SencorpWhite Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

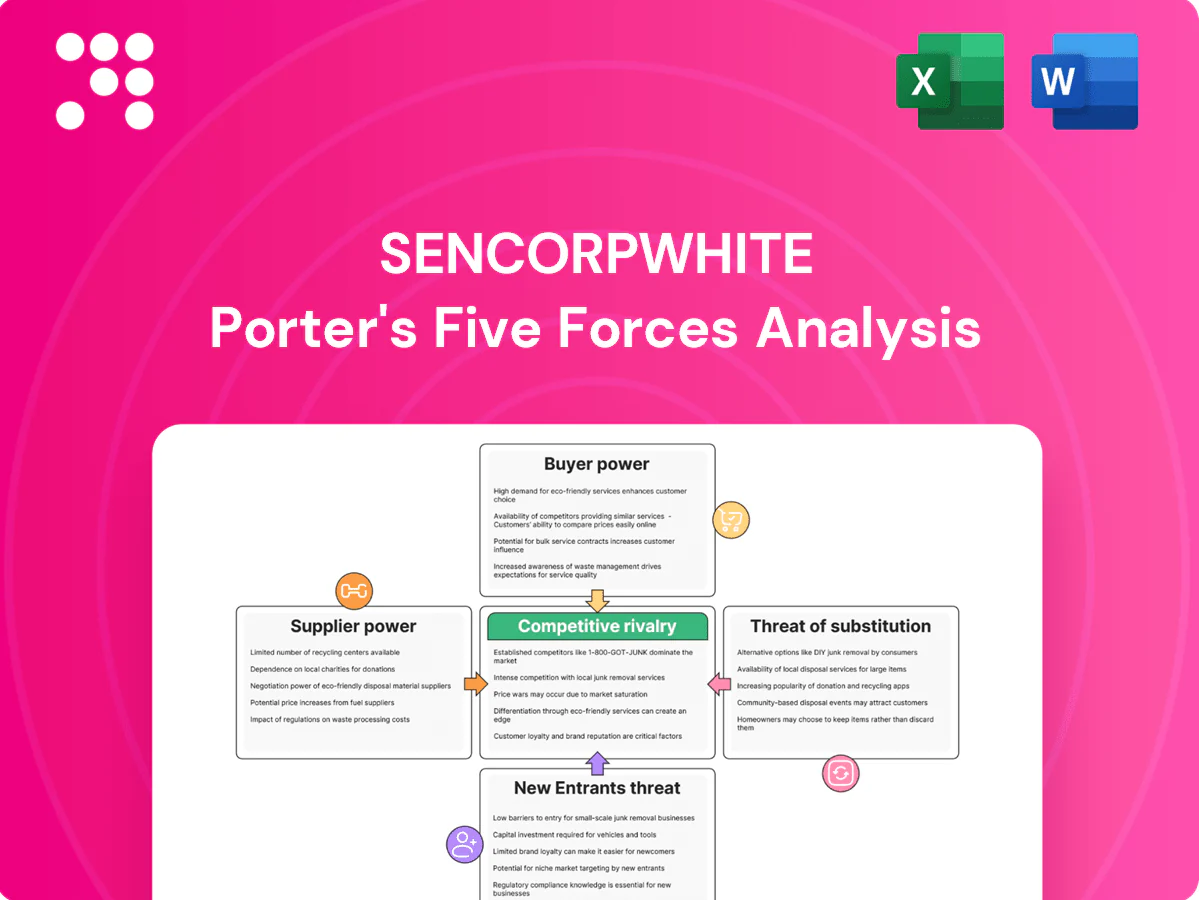

SencorpWhite’s Porter's Five Forces snapshot highlights supplier concentration, moderate buyer power, niche barriers to entry, substitute risks, and competitive rivalry shaping profitability. This concise view reveals key strategic pressures and blind spots. Ready for deeper, data-driven insights? Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Specialized component dependence

Precision robotics, servomotors, PLCs, vision sensors and custom tooling for SencorpWhite come from a concentrated set of global suppliers, with the industrial robotics market valued at about $56.7 billion in 2024, limiting alternatives and raising switching costs. Concentration lengthens lead times and grants suppliers pricing leverage, pressuring margins. Dual-sourcing and design-for-substitution reduce exposure and lower disruption risk.

Electronic and software stacks

Industrial PCs, embedded controls and vision/SCADA/MES licenses are highly sticky for SencorpWhite; 2024 industry norms show annual maintenance fees around 18–22% of license value, reinforcing supplier leverage. Version lock-in and certification needs elevate switching costs and supplier power. EOL notices or price hikes can force redesigns costing hundreds of thousands to millions, while strategic partnerships and modular architectures materially lower that risk.

Metals and fabricated assemblies

Steel, aluminum and machined parts are largely commoditized yet showed notable price volatility in 2023–24, with spot-price swings around 20–30%, increasing supplier leverage intermittently. Regional fabricators and secondary mills (serving ~40–60% of assembly needs) provide alternatives that moderate supplier power. Tight tolerances and QA specs shrink the qualified supplier pool, concentrating leverage on capable vendors. Long-term contracts and VMI programs have been used to stabilize costs and lead times.

Custom tooling and molds

Thermoforming tooling is bespoke and schedule-critical; 2024 industry norms show lead times typically 8–16 weeks, giving the few high-precision shops disproportionate leverage when quality and cycle-time matter. Tooling delays are frequent project bottlenecks, while in-house tooling or certified panel suppliers have proven to rebalance negotiating terms and reduce time-to-market.

- Lead times: 8–16 weeks

- High-precision suppliers: limited, high leverage

- Mitigation: in-house or certified panels

Logistics and lead-time sensitivity

Global supply chains for SencorpWhite increase dependency on freight capacity; Drewry's World Container Index averaged roughly USD 1,000 per 40ft in 2024, making expedited shipping premiums (often 2–3x) and buffer inventory materially raise costs and margin pressure. Suppliers with regional hubs gain influence during disruptions, while nearshoring and increased safety stocks have reduced outage exposure.

- Freight cost: ~USD 1,000/40ft (2024)

- Expedited premium: 2–3x

- Buffer stock raises COGS

- Nearshoring lowers lead-time risk

Supplier concentration raises pricing power; maintenance fees 18-22%

Supplier base is concentrated for precision robotics and tooling, giving pricing and lead-time leverage (industrial robotics market $56.7B in 2024). Software/controls are sticky with maintenance fees ~18–22%, raising switching costs. Metals are commoditized but showed 20–30% spot volatility in 2023–24, tightening qualified suppliers. Freight (Drewry WCI ~$1,000/40ft in 2024) and thermoforming (8–16 wks) add episodic supplier power.

| Item | 2024 metric |

|---|---|

| Robotics market | $56.7B |

| License maintenance | 18–22% |

| Metal spot volatility | 20–30% |

| Thermoforming lead time | 8–16 wks |

| Container cost | $1,000/40ft |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to SencorpWhite, revealing competitive intensity, buyer/supplier leverage, threat of substitutes and entry barriers, and highlighting disruptive risks and strategic defense points.

A concise, one-sheet Porter's Five Forces for SencorpWhite that instantly highlights competitive pressures and relieves strategic uncertainty—ready to drop into investor decks or operational planning.

Customers Bargaining Power

Large industrial buyers

Large industrial buyers in pharma, food, medical devices and e-commerce increasingly buy via formal RFPs, leveraging professional procurement teams to raise bargaining power. Global e-commerce sales hit about $6.3 trillion in 2024, reflecting scale that tightens supplier margins. They routinely demand customization, extended warranties and stringent SLAs, while competitive quoting keeps pricing and concessions compressed.

High switching costs, yet comparable bids

Integration with ERP/WMS and conveyor/robotics ecosystems raises switching costs for SencorpWhite customers, making replacements complex and time-consuming. Still, 3–5 credible OEMs in the packaging/automation space enable like-for-like comparisons, driving competitive bids. Buyers routinely use TCO analyses to negotiate 5–15% discounts, while demonstrated ROI (commonly 12–24 months) and customer references defend pricing.

Customization and specification control

Customers dictate specs, validation, and compliance (GMP, FDA, CE), driving engineering changes and scope creep toward SencorpWhite; tight acceptance criteria shift performance risk to suppliers. Market demand rose ~5.8% in 2024 for pharma packaging equipment, intensifying buyer leverage. Clear SOWs with phased milestones and validation gates are essential to rebalance risk and control change orders.

Aftermarket leverage

Aftermarket leverage is strong: spare parts, preventive-maintenance contracts and software updates generate recurring revenue and in 2024 accounted for roughly 30% of OEM service mix industry-wide. Buyers demand uptime guarantees and bundled pricing, while multi-year service contracts are often rebid or unbundled to reduce costs. Performance-based SLAs can align incentives and protect margins.

- Recurring parts/software/PM

- Uptime guarantees drive pricing

- Contracts rebid/unbundled

- Performance SLAs align incentives

Cyclical capex timing

Cyclical capex timing drives buyer power: macro cycles and inventory swings push customers to time purchases, delaying projects to extract concessions in soft markets, while in tight cycles 58% of industrial buyers in 2024 surveys prioritized lead-time over price; flexible financing reduced procurement pushback by ~20%.

RFPs Drive 5–15% Savings as E-commerce Pressure and ERP Lock-in Shape OEM Aftermarket

Buyers use RFPs to secure 5–15% discounts; global e‑commerce ~$6.3T (2024) tightens margins. ERP/WMS integration raises switching costs, but 3–5 OEMs sustain competitive bids; ROI 12–24 months supports pricing. Aftermarket ~30% of OEM service mix (2024); buyers rebid contracts and demand uptime SLAs.

| Metric | 2024 |

|---|---|

| Global e‑commerce | $6.3T |

| Aftermarket share | ~30% |

| Buyer discount range | 5–15% |

| OEM competitors | 3–5 |

Full Version Awaits

SencorpWhite Porter's Five Forces Analysis

This preview of the SencorpWhite Porter's Five Forces Analysis is the exact, fully formatted document you'll receive immediately after purchase—no placeholders or samples. It delivers the full assessment of competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry, ready for immediate download and use.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

SencorpWhite’s Porter's Five Forces snapshot highlights supplier concentration, moderate buyer power, niche barriers to entry, substitute risks, and competitive rivalry shaping profitability. This concise view reveals key strategic pressures and blind spots. Ready for deeper, data-driven insights? Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Specialized component dependence

Precision robotics, servomotors, PLCs, vision sensors and custom tooling for SencorpWhite come from a concentrated set of global suppliers, with the industrial robotics market valued at about $56.7 billion in 2024, limiting alternatives and raising switching costs. Concentration lengthens lead times and grants suppliers pricing leverage, pressuring margins. Dual-sourcing and design-for-substitution reduce exposure and lower disruption risk.

Electronic and software stacks

Industrial PCs, embedded controls and vision/SCADA/MES licenses are highly sticky for SencorpWhite; 2024 industry norms show annual maintenance fees around 18–22% of license value, reinforcing supplier leverage. Version lock-in and certification needs elevate switching costs and supplier power. EOL notices or price hikes can force redesigns costing hundreds of thousands to millions, while strategic partnerships and modular architectures materially lower that risk.

Metals and fabricated assemblies

Steel, aluminum and machined parts are largely commoditized yet showed notable price volatility in 2023–24, with spot-price swings around 20–30%, increasing supplier leverage intermittently. Regional fabricators and secondary mills (serving ~40–60% of assembly needs) provide alternatives that moderate supplier power. Tight tolerances and QA specs shrink the qualified supplier pool, concentrating leverage on capable vendors. Long-term contracts and VMI programs have been used to stabilize costs and lead times.

Custom tooling and molds

Thermoforming tooling is bespoke and schedule-critical; 2024 industry norms show lead times typically 8–16 weeks, giving the few high-precision shops disproportionate leverage when quality and cycle-time matter. Tooling delays are frequent project bottlenecks, while in-house tooling or certified panel suppliers have proven to rebalance negotiating terms and reduce time-to-market.

- Lead times: 8–16 weeks

- High-precision suppliers: limited, high leverage

- Mitigation: in-house or certified panels

Logistics and lead-time sensitivity

Global supply chains for SencorpWhite increase dependency on freight capacity; Drewry's World Container Index averaged roughly USD 1,000 per 40ft in 2024, making expedited shipping premiums (often 2–3x) and buffer inventory materially raise costs and margin pressure. Suppliers with regional hubs gain influence during disruptions, while nearshoring and increased safety stocks have reduced outage exposure.

- Freight cost: ~USD 1,000/40ft (2024)

- Expedited premium: 2–3x

- Buffer stock raises COGS

- Nearshoring lowers lead-time risk

Supplier concentration raises pricing power; maintenance fees 18-22%

Supplier base is concentrated for precision robotics and tooling, giving pricing and lead-time leverage (industrial robotics market $56.7B in 2024). Software/controls are sticky with maintenance fees ~18–22%, raising switching costs. Metals are commoditized but showed 20–30% spot volatility in 2023–24, tightening qualified suppliers. Freight (Drewry WCI ~$1,000/40ft in 2024) and thermoforming (8–16 wks) add episodic supplier power.

| Item | 2024 metric |

|---|---|

| Robotics market | $56.7B |

| License maintenance | 18–22% |

| Metal spot volatility | 20–30% |

| Thermoforming lead time | 8–16 wks |

| Container cost | $1,000/40ft |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to SencorpWhite, revealing competitive intensity, buyer/supplier leverage, threat of substitutes and entry barriers, and highlighting disruptive risks and strategic defense points.

A concise, one-sheet Porter's Five Forces for SencorpWhite that instantly highlights competitive pressures and relieves strategic uncertainty—ready to drop into investor decks or operational planning.

Customers Bargaining Power

Large industrial buyers

Large industrial buyers in pharma, food, medical devices and e-commerce increasingly buy via formal RFPs, leveraging professional procurement teams to raise bargaining power. Global e-commerce sales hit about $6.3 trillion in 2024, reflecting scale that tightens supplier margins. They routinely demand customization, extended warranties and stringent SLAs, while competitive quoting keeps pricing and concessions compressed.

High switching costs, yet comparable bids

Integration with ERP/WMS and conveyor/robotics ecosystems raises switching costs for SencorpWhite customers, making replacements complex and time-consuming. Still, 3–5 credible OEMs in the packaging/automation space enable like-for-like comparisons, driving competitive bids. Buyers routinely use TCO analyses to negotiate 5–15% discounts, while demonstrated ROI (commonly 12–24 months) and customer references defend pricing.

Customization and specification control

Customers dictate specs, validation, and compliance (GMP, FDA, CE), driving engineering changes and scope creep toward SencorpWhite; tight acceptance criteria shift performance risk to suppliers. Market demand rose ~5.8% in 2024 for pharma packaging equipment, intensifying buyer leverage. Clear SOWs with phased milestones and validation gates are essential to rebalance risk and control change orders.

Aftermarket leverage

Aftermarket leverage is strong: spare parts, preventive-maintenance contracts and software updates generate recurring revenue and in 2024 accounted for roughly 30% of OEM service mix industry-wide. Buyers demand uptime guarantees and bundled pricing, while multi-year service contracts are often rebid or unbundled to reduce costs. Performance-based SLAs can align incentives and protect margins.

- Recurring parts/software/PM

- Uptime guarantees drive pricing

- Contracts rebid/unbundled

- Performance SLAs align incentives

Cyclical capex timing

Cyclical capex timing drives buyer power: macro cycles and inventory swings push customers to time purchases, delaying projects to extract concessions in soft markets, while in tight cycles 58% of industrial buyers in 2024 surveys prioritized lead-time over price; flexible financing reduced procurement pushback by ~20%.

RFPs Drive 5–15% Savings as E-commerce Pressure and ERP Lock-in Shape OEM Aftermarket

Buyers use RFPs to secure 5–15% discounts; global e‑commerce ~$6.3T (2024) tightens margins. ERP/WMS integration raises switching costs, but 3–5 OEMs sustain competitive bids; ROI 12–24 months supports pricing. Aftermarket ~30% of OEM service mix (2024); buyers rebid contracts and demand uptime SLAs.

| Metric | 2024 |

|---|---|

| Global e‑commerce | $6.3T |

| Aftermarket share | ~30% |

| Buyer discount range | 5–15% |

| OEM competitors | 3–5 |

Full Version Awaits

SencorpWhite Porter's Five Forces Analysis

This preview of the SencorpWhite Porter's Five Forces Analysis is the exact, fully formatted document you'll receive immediately after purchase—no placeholders or samples. It delivers the full assessment of competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry, ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

SencorpWhite’s Porter's Five Forces snapshot highlights supplier concentration, moderate buyer power, niche barriers to entry, substitute risks, and competitive rivalry shaping profitability. This concise view reveals key strategic pressures and blind spots. Ready for deeper, data-driven insights? Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Specialized component dependence

Precision robotics, servomotors, PLCs, vision sensors and custom tooling for SencorpWhite come from a concentrated set of global suppliers, with the industrial robotics market valued at about $56.7 billion in 2024, limiting alternatives and raising switching costs. Concentration lengthens lead times and grants suppliers pricing leverage, pressuring margins. Dual-sourcing and design-for-substitution reduce exposure and lower disruption risk.

Electronic and software stacks

Industrial PCs, embedded controls and vision/SCADA/MES licenses are highly sticky for SencorpWhite; 2024 industry norms show annual maintenance fees around 18–22% of license value, reinforcing supplier leverage. Version lock-in and certification needs elevate switching costs and supplier power. EOL notices or price hikes can force redesigns costing hundreds of thousands to millions, while strategic partnerships and modular architectures materially lower that risk.

Metals and fabricated assemblies

Steel, aluminum and machined parts are largely commoditized yet showed notable price volatility in 2023–24, with spot-price swings around 20–30%, increasing supplier leverage intermittently. Regional fabricators and secondary mills (serving ~40–60% of assembly needs) provide alternatives that moderate supplier power. Tight tolerances and QA specs shrink the qualified supplier pool, concentrating leverage on capable vendors. Long-term contracts and VMI programs have been used to stabilize costs and lead times.

Custom tooling and molds

Thermoforming tooling is bespoke and schedule-critical; 2024 industry norms show lead times typically 8–16 weeks, giving the few high-precision shops disproportionate leverage when quality and cycle-time matter. Tooling delays are frequent project bottlenecks, while in-house tooling or certified panel suppliers have proven to rebalance negotiating terms and reduce time-to-market.

- Lead times: 8–16 weeks

- High-precision suppliers: limited, high leverage

- Mitigation: in-house or certified panels

Logistics and lead-time sensitivity

Global supply chains for SencorpWhite increase dependency on freight capacity; Drewry's World Container Index averaged roughly USD 1,000 per 40ft in 2024, making expedited shipping premiums (often 2–3x) and buffer inventory materially raise costs and margin pressure. Suppliers with regional hubs gain influence during disruptions, while nearshoring and increased safety stocks have reduced outage exposure.

- Freight cost: ~USD 1,000/40ft (2024)

- Expedited premium: 2–3x

- Buffer stock raises COGS

- Nearshoring lowers lead-time risk

Supplier concentration raises pricing power; maintenance fees 18-22%

Supplier base is concentrated for precision robotics and tooling, giving pricing and lead-time leverage (industrial robotics market $56.7B in 2024). Software/controls are sticky with maintenance fees ~18–22%, raising switching costs. Metals are commoditized but showed 20–30% spot volatility in 2023–24, tightening qualified suppliers. Freight (Drewry WCI ~$1,000/40ft in 2024) and thermoforming (8–16 wks) add episodic supplier power.

| Item | 2024 metric |

|---|---|

| Robotics market | $56.7B |

| License maintenance | 18–22% |

| Metal spot volatility | 20–30% |

| Thermoforming lead time | 8–16 wks |

| Container cost | $1,000/40ft |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to SencorpWhite, revealing competitive intensity, buyer/supplier leverage, threat of substitutes and entry barriers, and highlighting disruptive risks and strategic defense points.

A concise, one-sheet Porter's Five Forces for SencorpWhite that instantly highlights competitive pressures and relieves strategic uncertainty—ready to drop into investor decks or operational planning.

Customers Bargaining Power

Large industrial buyers

Large industrial buyers in pharma, food, medical devices and e-commerce increasingly buy via formal RFPs, leveraging professional procurement teams to raise bargaining power. Global e-commerce sales hit about $6.3 trillion in 2024, reflecting scale that tightens supplier margins. They routinely demand customization, extended warranties and stringent SLAs, while competitive quoting keeps pricing and concessions compressed.

High switching costs, yet comparable bids

Integration with ERP/WMS and conveyor/robotics ecosystems raises switching costs for SencorpWhite customers, making replacements complex and time-consuming. Still, 3–5 credible OEMs in the packaging/automation space enable like-for-like comparisons, driving competitive bids. Buyers routinely use TCO analyses to negotiate 5–15% discounts, while demonstrated ROI (commonly 12–24 months) and customer references defend pricing.

Customization and specification control

Customers dictate specs, validation, and compliance (GMP, FDA, CE), driving engineering changes and scope creep toward SencorpWhite; tight acceptance criteria shift performance risk to suppliers. Market demand rose ~5.8% in 2024 for pharma packaging equipment, intensifying buyer leverage. Clear SOWs with phased milestones and validation gates are essential to rebalance risk and control change orders.

Aftermarket leverage

Aftermarket leverage is strong: spare parts, preventive-maintenance contracts and software updates generate recurring revenue and in 2024 accounted for roughly 30% of OEM service mix industry-wide. Buyers demand uptime guarantees and bundled pricing, while multi-year service contracts are often rebid or unbundled to reduce costs. Performance-based SLAs can align incentives and protect margins.

- Recurring parts/software/PM

- Uptime guarantees drive pricing

- Contracts rebid/unbundled

- Performance SLAs align incentives

Cyclical capex timing

Cyclical capex timing drives buyer power: macro cycles and inventory swings push customers to time purchases, delaying projects to extract concessions in soft markets, while in tight cycles 58% of industrial buyers in 2024 surveys prioritized lead-time over price; flexible financing reduced procurement pushback by ~20%.

RFPs Drive 5–15% Savings as E-commerce Pressure and ERP Lock-in Shape OEM Aftermarket

Buyers use RFPs to secure 5–15% discounts; global e‑commerce ~$6.3T (2024) tightens margins. ERP/WMS integration raises switching costs, but 3–5 OEMs sustain competitive bids; ROI 12–24 months supports pricing. Aftermarket ~30% of OEM service mix (2024); buyers rebid contracts and demand uptime SLAs.

| Metric | 2024 |

|---|---|

| Global e‑commerce | $6.3T |

| Aftermarket share | ~30% |

| Buyer discount range | 5–15% |

| OEM competitors | 3–5 |

Full Version Awaits

SencorpWhite Porter's Five Forces Analysis

This preview of the SencorpWhite Porter's Five Forces Analysis is the exact, fully formatted document you'll receive immediately after purchase—no placeholders or samples. It delivers the full assessment of competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry, ready for immediate download and use.