Scout24 Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

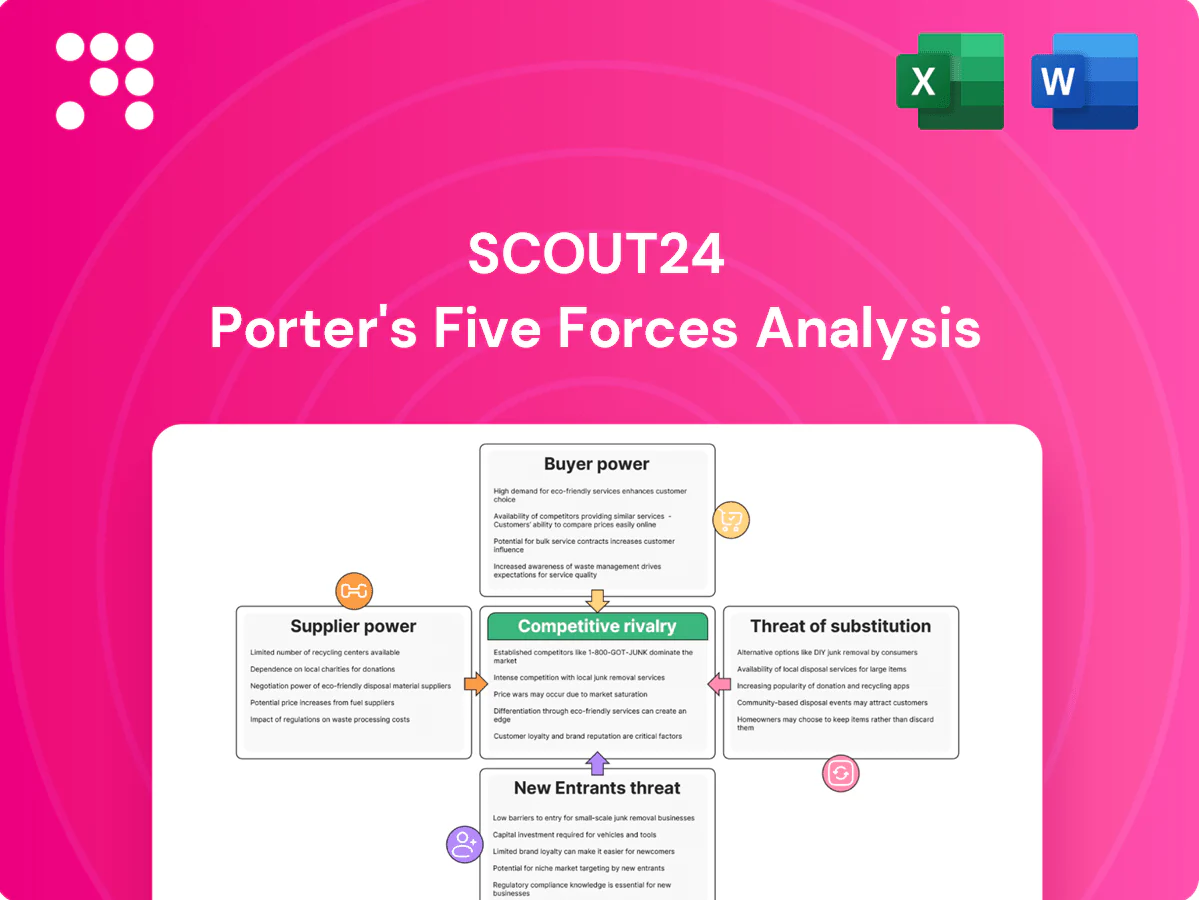

Scout24 faces moderate buyer power and rising competition from vertical platforms, while supplier leverage is limited and new entrants are impeded by strong network effects and brand recognition. This snapshot highlights key pressures but omits granular, force-by-force ratings. Unlock the full Porter's Five Forces Analysis to see visuals, data, and strategic implications for Scout24.

Suppliers Bargaining Power

Inventory from agents and landlords

Agents, landlords and developers supply the listings that drive Scout24’s value; large broker networks can extract favorable terms or premium placement given volume. Scout24 reported roughly 40 million monthly visits in 2024, making the platform hard for suppliers to ignore. Multi-homing by listers (using competing portals) reduces but does not remove supplier leverage.

Cloud and infrastructure dependence

Reliance on major cloud providers and CDNs concentrates supplier power—AWS (≈32%), Microsoft Azure (≈23%) and Google Cloud (≈11%) dominated the 2024 market—so pricing moves or incidents can materially affect uptime and margins. Switching providers is feasible but operationally complex and can take months with significant migration costs. Vendor price changes or service incidents could compress margins; long‑term contracts and multi‑cloud strategies reduce that risk.

App stores and mobile ecosystems

Distribution via Apple App Store and Google Play exposes Scout24 to platform fees (tiered 15–30% rates in 2024), policy control and algorithmic visibility; ATT and privacy-driven attribution shifts since 2021 have already altered user-acquisition economics. Featured placement and ratings materially drive download velocity and engagement. Web channels offset some costs, but mobile (>50% of global web traffic in 2024) remains critical for reach.

Data, mapping, and verification services

Third-party data (maps, geocoding, valuations, fraud checks) underpins listing quality and user trust; a small set of premium vendors hold outsized influence, making supplier pricing power material while in-house replication entails high engineering and data costs.

- Concentration risk: few high-quality providers

- High build/maintain cost for in-house

- Negotiate volume tiers to cut unit price

- Diversify vendors to reduce exposure

Marketing and lead-generation partners

Marketing and lead-generation partners—performance platforms and affiliate networks—directly influence Scout24s traffic acquisition costs; industry data in 2024 showed auction-driven CPAs can spike 20–40% during peak periods. Dependency is moderated by a strong share of direct and organic visits, while continuous funnel optimization and brand investment reduce suppliers’ pricing power.

- 2024 CPA spikes: 20–40%

- Mitigation: high direct/organic share

- Countermeasures: optimization + brand spend

High traffic platform limits partner leverage; cloud concentration and app fees raise supplier risk

Agents, landlords and developer networks hold moderate leverage but Scout24’s ~40M monthly visits (2024) and high listing volume limit extraction. Cloud/CDN concentration (AWS≈32%, Azure≈23%, GCP≈11% 2024) and app-store fees (15–30%) raise supplier risk; multi‑cloud and direct channels mitigate it.

| Metric | 2024 |

|---|---|

| Monthly visits | 40M |

| Cloud share (AWS/Azure/GCP) | 32/23/11% |

| App fees | 15–30% |

| CPA spikes | 20–40% |

What is included in the product

Uncovers key drivers of competition, customer influence, market entry risks, and substitutes for Scout24; evaluates supplier and buyer power, rivalry intensity, and barriers protecting incumbents, with strategic commentary and editable Word format for use in investor materials and strategy decks.

A concise Porter's Five Forces snapshot for Scout24—streamlines competitive analysis and accelerates strategic decision-making. Editable pressure levels and an instant radar view let you compare scenarios, export clean visuals for decks, and update assumptions without complex tools.

Customers Bargaining Power

Large agencies and developers

High-volume agencies and developers command strong bargaining power—repeat spend and inventory control in Berlin, Munich and Hamburg let them negotiate rates, premium placement and bespoke volume discounts; Scout24 offsets this with ROI analytics and a unique audience reach of about 13–15 million monthly users in 2024, preserving ad pricing power and platform liquidity.

Multi-homing across portals

Listers commonly post across ImmoWelt/Immonet and eBay Kleinanzeigen to maximize leads, lowering switching costs and increasing price sensitivity; ImmoScout24 held roughly 60% of German online property search share (2024) while eBay Kleinanzeigen reported about 34 million monthly users (2023). Differentiated tools and verified-lead products let Scout24 justify premium pricing and reduce churn. Exclusive-inventory initiatives and advertiser partnerships can curb multi-homing and defend margins.

Price transparency and ROI tracking

Advertisers on Scout24 closely monitor cost-per-lead and time-to-let/sell, and clear attribution makes any platform price increases immediately visible and contested. Packaged value-adds like premium placement and market-data insights can soften resistance by tying spend to measurable outcomes. Tiered offerings that align fees with lead quality and conversion rates help retain customers by matching cost to ROI expectations.

Consumer expectations and experience

End-users are price-insensitive but wield power through engagement and churn: poor UX, spam, or low-quality listings rapidly divert traffic to alternatives, eroding platform monetization.

Trust features, verified listings, and accurate inventory are key to sustaining loyalty and reducing switching; high consumer share strengthens Scout24’s negotiating position versus advertisers.

- Engagement-driven leverage

- UX and trust preserve retention

- Large consumer share lowers advertiser bargaining power

Macro cycles and budget pressure

In downturns listers cut marketing spend or shift to cheaper channels, increasing price sensitivity for listing fees; Immobilienscout24 reported c.13 million monthly visits in 2024, amplifying competition for fewer paid listings.

Counter-cyclical products like rentals and landlord tools stabilized ARPU in 2024, while flexible contracts and outcome-based pricing reduced churn and retained clients.

- Macro pressure: higher fee sensitivity in 2024

- Traffic: ~13 million monthly visits (2024)

- Stabilizers: rentals/landlord tools bolster ARPU

- Retention: flexible/outcome pricing lowers churn

Market leader momentum: 13–15m monthly users and ~60% share sustain pricing power

High-volume agents exert strong bargaining power via repeat spend and inventory control, but Scout24's ~13–15m monthly users (2024) and ~60% German market share (ImmoScout24, 2024) preserve pricing power. Multi-homing with ImmoWelt/eBay Kleinanzeigen raises price sensitivity; clear attribution and verified-lead products help retain advertisers. Rentals and landlord tools stabilized ARPU in 2024, reducing churn.

| Metric | Value |

|---|---|

| Monthly users (ImmoScout24) | 13–15m (2024) |

| German market share | ~60% (2024) |

| eBay Kleinanzeigen users | 34m (2023) |

Same Document Delivered

Scout24 Porter's Five Forces Analysis

This Scout24 Porter’s Five Forces analysis delivers a concise, professional assessment of competitive rivalry, buyer and supplier power, substitutes, and barriers to entry, with actionable implications for strategy and valuation. It highlights key risks, opportunities, and their likely impact on margins and growth prospects. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use.

A Must-Have Tool for Decision-Makers

Scout24 faces moderate buyer power and rising competition from vertical platforms, while supplier leverage is limited and new entrants are impeded by strong network effects and brand recognition. This snapshot highlights key pressures but omits granular, force-by-force ratings. Unlock the full Porter's Five Forces Analysis to see visuals, data, and strategic implications for Scout24.

Suppliers Bargaining Power

Inventory from agents and landlords

Agents, landlords and developers supply the listings that drive Scout24’s value; large broker networks can extract favorable terms or premium placement given volume. Scout24 reported roughly 40 million monthly visits in 2024, making the platform hard for suppliers to ignore. Multi-homing by listers (using competing portals) reduces but does not remove supplier leverage.

Cloud and infrastructure dependence

Reliance on major cloud providers and CDNs concentrates supplier power—AWS (≈32%), Microsoft Azure (≈23%) and Google Cloud (≈11%) dominated the 2024 market—so pricing moves or incidents can materially affect uptime and margins. Switching providers is feasible but operationally complex and can take months with significant migration costs. Vendor price changes or service incidents could compress margins; long‑term contracts and multi‑cloud strategies reduce that risk.

App stores and mobile ecosystems

Distribution via Apple App Store and Google Play exposes Scout24 to platform fees (tiered 15–30% rates in 2024), policy control and algorithmic visibility; ATT and privacy-driven attribution shifts since 2021 have already altered user-acquisition economics. Featured placement and ratings materially drive download velocity and engagement. Web channels offset some costs, but mobile (>50% of global web traffic in 2024) remains critical for reach.

Data, mapping, and verification services

Third-party data (maps, geocoding, valuations, fraud checks) underpins listing quality and user trust; a small set of premium vendors hold outsized influence, making supplier pricing power material while in-house replication entails high engineering and data costs.

- Concentration risk: few high-quality providers

- High build/maintain cost for in-house

- Negotiate volume tiers to cut unit price

- Diversify vendors to reduce exposure

Marketing and lead-generation partners

Marketing and lead-generation partners—performance platforms and affiliate networks—directly influence Scout24s traffic acquisition costs; industry data in 2024 showed auction-driven CPAs can spike 20–40% during peak periods. Dependency is moderated by a strong share of direct and organic visits, while continuous funnel optimization and brand investment reduce suppliers’ pricing power.

- 2024 CPA spikes: 20–40%

- Mitigation: high direct/organic share

- Countermeasures: optimization + brand spend

High traffic platform limits partner leverage; cloud concentration and app fees raise supplier risk

Agents, landlords and developer networks hold moderate leverage but Scout24’s ~40M monthly visits (2024) and high listing volume limit extraction. Cloud/CDN concentration (AWS≈32%, Azure≈23%, GCP≈11% 2024) and app-store fees (15–30%) raise supplier risk; multi‑cloud and direct channels mitigate it.

| Metric | 2024 |

|---|---|

| Monthly visits | 40M |

| Cloud share (AWS/Azure/GCP) | 32/23/11% |

| App fees | 15–30% |

| CPA spikes | 20–40% |

What is included in the product

Uncovers key drivers of competition, customer influence, market entry risks, and substitutes for Scout24; evaluates supplier and buyer power, rivalry intensity, and barriers protecting incumbents, with strategic commentary and editable Word format for use in investor materials and strategy decks.

A concise Porter's Five Forces snapshot for Scout24—streamlines competitive analysis and accelerates strategic decision-making. Editable pressure levels and an instant radar view let you compare scenarios, export clean visuals for decks, and update assumptions without complex tools.

Customers Bargaining Power

Large agencies and developers

High-volume agencies and developers command strong bargaining power—repeat spend and inventory control in Berlin, Munich and Hamburg let them negotiate rates, premium placement and bespoke volume discounts; Scout24 offsets this with ROI analytics and a unique audience reach of about 13–15 million monthly users in 2024, preserving ad pricing power and platform liquidity.

Multi-homing across portals

Listers commonly post across ImmoWelt/Immonet and eBay Kleinanzeigen to maximize leads, lowering switching costs and increasing price sensitivity; ImmoScout24 held roughly 60% of German online property search share (2024) while eBay Kleinanzeigen reported about 34 million monthly users (2023). Differentiated tools and verified-lead products let Scout24 justify premium pricing and reduce churn. Exclusive-inventory initiatives and advertiser partnerships can curb multi-homing and defend margins.

Price transparency and ROI tracking

Advertisers on Scout24 closely monitor cost-per-lead and time-to-let/sell, and clear attribution makes any platform price increases immediately visible and contested. Packaged value-adds like premium placement and market-data insights can soften resistance by tying spend to measurable outcomes. Tiered offerings that align fees with lead quality and conversion rates help retain customers by matching cost to ROI expectations.

Consumer expectations and experience

End-users are price-insensitive but wield power through engagement and churn: poor UX, spam, or low-quality listings rapidly divert traffic to alternatives, eroding platform monetization.

Trust features, verified listings, and accurate inventory are key to sustaining loyalty and reducing switching; high consumer share strengthens Scout24’s negotiating position versus advertisers.

- Engagement-driven leverage

- UX and trust preserve retention

- Large consumer share lowers advertiser bargaining power

Macro cycles and budget pressure

In downturns listers cut marketing spend or shift to cheaper channels, increasing price sensitivity for listing fees; Immobilienscout24 reported c.13 million monthly visits in 2024, amplifying competition for fewer paid listings.

Counter-cyclical products like rentals and landlord tools stabilized ARPU in 2024, while flexible contracts and outcome-based pricing reduced churn and retained clients.

- Macro pressure: higher fee sensitivity in 2024

- Traffic: ~13 million monthly visits (2024)

- Stabilizers: rentals/landlord tools bolster ARPU

- Retention: flexible/outcome pricing lowers churn

Market leader momentum: 13–15m monthly users and ~60% share sustain pricing power

High-volume agents exert strong bargaining power via repeat spend and inventory control, but Scout24's ~13–15m monthly users (2024) and ~60% German market share (ImmoScout24, 2024) preserve pricing power. Multi-homing with ImmoWelt/eBay Kleinanzeigen raises price sensitivity; clear attribution and verified-lead products help retain advertisers. Rentals and landlord tools stabilized ARPU in 2024, reducing churn.

| Metric | Value |

|---|---|

| Monthly users (ImmoScout24) | 13–15m (2024) |

| German market share | ~60% (2024) |

| eBay Kleinanzeigen users | 34m (2023) |

Same Document Delivered

Scout24 Porter's Five Forces Analysis

This Scout24 Porter’s Five Forces analysis delivers a concise, professional assessment of competitive rivalry, buyer and supplier power, substitutes, and barriers to entry, with actionable implications for strategy and valuation. It highlights key risks, opportunities, and their likely impact on margins and growth prospects. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Scout24 faces moderate buyer power and rising competition from vertical platforms, while supplier leverage is limited and new entrants are impeded by strong network effects and brand recognition. This snapshot highlights key pressures but omits granular, force-by-force ratings. Unlock the full Porter's Five Forces Analysis to see visuals, data, and strategic implications for Scout24.

Suppliers Bargaining Power

Inventory from agents and landlords

Agents, landlords and developers supply the listings that drive Scout24’s value; large broker networks can extract favorable terms or premium placement given volume. Scout24 reported roughly 40 million monthly visits in 2024, making the platform hard for suppliers to ignore. Multi-homing by listers (using competing portals) reduces but does not remove supplier leverage.

Cloud and infrastructure dependence

Reliance on major cloud providers and CDNs concentrates supplier power—AWS (≈32%), Microsoft Azure (≈23%) and Google Cloud (≈11%) dominated the 2024 market—so pricing moves or incidents can materially affect uptime and margins. Switching providers is feasible but operationally complex and can take months with significant migration costs. Vendor price changes or service incidents could compress margins; long‑term contracts and multi‑cloud strategies reduce that risk.

App stores and mobile ecosystems

Distribution via Apple App Store and Google Play exposes Scout24 to platform fees (tiered 15–30% rates in 2024), policy control and algorithmic visibility; ATT and privacy-driven attribution shifts since 2021 have already altered user-acquisition economics. Featured placement and ratings materially drive download velocity and engagement. Web channels offset some costs, but mobile (>50% of global web traffic in 2024) remains critical for reach.

Data, mapping, and verification services

Third-party data (maps, geocoding, valuations, fraud checks) underpins listing quality and user trust; a small set of premium vendors hold outsized influence, making supplier pricing power material while in-house replication entails high engineering and data costs.

- Concentration risk: few high-quality providers

- High build/maintain cost for in-house

- Negotiate volume tiers to cut unit price

- Diversify vendors to reduce exposure

Marketing and lead-generation partners

Marketing and lead-generation partners—performance platforms and affiliate networks—directly influence Scout24s traffic acquisition costs; industry data in 2024 showed auction-driven CPAs can spike 20–40% during peak periods. Dependency is moderated by a strong share of direct and organic visits, while continuous funnel optimization and brand investment reduce suppliers’ pricing power.

- 2024 CPA spikes: 20–40%

- Mitigation: high direct/organic share

- Countermeasures: optimization + brand spend

High traffic platform limits partner leverage; cloud concentration and app fees raise supplier risk

Agents, landlords and developer networks hold moderate leverage but Scout24’s ~40M monthly visits (2024) and high listing volume limit extraction. Cloud/CDN concentration (AWS≈32%, Azure≈23%, GCP≈11% 2024) and app-store fees (15–30%) raise supplier risk; multi‑cloud and direct channels mitigate it.

| Metric | 2024 |

|---|---|

| Monthly visits | 40M |

| Cloud share (AWS/Azure/GCP) | 32/23/11% |

| App fees | 15–30% |

| CPA spikes | 20–40% |

What is included in the product

Uncovers key drivers of competition, customer influence, market entry risks, and substitutes for Scout24; evaluates supplier and buyer power, rivalry intensity, and barriers protecting incumbents, with strategic commentary and editable Word format for use in investor materials and strategy decks.

A concise Porter's Five Forces snapshot for Scout24—streamlines competitive analysis and accelerates strategic decision-making. Editable pressure levels and an instant radar view let you compare scenarios, export clean visuals for decks, and update assumptions without complex tools.

Customers Bargaining Power

Large agencies and developers

High-volume agencies and developers command strong bargaining power—repeat spend and inventory control in Berlin, Munich and Hamburg let them negotiate rates, premium placement and bespoke volume discounts; Scout24 offsets this with ROI analytics and a unique audience reach of about 13–15 million monthly users in 2024, preserving ad pricing power and platform liquidity.

Multi-homing across portals

Listers commonly post across ImmoWelt/Immonet and eBay Kleinanzeigen to maximize leads, lowering switching costs and increasing price sensitivity; ImmoScout24 held roughly 60% of German online property search share (2024) while eBay Kleinanzeigen reported about 34 million monthly users (2023). Differentiated tools and verified-lead products let Scout24 justify premium pricing and reduce churn. Exclusive-inventory initiatives and advertiser partnerships can curb multi-homing and defend margins.

Price transparency and ROI tracking

Advertisers on Scout24 closely monitor cost-per-lead and time-to-let/sell, and clear attribution makes any platform price increases immediately visible and contested. Packaged value-adds like premium placement and market-data insights can soften resistance by tying spend to measurable outcomes. Tiered offerings that align fees with lead quality and conversion rates help retain customers by matching cost to ROI expectations.

Consumer expectations and experience

End-users are price-insensitive but wield power through engagement and churn: poor UX, spam, or low-quality listings rapidly divert traffic to alternatives, eroding platform monetization.

Trust features, verified listings, and accurate inventory are key to sustaining loyalty and reducing switching; high consumer share strengthens Scout24’s negotiating position versus advertisers.

- Engagement-driven leverage

- UX and trust preserve retention

- Large consumer share lowers advertiser bargaining power

Macro cycles and budget pressure

In downturns listers cut marketing spend or shift to cheaper channels, increasing price sensitivity for listing fees; Immobilienscout24 reported c.13 million monthly visits in 2024, amplifying competition for fewer paid listings.

Counter-cyclical products like rentals and landlord tools stabilized ARPU in 2024, while flexible contracts and outcome-based pricing reduced churn and retained clients.

- Macro pressure: higher fee sensitivity in 2024

- Traffic: ~13 million monthly visits (2024)

- Stabilizers: rentals/landlord tools bolster ARPU

- Retention: flexible/outcome pricing lowers churn

Market leader momentum: 13–15m monthly users and ~60% share sustain pricing power

High-volume agents exert strong bargaining power via repeat spend and inventory control, but Scout24's ~13–15m monthly users (2024) and ~60% German market share (ImmoScout24, 2024) preserve pricing power. Multi-homing with ImmoWelt/eBay Kleinanzeigen raises price sensitivity; clear attribution and verified-lead products help retain advertisers. Rentals and landlord tools stabilized ARPU in 2024, reducing churn.

| Metric | Value |

|---|---|

| Monthly users (ImmoScout24) | 13–15m (2024) |

| German market share | ~60% (2024) |

| eBay Kleinanzeigen users | 34m (2023) |

Same Document Delivered

Scout24 Porter's Five Forces Analysis

This Scout24 Porter’s Five Forces analysis delivers a concise, professional assessment of competitive rivalry, buyer and supplier power, substitutes, and barriers to entry, with actionable implications for strategy and valuation. It highlights key risks, opportunities, and their likely impact on margins and growth prospects. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use.