Serco Group Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

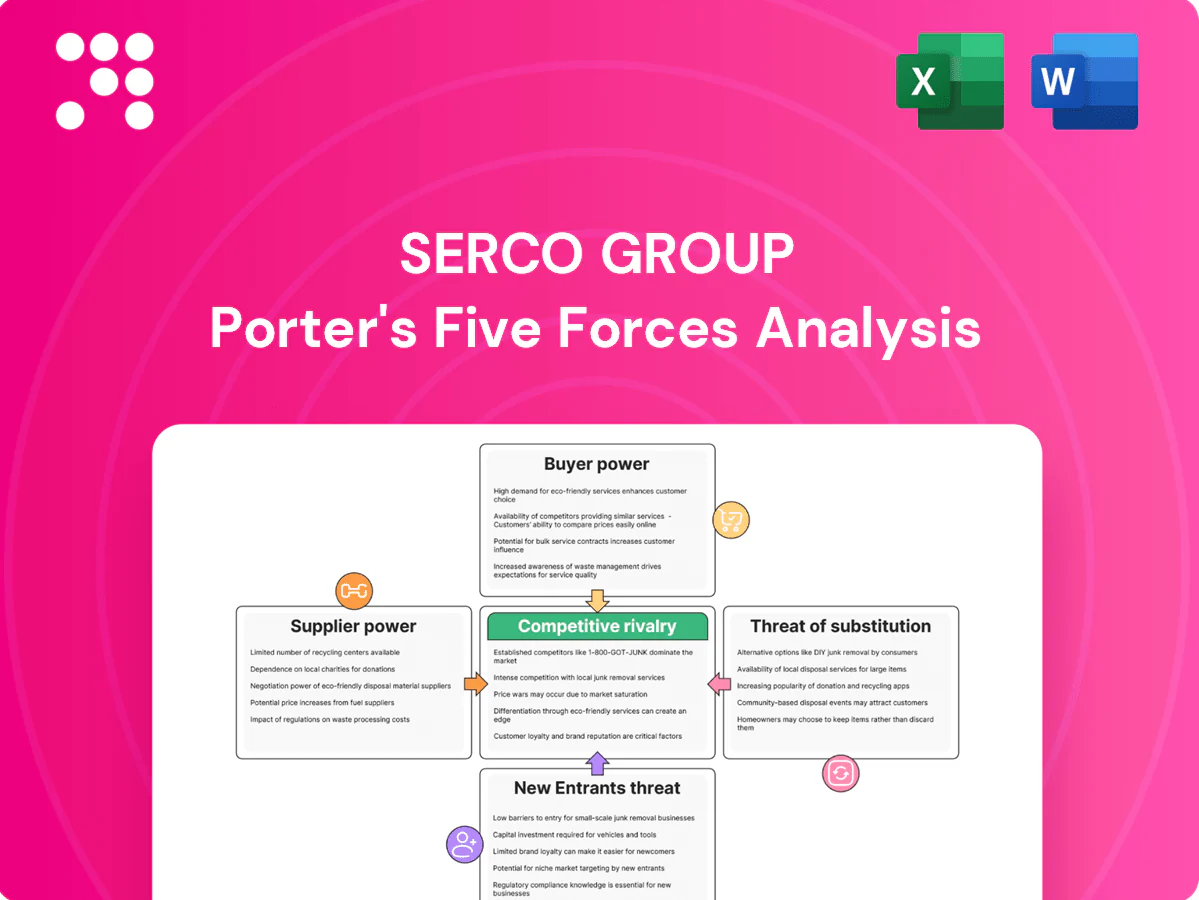

Serco Group faces moderate supplier power, high buyer scrutiny, and intense competitive rivalry driven by government contracting and performance metrics; barriers to entry are meaningful but niche substitutes and regulatory shifts pose real risks. This snapshot hints at strategic pressure points—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications for Serco Group.

Suppliers Bargaining Power

Specialized labor and clearances

Serco relies on a large pool of specialized, security-cleared and clinically licensed labor—c.55,000 employees globally per Serco’s 2024 filings—concentrated in defense, justice and healthcare, which raises supplier leverage. Scarcity of cleared or licensed talent drives wage inflation and retention premiums and heightens industrial action and compliance-cost risks. Serco mitigates through workforce development, multi-country sourcing and long-term staffing partnerships.

Mission‑critical tech and data vendors

Core case‑management, command‑and‑control and scheduling platforms and hyperscale cloud providers (AWS/Azure/GCP ~65% combined IaaS share in 2024) are hard to switch, with vendor IP, deep integrations and cybersecurity accreditations raising lock‑in and switching costs. Data residency and accreditation narrow viable suppliers, boosting supplier power. Serco mitigates via modular architectures, open standards and competitive multi‑vendor frameworks.

Facilities, fleet, and asset providers

Transport fleets, detention facilities and medical equipment demand tight specs and often >99% uptime SLAs, giving OEMs and specialist maintainers pricing power; limited suppliers and certified vendors concentrate bargaining leverage. Long lead times of 6–24 months and multi‑year capex cycles limit Serco’s flexibility during transitions. Framework agreements and lifecycle outsourcing (outsourced maintenance contracts spanning 5–10 years) help Serco balance price and availability.

Niche subcontractors and local partners

Delivery often relies on small accredited local providers for on-the-ground services; in remote or highly regulated niches a handful of qualified partners can push rates or tighter terms, shifting performance risk upstream and increasing Serco's dependency. In FY2024 Serco reported revenue of £4.4bn and mitigates risk via tiered supplier panels, performance dashboards and supplier development programs.

- High dependency on niche partners raises bargaining power

- Remote/regulatory niches: limited supplier pool

- Risk transfer increases contractual leverage for suppliers

- Mitigation: tiered panels, dashboards, development

Regulatory and compliance services

External auditors, training/accreditation bodies and H&S consultants are mandatory for Serco contract compliance; limited approved providers and mandated standards raise supplier leverage and costs. Regulatory shifts in 2024 prompted unplanned supplier spend on certification and remediation. Serco offsets risk via internal centres of excellence and pre‑negotiated compliance frameworks, supporting its c.£3.8bn 2024 revenue base.

- Mandatory providers: raises supplier bargaining power

- Regulatory change 2024: increased unplanned compliance spend

- Mitigation: internal centres of excellence

- Mitigation: pre‑negotiated frameworks

High supplier leverage: 55k cleared staff, 65% hyperscale IaaS

Serco depends on c.55,000 cleared/licensed staff (2024), giving labour suppliers high leverage. Core platforms and hyperscale cloud (AWS/Azure/GCP ~65% IaaS share in 2024) create vendor lock‑in. OEMs with 6–24 month lead times and certified local providers further concentrate supplier power; Serco uses panels, multi‑vendor architectures and long‑term frameworks to mitigate.

| Supplier type | 2024 metric | Impact |

|---|---|---|

| Labour | c.55,000 staff | High |

| Cloud | ~65% IaaS share | High |

| OEMs/local | 6–24m lead time | Medium‑High |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Serco Group, assessing competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and highlighting regulatory, contract-based barriers and emerging disruptive risks to its public-sector services and profitability.

A concise one-sheet Porter's Five Forces for Serco Group—quickly spot competitive pressures, contract risk and regulatory exposure to speed boardroom decisions. Editable pressure sliders and a radar chart let you model scenarios (outsourcing shifts, tender wins) without macros or coding.

Customers Bargaining Power

Government as dominant buyer

National and regional governments drive concentrated, sophisticated demand for Serco, which reported FY2024 revenue of about £4.6bn with roughly 75% from public-sector contracts, giving buyers scale and budget leverage to press pricing and risk transfer. Single-buyer dependence on major programs raises rebid exposure and margin pressure. Serco mitigates this through geographic and sector diversification and by quantifying measurable public-value outcomes to retain incumbency.

Competitive tendering and frameworks

Open competitive tendering and frameworks drive steep price competition and standardized contract terms; buyers now demand strict KPIs, outcome-based payments and liquidated damages, while down-select processes compress margins for incumbents and challengers alike. Serco, with circa 50,000 employees and c.£4.6bn revenue in 2024, emphasizes differentiation via proven transitions, clear innovation roadmaps and stronger governance to protect margin.

Performance and penalty regimes

Contracts often include stringent service credits and clawbacks, shifting operational risk to providers; Serco reported FY2024 revenue of £4.8bn and manages an order book near £28.0bn, increasing stakes on performance outcomes. Buyers can enforce step-in rights and adverse publicity carries reputational and financial costs, enhancing customer leverage. Serco invests in real-time performance management to preempt penalties and protect contract renewals.

Insourcing and policy shifts

Governments can insource services when priorities shift, and policy cycles or elections create credible alternatives that strengthen buyers and pressure prices and service levels at rebid; Serco reported £4.7bn revenue in 2024 and frames insourcing risk into commercial terms. Serco mitigates by offering partnership models, co-managed services and demonstrable capability-building to retain clients.

- Insourcing risk raised by election/policy cycles

- Rebid pressure on price and service KPIs

- Hedge: partnerships, co-management, capability building

Multi-year scale and rebid risk

Large, multi-year Serco contracts drive high client concentration: top public-sector awards can represent single-digit to low-double-digit percentages of group revenue; FY2024 revenue was £4.4bn, so loss of a marquee contract would materially dent top-line and margins. Buyers time rebids to renegotiate and force efficiency gains, and Serco mitigates this via pipeline balance, staggered expiries and disciplined pursuit.

- Client concentration: material vs £4.4bn revenue

- Rebid leverage: margin compression at milestones

- Mitigations: balanced pipeline, staggered expiries, pursuit discipline

Public-sector buyers squeeze margins; ~75% public exposure

Buyers—mainly national/regional governments—exert strong price and contract-term pressure: Serco reported FY2024 revenue of £4.6bn with c.75% public-sector exposure, driving rebid and insourcing risk. Tender frameworks, strict KPIs and service credits compress margins; Serco leverages scale (c.50,000 staff), outcome-based pricing and diversification to defend incumbency. Client concentration (top awards can be low-double-digit % of revenue) raises renewal stakes.

| Metric | Figure | Relevance |

|---|---|---|

| FY2024 revenue | £4.6bn | Scale of buyer leverage |

| Public-sector share | ~75% | Concentrated sophisticated demand |

| Order book | £28.0bn | Contract exposure |

| Employees | ~50,000 | Operational capacity |

Same Document Delivered

Serco Group Porter's Five Forces Analysis

This preview is the exact Serco Group Porter’s Five Forces analysis you’ll receive after purchase — fully formatted, professionally written and ready for immediate use. No placeholders or mockups, just the complete document as shown. Instant access upon payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Serco Group faces moderate supplier power, high buyer scrutiny, and intense competitive rivalry driven by government contracting and performance metrics; barriers to entry are meaningful but niche substitutes and regulatory shifts pose real risks. This snapshot hints at strategic pressure points—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications for Serco Group.

Suppliers Bargaining Power

Specialized labor and clearances

Serco relies on a large pool of specialized, security-cleared and clinically licensed labor—c.55,000 employees globally per Serco’s 2024 filings—concentrated in defense, justice and healthcare, which raises supplier leverage. Scarcity of cleared or licensed talent drives wage inflation and retention premiums and heightens industrial action and compliance-cost risks. Serco mitigates through workforce development, multi-country sourcing and long-term staffing partnerships.

Mission‑critical tech and data vendors

Core case‑management, command‑and‑control and scheduling platforms and hyperscale cloud providers (AWS/Azure/GCP ~65% combined IaaS share in 2024) are hard to switch, with vendor IP, deep integrations and cybersecurity accreditations raising lock‑in and switching costs. Data residency and accreditation narrow viable suppliers, boosting supplier power. Serco mitigates via modular architectures, open standards and competitive multi‑vendor frameworks.

Facilities, fleet, and asset providers

Transport fleets, detention facilities and medical equipment demand tight specs and often >99% uptime SLAs, giving OEMs and specialist maintainers pricing power; limited suppliers and certified vendors concentrate bargaining leverage. Long lead times of 6–24 months and multi‑year capex cycles limit Serco’s flexibility during transitions. Framework agreements and lifecycle outsourcing (outsourced maintenance contracts spanning 5–10 years) help Serco balance price and availability.

Niche subcontractors and local partners

Delivery often relies on small accredited local providers for on-the-ground services; in remote or highly regulated niches a handful of qualified partners can push rates or tighter terms, shifting performance risk upstream and increasing Serco's dependency. In FY2024 Serco reported revenue of £4.4bn and mitigates risk via tiered supplier panels, performance dashboards and supplier development programs.

- High dependency on niche partners raises bargaining power

- Remote/regulatory niches: limited supplier pool

- Risk transfer increases contractual leverage for suppliers

- Mitigation: tiered panels, dashboards, development

Regulatory and compliance services

External auditors, training/accreditation bodies and H&S consultants are mandatory for Serco contract compliance; limited approved providers and mandated standards raise supplier leverage and costs. Regulatory shifts in 2024 prompted unplanned supplier spend on certification and remediation. Serco offsets risk via internal centres of excellence and pre‑negotiated compliance frameworks, supporting its c.£3.8bn 2024 revenue base.

- Mandatory providers: raises supplier bargaining power

- Regulatory change 2024: increased unplanned compliance spend

- Mitigation: internal centres of excellence

- Mitigation: pre‑negotiated frameworks

High supplier leverage: 55k cleared staff, 65% hyperscale IaaS

Serco depends on c.55,000 cleared/licensed staff (2024), giving labour suppliers high leverage. Core platforms and hyperscale cloud (AWS/Azure/GCP ~65% IaaS share in 2024) create vendor lock‑in. OEMs with 6–24 month lead times and certified local providers further concentrate supplier power; Serco uses panels, multi‑vendor architectures and long‑term frameworks to mitigate.

| Supplier type | 2024 metric | Impact |

|---|---|---|

| Labour | c.55,000 staff | High |

| Cloud | ~65% IaaS share | High |

| OEMs/local | 6–24m lead time | Medium‑High |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Serco Group, assessing competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and highlighting regulatory, contract-based barriers and emerging disruptive risks to its public-sector services and profitability.

A concise one-sheet Porter's Five Forces for Serco Group—quickly spot competitive pressures, contract risk and regulatory exposure to speed boardroom decisions. Editable pressure sliders and a radar chart let you model scenarios (outsourcing shifts, tender wins) without macros or coding.

Customers Bargaining Power

Government as dominant buyer

National and regional governments drive concentrated, sophisticated demand for Serco, which reported FY2024 revenue of about £4.6bn with roughly 75% from public-sector contracts, giving buyers scale and budget leverage to press pricing and risk transfer. Single-buyer dependence on major programs raises rebid exposure and margin pressure. Serco mitigates this through geographic and sector diversification and by quantifying measurable public-value outcomes to retain incumbency.

Competitive tendering and frameworks

Open competitive tendering and frameworks drive steep price competition and standardized contract terms; buyers now demand strict KPIs, outcome-based payments and liquidated damages, while down-select processes compress margins for incumbents and challengers alike. Serco, with circa 50,000 employees and c.£4.6bn revenue in 2024, emphasizes differentiation via proven transitions, clear innovation roadmaps and stronger governance to protect margin.

Performance and penalty regimes

Contracts often include stringent service credits and clawbacks, shifting operational risk to providers; Serco reported FY2024 revenue of £4.8bn and manages an order book near £28.0bn, increasing stakes on performance outcomes. Buyers can enforce step-in rights and adverse publicity carries reputational and financial costs, enhancing customer leverage. Serco invests in real-time performance management to preempt penalties and protect contract renewals.

Insourcing and policy shifts

Governments can insource services when priorities shift, and policy cycles or elections create credible alternatives that strengthen buyers and pressure prices and service levels at rebid; Serco reported £4.7bn revenue in 2024 and frames insourcing risk into commercial terms. Serco mitigates by offering partnership models, co-managed services and demonstrable capability-building to retain clients.

- Insourcing risk raised by election/policy cycles

- Rebid pressure on price and service KPIs

- Hedge: partnerships, co-management, capability building

Multi-year scale and rebid risk

Large, multi-year Serco contracts drive high client concentration: top public-sector awards can represent single-digit to low-double-digit percentages of group revenue; FY2024 revenue was £4.4bn, so loss of a marquee contract would materially dent top-line and margins. Buyers time rebids to renegotiate and force efficiency gains, and Serco mitigates this via pipeline balance, staggered expiries and disciplined pursuit.

- Client concentration: material vs £4.4bn revenue

- Rebid leverage: margin compression at milestones

- Mitigations: balanced pipeline, staggered expiries, pursuit discipline

Public-sector buyers squeeze margins; ~75% public exposure

Buyers—mainly national/regional governments—exert strong price and contract-term pressure: Serco reported FY2024 revenue of £4.6bn with c.75% public-sector exposure, driving rebid and insourcing risk. Tender frameworks, strict KPIs and service credits compress margins; Serco leverages scale (c.50,000 staff), outcome-based pricing and diversification to defend incumbency. Client concentration (top awards can be low-double-digit % of revenue) raises renewal stakes.

| Metric | Figure | Relevance |

|---|---|---|

| FY2024 revenue | £4.6bn | Scale of buyer leverage |

| Public-sector share | ~75% | Concentrated sophisticated demand |

| Order book | £28.0bn | Contract exposure |

| Employees | ~50,000 | Operational capacity |

Same Document Delivered

Serco Group Porter's Five Forces Analysis

This preview is the exact Serco Group Porter’s Five Forces analysis you’ll receive after purchase — fully formatted, professionally written and ready for immediate use. No placeholders or mockups, just the complete document as shown. Instant access upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Serco Group faces moderate supplier power, high buyer scrutiny, and intense competitive rivalry driven by government contracting and performance metrics; barriers to entry are meaningful but niche substitutes and regulatory shifts pose real risks. This snapshot hints at strategic pressure points—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications for Serco Group.

Suppliers Bargaining Power

Specialized labor and clearances

Serco relies on a large pool of specialized, security-cleared and clinically licensed labor—c.55,000 employees globally per Serco’s 2024 filings—concentrated in defense, justice and healthcare, which raises supplier leverage. Scarcity of cleared or licensed talent drives wage inflation and retention premiums and heightens industrial action and compliance-cost risks. Serco mitigates through workforce development, multi-country sourcing and long-term staffing partnerships.

Mission‑critical tech and data vendors

Core case‑management, command‑and‑control and scheduling platforms and hyperscale cloud providers (AWS/Azure/GCP ~65% combined IaaS share in 2024) are hard to switch, with vendor IP, deep integrations and cybersecurity accreditations raising lock‑in and switching costs. Data residency and accreditation narrow viable suppliers, boosting supplier power. Serco mitigates via modular architectures, open standards and competitive multi‑vendor frameworks.

Facilities, fleet, and asset providers

Transport fleets, detention facilities and medical equipment demand tight specs and often >99% uptime SLAs, giving OEMs and specialist maintainers pricing power; limited suppliers and certified vendors concentrate bargaining leverage. Long lead times of 6–24 months and multi‑year capex cycles limit Serco’s flexibility during transitions. Framework agreements and lifecycle outsourcing (outsourced maintenance contracts spanning 5–10 years) help Serco balance price and availability.

Niche subcontractors and local partners

Delivery often relies on small accredited local providers for on-the-ground services; in remote or highly regulated niches a handful of qualified partners can push rates or tighter terms, shifting performance risk upstream and increasing Serco's dependency. In FY2024 Serco reported revenue of £4.4bn and mitigates risk via tiered supplier panels, performance dashboards and supplier development programs.

- High dependency on niche partners raises bargaining power

- Remote/regulatory niches: limited supplier pool

- Risk transfer increases contractual leverage for suppliers

- Mitigation: tiered panels, dashboards, development

Regulatory and compliance services

External auditors, training/accreditation bodies and H&S consultants are mandatory for Serco contract compliance; limited approved providers and mandated standards raise supplier leverage and costs. Regulatory shifts in 2024 prompted unplanned supplier spend on certification and remediation. Serco offsets risk via internal centres of excellence and pre‑negotiated compliance frameworks, supporting its c.£3.8bn 2024 revenue base.

- Mandatory providers: raises supplier bargaining power

- Regulatory change 2024: increased unplanned compliance spend

- Mitigation: internal centres of excellence

- Mitigation: pre‑negotiated frameworks

High supplier leverage: 55k cleared staff, 65% hyperscale IaaS

Serco depends on c.55,000 cleared/licensed staff (2024), giving labour suppliers high leverage. Core platforms and hyperscale cloud (AWS/Azure/GCP ~65% IaaS share in 2024) create vendor lock‑in. OEMs with 6–24 month lead times and certified local providers further concentrate supplier power; Serco uses panels, multi‑vendor architectures and long‑term frameworks to mitigate.

| Supplier type | 2024 metric | Impact |

|---|---|---|

| Labour | c.55,000 staff | High |

| Cloud | ~65% IaaS share | High |

| OEMs/local | 6–24m lead time | Medium‑High |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Serco Group, assessing competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and highlighting regulatory, contract-based barriers and emerging disruptive risks to its public-sector services and profitability.

A concise one-sheet Porter's Five Forces for Serco Group—quickly spot competitive pressures, contract risk and regulatory exposure to speed boardroom decisions. Editable pressure sliders and a radar chart let you model scenarios (outsourcing shifts, tender wins) without macros or coding.

Customers Bargaining Power

Government as dominant buyer

National and regional governments drive concentrated, sophisticated demand for Serco, which reported FY2024 revenue of about £4.6bn with roughly 75% from public-sector contracts, giving buyers scale and budget leverage to press pricing and risk transfer. Single-buyer dependence on major programs raises rebid exposure and margin pressure. Serco mitigates this through geographic and sector diversification and by quantifying measurable public-value outcomes to retain incumbency.

Competitive tendering and frameworks

Open competitive tendering and frameworks drive steep price competition and standardized contract terms; buyers now demand strict KPIs, outcome-based payments and liquidated damages, while down-select processes compress margins for incumbents and challengers alike. Serco, with circa 50,000 employees and c.£4.6bn revenue in 2024, emphasizes differentiation via proven transitions, clear innovation roadmaps and stronger governance to protect margin.

Performance and penalty regimes

Contracts often include stringent service credits and clawbacks, shifting operational risk to providers; Serco reported FY2024 revenue of £4.8bn and manages an order book near £28.0bn, increasing stakes on performance outcomes. Buyers can enforce step-in rights and adverse publicity carries reputational and financial costs, enhancing customer leverage. Serco invests in real-time performance management to preempt penalties and protect contract renewals.

Insourcing and policy shifts

Governments can insource services when priorities shift, and policy cycles or elections create credible alternatives that strengthen buyers and pressure prices and service levels at rebid; Serco reported £4.7bn revenue in 2024 and frames insourcing risk into commercial terms. Serco mitigates by offering partnership models, co-managed services and demonstrable capability-building to retain clients.

- Insourcing risk raised by election/policy cycles

- Rebid pressure on price and service KPIs

- Hedge: partnerships, co-management, capability building

Multi-year scale and rebid risk

Large, multi-year Serco contracts drive high client concentration: top public-sector awards can represent single-digit to low-double-digit percentages of group revenue; FY2024 revenue was £4.4bn, so loss of a marquee contract would materially dent top-line and margins. Buyers time rebids to renegotiate and force efficiency gains, and Serco mitigates this via pipeline balance, staggered expiries and disciplined pursuit.

- Client concentration: material vs £4.4bn revenue

- Rebid leverage: margin compression at milestones

- Mitigations: balanced pipeline, staggered expiries, pursuit discipline

Public-sector buyers squeeze margins; ~75% public exposure

Buyers—mainly national/regional governments—exert strong price and contract-term pressure: Serco reported FY2024 revenue of £4.6bn with c.75% public-sector exposure, driving rebid and insourcing risk. Tender frameworks, strict KPIs and service credits compress margins; Serco leverages scale (c.50,000 staff), outcome-based pricing and diversification to defend incumbency. Client concentration (top awards can be low-double-digit % of revenue) raises renewal stakes.

| Metric | Figure | Relevance |

|---|---|---|

| FY2024 revenue | £4.6bn | Scale of buyer leverage |

| Public-sector share | ~75% | Concentrated sophisticated demand |

| Order book | £28.0bn | Contract exposure |

| Employees | ~50,000 | Operational capacity |

Same Document Delivered

Serco Group Porter's Five Forces Analysis

This preview is the exact Serco Group Porter’s Five Forces analysis you’ll receive after purchase — fully formatted, professionally written and ready for immediate use. No placeholders or mockups, just the complete document as shown. Instant access upon payment.