Showa Denko K.K. Boston Consulting Group Matrix

Download Your Competitive Advantage

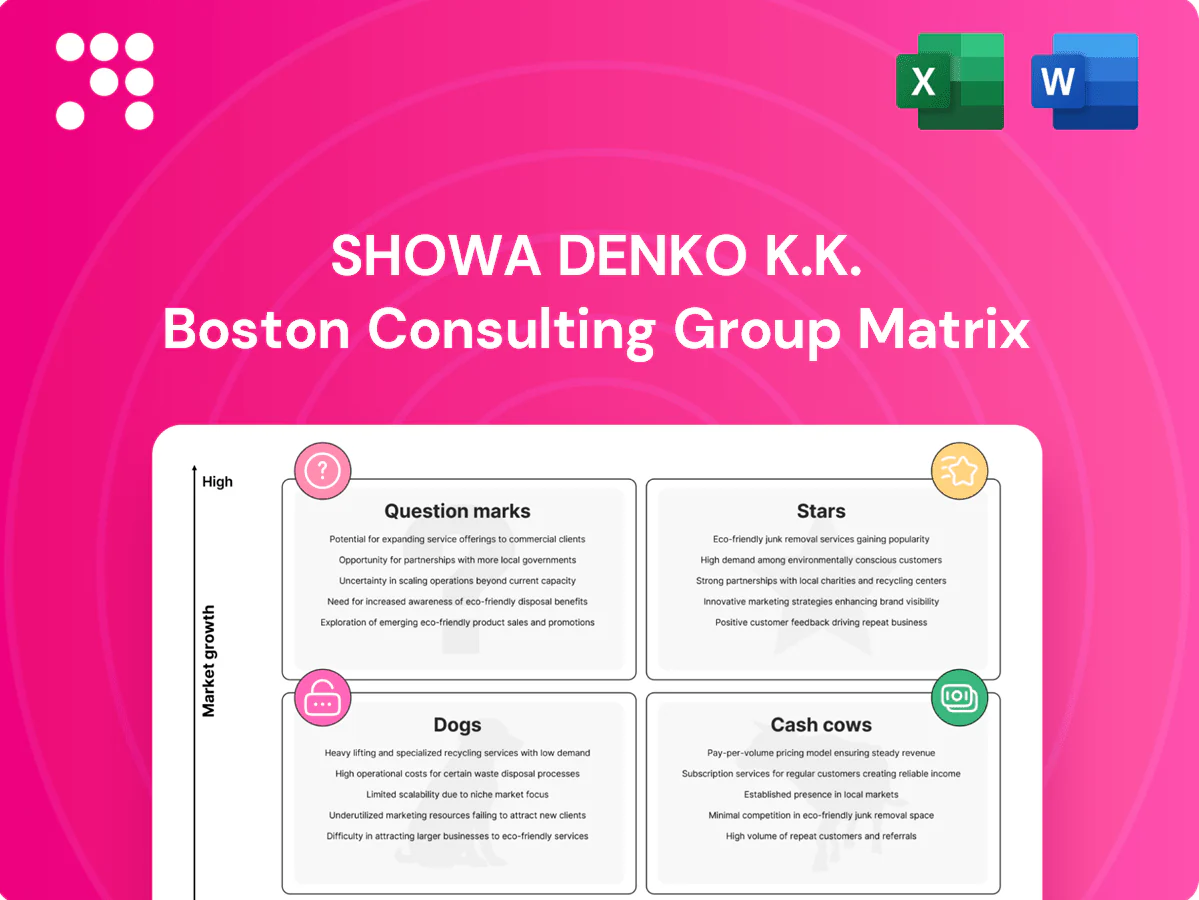

Quick look at Showa Denko K.K.'s BCG Matrix shows where its chemicals, electronic materials and carbon products sit in the market—some are clear Stars, others edging toward Cash Cows or Question Marks. This preview maps the big moves, but the full BCG Matrix gives quadrant-by-quadrant data, strategic recommendations, and actionable next steps. Buy the full report to get a polished Word analysis plus an Excel summary you can use in board decks. Purchase now and skip the guesswork—get clarity fast.

Stars

SiC epitaxial wafers (power semiconductors)

SiC epitaxial wafers sit in a high-growth end market driven by EV inverters and industrial power drives, with industry forecasts in 2024 projecting mid-to-high double-digit CAGR for SiC device demand. Resonac (ex-Showa Denko), renamed in 2023, is a recognized leader in epi quality and capacity, securing design-wins with Tier‑1 device makers. The business soaks up capex today but scaling capacity now is the play to convert volume into long-term margin expansion.

CMP slurries & pads for advanced nodes

Wafer complexity keeps rising—more layers and denser metallization increase planarization demand, reinforcing CMP slurries & pads as a star business for Showa Denko. The unit holds strong share in critical slurry formulations with sticky qualifications that create high switching costs for customers. Growth is brisk while cash needs are heavy for R&D and customer support to defend specs. Strategy: stay on offense—invest in formulation wins and bundle services to lock in customers.

Specialty electronic gases (high purity)

Specialty electronic gases lead in select etch/clean chemistries for advanced logic and memory, directly tied to node shrinks and scaling; segment reports high-teens to low-double-digit growth rates industry-wide (CAGR >10%). High technical barriers and intensive QA/logistics create steep entry costs and recurring CAPEX; cash generated is reinvested into purification, distribution, and reliability. Scale and customer trust function as durable moats, supporting premium pricing and long-term contracts.

Semiconductor packaging materials (encapsulation, die-attach)

Advanced packaging demand is running hot in 2024 driven by chiplets, 2.5D/3D interposers and rising automotive reliability requirements; automotive semiconductor content averaged about USD 550 per vehicle in 2024, boosting need for robust encapsulation and die-attach. Showa Denko’s materials are entrenched with major OSATs and IDMs, and new formulations keep design windows open. The segment is growthy, lab-intensive and cash-hungry, so continued capex and R&D are required to convert design-ins into durable share.

- Market tailwinds: advanced packaging CAGR ~12% from 2024 (industry consensus)

- Competitive moat: long OEM/OSAT qualification cycles favor incumbents

- Cash profile: high R&D and pilot-line costs; reinvest to secure long-term share

EV battery materials (anodes/binders)

EV battery materials (anodes/binders) are Stars: Li-ion demand remains steep with global EV sales ~14 million in 2023 and battery supply needs accelerating; Hitachi Chemical heritage (integrated into Showa Denko since 2020) provides proven tech and customer ties. OEM and cell-maker qualifications (typically 12–24 months) create high switching costs; growth is strong but capex is heavy, with gigafactory investments often >$1bn. Push capacity where contracts are sticky and chemistries defensible.

- Demand tag: global EV sales ~14m (2023)

- Qualification tag: 12–24 months

- Capex tag: gigafactory >$1bn

- Strategy tag: focus on sticky contracts & defensible chemistries

SiC, CMP slurries and EV battery materials: high-growth, capex-heavy markets

Stars: SiC epi/wafers and CMP slurries sit in mid-to-high double-digit growth markets (2024 forecasts) with Resonac leadership in epi design-wins; advanced packaging ~12% CAGR from 2024 and automotive content ~USD 550/vehicle (2024). EV battery materials remain high-growth after ~14m EVs sold in 2023; capex and R&D intensity are high to convert share into margin.

| Segment | Growth (CAGR) | Capex | Moat |

|---|---|---|---|

| SiC epi/wafers | mid-high double-digit | high | design-wins |

| CMP slurries | high | moderate-high | sticky quals |

| EV battery materials | high | >$1bn gigafactory | OEM quals |

What is included in the product

BCG review of Showa Denko’s portfolio, defining Stars, Cash Cows, Question Marks and Dogs with clear invest/hold/divest guidance.

One-page overview placing Showa Denko K.K. units in BCG quadrants for quick C-level clarity.

Cash Cows

Graphite electrodes (EAF steelmaking)

Graphite electrodes (EAF steelmaking): mature market where Showa Denko leverages established global share and deep operational know-how to serve steelmakers worldwide.

Demand is cyclical—US EAF penetration is about 70%—but over cycles electrodes generate strong free cash flow, especially when capacity utilization rises.

Incremental efficiency improvements outperform big promo spend; milk the business, maintain customer service, and stay disciplined on inventory levels.

HDD aluminum substrates

Flat to modest growth in 2024, with stable replacement and nearline demand sustaining volumes for Showa Denko K.K. HDD aluminum substrates. The company is one of the world’s largest aluminum substrate suppliers, holding high market share and meeting tight specs, enabling predictable cash generation. Limited incremental marketing is required given entrenched OEM relationships. Operational focus remains on yield improvement and cost control to preserve margins.

Aluminum rolled/extruded products (Japan-centric)

Aluminum rolled/extruded products are Showa Denko’s Japan-centric workhorse, serving entrenched transportation and industrial customers and generating steady cash flow in 2024. Not flashy but dependable, margin expansion has come from process improvements and energy-management programs that widened spreads versus 2023. Priority is to keep lines humming and avoid vanity capex to preserve free cash.

Inorganic ceramics/alumina for LEDs and industrials

Inorganic ceramics/alumina for LEDs and industrials sits in Showa Denko's cash cows: mature applications with sticky qualifications and repeat orders driving stable, positive cash flow and requiring modest R&D investment. Operational efficiency and uptime matter more than promotion, so focus is on optimizing asset loading and margin mix to sustain profitability. Volume-backed contracts and long qualification cycles protect margins and predictability.

- mature demand

- sticky qualifications

- repeat orders

- cash-flow positive

- modest R&D

- optimize asset loading

- margin mix focus

Basic petrochemical derivatives (selected)

Basic petrochemical derivatives are low-growth cash cows for Showa Denko, where integrated upstream positions and long-term contracts secure steady throughput and margin resilience despite limited pricing power.

Strict cost control and tight operating discipline convert steady volumes into reliable free cash flow; prioritize margin preservation over chasing incremental volume that erodes returns.

- Integrated supply chain: stabilizes feedstock access and throughput

- Contracted volumes: reduce demand volatility

- Pricing power: constrained vs. feedstock-linked peers

- Focus: maintain tight cost and utilization to maximize cash

Cyclic electrodes drive high FCF; aluminum steady; uptime keeps cash flowing

Graphite electrodes: mature, cyclical market (US EAF penetration ~70%) generating strong FCF at high utilization. Aluminum substrates: flat to modest 2024 growth, high share, predictable cash generation from OEM contracts. Petrochemicals/rolled aluminum/ceramics: low-growth, repeat orders, focus on uptime, cost control to preserve free cash.

| Business | 2024 trend | Cash profile |

|---|---|---|

| Graphite electrodes | Cyclical | High FCF |

| Aluminum substrates | Flat-modest growth | Stable cash |

| Petrochemicals/ceramics | Low growth | Reliable cash |

Full Transparency, Always

Showa Denko K.K. BCG Matrix

The Showa Denko K.K. BCG Matrix you’re previewing here is the exact file you’ll receive after purchase. No watermarks, no placeholders—just the finished, professionally formatted analysis ready to use. It’s built for immediate editing, printing, or dropping into investor decks. Once paid, the full document is delivered to your inbox with no surprises and no extra steps.

Download Your Competitive Advantage

Quick look at Showa Denko K.K.'s BCG Matrix shows where its chemicals, electronic materials and carbon products sit in the market—some are clear Stars, others edging toward Cash Cows or Question Marks. This preview maps the big moves, but the full BCG Matrix gives quadrant-by-quadrant data, strategic recommendations, and actionable next steps. Buy the full report to get a polished Word analysis plus an Excel summary you can use in board decks. Purchase now and skip the guesswork—get clarity fast.

Stars

SiC epitaxial wafers (power semiconductors)

SiC epitaxial wafers sit in a high-growth end market driven by EV inverters and industrial power drives, with industry forecasts in 2024 projecting mid-to-high double-digit CAGR for SiC device demand. Resonac (ex-Showa Denko), renamed in 2023, is a recognized leader in epi quality and capacity, securing design-wins with Tier‑1 device makers. The business soaks up capex today but scaling capacity now is the play to convert volume into long-term margin expansion.

CMP slurries & pads for advanced nodes

Wafer complexity keeps rising—more layers and denser metallization increase planarization demand, reinforcing CMP slurries & pads as a star business for Showa Denko. The unit holds strong share in critical slurry formulations with sticky qualifications that create high switching costs for customers. Growth is brisk while cash needs are heavy for R&D and customer support to defend specs. Strategy: stay on offense—invest in formulation wins and bundle services to lock in customers.

Specialty electronic gases (high purity)

Specialty electronic gases lead in select etch/clean chemistries for advanced logic and memory, directly tied to node shrinks and scaling; segment reports high-teens to low-double-digit growth rates industry-wide (CAGR >10%). High technical barriers and intensive QA/logistics create steep entry costs and recurring CAPEX; cash generated is reinvested into purification, distribution, and reliability. Scale and customer trust function as durable moats, supporting premium pricing and long-term contracts.

Semiconductor packaging materials (encapsulation, die-attach)

Advanced packaging demand is running hot in 2024 driven by chiplets, 2.5D/3D interposers and rising automotive reliability requirements; automotive semiconductor content averaged about USD 550 per vehicle in 2024, boosting need for robust encapsulation and die-attach. Showa Denko’s materials are entrenched with major OSATs and IDMs, and new formulations keep design windows open. The segment is growthy, lab-intensive and cash-hungry, so continued capex and R&D are required to convert design-ins into durable share.

- Market tailwinds: advanced packaging CAGR ~12% from 2024 (industry consensus)

- Competitive moat: long OEM/OSAT qualification cycles favor incumbents

- Cash profile: high R&D and pilot-line costs; reinvest to secure long-term share

EV battery materials (anodes/binders)

EV battery materials (anodes/binders) are Stars: Li-ion demand remains steep with global EV sales ~14 million in 2023 and battery supply needs accelerating; Hitachi Chemical heritage (integrated into Showa Denko since 2020) provides proven tech and customer ties. OEM and cell-maker qualifications (typically 12–24 months) create high switching costs; growth is strong but capex is heavy, with gigafactory investments often >$1bn. Push capacity where contracts are sticky and chemistries defensible.

- Demand tag: global EV sales ~14m (2023)

- Qualification tag: 12–24 months

- Capex tag: gigafactory >$1bn

- Strategy tag: focus on sticky contracts & defensible chemistries

SiC, CMP slurries and EV battery materials: high-growth, capex-heavy markets

Stars: SiC epi/wafers and CMP slurries sit in mid-to-high double-digit growth markets (2024 forecasts) with Resonac leadership in epi design-wins; advanced packaging ~12% CAGR from 2024 and automotive content ~USD 550/vehicle (2024). EV battery materials remain high-growth after ~14m EVs sold in 2023; capex and R&D intensity are high to convert share into margin.

| Segment | Growth (CAGR) | Capex | Moat |

|---|---|---|---|

| SiC epi/wafers | mid-high double-digit | high | design-wins |

| CMP slurries | high | moderate-high | sticky quals |

| EV battery materials | high | >$1bn gigafactory | OEM quals |

What is included in the product

BCG review of Showa Denko’s portfolio, defining Stars, Cash Cows, Question Marks and Dogs with clear invest/hold/divest guidance.

One-page overview placing Showa Denko K.K. units in BCG quadrants for quick C-level clarity.

Cash Cows

Graphite electrodes (EAF steelmaking)

Graphite electrodes (EAF steelmaking): mature market where Showa Denko leverages established global share and deep operational know-how to serve steelmakers worldwide.

Demand is cyclical—US EAF penetration is about 70%—but over cycles electrodes generate strong free cash flow, especially when capacity utilization rises.

Incremental efficiency improvements outperform big promo spend; milk the business, maintain customer service, and stay disciplined on inventory levels.

HDD aluminum substrates

Flat to modest growth in 2024, with stable replacement and nearline demand sustaining volumes for Showa Denko K.K. HDD aluminum substrates. The company is one of the world’s largest aluminum substrate suppliers, holding high market share and meeting tight specs, enabling predictable cash generation. Limited incremental marketing is required given entrenched OEM relationships. Operational focus remains on yield improvement and cost control to preserve margins.

Aluminum rolled/extruded products (Japan-centric)

Aluminum rolled/extruded products are Showa Denko’s Japan-centric workhorse, serving entrenched transportation and industrial customers and generating steady cash flow in 2024. Not flashy but dependable, margin expansion has come from process improvements and energy-management programs that widened spreads versus 2023. Priority is to keep lines humming and avoid vanity capex to preserve free cash.

Inorganic ceramics/alumina for LEDs and industrials

Inorganic ceramics/alumina for LEDs and industrials sits in Showa Denko's cash cows: mature applications with sticky qualifications and repeat orders driving stable, positive cash flow and requiring modest R&D investment. Operational efficiency and uptime matter more than promotion, so focus is on optimizing asset loading and margin mix to sustain profitability. Volume-backed contracts and long qualification cycles protect margins and predictability.

- mature demand

- sticky qualifications

- repeat orders

- cash-flow positive

- modest R&D

- optimize asset loading

- margin mix focus

Basic petrochemical derivatives (selected)

Basic petrochemical derivatives are low-growth cash cows for Showa Denko, where integrated upstream positions and long-term contracts secure steady throughput and margin resilience despite limited pricing power.

Strict cost control and tight operating discipline convert steady volumes into reliable free cash flow; prioritize margin preservation over chasing incremental volume that erodes returns.

- Integrated supply chain: stabilizes feedstock access and throughput

- Contracted volumes: reduce demand volatility

- Pricing power: constrained vs. feedstock-linked peers

- Focus: maintain tight cost and utilization to maximize cash

Cyclic electrodes drive high FCF; aluminum steady; uptime keeps cash flowing

Graphite electrodes: mature, cyclical market (US EAF penetration ~70%) generating strong FCF at high utilization. Aluminum substrates: flat to modest 2024 growth, high share, predictable cash generation from OEM contracts. Petrochemicals/rolled aluminum/ceramics: low-growth, repeat orders, focus on uptime, cost control to preserve free cash.

| Business | 2024 trend | Cash profile |

|---|---|---|

| Graphite electrodes | Cyclical | High FCF |

| Aluminum substrates | Flat-modest growth | Stable cash |

| Petrochemicals/ceramics | Low growth | Reliable cash |

Full Transparency, Always

Showa Denko K.K. BCG Matrix

The Showa Denko K.K. BCG Matrix you’re previewing here is the exact file you’ll receive after purchase. No watermarks, no placeholders—just the finished, professionally formatted analysis ready to use. It’s built for immediate editing, printing, or dropping into investor decks. Once paid, the full document is delivered to your inbox with no surprises and no extra steps.

Original: $10.00

-65%$10.00

$3.50Description

Download Your Competitive Advantage

Quick look at Showa Denko K.K.'s BCG Matrix shows where its chemicals, electronic materials and carbon products sit in the market—some are clear Stars, others edging toward Cash Cows or Question Marks. This preview maps the big moves, but the full BCG Matrix gives quadrant-by-quadrant data, strategic recommendations, and actionable next steps. Buy the full report to get a polished Word analysis plus an Excel summary you can use in board decks. Purchase now and skip the guesswork—get clarity fast.

Stars

SiC epitaxial wafers (power semiconductors)

SiC epitaxial wafers sit in a high-growth end market driven by EV inverters and industrial power drives, with industry forecasts in 2024 projecting mid-to-high double-digit CAGR for SiC device demand. Resonac (ex-Showa Denko), renamed in 2023, is a recognized leader in epi quality and capacity, securing design-wins with Tier‑1 device makers. The business soaks up capex today but scaling capacity now is the play to convert volume into long-term margin expansion.

CMP slurries & pads for advanced nodes

Wafer complexity keeps rising—more layers and denser metallization increase planarization demand, reinforcing CMP slurries & pads as a star business for Showa Denko. The unit holds strong share in critical slurry formulations with sticky qualifications that create high switching costs for customers. Growth is brisk while cash needs are heavy for R&D and customer support to defend specs. Strategy: stay on offense—invest in formulation wins and bundle services to lock in customers.

Specialty electronic gases (high purity)

Specialty electronic gases lead in select etch/clean chemistries for advanced logic and memory, directly tied to node shrinks and scaling; segment reports high-teens to low-double-digit growth rates industry-wide (CAGR >10%). High technical barriers and intensive QA/logistics create steep entry costs and recurring CAPEX; cash generated is reinvested into purification, distribution, and reliability. Scale and customer trust function as durable moats, supporting premium pricing and long-term contracts.

Semiconductor packaging materials (encapsulation, die-attach)

Advanced packaging demand is running hot in 2024 driven by chiplets, 2.5D/3D interposers and rising automotive reliability requirements; automotive semiconductor content averaged about USD 550 per vehicle in 2024, boosting need for robust encapsulation and die-attach. Showa Denko’s materials are entrenched with major OSATs and IDMs, and new formulations keep design windows open. The segment is growthy, lab-intensive and cash-hungry, so continued capex and R&D are required to convert design-ins into durable share.

- Market tailwinds: advanced packaging CAGR ~12% from 2024 (industry consensus)

- Competitive moat: long OEM/OSAT qualification cycles favor incumbents

- Cash profile: high R&D and pilot-line costs; reinvest to secure long-term share

EV battery materials (anodes/binders)

EV battery materials (anodes/binders) are Stars: Li-ion demand remains steep with global EV sales ~14 million in 2023 and battery supply needs accelerating; Hitachi Chemical heritage (integrated into Showa Denko since 2020) provides proven tech and customer ties. OEM and cell-maker qualifications (typically 12–24 months) create high switching costs; growth is strong but capex is heavy, with gigafactory investments often >$1bn. Push capacity where contracts are sticky and chemistries defensible.

- Demand tag: global EV sales ~14m (2023)

- Qualification tag: 12–24 months

- Capex tag: gigafactory >$1bn

- Strategy tag: focus on sticky contracts & defensible chemistries

SiC, CMP slurries and EV battery materials: high-growth, capex-heavy markets

Stars: SiC epi/wafers and CMP slurries sit in mid-to-high double-digit growth markets (2024 forecasts) with Resonac leadership in epi design-wins; advanced packaging ~12% CAGR from 2024 and automotive content ~USD 550/vehicle (2024). EV battery materials remain high-growth after ~14m EVs sold in 2023; capex and R&D intensity are high to convert share into margin.

| Segment | Growth (CAGR) | Capex | Moat |

|---|---|---|---|

| SiC epi/wafers | mid-high double-digit | high | design-wins |

| CMP slurries | high | moderate-high | sticky quals |

| EV battery materials | high | >$1bn gigafactory | OEM quals |

What is included in the product

BCG review of Showa Denko’s portfolio, defining Stars, Cash Cows, Question Marks and Dogs with clear invest/hold/divest guidance.

One-page overview placing Showa Denko K.K. units in BCG quadrants for quick C-level clarity.

Cash Cows

Graphite electrodes (EAF steelmaking)

Graphite electrodes (EAF steelmaking): mature market where Showa Denko leverages established global share and deep operational know-how to serve steelmakers worldwide.

Demand is cyclical—US EAF penetration is about 70%—but over cycles electrodes generate strong free cash flow, especially when capacity utilization rises.

Incremental efficiency improvements outperform big promo spend; milk the business, maintain customer service, and stay disciplined on inventory levels.

HDD aluminum substrates

Flat to modest growth in 2024, with stable replacement and nearline demand sustaining volumes for Showa Denko K.K. HDD aluminum substrates. The company is one of the world’s largest aluminum substrate suppliers, holding high market share and meeting tight specs, enabling predictable cash generation. Limited incremental marketing is required given entrenched OEM relationships. Operational focus remains on yield improvement and cost control to preserve margins.

Aluminum rolled/extruded products (Japan-centric)

Aluminum rolled/extruded products are Showa Denko’s Japan-centric workhorse, serving entrenched transportation and industrial customers and generating steady cash flow in 2024. Not flashy but dependable, margin expansion has come from process improvements and energy-management programs that widened spreads versus 2023. Priority is to keep lines humming and avoid vanity capex to preserve free cash.

Inorganic ceramics/alumina for LEDs and industrials

Inorganic ceramics/alumina for LEDs and industrials sits in Showa Denko's cash cows: mature applications with sticky qualifications and repeat orders driving stable, positive cash flow and requiring modest R&D investment. Operational efficiency and uptime matter more than promotion, so focus is on optimizing asset loading and margin mix to sustain profitability. Volume-backed contracts and long qualification cycles protect margins and predictability.

- mature demand

- sticky qualifications

- repeat orders

- cash-flow positive

- modest R&D

- optimize asset loading

- margin mix focus

Basic petrochemical derivatives (selected)

Basic petrochemical derivatives are low-growth cash cows for Showa Denko, where integrated upstream positions and long-term contracts secure steady throughput and margin resilience despite limited pricing power.

Strict cost control and tight operating discipline convert steady volumes into reliable free cash flow; prioritize margin preservation over chasing incremental volume that erodes returns.

- Integrated supply chain: stabilizes feedstock access and throughput

- Contracted volumes: reduce demand volatility

- Pricing power: constrained vs. feedstock-linked peers

- Focus: maintain tight cost and utilization to maximize cash

Cyclic electrodes drive high FCF; aluminum steady; uptime keeps cash flowing

Graphite electrodes: mature, cyclical market (US EAF penetration ~70%) generating strong FCF at high utilization. Aluminum substrates: flat to modest 2024 growth, high share, predictable cash generation from OEM contracts. Petrochemicals/rolled aluminum/ceramics: low-growth, repeat orders, focus on uptime, cost control to preserve free cash.

| Business | 2024 trend | Cash profile |

|---|---|---|

| Graphite electrodes | Cyclical | High FCF |

| Aluminum substrates | Flat-modest growth | Stable cash |

| Petrochemicals/ceramics | Low growth | Reliable cash |

Full Transparency, Always

Showa Denko K.K. BCG Matrix

The Showa Denko K.K. BCG Matrix you’re previewing here is the exact file you’ll receive after purchase. No watermarks, no placeholders—just the finished, professionally formatted analysis ready to use. It’s built for immediate editing, printing, or dropping into investor decks. Once paid, the full document is delivered to your inbox with no surprises and no extra steps.