Sealed Air PESTLE Analysis

Your Shortcut to Market Insight Starts Here

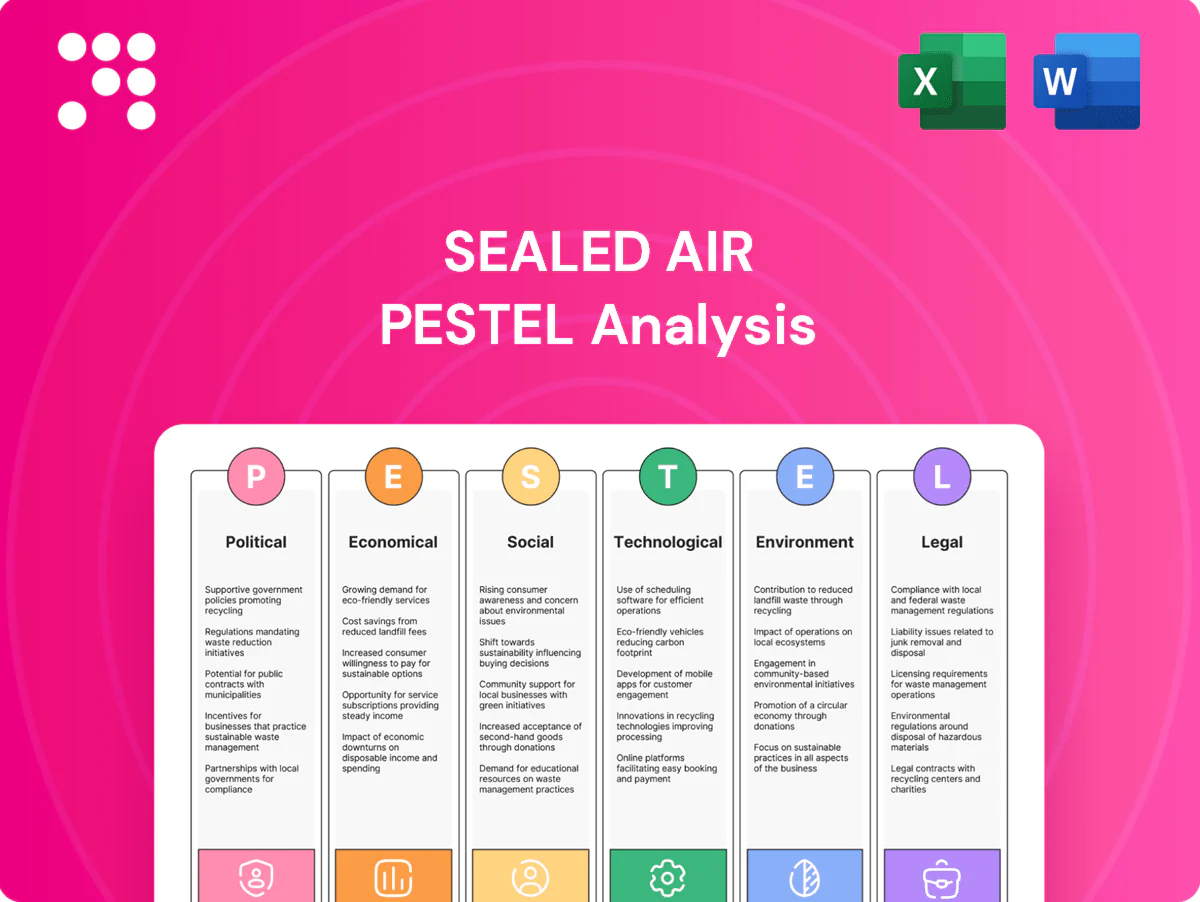

Unlock strategic advantage with our PESTLE Analysis of Sealed Air—three concise sections reveal how political shifts, economic pressures, and environmental trends reshape its outlook. Ideal for investors and strategists, this report is ready to use. Purchase the full analysis for the detailed insights you need now.

Political factors

Trade policies and tariffs

Global packaging supply chains remain exposed to tariff shifts and non-tariff barriers, highlighted by US tariffs since 2018 covering roughly $370 billion of Chinese goods, which can quickly alter input costs and pricing power for Sealed Air.

Changes in US–China and EU trade relations can compress margins, so Sealed Air must diversify sourcing and adjust transfer pricing to mitigate volatility.

Proactive lobbying and scenario planning preserve margins amid policy uncertainty.

Food security and public health priorities

Governments prioritise food safety, driving demand for hygienic, shelf‑life‑extending packaging as WHO reports 600 million foodborne illnesses annually. Public funding and standards accelerate adoption of advanced materials amid FAO estimates of 1.3 billion tonnes of food lost annually. Policy emphasis on cold chain integrity aligns with Sealed Air’s offerings and can unlock national procurement channels.

Industrial policy and reshoring incentives

Industrial policy and reshoring incentives reshape Sealed Airs plant footprint and capex timing as the Inflation Reduction Act earmarks roughly 369 billion USD for clean-energy and manufacturing support through the 2020s, lowering energy and production unit costs via tax credits and grants. Reshoring improves service levels and lead times but requires development of localized supplier networks and higher working-capital to regionalize. Balancing these incentives against logistics cost and efficiency is essential.

Geopolitical instability and logistics risk

Geopolitical conflicts and sanctions since 2022 have disrupted resin and chemical flows and constrained shipping lanes, increasing supply risk for Sealed Air. Freight rerouting has lengthened lead times and pushed up working capital needs. Multiregion inventory buffers, dual-sourcing, insurance and hedging become critical risk mitigants.

- Resin/chemical flow disruption

- Higher lead times & working capital

- Multiregion buffers & dual-sourcing

- Insurance & hedging essential

Government sustainability agendas

Tariffs, food-safety pressure and recycling targets reshape packaging margins and capex

Tariff shifts (US tariffs since 2018 on ≈$370bn of Chinese goods) and US–China/EU tensions can raise input costs and compress margins for Sealed Air.

Food-safety policy drives demand—WHO: 600m foodborne illnesses/yr; FAO: 1.3bn t food loss—favoring shelf‑life solutions.

Industrial policy/IRA (~$369bn) and reshoring incentives alter capex and localization needs.

EU recyclability target 2030 and 65% municipal recycling by 2035 force portfolio shifts to recyclable/recycled content.

| Metric | Value |

|---|---|

| US tariffs (since 2018) | $370bn |

| WHO foodborne illnesses | 600m/yr |

| FAO food loss | 1.3bn t/yr |

| IRA manufacturing funds | $369bn |

| EU recyclable target | 2030 |

What is included in the product

Explores how macro-environmental forces uniquely affect the Sealed Air across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk management, and investor communications.

A concise, visually segmented Sealed Air PESTLE summary that relieves meeting prep pain by highlighting key external risks and opportunities for quick drop‑in to presentations, team alignment, or consultant reports.

Economic factors

Resin and energy price volatility

Polymer feedstocks and utilities are a large share of Sealed Air's COGS, and industry data show North American polyethylene prices dropped roughly 35% from 2022 to 2023 (IHS Markit), illustrating volatility that can swing margins sharply.

Price spikes compress margins unless pass-throughs work; hedging and long-term resin/energy contracts stabilize costs but cap upside, while process efficiency and lightweighting reduce sensitivity to these cycles.

Consumer demand and e-commerce growth

Rising e-commerce — ~22% of global retail sales in 2024 — amplifies demand elasticity for protective packaging as volumes and return rates fluctuate. Macroeconomic slowdowns trimmed global parcel volumes ~3% in 2023–24, compressing shipping activity and shifting SKU mixes toward smaller, cost-sensitive items. Value-engineered solutions help defend volumes in downcycles, while omnichannel logistics growth drives demand for automation-ready packaging systems to cut labor and speed fulfilment.

Food inflation and retailer pressure

Retailers facing 2024 food-at-home inflation of roughly 5.6% (BLS) increasingly push suppliers for cost containment, heightening margin pressure on packaged-food customers. Packaging that reduces shrink and extends shelf life—reducing waste by 10–20% in retailer pilots—helps offset price pressure by protecting sell-through. ROI-proven Sealed Air solutions shift conversations from unit cost to total value, and joint business planning with major grocers can lock in category share through co-funded trials and guaranteed replenishment programs.

Currency fluctuations

Sealed Air faces material FX risk as multicurrency revenues and costs expose reported results to exchange-rate swings, especially between USD, EUR and emerging-market currencies.

Local production and sourcing provide natural hedges that reduce translation risk, while dynamic pricing, surcharges and contract clauses are used to pass through cost changes.

Treasury centralization focuses on cash repatriation, netting and currency-denominated debt to optimize debt servicing and liquidity.

- FX exposure: multicurrency revenues vs costs

- Natural hedging: local production reduces translation risk

- Pricing tools: surcharges and indexation manage volatility

- Treasury: cash netting, repatriation, currency debt

Capex cycles and automation spend

Customers ramp up packaging equipment buys during expansion phases, but higher borrowing costs in 2023–24 slowed automation projects and extended sales cycles; the global industrial automation market reached about $230 billion in 2024, highlighting persistent demand. Rising labor costs have shortened payback periods for automation investments, and flexible financing options help sustain equipment adoption through downturns.

- Capex sensitivity: higher rates lengthen sales cycles

- Payback improvement: rising labor costs favor automation

- Finance role: flexible terms sustain adoption through cycles

Tariffs, food-safety pressure and recycling targets reshape packaging margins and capex

Polymer feedstock volatility (NA polyethylene down ~35% 2022–23) and rising inputs drive margin swings; hedging, long-term contracts and lightweighting mitigate impact. E-commerce ~22% of global retail sales (2024) and a ~$230B automation market (2024) push demand for protective, automation-ready packaging. Food-at-home inflation ~5.6% (2024) and FX exposure increase pricing and cash-management pressure.

Preview Before You Purchase

Sealed Air PESTLE Analysis

The preview shown here is the exact Sealed Air PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. What you see in this preview is the final file delivered upon checkout with no placeholders or surprises. Download instantly and apply the analysis immediately.

Your Shortcut to Market Insight Starts Here

Unlock strategic advantage with our PESTLE Analysis of Sealed Air—three concise sections reveal how political shifts, economic pressures, and environmental trends reshape its outlook. Ideal for investors and strategists, this report is ready to use. Purchase the full analysis for the detailed insights you need now.

Political factors

Trade policies and tariffs

Global packaging supply chains remain exposed to tariff shifts and non-tariff barriers, highlighted by US tariffs since 2018 covering roughly $370 billion of Chinese goods, which can quickly alter input costs and pricing power for Sealed Air.

Changes in US–China and EU trade relations can compress margins, so Sealed Air must diversify sourcing and adjust transfer pricing to mitigate volatility.

Proactive lobbying and scenario planning preserve margins amid policy uncertainty.

Food security and public health priorities

Governments prioritise food safety, driving demand for hygienic, shelf‑life‑extending packaging as WHO reports 600 million foodborne illnesses annually. Public funding and standards accelerate adoption of advanced materials amid FAO estimates of 1.3 billion tonnes of food lost annually. Policy emphasis on cold chain integrity aligns with Sealed Air’s offerings and can unlock national procurement channels.

Industrial policy and reshoring incentives

Industrial policy and reshoring incentives reshape Sealed Airs plant footprint and capex timing as the Inflation Reduction Act earmarks roughly 369 billion USD for clean-energy and manufacturing support through the 2020s, lowering energy and production unit costs via tax credits and grants. Reshoring improves service levels and lead times but requires development of localized supplier networks and higher working-capital to regionalize. Balancing these incentives against logistics cost and efficiency is essential.

Geopolitical instability and logistics risk

Geopolitical conflicts and sanctions since 2022 have disrupted resin and chemical flows and constrained shipping lanes, increasing supply risk for Sealed Air. Freight rerouting has lengthened lead times and pushed up working capital needs. Multiregion inventory buffers, dual-sourcing, insurance and hedging become critical risk mitigants.

- Resin/chemical flow disruption

- Higher lead times & working capital

- Multiregion buffers & dual-sourcing

- Insurance & hedging essential

Government sustainability agendas

Tariffs, food-safety pressure and recycling targets reshape packaging margins and capex

Tariff shifts (US tariffs since 2018 on ≈$370bn of Chinese goods) and US–China/EU tensions can raise input costs and compress margins for Sealed Air.

Food-safety policy drives demand—WHO: 600m foodborne illnesses/yr; FAO: 1.3bn t food loss—favoring shelf‑life solutions.

Industrial policy/IRA (~$369bn) and reshoring incentives alter capex and localization needs.

EU recyclability target 2030 and 65% municipal recycling by 2035 force portfolio shifts to recyclable/recycled content.

| Metric | Value |

|---|---|

| US tariffs (since 2018) | $370bn |

| WHO foodborne illnesses | 600m/yr |

| FAO food loss | 1.3bn t/yr |

| IRA manufacturing funds | $369bn |

| EU recyclable target | 2030 |

What is included in the product

Explores how macro-environmental forces uniquely affect the Sealed Air across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk management, and investor communications.

A concise, visually segmented Sealed Air PESTLE summary that relieves meeting prep pain by highlighting key external risks and opportunities for quick drop‑in to presentations, team alignment, or consultant reports.

Economic factors

Resin and energy price volatility

Polymer feedstocks and utilities are a large share of Sealed Air's COGS, and industry data show North American polyethylene prices dropped roughly 35% from 2022 to 2023 (IHS Markit), illustrating volatility that can swing margins sharply.

Price spikes compress margins unless pass-throughs work; hedging and long-term resin/energy contracts stabilize costs but cap upside, while process efficiency and lightweighting reduce sensitivity to these cycles.

Consumer demand and e-commerce growth

Rising e-commerce — ~22% of global retail sales in 2024 — amplifies demand elasticity for protective packaging as volumes and return rates fluctuate. Macroeconomic slowdowns trimmed global parcel volumes ~3% in 2023–24, compressing shipping activity and shifting SKU mixes toward smaller, cost-sensitive items. Value-engineered solutions help defend volumes in downcycles, while omnichannel logistics growth drives demand for automation-ready packaging systems to cut labor and speed fulfilment.

Food inflation and retailer pressure

Retailers facing 2024 food-at-home inflation of roughly 5.6% (BLS) increasingly push suppliers for cost containment, heightening margin pressure on packaged-food customers. Packaging that reduces shrink and extends shelf life—reducing waste by 10–20% in retailer pilots—helps offset price pressure by protecting sell-through. ROI-proven Sealed Air solutions shift conversations from unit cost to total value, and joint business planning with major grocers can lock in category share through co-funded trials and guaranteed replenishment programs.

Currency fluctuations

Sealed Air faces material FX risk as multicurrency revenues and costs expose reported results to exchange-rate swings, especially between USD, EUR and emerging-market currencies.

Local production and sourcing provide natural hedges that reduce translation risk, while dynamic pricing, surcharges and contract clauses are used to pass through cost changes.

Treasury centralization focuses on cash repatriation, netting and currency-denominated debt to optimize debt servicing and liquidity.

- FX exposure: multicurrency revenues vs costs

- Natural hedging: local production reduces translation risk

- Pricing tools: surcharges and indexation manage volatility

- Treasury: cash netting, repatriation, currency debt

Capex cycles and automation spend

Customers ramp up packaging equipment buys during expansion phases, but higher borrowing costs in 2023–24 slowed automation projects and extended sales cycles; the global industrial automation market reached about $230 billion in 2024, highlighting persistent demand. Rising labor costs have shortened payback periods for automation investments, and flexible financing options help sustain equipment adoption through downturns.

- Capex sensitivity: higher rates lengthen sales cycles

- Payback improvement: rising labor costs favor automation

- Finance role: flexible terms sustain adoption through cycles

Tariffs, food-safety pressure and recycling targets reshape packaging margins and capex

Polymer feedstock volatility (NA polyethylene down ~35% 2022–23) and rising inputs drive margin swings; hedging, long-term contracts and lightweighting mitigate impact. E-commerce ~22% of global retail sales (2024) and a ~$230B automation market (2024) push demand for protective, automation-ready packaging. Food-at-home inflation ~5.6% (2024) and FX exposure increase pricing and cash-management pressure.

Preview Before You Purchase

Sealed Air PESTLE Analysis

The preview shown here is the exact Sealed Air PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. What you see in this preview is the final file delivered upon checkout with no placeholders or surprises. Download instantly and apply the analysis immediately.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Unlock strategic advantage with our PESTLE Analysis of Sealed Air—three concise sections reveal how political shifts, economic pressures, and environmental trends reshape its outlook. Ideal for investors and strategists, this report is ready to use. Purchase the full analysis for the detailed insights you need now.

Political factors

Trade policies and tariffs

Global packaging supply chains remain exposed to tariff shifts and non-tariff barriers, highlighted by US tariffs since 2018 covering roughly $370 billion of Chinese goods, which can quickly alter input costs and pricing power for Sealed Air.

Changes in US–China and EU trade relations can compress margins, so Sealed Air must diversify sourcing and adjust transfer pricing to mitigate volatility.

Proactive lobbying and scenario planning preserve margins amid policy uncertainty.

Food security and public health priorities

Governments prioritise food safety, driving demand for hygienic, shelf‑life‑extending packaging as WHO reports 600 million foodborne illnesses annually. Public funding and standards accelerate adoption of advanced materials amid FAO estimates of 1.3 billion tonnes of food lost annually. Policy emphasis on cold chain integrity aligns with Sealed Air’s offerings and can unlock national procurement channels.

Industrial policy and reshoring incentives

Industrial policy and reshoring incentives reshape Sealed Airs plant footprint and capex timing as the Inflation Reduction Act earmarks roughly 369 billion USD for clean-energy and manufacturing support through the 2020s, lowering energy and production unit costs via tax credits and grants. Reshoring improves service levels and lead times but requires development of localized supplier networks and higher working-capital to regionalize. Balancing these incentives against logistics cost and efficiency is essential.

Geopolitical instability and logistics risk

Geopolitical conflicts and sanctions since 2022 have disrupted resin and chemical flows and constrained shipping lanes, increasing supply risk for Sealed Air. Freight rerouting has lengthened lead times and pushed up working capital needs. Multiregion inventory buffers, dual-sourcing, insurance and hedging become critical risk mitigants.

- Resin/chemical flow disruption

- Higher lead times & working capital

- Multiregion buffers & dual-sourcing

- Insurance & hedging essential

Government sustainability agendas

Tariffs, food-safety pressure and recycling targets reshape packaging margins and capex

Tariff shifts (US tariffs since 2018 on ≈$370bn of Chinese goods) and US–China/EU tensions can raise input costs and compress margins for Sealed Air.

Food-safety policy drives demand—WHO: 600m foodborne illnesses/yr; FAO: 1.3bn t food loss—favoring shelf‑life solutions.

Industrial policy/IRA (~$369bn) and reshoring incentives alter capex and localization needs.

EU recyclability target 2030 and 65% municipal recycling by 2035 force portfolio shifts to recyclable/recycled content.

| Metric | Value |

|---|---|

| US tariffs (since 2018) | $370bn |

| WHO foodborne illnesses | 600m/yr |

| FAO food loss | 1.3bn t/yr |

| IRA manufacturing funds | $369bn |

| EU recyclable target | 2030 |

What is included in the product

Explores how macro-environmental forces uniquely affect the Sealed Air across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk management, and investor communications.

A concise, visually segmented Sealed Air PESTLE summary that relieves meeting prep pain by highlighting key external risks and opportunities for quick drop‑in to presentations, team alignment, or consultant reports.

Economic factors

Resin and energy price volatility

Polymer feedstocks and utilities are a large share of Sealed Air's COGS, and industry data show North American polyethylene prices dropped roughly 35% from 2022 to 2023 (IHS Markit), illustrating volatility that can swing margins sharply.

Price spikes compress margins unless pass-throughs work; hedging and long-term resin/energy contracts stabilize costs but cap upside, while process efficiency and lightweighting reduce sensitivity to these cycles.

Consumer demand and e-commerce growth

Rising e-commerce — ~22% of global retail sales in 2024 — amplifies demand elasticity for protective packaging as volumes and return rates fluctuate. Macroeconomic slowdowns trimmed global parcel volumes ~3% in 2023–24, compressing shipping activity and shifting SKU mixes toward smaller, cost-sensitive items. Value-engineered solutions help defend volumes in downcycles, while omnichannel logistics growth drives demand for automation-ready packaging systems to cut labor and speed fulfilment.

Food inflation and retailer pressure

Retailers facing 2024 food-at-home inflation of roughly 5.6% (BLS) increasingly push suppliers for cost containment, heightening margin pressure on packaged-food customers. Packaging that reduces shrink and extends shelf life—reducing waste by 10–20% in retailer pilots—helps offset price pressure by protecting sell-through. ROI-proven Sealed Air solutions shift conversations from unit cost to total value, and joint business planning with major grocers can lock in category share through co-funded trials and guaranteed replenishment programs.

Currency fluctuations

Sealed Air faces material FX risk as multicurrency revenues and costs expose reported results to exchange-rate swings, especially between USD, EUR and emerging-market currencies.

Local production and sourcing provide natural hedges that reduce translation risk, while dynamic pricing, surcharges and contract clauses are used to pass through cost changes.

Treasury centralization focuses on cash repatriation, netting and currency-denominated debt to optimize debt servicing and liquidity.

- FX exposure: multicurrency revenues vs costs

- Natural hedging: local production reduces translation risk

- Pricing tools: surcharges and indexation manage volatility

- Treasury: cash netting, repatriation, currency debt

Capex cycles and automation spend

Customers ramp up packaging equipment buys during expansion phases, but higher borrowing costs in 2023–24 slowed automation projects and extended sales cycles; the global industrial automation market reached about $230 billion in 2024, highlighting persistent demand. Rising labor costs have shortened payback periods for automation investments, and flexible financing options help sustain equipment adoption through downturns.

- Capex sensitivity: higher rates lengthen sales cycles

- Payback improvement: rising labor costs favor automation

- Finance role: flexible terms sustain adoption through cycles

Tariffs, food-safety pressure and recycling targets reshape packaging margins and capex

Polymer feedstock volatility (NA polyethylene down ~35% 2022–23) and rising inputs drive margin swings; hedging, long-term contracts and lightweighting mitigate impact. E-commerce ~22% of global retail sales (2024) and a ~$230B automation market (2024) push demand for protective, automation-ready packaging. Food-at-home inflation ~5.6% (2024) and FX exposure increase pricing and cash-management pressure.

Preview Before You Purchase

Sealed Air PESTLE Analysis

The preview shown here is the exact Sealed Air PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. What you see in this preview is the final file delivered upon checkout with no placeholders or surprises. Download instantly and apply the analysis immediately.