Sectra AB Porter's Five Forces Analysis

Don't Miss the Bigger Picture

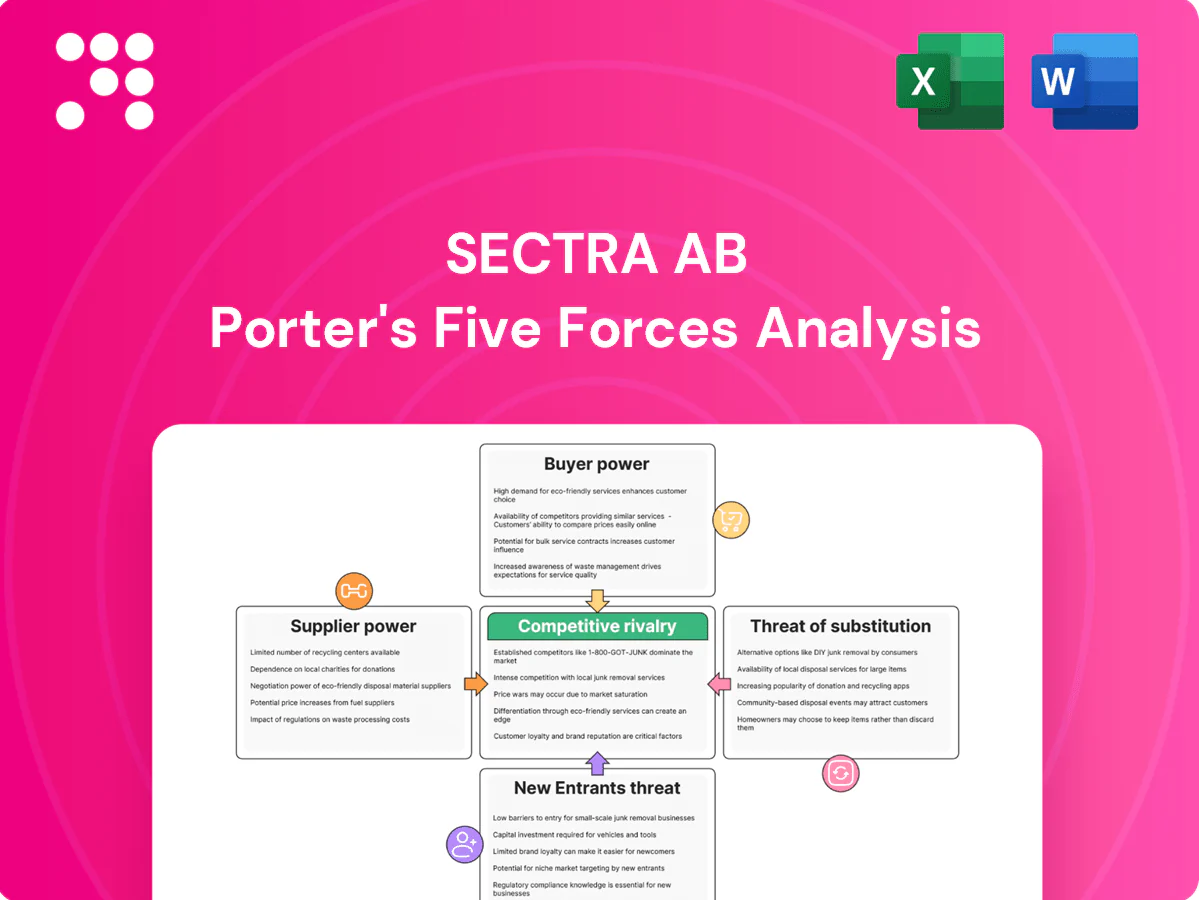

Sectra AB operates in a niche, tech-driven healthcare and secure communications market where strong IP, regulatory compliance, and customer relationships create high entry barriers and moderate competitive rivalry. Supplier and buyer power are balanced by specialized products and long-term contracts, while substitutes and new entrants pose limited but evolving threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Sectra AB’s competitive dynamics and strategic implications in depth.

Suppliers Bargaining Power

Dependence on hyperscale cloud

Sectra's growing reliance on hyperscalers concentrates supplier power: AWS, Microsoft Azure and Google Cloud held roughly 33%, 22% and 11% of global cloud market share in 2024, totaling ~66%. Contract terms and egress fees (AWS S3 data-out about 0.09 USD/GB for initial tiers) and regional data-residency rules can materially shift costs. Multi-cloud and on-premise paths reduce but do not remove vendor leverage. Preferred-partner status and committed-spend discounts can soften pricing pressure.

Specialized hardware and components

High-performance storage, GPUs, secure chips and imaging workstations rely on few qualified vendors—Nvidia held roughly 80% of the AI/data‑center GPU market in 2023–2024—giving suppliers strong leverage. Vendor roadmaps and multi‑month lead times directly affect product performance and delivery schedules. Long‑term framework agreements lower supply risk but lock in dependencies. US export controls since 2022–23 can spike costs and delay deployments.

Third‑party software and AI toolchains

Dependencies on DICOM stacks, databases, AI frameworks and cybersecurity libraries create tangible switching friction for Sectra, raising migration costs and integration risk. License changes and disclosed vulnerabilities can rapidly shift bargaining power to suppliers. Open‑source alternatives are available but increase support and compliance burdens, while EU NIS2 and expanded SBOM expectations (applicable from Oct 2024) add negotiation complexity.

Talent and certified services

Telecom and secure device vendors

Secure comms for Sectra rely on vetted devices, HSMs and carrier-grade networks, and with fewer than a dozen vendors meeting strict government/defense certifications in 2024 supplier leverage remains high; interoperability mandates reduce lock-in but slow integration, while volume commitments and co-development improve pricing and roadmap influence.

- Fewer than 12 certified vendors (2024)

- Interoperability mandates lower lock-in but extend integration by months

- Volume/co-development → better terms and product alignment

Concentrated cloud & GPU power: 66%, 80%

Sectra faces concentrated supplier power: hyperscalers held ~66% global cloud share in 2024 (AWS 33%, Azure 22%, GCP 11%), Nvidia ~80% AI GPU share (2023–24). Talent gap ~3.4M (ISC2) raises costs 10–20% for certified staff. Cert‑restricted secure‑comm vendors <12 in 2024; long lead times and export controls increase dependence.

| Item | Metric (2023–24) |

|---|---|

| Hyperscaler share | ~66% |

| Nvidia GPU | ~80% |

| Cyber talent gap | ~3.4M |

| Certified vendors | <12 |

What is included in the product

Tailored Porter's Five Forces for Sectra AB uncovering key competitive drivers, buyer/supplier power, threat of new entrants and substitutes, and identifying disruptive technologies and market barriers that shape its profitability.

A concise one-sheet Porter's Five Forces for Sectra AB that visualizes strategic pressure with an instant radar chart, lets you customize force levels for emerging threats or regulation scenarios, and exports cleanly into pitch decks or Excel dashboards for boardroom-ready decision-making.

Customers Bargaining Power

Consolidated hospital networks

Consolidated hospital networks (AHA 2023: ~56% of U.S. hospitals in systems) push aggressive price and SLA negotiations, running competitive RFPs that demand interoperability and outcome guarantees. Volume contracts trade lower margins for footprint and referenceability, with many RFPs stipulating uptime, patient-outcome metrics and integration timelines. High switching costs from PACS/IT integrations and training temper but do not eliminate buyer power.

Government and defense buyers

Government and defense buyers impose strict procurement standards, audits and often long payment terms (commonly 60–120 days), increasing working capital strain on suppliers. Security accreditation and data sovereignty rules raise compliance costs and slow deployments, especially after tightened EU guidance on cross‑border data in 2024. Budget cycles and rigid tender rules amplify price sensitivity, making framework contracts decisive but typically margin‑thin for vendors.

High switching and integration frictions

Migrating archives, workflows and user training create significant lock-in for Sectra, moderating buyer leverage despite procurement pressure.

Buyers counter with phased multi-vendor strategies to retain options, while API and FHIR/DICOM interoperability—DICOM standardized since 1993 and HL7 FHIR R4 normative since 2019—shifts competition toward price and service.

Robust migration toolkits can turn lock-in into upsell by lowering migration risk and accelerating deployment.

Outcome and uptime expectations

Buyers demand 24/7 availability with SLAs of 99.9–99.99% (≈8.8 hours to ≈52.6 minutes downtime/year); cybersecurity posture and clinical throughput KPIs are contractual. Penalties and credits, commonly 5–10% of service fees, shift risk onto vendors. Customers push XaaS with elastic pricing, while strong uptime references allow vendors to command premium pricing.

- SLAs: 99.9–99.99%

- Penalties/credits: ~5–10% of fees

- Trend: XaaS + elastic pricing

- Value: proven uptime justifies premium

AI and total cost scrutiny

Buyers benchmark AI-enabled workflows on ROI, pushing vendors to bundle AI, storage and analytics into predictable subscriptions; vendor filings in 2024 show a clear shift toward ARR-focused deals. Data egress (≈$0.09/GB on major clouds in 2024) and inference compute (dozens of $/hr on GPU instances) are frequent negotiation focal points. Transparent TCO models help defend value.

- ROI-first buying

- Subscription bundling

- Data egress ≈$0.09/GB (2024)

- Inference = major cost driver

- Transparent TCO = defense

Consolidation fuels buyer leverage: long payments, tight SLAs, data egress ≈ $0.09/GB

Consolidated hospital systems (AHA 2023: ~56% in systems) and government tenders drive aggressive price/SLA negotiation, leveraging RFPs, volume contracts and long payment terms (60–120 days). High PACS/IT switching costs and proven uptime (SLAs 99.9–99.99%) moderate but don’t erase buyer power; buyers push XaaS, ROI‑bundles and data‑egress/inference cost transparency (egress ≈$0.09/GB in 2024).

| Metric | Value |

|---|---|

| Hospitals in systems | ~56% (AHA 2023) |

| Payment terms | 60–120 days |

| SLAs | 99.9–99.99% |

| Penalties | 5–10% fees |

| Data egress (2024) | ≈$0.09/GB |

Same Document Delivered

Sectra AB Porter's Five Forces Analysis

This preview shows the exact Sectra AB Porter's Five Forces Analysis you'll receive upon purchase—no placeholders or mockups. The full, professionally formatted document is ready for immediate download and use the moment you buy. What you see is what you get.

Don't Miss the Bigger Picture

Sectra AB operates in a niche, tech-driven healthcare and secure communications market where strong IP, regulatory compliance, and customer relationships create high entry barriers and moderate competitive rivalry. Supplier and buyer power are balanced by specialized products and long-term contracts, while substitutes and new entrants pose limited but evolving threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Sectra AB’s competitive dynamics and strategic implications in depth.

Suppliers Bargaining Power

Dependence on hyperscale cloud

Sectra's growing reliance on hyperscalers concentrates supplier power: AWS, Microsoft Azure and Google Cloud held roughly 33%, 22% and 11% of global cloud market share in 2024, totaling ~66%. Contract terms and egress fees (AWS S3 data-out about 0.09 USD/GB for initial tiers) and regional data-residency rules can materially shift costs. Multi-cloud and on-premise paths reduce but do not remove vendor leverage. Preferred-partner status and committed-spend discounts can soften pricing pressure.

Specialized hardware and components

High-performance storage, GPUs, secure chips and imaging workstations rely on few qualified vendors—Nvidia held roughly 80% of the AI/data‑center GPU market in 2023–2024—giving suppliers strong leverage. Vendor roadmaps and multi‑month lead times directly affect product performance and delivery schedules. Long‑term framework agreements lower supply risk but lock in dependencies. US export controls since 2022–23 can spike costs and delay deployments.

Third‑party software and AI toolchains

Dependencies on DICOM stacks, databases, AI frameworks and cybersecurity libraries create tangible switching friction for Sectra, raising migration costs and integration risk. License changes and disclosed vulnerabilities can rapidly shift bargaining power to suppliers. Open‑source alternatives are available but increase support and compliance burdens, while EU NIS2 and expanded SBOM expectations (applicable from Oct 2024) add negotiation complexity.

Talent and certified services

Telecom and secure device vendors

Secure comms for Sectra rely on vetted devices, HSMs and carrier-grade networks, and with fewer than a dozen vendors meeting strict government/defense certifications in 2024 supplier leverage remains high; interoperability mandates reduce lock-in but slow integration, while volume commitments and co-development improve pricing and roadmap influence.

- Fewer than 12 certified vendors (2024)

- Interoperability mandates lower lock-in but extend integration by months

- Volume/co-development → better terms and product alignment

Concentrated cloud & GPU power: 66%, 80%

Sectra faces concentrated supplier power: hyperscalers held ~66% global cloud share in 2024 (AWS 33%, Azure 22%, GCP 11%), Nvidia ~80% AI GPU share (2023–24). Talent gap ~3.4M (ISC2) raises costs 10–20% for certified staff. Cert‑restricted secure‑comm vendors <12 in 2024; long lead times and export controls increase dependence.

| Item | Metric (2023–24) |

|---|---|

| Hyperscaler share | ~66% |

| Nvidia GPU | ~80% |

| Cyber talent gap | ~3.4M |

| Certified vendors | <12 |

What is included in the product

Tailored Porter's Five Forces for Sectra AB uncovering key competitive drivers, buyer/supplier power, threat of new entrants and substitutes, and identifying disruptive technologies and market barriers that shape its profitability.

A concise one-sheet Porter's Five Forces for Sectra AB that visualizes strategic pressure with an instant radar chart, lets you customize force levels for emerging threats or regulation scenarios, and exports cleanly into pitch decks or Excel dashboards for boardroom-ready decision-making.

Customers Bargaining Power

Consolidated hospital networks

Consolidated hospital networks (AHA 2023: ~56% of U.S. hospitals in systems) push aggressive price and SLA negotiations, running competitive RFPs that demand interoperability and outcome guarantees. Volume contracts trade lower margins for footprint and referenceability, with many RFPs stipulating uptime, patient-outcome metrics and integration timelines. High switching costs from PACS/IT integrations and training temper but do not eliminate buyer power.

Government and defense buyers

Government and defense buyers impose strict procurement standards, audits and often long payment terms (commonly 60–120 days), increasing working capital strain on suppliers. Security accreditation and data sovereignty rules raise compliance costs and slow deployments, especially after tightened EU guidance on cross‑border data in 2024. Budget cycles and rigid tender rules amplify price sensitivity, making framework contracts decisive but typically margin‑thin for vendors.

High switching and integration frictions

Migrating archives, workflows and user training create significant lock-in for Sectra, moderating buyer leverage despite procurement pressure.

Buyers counter with phased multi-vendor strategies to retain options, while API and FHIR/DICOM interoperability—DICOM standardized since 1993 and HL7 FHIR R4 normative since 2019—shifts competition toward price and service.

Robust migration toolkits can turn lock-in into upsell by lowering migration risk and accelerating deployment.

Outcome and uptime expectations

Buyers demand 24/7 availability with SLAs of 99.9–99.99% (≈8.8 hours to ≈52.6 minutes downtime/year); cybersecurity posture and clinical throughput KPIs are contractual. Penalties and credits, commonly 5–10% of service fees, shift risk onto vendors. Customers push XaaS with elastic pricing, while strong uptime references allow vendors to command premium pricing.

- SLAs: 99.9–99.99%

- Penalties/credits: ~5–10% of fees

- Trend: XaaS + elastic pricing

- Value: proven uptime justifies premium

AI and total cost scrutiny

Buyers benchmark AI-enabled workflows on ROI, pushing vendors to bundle AI, storage and analytics into predictable subscriptions; vendor filings in 2024 show a clear shift toward ARR-focused deals. Data egress (≈$0.09/GB on major clouds in 2024) and inference compute (dozens of $/hr on GPU instances) are frequent negotiation focal points. Transparent TCO models help defend value.

- ROI-first buying

- Subscription bundling

- Data egress ≈$0.09/GB (2024)

- Inference = major cost driver

- Transparent TCO = defense

Consolidation fuels buyer leverage: long payments, tight SLAs, data egress ≈ $0.09/GB

Consolidated hospital systems (AHA 2023: ~56% in systems) and government tenders drive aggressive price/SLA negotiation, leveraging RFPs, volume contracts and long payment terms (60–120 days). High PACS/IT switching costs and proven uptime (SLAs 99.9–99.99%) moderate but don’t erase buyer power; buyers push XaaS, ROI‑bundles and data‑egress/inference cost transparency (egress ≈$0.09/GB in 2024).

| Metric | Value |

|---|---|

| Hospitals in systems | ~56% (AHA 2023) |

| Payment terms | 60–120 days |

| SLAs | 99.9–99.99% |

| Penalties | 5–10% fees |

| Data egress (2024) | ≈$0.09/GB |

Same Document Delivered

Sectra AB Porter's Five Forces Analysis

This preview shows the exact Sectra AB Porter's Five Forces Analysis you'll receive upon purchase—no placeholders or mockups. The full, professionally formatted document is ready for immediate download and use the moment you buy. What you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Sectra AB operates in a niche, tech-driven healthcare and secure communications market where strong IP, regulatory compliance, and customer relationships create high entry barriers and moderate competitive rivalry. Supplier and buyer power are balanced by specialized products and long-term contracts, while substitutes and new entrants pose limited but evolving threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Sectra AB’s competitive dynamics and strategic implications in depth.

Suppliers Bargaining Power

Dependence on hyperscale cloud

Sectra's growing reliance on hyperscalers concentrates supplier power: AWS, Microsoft Azure and Google Cloud held roughly 33%, 22% and 11% of global cloud market share in 2024, totaling ~66%. Contract terms and egress fees (AWS S3 data-out about 0.09 USD/GB for initial tiers) and regional data-residency rules can materially shift costs. Multi-cloud and on-premise paths reduce but do not remove vendor leverage. Preferred-partner status and committed-spend discounts can soften pricing pressure.

Specialized hardware and components

High-performance storage, GPUs, secure chips and imaging workstations rely on few qualified vendors—Nvidia held roughly 80% of the AI/data‑center GPU market in 2023–2024—giving suppliers strong leverage. Vendor roadmaps and multi‑month lead times directly affect product performance and delivery schedules. Long‑term framework agreements lower supply risk but lock in dependencies. US export controls since 2022–23 can spike costs and delay deployments.

Third‑party software and AI toolchains

Dependencies on DICOM stacks, databases, AI frameworks and cybersecurity libraries create tangible switching friction for Sectra, raising migration costs and integration risk. License changes and disclosed vulnerabilities can rapidly shift bargaining power to suppliers. Open‑source alternatives are available but increase support and compliance burdens, while EU NIS2 and expanded SBOM expectations (applicable from Oct 2024) add negotiation complexity.

Talent and certified services

Telecom and secure device vendors

Secure comms for Sectra rely on vetted devices, HSMs and carrier-grade networks, and with fewer than a dozen vendors meeting strict government/defense certifications in 2024 supplier leverage remains high; interoperability mandates reduce lock-in but slow integration, while volume commitments and co-development improve pricing and roadmap influence.

- Fewer than 12 certified vendors (2024)

- Interoperability mandates lower lock-in but extend integration by months

- Volume/co-development → better terms and product alignment

Concentrated cloud & GPU power: 66%, 80%

Sectra faces concentrated supplier power: hyperscalers held ~66% global cloud share in 2024 (AWS 33%, Azure 22%, GCP 11%), Nvidia ~80% AI GPU share (2023–24). Talent gap ~3.4M (ISC2) raises costs 10–20% for certified staff. Cert‑restricted secure‑comm vendors <12 in 2024; long lead times and export controls increase dependence.

| Item | Metric (2023–24) |

|---|---|

| Hyperscaler share | ~66% |

| Nvidia GPU | ~80% |

| Cyber talent gap | ~3.4M |

| Certified vendors | <12 |

What is included in the product

Tailored Porter's Five Forces for Sectra AB uncovering key competitive drivers, buyer/supplier power, threat of new entrants and substitutes, and identifying disruptive technologies and market barriers that shape its profitability.

A concise one-sheet Porter's Five Forces for Sectra AB that visualizes strategic pressure with an instant radar chart, lets you customize force levels for emerging threats or regulation scenarios, and exports cleanly into pitch decks or Excel dashboards for boardroom-ready decision-making.

Customers Bargaining Power

Consolidated hospital networks

Consolidated hospital networks (AHA 2023: ~56% of U.S. hospitals in systems) push aggressive price and SLA negotiations, running competitive RFPs that demand interoperability and outcome guarantees. Volume contracts trade lower margins for footprint and referenceability, with many RFPs stipulating uptime, patient-outcome metrics and integration timelines. High switching costs from PACS/IT integrations and training temper but do not eliminate buyer power.

Government and defense buyers

Government and defense buyers impose strict procurement standards, audits and often long payment terms (commonly 60–120 days), increasing working capital strain on suppliers. Security accreditation and data sovereignty rules raise compliance costs and slow deployments, especially after tightened EU guidance on cross‑border data in 2024. Budget cycles and rigid tender rules amplify price sensitivity, making framework contracts decisive but typically margin‑thin for vendors.

High switching and integration frictions

Migrating archives, workflows and user training create significant lock-in for Sectra, moderating buyer leverage despite procurement pressure.

Buyers counter with phased multi-vendor strategies to retain options, while API and FHIR/DICOM interoperability—DICOM standardized since 1993 and HL7 FHIR R4 normative since 2019—shifts competition toward price and service.

Robust migration toolkits can turn lock-in into upsell by lowering migration risk and accelerating deployment.

Outcome and uptime expectations

Buyers demand 24/7 availability with SLAs of 99.9–99.99% (≈8.8 hours to ≈52.6 minutes downtime/year); cybersecurity posture and clinical throughput KPIs are contractual. Penalties and credits, commonly 5–10% of service fees, shift risk onto vendors. Customers push XaaS with elastic pricing, while strong uptime references allow vendors to command premium pricing.

- SLAs: 99.9–99.99%

- Penalties/credits: ~5–10% of fees

- Trend: XaaS + elastic pricing

- Value: proven uptime justifies premium

AI and total cost scrutiny

Buyers benchmark AI-enabled workflows on ROI, pushing vendors to bundle AI, storage and analytics into predictable subscriptions; vendor filings in 2024 show a clear shift toward ARR-focused deals. Data egress (≈$0.09/GB on major clouds in 2024) and inference compute (dozens of $/hr on GPU instances) are frequent negotiation focal points. Transparent TCO models help defend value.

- ROI-first buying

- Subscription bundling

- Data egress ≈$0.09/GB (2024)

- Inference = major cost driver

- Transparent TCO = defense

Consolidation fuels buyer leverage: long payments, tight SLAs, data egress ≈ $0.09/GB

Consolidated hospital systems (AHA 2023: ~56% in systems) and government tenders drive aggressive price/SLA negotiation, leveraging RFPs, volume contracts and long payment terms (60–120 days). High PACS/IT switching costs and proven uptime (SLAs 99.9–99.99%) moderate but don’t erase buyer power; buyers push XaaS, ROI‑bundles and data‑egress/inference cost transparency (egress ≈$0.09/GB in 2024).

| Metric | Value |

|---|---|

| Hospitals in systems | ~56% (AHA 2023) |

| Payment terms | 60–120 days |

| SLAs | 99.9–99.99% |

| Penalties | 5–10% fees |

| Data egress (2024) | ≈$0.09/GB |

Same Document Delivered

Sectra AB Porter's Five Forces Analysis

This preview shows the exact Sectra AB Porter's Five Forces Analysis you'll receive upon purchase—no placeholders or mockups. The full, professionally formatted document is ready for immediate download and use the moment you buy. What you see is what you get.