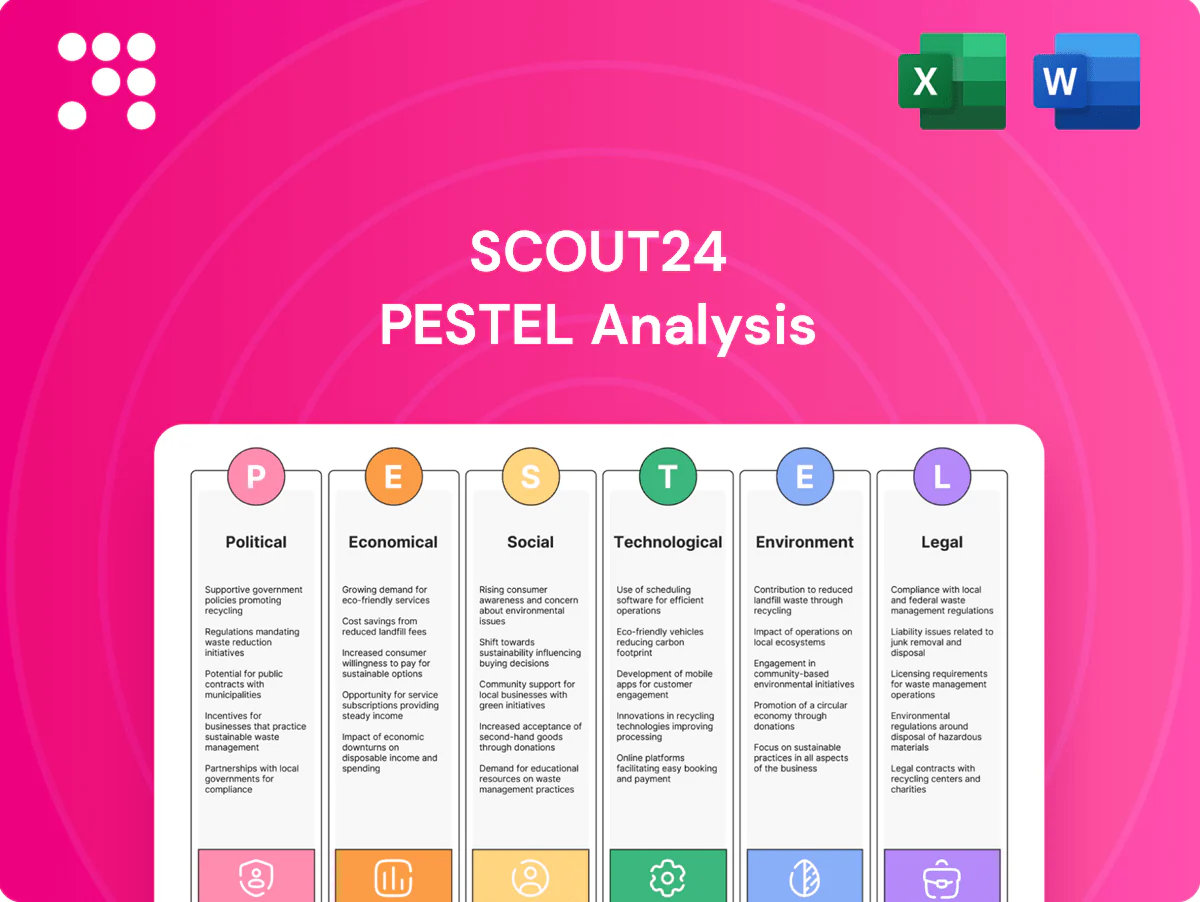

Scout24 PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic advantage with our focused PESTLE Analysis of Scout24—three concise insights into political, economic, and technological forces shaping its market position. Ideal for investors and strategists seeking actionable intelligence. Buy the full report to access the complete, editable deep-dive and make confident decisions.

Political factors

German housing policy shifts

Changes to rent caps and Mietspiegel rules and incentives for affordable housing—against the federal goal of 400,000 new homes/year—directly affect listing supply and landlord activity. Coalition priorities at federal and Länder levels can tighten or relax market dynamics, since Länder control local Mietspiegel implementation. Scout24 must monitor policy cycles to adjust pricing, products and communications. Regional variations across Länder require localized go-to-market strategies.

Urban planning and zoning

Zoning approvals and Germanys densification target of 400,000 new homes per year drive developer marketing spend and new-supply volumes, while building permits (~270,000 permits in 2023 per Destatis) directly constrain pipeline and listings. Delays or planning reforms shift demand onto existing stock, altering listing composition and price dynamics. Partnerships with municipalities to provide data-driven planning tools reinforce Scout24s role as a market-intelligence partner.

EU digital platform oversight

EU and German momentum for stricter platform governance (DMA effective 2023; 22 gatekeepers designated) raises compliance expectations, with DMA fines up to 10% and DSA fines up to 6% of global turnover. Political scrutiny of marketplace fairness can force changes to ranking, ad labeling and access rules. Proactive stakeholder engagement reduces regulatory friction and helps shape pragmatic standards for real estate portals.

Public housing and subsidies

Scout24 can integrate subsidy workflows and eligibility filters into listings and lead flows to improve matching and conversion; the EU Renovation Wave aims to double renovation rates by 2030, creating landlord incentives for energy-efficient upgrades.

- Align listings with subsidy eligibility filters

- Target landlord tools for energy-efficiency upgrades

- Monitor budget shifts to predict rental vs purchase demand

Geopolitical and migration dynamics

Migration inflows and humanitarian policies concentrate demand in major cities and tighten rentals; UNHCR reported 108.4 million displaced worldwide end-2023 and Eurostat recorded 828,000 first-time asylum applicants in EU+EFTA in 2023. Political responses shape temporary housing, integration programs and regional allocation, altering local supply. Scout24 can add filters for short-term, furnished and shared options to capture these policy-driven segments.

- Short-term rentals

- Furnished listings

- Shared/accommodation

- Regional allocation tracking

Listings squeezed: target 400,000/yr vs permits ~270k

Policy on rent caps, Mietspiegel and Germanys 400,000 homes/year target (federal) alters listing supply and landlord incentives; 2023 building permits ~270,000 (Destatis) constrain new listings. DMA/DSA governance (DMA effective 2023; fines up to 10%/6% turnover) increases platform compliance costs. Subsidies and Renovation Wave (double renovations by 2030) shift demand toward energy-efficient upgrades; homeownership ~46% (Eurostat).

| Metric | Value |

|---|---|

| Homes target | 400,000/yr |

| Building permits 2023 | ~270,000 |

| Homeownership | ~46% |

| Displaced (end‑2023) | 108.4M (UNHCR) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Scout24, combining data-driven trends and region-specific regulatory context to identify strategic risks and opportunities for executives, investors, and consultants with forward-looking insights ready for reports and pitch decks.

Concise, visually segmented Scout24 PESTLE summary for quick reference in meetings or presentations, easily editable for regional or business-specific notes and shareable across teams to support risk and strategy discussions.

Economic factors

Interest rate and mortgage cycles

ECB rate moves (deposit rate ~4.00% in 2024–25) directly affect mortgage affordability and German transaction volumes, which fell about 15% at peak rates while lower rates later revived buyer traffic and listings. Higher rates have shifted demand toward renting. Scout24’s revenue mix should balance listing products with value-added services; flexible pricing and ancillary services can buffer cyclical swings.

Construction slowdown and supply gaps

Cost inflation and rising builder insolvencies are constraining new supply, keeping vacancy in major German cities below 2% and sustaining tight rental markets. Lower completions keep demand concentrated on existing stock, supporting higher listing engagement on Scout24 platforms. Developers are reallocating budgets toward more efficient digital marketing; Scout24 can capture this by offering performance-based packages tied to leads and conversions.

Advertising and agent budgets

Broker and landlord ad spend closely tracks transaction volumes and time-to-let/sell, so downturns see budgets shift to highest-ROI channels, favoring category leaders like major portals. Clear attribution and lead-quality metrics underpin pricing power by proving superior conversion and lower cost-per-lease. Vendors offset softer volumes by upselling analytics and premium listing tools tied to measurable outcomes.

Household income and inflation

Real wages in Germany fell about 1.8% in 2023, tightening household affordability and shifting search filters toward lower-price tiers; with inflation around 3.4% in 2024, time-on-market shortens for budget listings while premium listings see weaker conversion. Tenants trade down to smaller units and suburban locations; Scout24 must price premium placements to deliver clear ROI and offer flexible bundles to retain advertisers.

- real-wage decline presses affordability

- inflation → demand for smaller, peripheral units

- premium pricing must match ROI; flexible bundles aid retention

Liquidity and investor sentiment

Institutional appetite for residential assets rose to roughly 25% of German transaction volumes by 2023, increasing portfolio churn and professional listings as investors seek scale; yield expectations around 3–5% versus financing costs elevated by policy rates near 4% in 2024–25 compress deal flow and slow pacing. Scout24 can monetise this by selling pricing, comps and absorption analytics to investors and brokers, diversifying revenue beyond pure listings.

- institutional-share: ~25% (Germany, 2023)

- policy-rate: ~4% (2024–25)

- product-opportunity: pricing, comps, absorption data

Listings squeezed: target 400,000/yr vs permits ~270k

ECB deposit rate ~4.0% (2024–25) tightened mortgage affordability, German transaction volumes fell ~15% at peak rates before partial recovery; renting demand rose as vacancy in major cities stayed below 2%. Real wages declined ~1.8% in 2023 with inflation ~3.4% (2024), shifting searches to lower-price tiers; institutional share reached ~25% of transactions (2023), yields ~3–5%.

| Metric | Value |

|---|---|

| ECB deposit rate | ~4.0% (2024–25) |

| Transaction volume drop | ~15% at peak rates |

| Urban vacancy | <2% |

| Real wages (2023) | −1.8% |

| Institutional share (2023) | ~25% |

| Yield expectations | ~3–5% |

Same Document Delivered

Scout24 PESTLE Analysis

The Scout24 PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying and will be delivered exactly as shown, with no placeholders or teasers. The content, layout, and structure visible here are the same file you’ll download immediately after payment.

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic advantage with our focused PESTLE Analysis of Scout24—three concise insights into political, economic, and technological forces shaping its market position. Ideal for investors and strategists seeking actionable intelligence. Buy the full report to access the complete, editable deep-dive and make confident decisions.

Political factors

German housing policy shifts

Changes to rent caps and Mietspiegel rules and incentives for affordable housing—against the federal goal of 400,000 new homes/year—directly affect listing supply and landlord activity. Coalition priorities at federal and Länder levels can tighten or relax market dynamics, since Länder control local Mietspiegel implementation. Scout24 must monitor policy cycles to adjust pricing, products and communications. Regional variations across Länder require localized go-to-market strategies.

Urban planning and zoning

Zoning approvals and Germanys densification target of 400,000 new homes per year drive developer marketing spend and new-supply volumes, while building permits (~270,000 permits in 2023 per Destatis) directly constrain pipeline and listings. Delays or planning reforms shift demand onto existing stock, altering listing composition and price dynamics. Partnerships with municipalities to provide data-driven planning tools reinforce Scout24s role as a market-intelligence partner.

EU digital platform oversight

EU and German momentum for stricter platform governance (DMA effective 2023; 22 gatekeepers designated) raises compliance expectations, with DMA fines up to 10% and DSA fines up to 6% of global turnover. Political scrutiny of marketplace fairness can force changes to ranking, ad labeling and access rules. Proactive stakeholder engagement reduces regulatory friction and helps shape pragmatic standards for real estate portals.

Public housing and subsidies

Scout24 can integrate subsidy workflows and eligibility filters into listings and lead flows to improve matching and conversion; the EU Renovation Wave aims to double renovation rates by 2030, creating landlord incentives for energy-efficient upgrades.

- Align listings with subsidy eligibility filters

- Target landlord tools for energy-efficiency upgrades

- Monitor budget shifts to predict rental vs purchase demand

Geopolitical and migration dynamics

Migration inflows and humanitarian policies concentrate demand in major cities and tighten rentals; UNHCR reported 108.4 million displaced worldwide end-2023 and Eurostat recorded 828,000 first-time asylum applicants in EU+EFTA in 2023. Political responses shape temporary housing, integration programs and regional allocation, altering local supply. Scout24 can add filters for short-term, furnished and shared options to capture these policy-driven segments.

- Short-term rentals

- Furnished listings

- Shared/accommodation

- Regional allocation tracking

Listings squeezed: target 400,000/yr vs permits ~270k

Policy on rent caps, Mietspiegel and Germanys 400,000 homes/year target (federal) alters listing supply and landlord incentives; 2023 building permits ~270,000 (Destatis) constrain new listings. DMA/DSA governance (DMA effective 2023; fines up to 10%/6% turnover) increases platform compliance costs. Subsidies and Renovation Wave (double renovations by 2030) shift demand toward energy-efficient upgrades; homeownership ~46% (Eurostat).

| Metric | Value |

|---|---|

| Homes target | 400,000/yr |

| Building permits 2023 | ~270,000 |

| Homeownership | ~46% |

| Displaced (end‑2023) | 108.4M (UNHCR) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Scout24, combining data-driven trends and region-specific regulatory context to identify strategic risks and opportunities for executives, investors, and consultants with forward-looking insights ready for reports and pitch decks.

Concise, visually segmented Scout24 PESTLE summary for quick reference in meetings or presentations, easily editable for regional or business-specific notes and shareable across teams to support risk and strategy discussions.

Economic factors

Interest rate and mortgage cycles

ECB rate moves (deposit rate ~4.00% in 2024–25) directly affect mortgage affordability and German transaction volumes, which fell about 15% at peak rates while lower rates later revived buyer traffic and listings. Higher rates have shifted demand toward renting. Scout24’s revenue mix should balance listing products with value-added services; flexible pricing and ancillary services can buffer cyclical swings.

Construction slowdown and supply gaps

Cost inflation and rising builder insolvencies are constraining new supply, keeping vacancy in major German cities below 2% and sustaining tight rental markets. Lower completions keep demand concentrated on existing stock, supporting higher listing engagement on Scout24 platforms. Developers are reallocating budgets toward more efficient digital marketing; Scout24 can capture this by offering performance-based packages tied to leads and conversions.

Advertising and agent budgets

Broker and landlord ad spend closely tracks transaction volumes and time-to-let/sell, so downturns see budgets shift to highest-ROI channels, favoring category leaders like major portals. Clear attribution and lead-quality metrics underpin pricing power by proving superior conversion and lower cost-per-lease. Vendors offset softer volumes by upselling analytics and premium listing tools tied to measurable outcomes.

Household income and inflation

Real wages in Germany fell about 1.8% in 2023, tightening household affordability and shifting search filters toward lower-price tiers; with inflation around 3.4% in 2024, time-on-market shortens for budget listings while premium listings see weaker conversion. Tenants trade down to smaller units and suburban locations; Scout24 must price premium placements to deliver clear ROI and offer flexible bundles to retain advertisers.

- real-wage decline presses affordability

- inflation → demand for smaller, peripheral units

- premium pricing must match ROI; flexible bundles aid retention

Liquidity and investor sentiment

Institutional appetite for residential assets rose to roughly 25% of German transaction volumes by 2023, increasing portfolio churn and professional listings as investors seek scale; yield expectations around 3–5% versus financing costs elevated by policy rates near 4% in 2024–25 compress deal flow and slow pacing. Scout24 can monetise this by selling pricing, comps and absorption analytics to investors and brokers, diversifying revenue beyond pure listings.

- institutional-share: ~25% (Germany, 2023)

- policy-rate: ~4% (2024–25)

- product-opportunity: pricing, comps, absorption data

Listings squeezed: target 400,000/yr vs permits ~270k

ECB deposit rate ~4.0% (2024–25) tightened mortgage affordability, German transaction volumes fell ~15% at peak rates before partial recovery; renting demand rose as vacancy in major cities stayed below 2%. Real wages declined ~1.8% in 2023 with inflation ~3.4% (2024), shifting searches to lower-price tiers; institutional share reached ~25% of transactions (2023), yields ~3–5%.

| Metric | Value |

|---|---|

| ECB deposit rate | ~4.0% (2024–25) |

| Transaction volume drop | ~15% at peak rates |

| Urban vacancy | <2% |

| Real wages (2023) | −1.8% |

| Institutional share (2023) | ~25% |

| Yield expectations | ~3–5% |

Same Document Delivered

Scout24 PESTLE Analysis

The Scout24 PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying and will be delivered exactly as shown, with no placeholders or teasers. The content, layout, and structure visible here are the same file you’ll download immediately after payment.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic advantage with our focused PESTLE Analysis of Scout24—three concise insights into political, economic, and technological forces shaping its market position. Ideal for investors and strategists seeking actionable intelligence. Buy the full report to access the complete, editable deep-dive and make confident decisions.

Political factors

German housing policy shifts

Changes to rent caps and Mietspiegel rules and incentives for affordable housing—against the federal goal of 400,000 new homes/year—directly affect listing supply and landlord activity. Coalition priorities at federal and Länder levels can tighten or relax market dynamics, since Länder control local Mietspiegel implementation. Scout24 must monitor policy cycles to adjust pricing, products and communications. Regional variations across Länder require localized go-to-market strategies.

Urban planning and zoning

Zoning approvals and Germanys densification target of 400,000 new homes per year drive developer marketing spend and new-supply volumes, while building permits (~270,000 permits in 2023 per Destatis) directly constrain pipeline and listings. Delays or planning reforms shift demand onto existing stock, altering listing composition and price dynamics. Partnerships with municipalities to provide data-driven planning tools reinforce Scout24s role as a market-intelligence partner.

EU digital platform oversight

EU and German momentum for stricter platform governance (DMA effective 2023; 22 gatekeepers designated) raises compliance expectations, with DMA fines up to 10% and DSA fines up to 6% of global turnover. Political scrutiny of marketplace fairness can force changes to ranking, ad labeling and access rules. Proactive stakeholder engagement reduces regulatory friction and helps shape pragmatic standards for real estate portals.

Public housing and subsidies

Scout24 can integrate subsidy workflows and eligibility filters into listings and lead flows to improve matching and conversion; the EU Renovation Wave aims to double renovation rates by 2030, creating landlord incentives for energy-efficient upgrades.

- Align listings with subsidy eligibility filters

- Target landlord tools for energy-efficiency upgrades

- Monitor budget shifts to predict rental vs purchase demand

Geopolitical and migration dynamics

Migration inflows and humanitarian policies concentrate demand in major cities and tighten rentals; UNHCR reported 108.4 million displaced worldwide end-2023 and Eurostat recorded 828,000 first-time asylum applicants in EU+EFTA in 2023. Political responses shape temporary housing, integration programs and regional allocation, altering local supply. Scout24 can add filters for short-term, furnished and shared options to capture these policy-driven segments.

- Short-term rentals

- Furnished listings

- Shared/accommodation

- Regional allocation tracking

Listings squeezed: target 400,000/yr vs permits ~270k

Policy on rent caps, Mietspiegel and Germanys 400,000 homes/year target (federal) alters listing supply and landlord incentives; 2023 building permits ~270,000 (Destatis) constrain new listings. DMA/DSA governance (DMA effective 2023; fines up to 10%/6% turnover) increases platform compliance costs. Subsidies and Renovation Wave (double renovations by 2030) shift demand toward energy-efficient upgrades; homeownership ~46% (Eurostat).

| Metric | Value |

|---|---|

| Homes target | 400,000/yr |

| Building permits 2023 | ~270,000 |

| Homeownership | ~46% |

| Displaced (end‑2023) | 108.4M (UNHCR) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Scout24, combining data-driven trends and region-specific regulatory context to identify strategic risks and opportunities for executives, investors, and consultants with forward-looking insights ready for reports and pitch decks.

Concise, visually segmented Scout24 PESTLE summary for quick reference in meetings or presentations, easily editable for regional or business-specific notes and shareable across teams to support risk and strategy discussions.

Economic factors

Interest rate and mortgage cycles

ECB rate moves (deposit rate ~4.00% in 2024–25) directly affect mortgage affordability and German transaction volumes, which fell about 15% at peak rates while lower rates later revived buyer traffic and listings. Higher rates have shifted demand toward renting. Scout24’s revenue mix should balance listing products with value-added services; flexible pricing and ancillary services can buffer cyclical swings.

Construction slowdown and supply gaps

Cost inflation and rising builder insolvencies are constraining new supply, keeping vacancy in major German cities below 2% and sustaining tight rental markets. Lower completions keep demand concentrated on existing stock, supporting higher listing engagement on Scout24 platforms. Developers are reallocating budgets toward more efficient digital marketing; Scout24 can capture this by offering performance-based packages tied to leads and conversions.

Advertising and agent budgets

Broker and landlord ad spend closely tracks transaction volumes and time-to-let/sell, so downturns see budgets shift to highest-ROI channels, favoring category leaders like major portals. Clear attribution and lead-quality metrics underpin pricing power by proving superior conversion and lower cost-per-lease. Vendors offset softer volumes by upselling analytics and premium listing tools tied to measurable outcomes.

Household income and inflation

Real wages in Germany fell about 1.8% in 2023, tightening household affordability and shifting search filters toward lower-price tiers; with inflation around 3.4% in 2024, time-on-market shortens for budget listings while premium listings see weaker conversion. Tenants trade down to smaller units and suburban locations; Scout24 must price premium placements to deliver clear ROI and offer flexible bundles to retain advertisers.

- real-wage decline presses affordability

- inflation → demand for smaller, peripheral units

- premium pricing must match ROI; flexible bundles aid retention

Liquidity and investor sentiment

Institutional appetite for residential assets rose to roughly 25% of German transaction volumes by 2023, increasing portfolio churn and professional listings as investors seek scale; yield expectations around 3–5% versus financing costs elevated by policy rates near 4% in 2024–25 compress deal flow and slow pacing. Scout24 can monetise this by selling pricing, comps and absorption analytics to investors and brokers, diversifying revenue beyond pure listings.

- institutional-share: ~25% (Germany, 2023)

- policy-rate: ~4% (2024–25)

- product-opportunity: pricing, comps, absorption data

Listings squeezed: target 400,000/yr vs permits ~270k

ECB deposit rate ~4.0% (2024–25) tightened mortgage affordability, German transaction volumes fell ~15% at peak rates before partial recovery; renting demand rose as vacancy in major cities stayed below 2%. Real wages declined ~1.8% in 2023 with inflation ~3.4% (2024), shifting searches to lower-price tiers; institutional share reached ~25% of transactions (2023), yields ~3–5%.

| Metric | Value |

|---|---|

| ECB deposit rate | ~4.0% (2024–25) |

| Transaction volume drop | ~15% at peak rates |

| Urban vacancy | <2% |

| Real wages (2023) | −1.8% |

| Institutional share (2023) | ~25% |

| Yield expectations | ~3–5% |

Same Document Delivered

Scout24 PESTLE Analysis

The Scout24 PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying and will be delivered exactly as shown, with no placeholders or teasers. The content, layout, and structure visible here are the same file you’ll download immediately after payment.