Seaboard Porter's Five Forces Analysis

From Overview to Strategy Blueprint

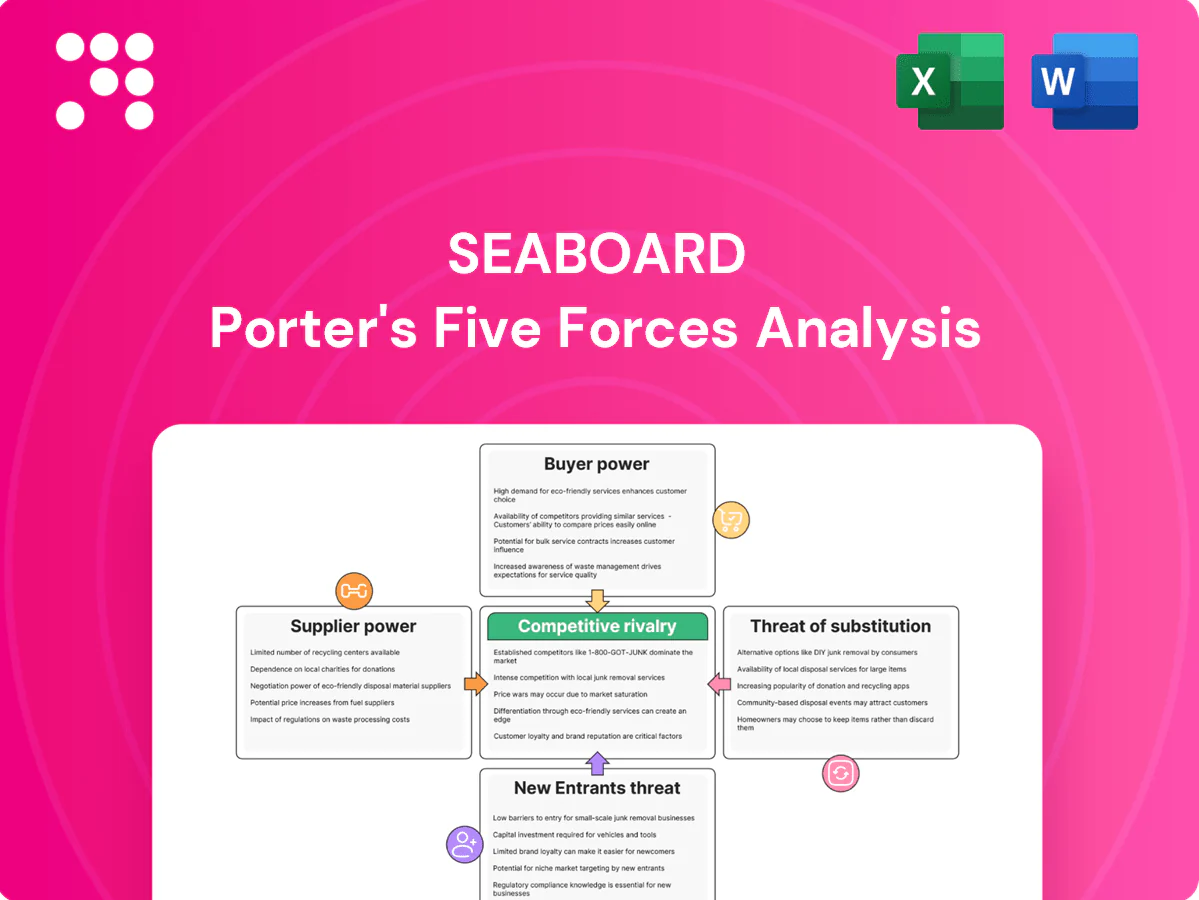

Seaboard faces moderate supplier power, cyclical buyer demand, and material substitution risks across its agribusiness and shipping units, while scale and regulatory barriers limit new entrants and rivalry varies by segment. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Concentrated feed and livestock inputs

Seaboard relies heavily on corn, soybean meal and specialized pork genetics sourced from concentrated suppliers; feed accounts for about 60% of hog production costs (USDA ERS 2024). US average corn was roughly $6/bu and soybean meal near $400/ton in 2024, so commodity volatility can spike input costs faster than pass-through. Long-term contracts and hedging reduce but do not remove exposure, while biosecurity constraints and proprietary genetics limit easy supplier switching.

Fuel and marine services dependence

Ocean transport depends on bunker fuel, lubricants and port services concentrated at hubs like Singapore and Rotterdam, letting suppliers levy fees, surcharges or limit availability. Suppliers at key ports can extract rent through port dues and bunkering premiums; the EU extended its Emissions Trading System to shipping in 2024, adding compliance costs. Multi-port optionality reduces but does not eliminate switching due to fixed route networks and slot schedules.

Equipment OEMs and maintenance parts

Processing plants, mills and ships rely on proprietary equipment and parts from a few OEMs; 2024 industry reports show the top three suppliers control over 60% of the critical-components market. Lead times often exceed 12 weeks and technical lock-in creates high switching costs, while planned maintenance windows elevate supplier leverage. Framework agreements reduce price spikes but do not eliminate dependence on OEMs for spares and upgrades.

Agri smallholders and origin concentration

In developing markets, grain and sugarcane supply is often fragmented yet seasonally tight and regionally concentrated, so weather, logistics, and political disruptions can shift bargaining power to local aggregators and cooperatives.

Seaboard’s multi-origin sourcing and logistics footprint helps balance that volatility, reducing single-origin exposure; however, sudden export restrictions in 2022–24 episodes showed supplier leverage can spike quickly.

- Fragmentation increases local aggregator power

- Seasonal tightness amplifies price volatility

- Origin diversification mitigates single-source risk

- Export bans can rapidly elevate supplier leverage

Skilled labor and compliance services

Veterinary, food-safety, maritime crew and compliance specialists act as critical suppliers; tight labor markets (US unemployment averaged 3.7% in 2024) and certification needs (FSMA, STCW) boost their bargaining power, while targeted training and retention programs partially offset wage pressure; regulatory updates can quickly raise specialized-service costs.

- Suppliers: veterinary, food safety, maritime, compliance

- Labor tightness: US unemployment 3.7% (2024)

- Certifications: FSMA, STCW raise entry barriers

- Mitigation: training/retention programs

Pork producer faces higher input and shipping costs from feed, OEMs, and labor tightness

Seaboard faces elevated supplier power as feed (≈60% of hog cost) and proprietary genetics concentrate inputs, with 2024 corn ≈$6/bu and soybean meal ≈$400/ton increasing pass-through risk. Maritime and port services plus 2024 ETS shipping rules add compliance and bunker cost pressure, while top-3 OEMs control ~60% of critical components. Labor tightness (US unemployment 3.7% in 2024) raises specialized-service costs.

| Metric | 2024 value | Implication |

|---|---|---|

| Feed share | 60% | High input leverage |

| Corn | $6/bu | Commodity volatility |

| Soymeal | $400/ton | Cost spikes |

| OEM conc. | ~60% | Switching costs |

| Unemp. | 3.7% | Wage pressure |

What is included in the product

Tailored exclusively for Seaboard, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, and substitute threats affecting pricing and profitability. It identifies barriers deterring entrants and highlights disruptive forces and strategic levers to protect and strengthen Seaboard's market position.

A concise Seaboard Porter’s Five Forces one-sheet that highlights competitive pain points and relief strategies, with customizable pressure sliders and an instant radar chart—ready to drop into pitch decks, Excel dashboards, or boardroom reports.

Customers Bargaining Power

Consolidated retail and foodservice

Consolidated retailers and foodservice buyers concentrate purchasing power in pork and processed foods, with Walmart holding about 25% of US grocery sales in 2024 and the top chains capturing roughly 40% of market volume. They demand sharp pricing, consistent specs and private-label options (private label penetration ~18% in 2024), while slotting and marketing allowances squeeze margins and losing a major account can materially cut volumes.

Commodity traders and industrial buyers

Commodity traders and industrial buyers benchmark purchases to transparent indices such as CBOT and ICE, with 2024 average CBOT corn near $5.60/bu and ICE raw sugar around 20.4¢/lb, limiting Seaboard pricing discretion. Competitive tendering and auctions intensify buyer leverage, pressuring margins. Forward contracts secure volumes but lock in margins, while strict quality specs and delivery windows trigger penalties for variance.

Freight shippers with route alternatives

In regional ocean lanes shippers with route alternatives exert strong price and schedule comparison power; spot rates fell about 75% from 2022 peaks by 2024, lifting rate pressure when capacity loosens. Service differentiation and integrated port-to-door logistics reduce buyer leverage by adding switching costs, while long-term contracts—covering roughly 70% of volumes in many trades—temper but do not erase spot-market influence.

Power offtakers and PPAs

Utilities and governments procure generation largely via PPAs with strict performance, availability and liquidated-damage clauses, giving buyers leverage to push price and risk back to developers. Tender-based procurement and standardized contracts intensify buyer bargaining, while creditworthiness and regulatory oversight can cause multi-month payment and commissioning delays. Indexation clauses to fuel or market prices are common but are hotly negotiated to shift volatility.

- Buyer leverage: strict performance clauses

- Tenders: compress margins, shift risk

- Payments: delays from credit/regulation

- Indexation: mitigates fuel risk, negotiated hard

Certification and ESG demands

- Compliance cost: higher

- Supplier pool: narrowed

- Premium access vs margin pressure

- Non-compliance: delisting risk

Major buyer concentration, private-label growth and commodity pricing compress margins

Large retailers (Walmart ~25% US grocery sales in 2024) and foodservice buyers concentrate purchase power, pushing for low prices, private-label (~18% penetration 2024) and strict specs that compress margins. Commodity-indexed buyers (CBOT corn ~$5.60/bu, ICE sugar ~20.4¢/lb in 2024) limit pricing freedom; spot shipping rates fell ~75% from 2022 peaks by 2024. Long-term contracts (~70% of volumes in many lanes) and sustainability rules (EU CSRD 2024) moderate but do not remove buyer leverage.

| Metric | 2024 Value |

|---|---|

| Walmart share | ~25% |

| Private label | ~18% |

| CBOT corn | $5.60/bu |

| Spot rate decline | ~75% vs 2022 |

Preview Before You Purchase

Seaboard Porter's Five Forces Analysis

This preview shows the exact Seaboard Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is exactly what you’ll get.

From Overview to Strategy Blueprint

Seaboard faces moderate supplier power, cyclical buyer demand, and material substitution risks across its agribusiness and shipping units, while scale and regulatory barriers limit new entrants and rivalry varies by segment. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Concentrated feed and livestock inputs

Seaboard relies heavily on corn, soybean meal and specialized pork genetics sourced from concentrated suppliers; feed accounts for about 60% of hog production costs (USDA ERS 2024). US average corn was roughly $6/bu and soybean meal near $400/ton in 2024, so commodity volatility can spike input costs faster than pass-through. Long-term contracts and hedging reduce but do not remove exposure, while biosecurity constraints and proprietary genetics limit easy supplier switching.

Fuel and marine services dependence

Ocean transport depends on bunker fuel, lubricants and port services concentrated at hubs like Singapore and Rotterdam, letting suppliers levy fees, surcharges or limit availability. Suppliers at key ports can extract rent through port dues and bunkering premiums; the EU extended its Emissions Trading System to shipping in 2024, adding compliance costs. Multi-port optionality reduces but does not eliminate switching due to fixed route networks and slot schedules.

Equipment OEMs and maintenance parts

Processing plants, mills and ships rely on proprietary equipment and parts from a few OEMs; 2024 industry reports show the top three suppliers control over 60% of the critical-components market. Lead times often exceed 12 weeks and technical lock-in creates high switching costs, while planned maintenance windows elevate supplier leverage. Framework agreements reduce price spikes but do not eliminate dependence on OEMs for spares and upgrades.

Agri smallholders and origin concentration

In developing markets, grain and sugarcane supply is often fragmented yet seasonally tight and regionally concentrated, so weather, logistics, and political disruptions can shift bargaining power to local aggregators and cooperatives.

Seaboard’s multi-origin sourcing and logistics footprint helps balance that volatility, reducing single-origin exposure; however, sudden export restrictions in 2022–24 episodes showed supplier leverage can spike quickly.

- Fragmentation increases local aggregator power

- Seasonal tightness amplifies price volatility

- Origin diversification mitigates single-source risk

- Export bans can rapidly elevate supplier leverage

Skilled labor and compliance services

Veterinary, food-safety, maritime crew and compliance specialists act as critical suppliers; tight labor markets (US unemployment averaged 3.7% in 2024) and certification needs (FSMA, STCW) boost their bargaining power, while targeted training and retention programs partially offset wage pressure; regulatory updates can quickly raise specialized-service costs.

- Suppliers: veterinary, food safety, maritime, compliance

- Labor tightness: US unemployment 3.7% (2024)

- Certifications: FSMA, STCW raise entry barriers

- Mitigation: training/retention programs

Pork producer faces higher input and shipping costs from feed, OEMs, and labor tightness

Seaboard faces elevated supplier power as feed (≈60% of hog cost) and proprietary genetics concentrate inputs, with 2024 corn ≈$6/bu and soybean meal ≈$400/ton increasing pass-through risk. Maritime and port services plus 2024 ETS shipping rules add compliance and bunker cost pressure, while top-3 OEMs control ~60% of critical components. Labor tightness (US unemployment 3.7% in 2024) raises specialized-service costs.

| Metric | 2024 value | Implication |

|---|---|---|

| Feed share | 60% | High input leverage |

| Corn | $6/bu | Commodity volatility |

| Soymeal | $400/ton | Cost spikes |

| OEM conc. | ~60% | Switching costs |

| Unemp. | 3.7% | Wage pressure |

What is included in the product

Tailored exclusively for Seaboard, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, and substitute threats affecting pricing and profitability. It identifies barriers deterring entrants and highlights disruptive forces and strategic levers to protect and strengthen Seaboard's market position.

A concise Seaboard Porter’s Five Forces one-sheet that highlights competitive pain points and relief strategies, with customizable pressure sliders and an instant radar chart—ready to drop into pitch decks, Excel dashboards, or boardroom reports.

Customers Bargaining Power

Consolidated retail and foodservice

Consolidated retailers and foodservice buyers concentrate purchasing power in pork and processed foods, with Walmart holding about 25% of US grocery sales in 2024 and the top chains capturing roughly 40% of market volume. They demand sharp pricing, consistent specs and private-label options (private label penetration ~18% in 2024), while slotting and marketing allowances squeeze margins and losing a major account can materially cut volumes.

Commodity traders and industrial buyers

Commodity traders and industrial buyers benchmark purchases to transparent indices such as CBOT and ICE, with 2024 average CBOT corn near $5.60/bu and ICE raw sugar around 20.4¢/lb, limiting Seaboard pricing discretion. Competitive tendering and auctions intensify buyer leverage, pressuring margins. Forward contracts secure volumes but lock in margins, while strict quality specs and delivery windows trigger penalties for variance.

Freight shippers with route alternatives

In regional ocean lanes shippers with route alternatives exert strong price and schedule comparison power; spot rates fell about 75% from 2022 peaks by 2024, lifting rate pressure when capacity loosens. Service differentiation and integrated port-to-door logistics reduce buyer leverage by adding switching costs, while long-term contracts—covering roughly 70% of volumes in many trades—temper but do not erase spot-market influence.

Power offtakers and PPAs

Utilities and governments procure generation largely via PPAs with strict performance, availability and liquidated-damage clauses, giving buyers leverage to push price and risk back to developers. Tender-based procurement and standardized contracts intensify buyer bargaining, while creditworthiness and regulatory oversight can cause multi-month payment and commissioning delays. Indexation clauses to fuel or market prices are common but are hotly negotiated to shift volatility.

- Buyer leverage: strict performance clauses

- Tenders: compress margins, shift risk

- Payments: delays from credit/regulation

- Indexation: mitigates fuel risk, negotiated hard

Certification and ESG demands

- Compliance cost: higher

- Supplier pool: narrowed

- Premium access vs margin pressure

- Non-compliance: delisting risk

Major buyer concentration, private-label growth and commodity pricing compress margins

Large retailers (Walmart ~25% US grocery sales in 2024) and foodservice buyers concentrate purchase power, pushing for low prices, private-label (~18% penetration 2024) and strict specs that compress margins. Commodity-indexed buyers (CBOT corn ~$5.60/bu, ICE sugar ~20.4¢/lb in 2024) limit pricing freedom; spot shipping rates fell ~75% from 2022 peaks by 2024. Long-term contracts (~70% of volumes in many lanes) and sustainability rules (EU CSRD 2024) moderate but do not remove buyer leverage.

| Metric | 2024 Value |

|---|---|

| Walmart share | ~25% |

| Private label | ~18% |

| CBOT corn | $5.60/bu |

| Spot rate decline | ~75% vs 2022 |

Preview Before You Purchase

Seaboard Porter's Five Forces Analysis

This preview shows the exact Seaboard Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is exactly what you’ll get.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Seaboard faces moderate supplier power, cyclical buyer demand, and material substitution risks across its agribusiness and shipping units, while scale and regulatory barriers limit new entrants and rivalry varies by segment. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Concentrated feed and livestock inputs

Seaboard relies heavily on corn, soybean meal and specialized pork genetics sourced from concentrated suppliers; feed accounts for about 60% of hog production costs (USDA ERS 2024). US average corn was roughly $6/bu and soybean meal near $400/ton in 2024, so commodity volatility can spike input costs faster than pass-through. Long-term contracts and hedging reduce but do not remove exposure, while biosecurity constraints and proprietary genetics limit easy supplier switching.

Fuel and marine services dependence

Ocean transport depends on bunker fuel, lubricants and port services concentrated at hubs like Singapore and Rotterdam, letting suppliers levy fees, surcharges or limit availability. Suppliers at key ports can extract rent through port dues and bunkering premiums; the EU extended its Emissions Trading System to shipping in 2024, adding compliance costs. Multi-port optionality reduces but does not eliminate switching due to fixed route networks and slot schedules.

Equipment OEMs and maintenance parts

Processing plants, mills and ships rely on proprietary equipment and parts from a few OEMs; 2024 industry reports show the top three suppliers control over 60% of the critical-components market. Lead times often exceed 12 weeks and technical lock-in creates high switching costs, while planned maintenance windows elevate supplier leverage. Framework agreements reduce price spikes but do not eliminate dependence on OEMs for spares and upgrades.

Agri smallholders and origin concentration

In developing markets, grain and sugarcane supply is often fragmented yet seasonally tight and regionally concentrated, so weather, logistics, and political disruptions can shift bargaining power to local aggregators and cooperatives.

Seaboard’s multi-origin sourcing and logistics footprint helps balance that volatility, reducing single-origin exposure; however, sudden export restrictions in 2022–24 episodes showed supplier leverage can spike quickly.

- Fragmentation increases local aggregator power

- Seasonal tightness amplifies price volatility

- Origin diversification mitigates single-source risk

- Export bans can rapidly elevate supplier leverage

Skilled labor and compliance services

Veterinary, food-safety, maritime crew and compliance specialists act as critical suppliers; tight labor markets (US unemployment averaged 3.7% in 2024) and certification needs (FSMA, STCW) boost their bargaining power, while targeted training and retention programs partially offset wage pressure; regulatory updates can quickly raise specialized-service costs.

- Suppliers: veterinary, food safety, maritime, compliance

- Labor tightness: US unemployment 3.7% (2024)

- Certifications: FSMA, STCW raise entry barriers

- Mitigation: training/retention programs

Pork producer faces higher input and shipping costs from feed, OEMs, and labor tightness

Seaboard faces elevated supplier power as feed (≈60% of hog cost) and proprietary genetics concentrate inputs, with 2024 corn ≈$6/bu and soybean meal ≈$400/ton increasing pass-through risk. Maritime and port services plus 2024 ETS shipping rules add compliance and bunker cost pressure, while top-3 OEMs control ~60% of critical components. Labor tightness (US unemployment 3.7% in 2024) raises specialized-service costs.

| Metric | 2024 value | Implication |

|---|---|---|

| Feed share | 60% | High input leverage |

| Corn | $6/bu | Commodity volatility |

| Soymeal | $400/ton | Cost spikes |

| OEM conc. | ~60% | Switching costs |

| Unemp. | 3.7% | Wage pressure |

What is included in the product

Tailored exclusively for Seaboard, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, and substitute threats affecting pricing and profitability. It identifies barriers deterring entrants and highlights disruptive forces and strategic levers to protect and strengthen Seaboard's market position.

A concise Seaboard Porter’s Five Forces one-sheet that highlights competitive pain points and relief strategies, with customizable pressure sliders and an instant radar chart—ready to drop into pitch decks, Excel dashboards, or boardroom reports.

Customers Bargaining Power

Consolidated retail and foodservice

Consolidated retailers and foodservice buyers concentrate purchasing power in pork and processed foods, with Walmart holding about 25% of US grocery sales in 2024 and the top chains capturing roughly 40% of market volume. They demand sharp pricing, consistent specs and private-label options (private label penetration ~18% in 2024), while slotting and marketing allowances squeeze margins and losing a major account can materially cut volumes.

Commodity traders and industrial buyers

Commodity traders and industrial buyers benchmark purchases to transparent indices such as CBOT and ICE, with 2024 average CBOT corn near $5.60/bu and ICE raw sugar around 20.4¢/lb, limiting Seaboard pricing discretion. Competitive tendering and auctions intensify buyer leverage, pressuring margins. Forward contracts secure volumes but lock in margins, while strict quality specs and delivery windows trigger penalties for variance.

Freight shippers with route alternatives

In regional ocean lanes shippers with route alternatives exert strong price and schedule comparison power; spot rates fell about 75% from 2022 peaks by 2024, lifting rate pressure when capacity loosens. Service differentiation and integrated port-to-door logistics reduce buyer leverage by adding switching costs, while long-term contracts—covering roughly 70% of volumes in many trades—temper but do not erase spot-market influence.

Power offtakers and PPAs

Utilities and governments procure generation largely via PPAs with strict performance, availability and liquidated-damage clauses, giving buyers leverage to push price and risk back to developers. Tender-based procurement and standardized contracts intensify buyer bargaining, while creditworthiness and regulatory oversight can cause multi-month payment and commissioning delays. Indexation clauses to fuel or market prices are common but are hotly negotiated to shift volatility.

- Buyer leverage: strict performance clauses

- Tenders: compress margins, shift risk

- Payments: delays from credit/regulation

- Indexation: mitigates fuel risk, negotiated hard

Certification and ESG demands

- Compliance cost: higher

- Supplier pool: narrowed

- Premium access vs margin pressure

- Non-compliance: delisting risk

Major buyer concentration, private-label growth and commodity pricing compress margins

Large retailers (Walmart ~25% US grocery sales in 2024) and foodservice buyers concentrate purchase power, pushing for low prices, private-label (~18% penetration 2024) and strict specs that compress margins. Commodity-indexed buyers (CBOT corn ~$5.60/bu, ICE sugar ~20.4¢/lb in 2024) limit pricing freedom; spot shipping rates fell ~75% from 2022 peaks by 2024. Long-term contracts (~70% of volumes in many lanes) and sustainability rules (EU CSRD 2024) moderate but do not remove buyer leverage.

| Metric | 2024 Value |

|---|---|

| Walmart share | ~25% |

| Private label | ~18% |

| CBOT corn | $5.60/bu |

| Spot rate decline | ~75% vs 2022 |

Preview Before You Purchase

Seaboard Porter's Five Forces Analysis

This preview shows the exact Seaboard Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is exactly what you’ll get.