving high fixed and variable costs. Returns hinge on throughput and utilization, so idle capacity quickly erodes margins. Large capex cycles for upgrades or expansions can strain cash flow during commodity downturns. The heavy asset footprint is less agile than asset-light logistics or brokerage models.

Operational complexity

Coordinating multi-modal logistics, quality specs, and regulatory compliance across regions increases Scoular’s operational complexity and execution risk, especially given the US agricultural export market totaled about $178 billion in FY2023 (USDA), amplifying volume and regulatory oversight.

Process variability drives losses through shrink, demurrage, and quality claims; industry demurrage exposures can reach thousands per shipment, raising cost volatility for grain handlers.

Systems integration across facilities and partners is resource intensive, requiring continuous investment in IT and compliance to avoid elevated execution and regulatory penalties.

Scale disadvantage vs. global majors

Competing with mega-players like Cargill (~165 billion annual sales 2023), ADM (~79 billion 2024) and Bunge (~60 billion 2024) limits Scoulars pricing power; these incumbents secure preferential freight, insurance and cheaper financing and invest heavily in ports, digital tools and sustainability, pressuring margins in contested corridors.

- Scale gap vs majors

- Preferential logistics/finance

- Higher tech & sustainability spend

- Margin pressure in key corridors

Concentration in agricultural cycles

Scoular's results remain tightly linked to crop yields, plantings and feed demand, so seasonal swings and agronomic outcomes drive revenue and margin variability. Weather shocks or disease outbreaks can rapidly shift volumes and commodity mixes, while concentration in grains and oilseeds raises earnings volatility and limits non‑agricultural diversification.

- Exposure: grain/oilseed handling dominant

- Risk drivers: yield, plantings, feed demand

- Shock sensitivity: weather, disease

- Limited diversification outside ag

Thin, volatile commodity margins and heavy assets raise execution and capex risk in US ag exports

Thin, volatile commodity margins and hedging limits leave Scoular exposed to prolonged low volatility and freight/basis swings. Heavy asset base raises fixed costs and capex risk, reducing agility versus asset-light peers. Complex multi-modal operations and compliance increase execution risk amid a $178B US ag export market (USDA 2023).

| Metric | Figure |

|---|---|

| US ag exports 2023 | $178B |

| Cargill revenue 2023 | $165B |

| ADM revenue 2024 | $79B |

Full Version Awaits

Scoular SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in‑depth version. You’re viewing a live excerpt of the editable file that becomes available after checkout.