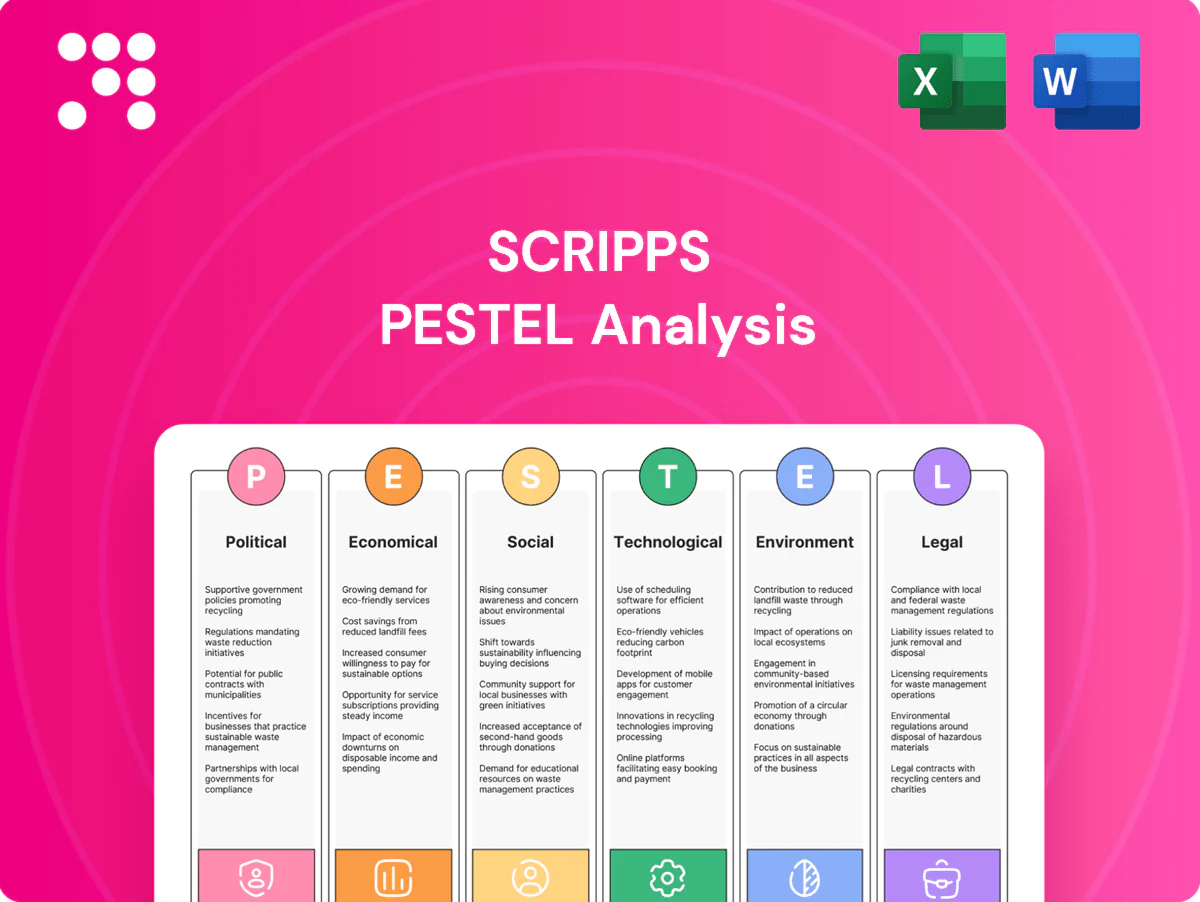

Scripps PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our targeted PESTLE analysis of Scripps—mapping political, economic, social, technological, legal, and environmental forces that will shape its trajectory. Ideal for investors, advisors, and strategists, this concise report highlights risks and opportunities you can act on. Purchase the full, editable analysis to get deep, ready-to-use insights now.

Political factors

FCC oversight and spectrum policy

Scripps operates roughly 60 TV stations reaching about 60% of US TV households (2024), while the FCC controls broadcast licenses, ownership limits and spectrum use that shape market reach and consolidation options. Changes in localism rules, cross-ownership policy or ATSC 3.0 mandates (NextGen TV ~80% household coverage in 2024) can shift competitive dynamics. Compliance drives capital planning and station portfolio strategy, so active advocacy is required to anticipate rulemaking shifts.

Political advertising cycles

Election years drive spikes in political ad revenue for local TV—2024 saw record national political ad spend, boosting broadcaster margins and producing outsized quarterly results for station groups. Off-cycle years create tougher comps and revenue volatility for Scripps as political line items decline. Shifts in campaign finance rules can reallocate spend across TV and digital, so Scripps must align inventory, pricing and sales capacity to electoral calendars.

Public media policy and subsidies

Debates over journalism support, tax incentives and misinformation countermeasures reshape local news economics and revenue models, influencing ad and subscription mixes. Government initiatives to fund solutions for news deserts or subsidize fact‑checking can alter competitive balance and market share. Policy favoring local content would benefit Scripps’ roughly 62 local TV stations, while tighter content regulation could raise compliance costs and cap margins.

Geopolitics and national security scrutiny

Geopolitical tensions increase scrutiny of broadcast infrastructure and signal security, pushing regulators to review vendor trustworthiness and incident reporting practices. Government guidance on disinformation control is prompting tighter operational standards for local newsrooms and content moderation workflows. Export controls and supply restrictions on telecom equipment have complicated upgrade timelines, so Scripps must harden networks and diversify vendors to maintain resilience.

- Heightened regulatory review of broadcast infrastructure

- Tighter disinformation controls affecting operations

- Supply restrictions constrain telecom upgrades

- Need to harden networks and diversify suppliers

State and municipal policies

State and municipal policies shape Scripps station profitability as local retransmission fee rules and varying state taxes/incentives affect carriage revenue and capex recovery; the FCC-mandated Emergency Alert System requires readiness across roughly 1,700 US full-power TV stations, adding compliance costs. Zoning and permitting influence transmitter siting and upgrade timelines, while coordinated government relations reduce project delays and expenses.

- Retransmission fee variability impacts revenue

- EAS readiness adds operational compliance

- Zoning/permitting affect capex timing

- Proactive government relations lower delays/costs

FCC, ATSC 3.0 and cyber mandates reshape broadcasters as 2024 political TV ad boom bites

Scripps faces FCC rulemaking on ownership, ATSC 3.0 mandates and localism that shape consolidation and capex choices; compliance drives station portfolio and advocacy. Election cycles cause large revenue swings—2024 saw national political TV ad spend >$10B, boosting broadcaster margins. Supply restrictions and cybersecurity scrutiny raise infrastructure costs and vendor diversification needs.

| Metric | 2024 |

|---|---|

| Owned stations | ~62 |

| US TV household reach | ~60% |

| ATSC 3.0 coverage | ~80% |

| Political ad spend (US) | >$10B |

What is included in the product

Explores how macro-environmental factors uniquely affect Scripps across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, forward-looking insights and actionable sub-points to help executives, investors and strategists identify risks, opportunities and competitive implications.

A concise, visually segmented Scripps PESTLE summary that’s easy to drop into presentations, share across teams, and edit for local context, using clear language to support planning discussions on external risk and market positioning.

Economic factors

Advertising spend sensitivity

Advertising spend sensitivity: Scripps revenue is highly cyclical, tracking ad budgets, CPI (US inflation ~3.4% in 2024) and GDP growth (US GDP ~2.5% in 2024), so macro slowdowns hit ad bookings quickly. Weak consumer sentiment compresses local and national demand, especially in auto and retail, while political cycles inject quarterly volatility. Diversification into digital audio and CTV helps smooth those swings.

Cord-cutting and distribution economics

Pay-TV declines—U.S. traditional pay-TV subs fell to roughly 50 million by 2024 per Leichtman Research Group—erode retransmission fee bases and audience reach, pressuring Scripps’ carriage revenues. Growth of vMVPDs and FAST/CTV shifts pricing, measurement and revenue shares toward ad-supported and programmatic models. Strong negotiation leverage with distributors is critical to preserve economics, while DTC experiments hedge distribution risk.

Cost inflation and capex needs

Content, labor, and energy inflation—US CPI rose about 3.4% in 2024—have pushed Scripps operating costs higher, feeding into tighter margins. ATSC 3.0 and IP workflow builds require ongoing capex, with industry estimates of roughly $0.5–2.0 million per station for upgrades. Ongoing supply-chain delays since 2021 can extend timelines and budgets; disciplined procurement and vendor diversification reduce exposure to cost shocks.

Interest rates and balance sheet

Higher interest rates (policy rates near 5.25% in mid‑2025) raise Scripps’ debt service and constrain free cash flow, limiting M&A capacity and pushing focus to refinancing windows and covenant headroom management.

- Higher debt service reduces liquidity

- Refinancing timing critical for covenant relief

- Free cash depends on retrans cycle and elections

- Capital allocation: deleveraging vs growth

Audience fragmentation

Shifts to streaming, podcasts and social platforms fragment reach and pressure CPMs; US podcast ad spend reached about 2.1 billion in 2024 and CTV ad dollars grew ~20% year-over-year, diluting linear inventory value.

- Measurement gaps suppress yield without verified attribution

- Bundled cross-platform packages defend share

- Data-driven sales lift pricing power across formats

FCC, ATSC 3.0 and cyber mandates reshape broadcasters as 2024 political TV ad boom bites

Scripps revenue is cyclical—ad spend tracks US CPI ~3.4% and GDP ~2.5% in 2024—so macro slowdowns and political cycles hit bookings; pay-TV subs fell to ~50M in 2024, shifting revenue to ad‑supported CTV/podcast channels. Higher rates (~5.25% mid‑2025) and station capex (ATSC 3.0 $0.5–2M) tighten cash flow and M&A optionality.

| Metric | 2024/2025 |

|---|---|

| US CPI (2024) | ~3.4% |

| US GDP (2024) | ~2.5% |

| Pay‑TV subs (US, 2024) | ~50M |

| Podcast ad spend (2024) | $2.1B |

| CTV ad growth (YoY) | ~20% |

| Policy rate (mid‑2025) | ~5.25% |

| ATSC 3.0 capex per station | $0.5–2.0M |

Preview the Actual Deliverable

Scripps PESTLE Analysis

The Scripps PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment. No placeholders or teasers—this is the final, downloadable file. What you see is what you’ll get upon checkout.

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our targeted PESTLE analysis of Scripps—mapping political, economic, social, technological, legal, and environmental forces that will shape its trajectory. Ideal for investors, advisors, and strategists, this concise report highlights risks and opportunities you can act on. Purchase the full, editable analysis to get deep, ready-to-use insights now.

Political factors

FCC oversight and spectrum policy

Scripps operates roughly 60 TV stations reaching about 60% of US TV households (2024), while the FCC controls broadcast licenses, ownership limits and spectrum use that shape market reach and consolidation options. Changes in localism rules, cross-ownership policy or ATSC 3.0 mandates (NextGen TV ~80% household coverage in 2024) can shift competitive dynamics. Compliance drives capital planning and station portfolio strategy, so active advocacy is required to anticipate rulemaking shifts.

Political advertising cycles

Election years drive spikes in political ad revenue for local TV—2024 saw record national political ad spend, boosting broadcaster margins and producing outsized quarterly results for station groups. Off-cycle years create tougher comps and revenue volatility for Scripps as political line items decline. Shifts in campaign finance rules can reallocate spend across TV and digital, so Scripps must align inventory, pricing and sales capacity to electoral calendars.

Public media policy and subsidies

Debates over journalism support, tax incentives and misinformation countermeasures reshape local news economics and revenue models, influencing ad and subscription mixes. Government initiatives to fund solutions for news deserts or subsidize fact‑checking can alter competitive balance and market share. Policy favoring local content would benefit Scripps’ roughly 62 local TV stations, while tighter content regulation could raise compliance costs and cap margins.

Geopolitics and national security scrutiny

Geopolitical tensions increase scrutiny of broadcast infrastructure and signal security, pushing regulators to review vendor trustworthiness and incident reporting practices. Government guidance on disinformation control is prompting tighter operational standards for local newsrooms and content moderation workflows. Export controls and supply restrictions on telecom equipment have complicated upgrade timelines, so Scripps must harden networks and diversify vendors to maintain resilience.

- Heightened regulatory review of broadcast infrastructure

- Tighter disinformation controls affecting operations

- Supply restrictions constrain telecom upgrades

- Need to harden networks and diversify suppliers

State and municipal policies

State and municipal policies shape Scripps station profitability as local retransmission fee rules and varying state taxes/incentives affect carriage revenue and capex recovery; the FCC-mandated Emergency Alert System requires readiness across roughly 1,700 US full-power TV stations, adding compliance costs. Zoning and permitting influence transmitter siting and upgrade timelines, while coordinated government relations reduce project delays and expenses.

- Retransmission fee variability impacts revenue

- EAS readiness adds operational compliance

- Zoning/permitting affect capex timing

- Proactive government relations lower delays/costs

FCC, ATSC 3.0 and cyber mandates reshape broadcasters as 2024 political TV ad boom bites

Scripps faces FCC rulemaking on ownership, ATSC 3.0 mandates and localism that shape consolidation and capex choices; compliance drives station portfolio and advocacy. Election cycles cause large revenue swings—2024 saw national political TV ad spend >$10B, boosting broadcaster margins. Supply restrictions and cybersecurity scrutiny raise infrastructure costs and vendor diversification needs.

| Metric | 2024 |

|---|---|

| Owned stations | ~62 |

| US TV household reach | ~60% |

| ATSC 3.0 coverage | ~80% |

| Political ad spend (US) | >$10B |

What is included in the product

Explores how macro-environmental factors uniquely affect Scripps across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, forward-looking insights and actionable sub-points to help executives, investors and strategists identify risks, opportunities and competitive implications.

A concise, visually segmented Scripps PESTLE summary that’s easy to drop into presentations, share across teams, and edit for local context, using clear language to support planning discussions on external risk and market positioning.

Economic factors

Advertising spend sensitivity

Advertising spend sensitivity: Scripps revenue is highly cyclical, tracking ad budgets, CPI (US inflation ~3.4% in 2024) and GDP growth (US GDP ~2.5% in 2024), so macro slowdowns hit ad bookings quickly. Weak consumer sentiment compresses local and national demand, especially in auto and retail, while political cycles inject quarterly volatility. Diversification into digital audio and CTV helps smooth those swings.

Cord-cutting and distribution economics

Pay-TV declines—U.S. traditional pay-TV subs fell to roughly 50 million by 2024 per Leichtman Research Group—erode retransmission fee bases and audience reach, pressuring Scripps’ carriage revenues. Growth of vMVPDs and FAST/CTV shifts pricing, measurement and revenue shares toward ad-supported and programmatic models. Strong negotiation leverage with distributors is critical to preserve economics, while DTC experiments hedge distribution risk.

Cost inflation and capex needs

Content, labor, and energy inflation—US CPI rose about 3.4% in 2024—have pushed Scripps operating costs higher, feeding into tighter margins. ATSC 3.0 and IP workflow builds require ongoing capex, with industry estimates of roughly $0.5–2.0 million per station for upgrades. Ongoing supply-chain delays since 2021 can extend timelines and budgets; disciplined procurement and vendor diversification reduce exposure to cost shocks.

Interest rates and balance sheet

Higher interest rates (policy rates near 5.25% in mid‑2025) raise Scripps’ debt service and constrain free cash flow, limiting M&A capacity and pushing focus to refinancing windows and covenant headroom management.

- Higher debt service reduces liquidity

- Refinancing timing critical for covenant relief

- Free cash depends on retrans cycle and elections

- Capital allocation: deleveraging vs growth

Audience fragmentation

Shifts to streaming, podcasts and social platforms fragment reach and pressure CPMs; US podcast ad spend reached about 2.1 billion in 2024 and CTV ad dollars grew ~20% year-over-year, diluting linear inventory value.

- Measurement gaps suppress yield without verified attribution

- Bundled cross-platform packages defend share

- Data-driven sales lift pricing power across formats

FCC, ATSC 3.0 and cyber mandates reshape broadcasters as 2024 political TV ad boom bites

Scripps revenue is cyclical—ad spend tracks US CPI ~3.4% and GDP ~2.5% in 2024—so macro slowdowns and political cycles hit bookings; pay-TV subs fell to ~50M in 2024, shifting revenue to ad‑supported CTV/podcast channels. Higher rates (~5.25% mid‑2025) and station capex (ATSC 3.0 $0.5–2M) tighten cash flow and M&A optionality.

| Metric | 2024/2025 |

|---|---|

| US CPI (2024) | ~3.4% |

| US GDP (2024) | ~2.5% |

| Pay‑TV subs (US, 2024) | ~50M |

| Podcast ad spend (2024) | $2.1B |

| CTV ad growth (YoY) | ~20% |

| Policy rate (mid‑2025) | ~5.25% |

| ATSC 3.0 capex per station | $0.5–2.0M |

Preview the Actual Deliverable

Scripps PESTLE Analysis

The Scripps PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment. No placeholders or teasers—this is the final, downloadable file. What you see is what you’ll get upon checkout.

Description

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our targeted PESTLE analysis of Scripps—mapping political, economic, social, technological, legal, and environmental forces that will shape its trajectory. Ideal for investors, advisors, and strategists, this concise report highlights risks and opportunities you can act on. Purchase the full, editable analysis to get deep, ready-to-use insights now.

Political factors

FCC oversight and spectrum policy

Scripps operates roughly 60 TV stations reaching about 60% of US TV households (2024), while the FCC controls broadcast licenses, ownership limits and spectrum use that shape market reach and consolidation options. Changes in localism rules, cross-ownership policy or ATSC 3.0 mandates (NextGen TV ~80% household coverage in 2024) can shift competitive dynamics. Compliance drives capital planning and station portfolio strategy, so active advocacy is required to anticipate rulemaking shifts.

Political advertising cycles

Election years drive spikes in political ad revenue for local TV—2024 saw record national political ad spend, boosting broadcaster margins and producing outsized quarterly results for station groups. Off-cycle years create tougher comps and revenue volatility for Scripps as political line items decline. Shifts in campaign finance rules can reallocate spend across TV and digital, so Scripps must align inventory, pricing and sales capacity to electoral calendars.

Public media policy and subsidies

Debates over journalism support, tax incentives and misinformation countermeasures reshape local news economics and revenue models, influencing ad and subscription mixes. Government initiatives to fund solutions for news deserts or subsidize fact‑checking can alter competitive balance and market share. Policy favoring local content would benefit Scripps’ roughly 62 local TV stations, while tighter content regulation could raise compliance costs and cap margins.

Geopolitics and national security scrutiny

Geopolitical tensions increase scrutiny of broadcast infrastructure and signal security, pushing regulators to review vendor trustworthiness and incident reporting practices. Government guidance on disinformation control is prompting tighter operational standards for local newsrooms and content moderation workflows. Export controls and supply restrictions on telecom equipment have complicated upgrade timelines, so Scripps must harden networks and diversify vendors to maintain resilience.

- Heightened regulatory review of broadcast infrastructure

- Tighter disinformation controls affecting operations

- Supply restrictions constrain telecom upgrades

- Need to harden networks and diversify suppliers

State and municipal policies

State and municipal policies shape Scripps station profitability as local retransmission fee rules and varying state taxes/incentives affect carriage revenue and capex recovery; the FCC-mandated Emergency Alert System requires readiness across roughly 1,700 US full-power TV stations, adding compliance costs. Zoning and permitting influence transmitter siting and upgrade timelines, while coordinated government relations reduce project delays and expenses.

- Retransmission fee variability impacts revenue

- EAS readiness adds operational compliance

- Zoning/permitting affect capex timing

- Proactive government relations lower delays/costs

FCC, ATSC 3.0 and cyber mandates reshape broadcasters as 2024 political TV ad boom bites

Scripps faces FCC rulemaking on ownership, ATSC 3.0 mandates and localism that shape consolidation and capex choices; compliance drives station portfolio and advocacy. Election cycles cause large revenue swings—2024 saw national political TV ad spend >$10B, boosting broadcaster margins. Supply restrictions and cybersecurity scrutiny raise infrastructure costs and vendor diversification needs.

| Metric | 2024 |

|---|---|

| Owned stations | ~62 |

| US TV household reach | ~60% |

| ATSC 3.0 coverage | ~80% |

| Political ad spend (US) | >$10B |

What is included in the product

Explores how macro-environmental factors uniquely affect Scripps across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, forward-looking insights and actionable sub-points to help executives, investors and strategists identify risks, opportunities and competitive implications.

A concise, visually segmented Scripps PESTLE summary that’s easy to drop into presentations, share across teams, and edit for local context, using clear language to support planning discussions on external risk and market positioning.

Economic factors

Advertising spend sensitivity

Advertising spend sensitivity: Scripps revenue is highly cyclical, tracking ad budgets, CPI (US inflation ~3.4% in 2024) and GDP growth (US GDP ~2.5% in 2024), so macro slowdowns hit ad bookings quickly. Weak consumer sentiment compresses local and national demand, especially in auto and retail, while political cycles inject quarterly volatility. Diversification into digital audio and CTV helps smooth those swings.

Cord-cutting and distribution economics

Pay-TV declines—U.S. traditional pay-TV subs fell to roughly 50 million by 2024 per Leichtman Research Group—erode retransmission fee bases and audience reach, pressuring Scripps’ carriage revenues. Growth of vMVPDs and FAST/CTV shifts pricing, measurement and revenue shares toward ad-supported and programmatic models. Strong negotiation leverage with distributors is critical to preserve economics, while DTC experiments hedge distribution risk.

Cost inflation and capex needs

Content, labor, and energy inflation—US CPI rose about 3.4% in 2024—have pushed Scripps operating costs higher, feeding into tighter margins. ATSC 3.0 and IP workflow builds require ongoing capex, with industry estimates of roughly $0.5–2.0 million per station for upgrades. Ongoing supply-chain delays since 2021 can extend timelines and budgets; disciplined procurement and vendor diversification reduce exposure to cost shocks.

Interest rates and balance sheet

Higher interest rates (policy rates near 5.25% in mid‑2025) raise Scripps’ debt service and constrain free cash flow, limiting M&A capacity and pushing focus to refinancing windows and covenant headroom management.

- Higher debt service reduces liquidity

- Refinancing timing critical for covenant relief

- Free cash depends on retrans cycle and elections

- Capital allocation: deleveraging vs growth

Audience fragmentation

Shifts to streaming, podcasts and social platforms fragment reach and pressure CPMs; US podcast ad spend reached about 2.1 billion in 2024 and CTV ad dollars grew ~20% year-over-year, diluting linear inventory value.

- Measurement gaps suppress yield without verified attribution

- Bundled cross-platform packages defend share

- Data-driven sales lift pricing power across formats

FCC, ATSC 3.0 and cyber mandates reshape broadcasters as 2024 political TV ad boom bites

Scripps revenue is cyclical—ad spend tracks US CPI ~3.4% and GDP ~2.5% in 2024—so macro slowdowns and political cycles hit bookings; pay-TV subs fell to ~50M in 2024, shifting revenue to ad‑supported CTV/podcast channels. Higher rates (~5.25% mid‑2025) and station capex (ATSC 3.0 $0.5–2M) tighten cash flow and M&A optionality.

| Metric | 2024/2025 |

|---|---|

| US CPI (2024) | ~3.4% |

| US GDP (2024) | ~2.5% |

| Pay‑TV subs (US, 2024) | ~50M |

| Podcast ad spend (2024) | $2.1B |

| CTV ad growth (YoY) | ~20% |

| Policy rate (mid‑2025) | ~5.25% |

| ATSC 3.0 capex per station | $0.5–2.0M |

Preview the Actual Deliverable

Scripps PESTLE Analysis

The Scripps PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment. No placeholders or teasers—this is the final, downloadable file. What you see is what you’ll get upon checkout.