SD BioSensor Porter's Five Forces Analysis

From Overview to Strategy Blueprint

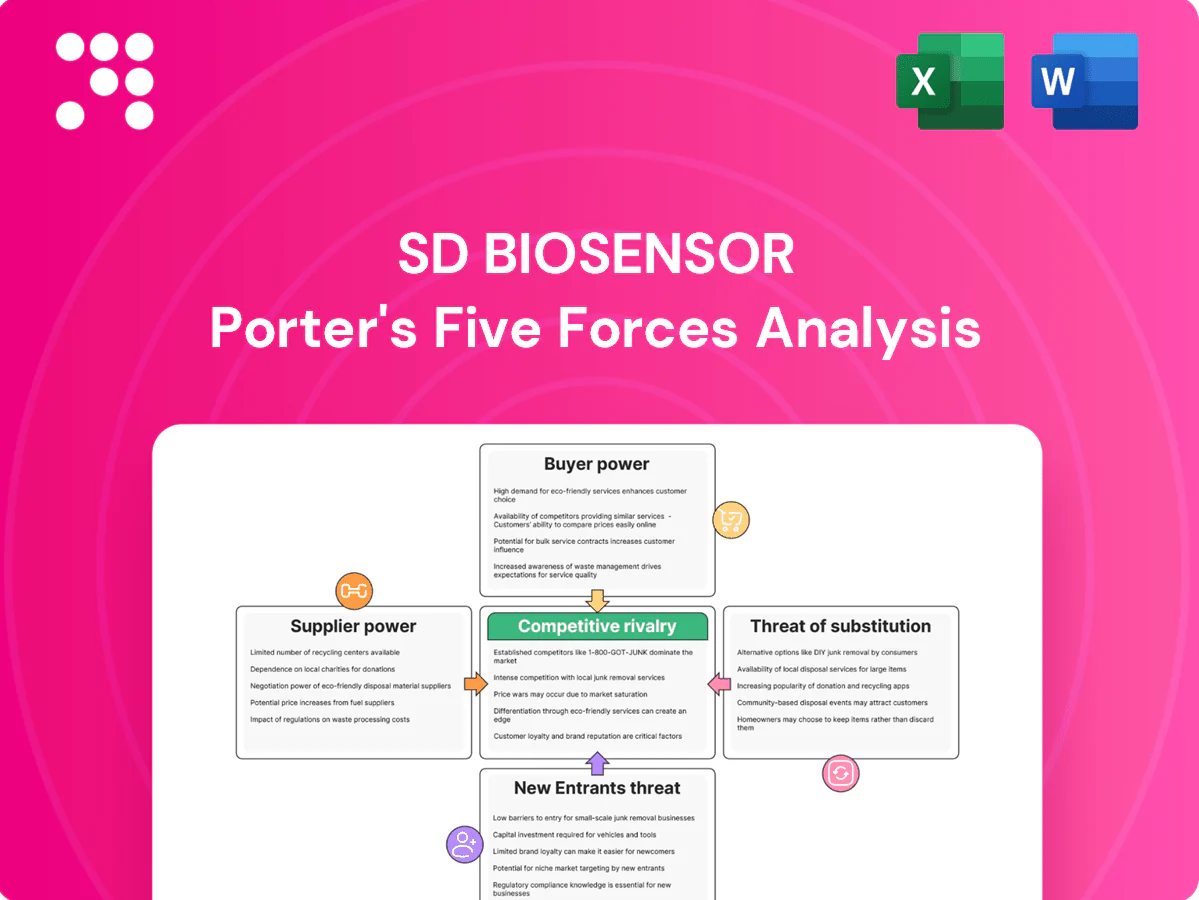

SD BioSensor faces moderate supplier power, strong buyer expectations for accuracy and cost, and significant rivalry from established diagnostics firms; regulatory hurdles and emerging tech substitutes shape competitive pressure. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategic insights.

Suppliers Bargaining Power

Concentrated specialty inputs

SD Biosensor depends on niche inputs—nitrocellulose membranes, monoclonal antibodies, enzymes and primers—sourced from a small pool of qualified suppliers, which in 2024 left buying leverage with vendors and raised supply risk. Any quality drift or disruption can stop production lines; industry experience in 2024 shows supplier qualification for diagnostics components typically requires 6–9 months and validation costs often range from $250k to $1M. Dual-sourcing is possible but materially raises capex and OPEX for revalidation and inventory buffering, compressing margins.

Regulatory-grade quality constraints

Inputs must meet ISO 13485 and IVD regulatory standards, elevating supplier influence; lot-to-lot consistency and traceable documentation are mandatory for audits. Suppliers certified to ISO 13485 with audit pass rates above 95% can demand firmer pricing and lead-time terms. Tight compliance reduces switching flexibility and raises switching costs for SD BioSensor, increasing supplier bargaining power.

Switching and revalidation costs

Changing a reagent or membrane triggers analytical and clinical revalidation, commonly adding 3–6 months to time-to-market and often exceeding $100,000 in validation and regulatory costs. These delays can cause labs to miss annual tender cycles and seasonal demand peaks, effectively locking customers to incumbent suppliers. Suppliers recognize these frictions and price with premiums, increasing their bargaining power.

Equipment and consumable lock-ins

- Proprietary cartridges drive recurring revenue and switching costs

- Tooling/mold requalification raises barriers and vendor leverage

- OEM dependence concentrates supplier bargaining power

Logistics and cold-chain exposure

Enzymes typically require frozen storage (−20°C to −80°C) and antibodies 2–8°C, making SD Biosensor highly dependent on reliable cold-chain logistics; in 2024 major logistics providers reported continued investment in temperature-controlled networks. Freight volatility and customs delays directly risk assay yields and time-to-market, while suppliers bundling cold-chain, customs brokerage and real-time monitoring gain pricing power. Currency and commodity swings in 2024 kept transport fuel surcharges variable, further tilting supplier terms.

- Temperature requirements: −20°C to −80°C (enzymes), 2–8°C (antibodies)

- Integrated 3PLs with monitoring and customs services = higher supplier leverage

- Freight/customs volatility and 2024 fuel surcharge swings increase cost/risk

Supplier concentration, long validation and cold-chain needs amplify vendor leverage

SD Biosensor relies on few qualified suppliers (qualification 6–9 months; validation $250k–$1M), raising vendor leverage in 2024. ISO 13485-certified suppliers (audit pass >95%) command premiums; switching triggers 3–6 month revalidation (+$100k). Cold-chain needs (enzymes −20°C to −80°C; antibodies 2–8°C) amplify logistics and cost risks.

What is included in the product

Concise Porter’s Five Forces for SD BioSensor revealing competitive intensity, supplier and buyer leverage, threat of substitutes and new entrants, plus regulatory and technological pressures shaping pricing and profitability.

A clear one-sheet Porter's Five Forces for SD Biosensor that instantly visualizes competitive pressure with a spider chart, lets you customize inputs for scenarios or regulatory shifts, and is ready to drop into pitch decks or Excel dashboards without macros.

Customers Bargaining Power

Large tenders and group purchasing

Governments, NGOs and hospital GPOs buy in bulk—US GPOs cover ~90% of hospitals and global tenders often exceed $10M—enabling steep price concessions. Tender-based procurement raises price transparency, driving public benchmark pricing. Volume rebates and framework agreements commonly shave 5–20% off list prices, compressing margins. Non-award risk can swing revenue forecasts by 20–50% and intensify pricing pressure.

Post-pandemic price sensitivity

Post-pandemic volume normalization has left buyers sharply cost-focused, turning procurement toward unit economics rather than brand—commodity rapid antigen tests saw mass-tender prices reported as low as $0.50 per unit in 2023–24. Aggressive price benchmarking across suppliers compresses margins and enables purchasers to credibly threaten switching to the lowest-cost alternative. This buyer power has largely restrained list-price increases across the sector through 2024.

Switching ease in commoditized tests

For common infectious panels switching cost is moderate when performance is comparable; buyers typically demand sensitivity and specificity at or above 95% and favor time-to-result under 60 minutes, so small performance gaps can trigger switches. Form-factor compatibility and retraining create limited stickiness, while private-label offerings—about 20% of rapid-test volumes in 2024—add pricing pressure.

Clinical performance and accreditation demands

Buyers demand robust peer-reviewed data and regulatory marks (WHO PQ, FDA clearance, CE‑IVDR) and prioritize demonstrable clinical performance; vendors with superior sensitivity/specificity routinely win tenders despite 10–30% price premiums. Weak post-market vigilance risks delistings and sanctions, while field service, QC support and fast complaint resolution drive renewals.

- Regulatory marks: WHO PQ, FDA, CE‑IVDR

- Performance beats price: 10–30% premium tolerated

- Post-market risk: delisting/sanctions

- Renewals hinge on service and QC

Channel concentration in distributors/retail

- 2024: top distributors >50% channel reach

- Retail chains demand higher shelf fees, lower margins

- MOQs and return rights transfer risk to supplier

GPOs force antigen-test prices to ~$0.50; performance/regulatory can add 10-30% premium

Buyers wield strong price leverage: hospital GPOs cover ~90% of US hospitals and tenders drive rebates of 5–20%, with non-award risk moving revenue 20–50%. Post‑pandemic cost focus pushed commodity antigen test tender prices to ~$0.50/unit in 2023–24 and kept list prices largely flat through 2024. Performance (sensitivity/specificity ≥95%) and regulatory marks can command 10–30% premiums. Top distributors held >50% channel reach in 2024, intensifying buyer bargaining.

| Metric | 2023–24 / 2024 |

|---|---|

| GPO hospital coverage | ~90% |

| Commodity test tender price | ~$0.50/unit |

| Rebates/framework discounts | 5–20% |

| Revenue swing if non-awarded | 20–50% |

| Private-label rapid-test share | ~20% |

| Top distributors' channel reach | >50% |

Full Version Awaits

SD BioSensor Porter's Five Forces Analysis

This preview shows the exact SD BioSensor Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. Instant access to the complete, final file.

From Overview to Strategy Blueprint

SD BioSensor faces moderate supplier power, strong buyer expectations for accuracy and cost, and significant rivalry from established diagnostics firms; regulatory hurdles and emerging tech substitutes shape competitive pressure. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategic insights.

Suppliers Bargaining Power

Concentrated specialty inputs

SD Biosensor depends on niche inputs—nitrocellulose membranes, monoclonal antibodies, enzymes and primers—sourced from a small pool of qualified suppliers, which in 2024 left buying leverage with vendors and raised supply risk. Any quality drift or disruption can stop production lines; industry experience in 2024 shows supplier qualification for diagnostics components typically requires 6–9 months and validation costs often range from $250k to $1M. Dual-sourcing is possible but materially raises capex and OPEX for revalidation and inventory buffering, compressing margins.

Regulatory-grade quality constraints

Inputs must meet ISO 13485 and IVD regulatory standards, elevating supplier influence; lot-to-lot consistency and traceable documentation are mandatory for audits. Suppliers certified to ISO 13485 with audit pass rates above 95% can demand firmer pricing and lead-time terms. Tight compliance reduces switching flexibility and raises switching costs for SD BioSensor, increasing supplier bargaining power.

Switching and revalidation costs

Changing a reagent or membrane triggers analytical and clinical revalidation, commonly adding 3–6 months to time-to-market and often exceeding $100,000 in validation and regulatory costs. These delays can cause labs to miss annual tender cycles and seasonal demand peaks, effectively locking customers to incumbent suppliers. Suppliers recognize these frictions and price with premiums, increasing their bargaining power.

Equipment and consumable lock-ins

- Proprietary cartridges drive recurring revenue and switching costs

- Tooling/mold requalification raises barriers and vendor leverage

- OEM dependence concentrates supplier bargaining power

Logistics and cold-chain exposure

Enzymes typically require frozen storage (−20°C to −80°C) and antibodies 2–8°C, making SD Biosensor highly dependent on reliable cold-chain logistics; in 2024 major logistics providers reported continued investment in temperature-controlled networks. Freight volatility and customs delays directly risk assay yields and time-to-market, while suppliers bundling cold-chain, customs brokerage and real-time monitoring gain pricing power. Currency and commodity swings in 2024 kept transport fuel surcharges variable, further tilting supplier terms.

- Temperature requirements: −20°C to −80°C (enzymes), 2–8°C (antibodies)

- Integrated 3PLs with monitoring and customs services = higher supplier leverage

- Freight/customs volatility and 2024 fuel surcharge swings increase cost/risk

Supplier concentration, long validation and cold-chain needs amplify vendor leverage

SD Biosensor relies on few qualified suppliers (qualification 6–9 months; validation $250k–$1M), raising vendor leverage in 2024. ISO 13485-certified suppliers (audit pass >95%) command premiums; switching triggers 3–6 month revalidation (+$100k). Cold-chain needs (enzymes −20°C to −80°C; antibodies 2–8°C) amplify logistics and cost risks.

What is included in the product

Concise Porter’s Five Forces for SD BioSensor revealing competitive intensity, supplier and buyer leverage, threat of substitutes and new entrants, plus regulatory and technological pressures shaping pricing and profitability.

A clear one-sheet Porter's Five Forces for SD Biosensor that instantly visualizes competitive pressure with a spider chart, lets you customize inputs for scenarios or regulatory shifts, and is ready to drop into pitch decks or Excel dashboards without macros.

Customers Bargaining Power

Large tenders and group purchasing

Governments, NGOs and hospital GPOs buy in bulk—US GPOs cover ~90% of hospitals and global tenders often exceed $10M—enabling steep price concessions. Tender-based procurement raises price transparency, driving public benchmark pricing. Volume rebates and framework agreements commonly shave 5–20% off list prices, compressing margins. Non-award risk can swing revenue forecasts by 20–50% and intensify pricing pressure.

Post-pandemic price sensitivity

Post-pandemic volume normalization has left buyers sharply cost-focused, turning procurement toward unit economics rather than brand—commodity rapid antigen tests saw mass-tender prices reported as low as $0.50 per unit in 2023–24. Aggressive price benchmarking across suppliers compresses margins and enables purchasers to credibly threaten switching to the lowest-cost alternative. This buyer power has largely restrained list-price increases across the sector through 2024.

Switching ease in commoditized tests

For common infectious panels switching cost is moderate when performance is comparable; buyers typically demand sensitivity and specificity at or above 95% and favor time-to-result under 60 minutes, so small performance gaps can trigger switches. Form-factor compatibility and retraining create limited stickiness, while private-label offerings—about 20% of rapid-test volumes in 2024—add pricing pressure.

Clinical performance and accreditation demands

Buyers demand robust peer-reviewed data and regulatory marks (WHO PQ, FDA clearance, CE‑IVDR) and prioritize demonstrable clinical performance; vendors with superior sensitivity/specificity routinely win tenders despite 10–30% price premiums. Weak post-market vigilance risks delistings and sanctions, while field service, QC support and fast complaint resolution drive renewals.

- Regulatory marks: WHO PQ, FDA, CE‑IVDR

- Performance beats price: 10–30% premium tolerated

- Post-market risk: delisting/sanctions

- Renewals hinge on service and QC

Channel concentration in distributors/retail

- 2024: top distributors >50% channel reach

- Retail chains demand higher shelf fees, lower margins

- MOQs and return rights transfer risk to supplier

GPOs force antigen-test prices to ~$0.50; performance/regulatory can add 10-30% premium

Buyers wield strong price leverage: hospital GPOs cover ~90% of US hospitals and tenders drive rebates of 5–20%, with non-award risk moving revenue 20–50%. Post‑pandemic cost focus pushed commodity antigen test tender prices to ~$0.50/unit in 2023–24 and kept list prices largely flat through 2024. Performance (sensitivity/specificity ≥95%) and regulatory marks can command 10–30% premiums. Top distributors held >50% channel reach in 2024, intensifying buyer bargaining.

| Metric | 2023–24 / 2024 |

|---|---|

| GPO hospital coverage | ~90% |

| Commodity test tender price | ~$0.50/unit |

| Rebates/framework discounts | 5–20% |

| Revenue swing if non-awarded | 20–50% |

| Private-label rapid-test share | ~20% |

| Top distributors' channel reach | >50% |

Full Version Awaits

SD BioSensor Porter's Five Forces Analysis

This preview shows the exact SD BioSensor Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. Instant access to the complete, final file.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

SD BioSensor faces moderate supplier power, strong buyer expectations for accuracy and cost, and significant rivalry from established diagnostics firms; regulatory hurdles and emerging tech substitutes shape competitive pressure. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategic insights.

Suppliers Bargaining Power

Concentrated specialty inputs

SD Biosensor depends on niche inputs—nitrocellulose membranes, monoclonal antibodies, enzymes and primers—sourced from a small pool of qualified suppliers, which in 2024 left buying leverage with vendors and raised supply risk. Any quality drift or disruption can stop production lines; industry experience in 2024 shows supplier qualification for diagnostics components typically requires 6–9 months and validation costs often range from $250k to $1M. Dual-sourcing is possible but materially raises capex and OPEX for revalidation and inventory buffering, compressing margins.

Regulatory-grade quality constraints

Inputs must meet ISO 13485 and IVD regulatory standards, elevating supplier influence; lot-to-lot consistency and traceable documentation are mandatory for audits. Suppliers certified to ISO 13485 with audit pass rates above 95% can demand firmer pricing and lead-time terms. Tight compliance reduces switching flexibility and raises switching costs for SD BioSensor, increasing supplier bargaining power.

Switching and revalidation costs

Changing a reagent or membrane triggers analytical and clinical revalidation, commonly adding 3–6 months to time-to-market and often exceeding $100,000 in validation and regulatory costs. These delays can cause labs to miss annual tender cycles and seasonal demand peaks, effectively locking customers to incumbent suppliers. Suppliers recognize these frictions and price with premiums, increasing their bargaining power.

Equipment and consumable lock-ins

- Proprietary cartridges drive recurring revenue and switching costs

- Tooling/mold requalification raises barriers and vendor leverage

- OEM dependence concentrates supplier bargaining power

Logistics and cold-chain exposure

Enzymes typically require frozen storage (−20°C to −80°C) and antibodies 2–8°C, making SD Biosensor highly dependent on reliable cold-chain logistics; in 2024 major logistics providers reported continued investment in temperature-controlled networks. Freight volatility and customs delays directly risk assay yields and time-to-market, while suppliers bundling cold-chain, customs brokerage and real-time monitoring gain pricing power. Currency and commodity swings in 2024 kept transport fuel surcharges variable, further tilting supplier terms.

- Temperature requirements: −20°C to −80°C (enzymes), 2–8°C (antibodies)

- Integrated 3PLs with monitoring and customs services = higher supplier leverage

- Freight/customs volatility and 2024 fuel surcharge swings increase cost/risk

Supplier concentration, long validation and cold-chain needs amplify vendor leverage

SD Biosensor relies on few qualified suppliers (qualification 6–9 months; validation $250k–$1M), raising vendor leverage in 2024. ISO 13485-certified suppliers (audit pass >95%) command premiums; switching triggers 3–6 month revalidation (+$100k). Cold-chain needs (enzymes −20°C to −80°C; antibodies 2–8°C) amplify logistics and cost risks.

What is included in the product

Concise Porter’s Five Forces for SD BioSensor revealing competitive intensity, supplier and buyer leverage, threat of substitutes and new entrants, plus regulatory and technological pressures shaping pricing and profitability.

A clear one-sheet Porter's Five Forces for SD Biosensor that instantly visualizes competitive pressure with a spider chart, lets you customize inputs for scenarios or regulatory shifts, and is ready to drop into pitch decks or Excel dashboards without macros.

Customers Bargaining Power

Large tenders and group purchasing

Governments, NGOs and hospital GPOs buy in bulk—US GPOs cover ~90% of hospitals and global tenders often exceed $10M—enabling steep price concessions. Tender-based procurement raises price transparency, driving public benchmark pricing. Volume rebates and framework agreements commonly shave 5–20% off list prices, compressing margins. Non-award risk can swing revenue forecasts by 20–50% and intensify pricing pressure.

Post-pandemic price sensitivity

Post-pandemic volume normalization has left buyers sharply cost-focused, turning procurement toward unit economics rather than brand—commodity rapid antigen tests saw mass-tender prices reported as low as $0.50 per unit in 2023–24. Aggressive price benchmarking across suppliers compresses margins and enables purchasers to credibly threaten switching to the lowest-cost alternative. This buyer power has largely restrained list-price increases across the sector through 2024.

Switching ease in commoditized tests

For common infectious panels switching cost is moderate when performance is comparable; buyers typically demand sensitivity and specificity at or above 95% and favor time-to-result under 60 minutes, so small performance gaps can trigger switches. Form-factor compatibility and retraining create limited stickiness, while private-label offerings—about 20% of rapid-test volumes in 2024—add pricing pressure.

Clinical performance and accreditation demands

Buyers demand robust peer-reviewed data and regulatory marks (WHO PQ, FDA clearance, CE‑IVDR) and prioritize demonstrable clinical performance; vendors with superior sensitivity/specificity routinely win tenders despite 10–30% price premiums. Weak post-market vigilance risks delistings and sanctions, while field service, QC support and fast complaint resolution drive renewals.

- Regulatory marks: WHO PQ, FDA, CE‑IVDR

- Performance beats price: 10–30% premium tolerated

- Post-market risk: delisting/sanctions

- Renewals hinge on service and QC

Channel concentration in distributors/retail

- 2024: top distributors >50% channel reach

- Retail chains demand higher shelf fees, lower margins

- MOQs and return rights transfer risk to supplier

GPOs force antigen-test prices to ~$0.50; performance/regulatory can add 10-30% premium

Buyers wield strong price leverage: hospital GPOs cover ~90% of US hospitals and tenders drive rebates of 5–20%, with non-award risk moving revenue 20–50%. Post‑pandemic cost focus pushed commodity antigen test tender prices to ~$0.50/unit in 2023–24 and kept list prices largely flat through 2024. Performance (sensitivity/specificity ≥95%) and regulatory marks can command 10–30% premiums. Top distributors held >50% channel reach in 2024, intensifying buyer bargaining.

| Metric | 2023–24 / 2024 |

|---|---|

| GPO hospital coverage | ~90% |

| Commodity test tender price | ~$0.50/unit |

| Rebates/framework discounts | 5–20% |

| Revenue swing if non-awarded | 20–50% |

| Private-label rapid-test share | ~20% |

| Top distributors' channel reach | >50% |

Full Version Awaits

SD BioSensor Porter's Five Forces Analysis

This preview shows the exact SD BioSensor Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. Instant access to the complete, final file.