ServiceTitan Porter's Five Forces Analysis

From Overview to Strategy Blueprint

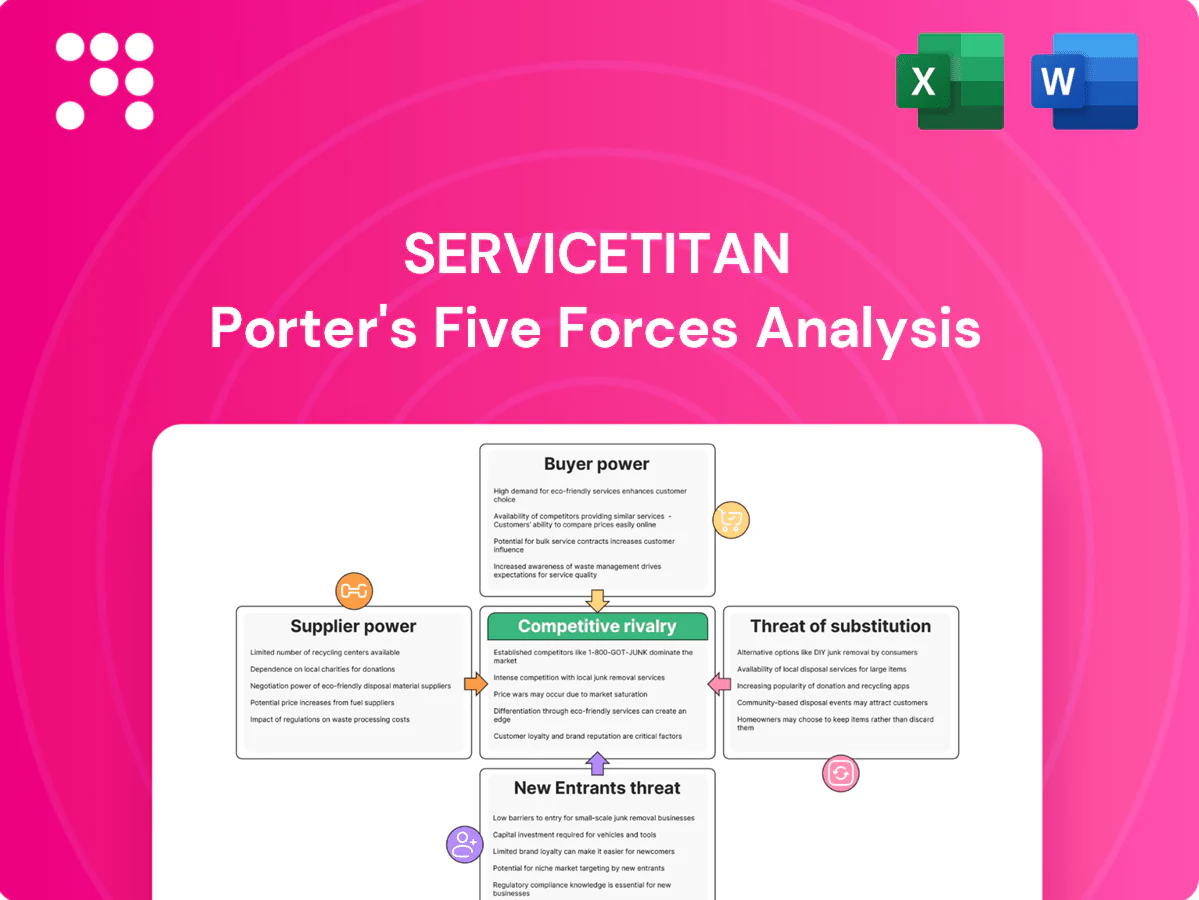

ServiceTitan’s Porter's Five Forces snapshot highlights strong buyer expectations, moderate supplier leverage, and rising competitive and substitute pressures driven by software innovation and consolidation. It flags key strategic risks and pockets of advantage for growth and margin defense. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated cloud and platform dependencies

ServiceTitan depends on hyperscale IaaS and mobile app ecosystems dominated by a few providers (AWS ~32%, Microsoft Azure ~23%, Google Cloud ~11% global market share in 2024 per Synergy), giving suppliers leverage on pricing, roadmap access, and compliance mandates. Adopting multi-cloud can reduce single-vendor risk but typically raises operational complexity and costs by double-digit percentages in total cost of ownership. Committing to long-term contracts secures meaningful discounts yet further entrenches supplier dependency.

Payments, SMS, and mapping API providers

Key ServiceTitan workflows rely on third-party payments, SMS and mapping APIs, with industry payment fees ~1.5–3% per transaction (2024), SMS costs ~$0.005–$0.03/msg and geospatial calls $0.002–$0.01/request, so vendors can raise fees, rate-limit or alter terms and hit unit economics and reliability. Volume-based pricing and scale give ServiceTitan negotiation leverage, but swapping core transaction rails or comms stacks requires substantial engineering time and cost.

Specialized data and integrations

OEM parts catalogs, financing partners and three major credit bureaus (Experian, TransUnion, Equifax) feed critical features like estimates and embedded finance, and because these suppliers are fewer and highly specialized their bargaining power is elevated. Co-marketing and revenue-sharing deals can align incentives but create multi-year lock-ins. Loss or degradation of any feed can materially impair differentiated modules and customer retention.

Talent and third-party implementers

Senior engineers, product talent and certified solution partners are scarce in vertical SaaS, concentrating bargaining power among suppliers. US senior engineer compensation often exceeds 150,000–200,000 USD, and third‑party implementer rates command sizable premiums, raising COGS for platforms like ServiceTitan. Deep knowledge of home‑services workflows further narrows the pool; retention programs and partner enablement cut risk but add ongoing cost.

- Talent scarcity: senior engineers scarce

- Compensation: typically 150k–200k+ USD

- Specialization: home‑services domain narrows suppliers

- Mitigation: retention/enablement reduce risk but increase expense

Security, compliance, and cloud tooling

Security, compliance, and cloud tooling exert high supplier power for ServiceTitan because PCI and SOC 2 tooling, observability, and security stacks are sticky, priced at a premium, and estimated in 2024 to comprise a ~13B USD cloud security tooling market with vendor premiums often 15–30%.

Vendors bundle features to capture share-of-wallet and regulatory shifts can force mandatory upgrades on supplier terms; supplier diversification improves resilience but adds integration and ops overhead.

- sticky-premium: 15–30% pricing uplift

- market-size-2024: ~13B USD

- bundling-increases-share-of-wallet

- diversification-tradeoff: resilience vs ops cost

Hyperscale cloud, payments, SMS and scarce senior engineers elevate supplier power, raising costs

ServiceTitan faces elevated supplier power from hyperscale IaaS (AWS 32%, Azure 23%, GCP 11% 2024), payments (fees 1.5–3%), SMS ($0.005–$0.03/msg), geospatial APIs ($0.002–$0.01/call), cloud security tooling (~$13B market, 15–30% premium) and scarce senior engineers (USD 150k–200k+), making diversification costly and long-term contracts common mitigants.

| Metric | 2024 Value |

|---|---|

| AWS/Azure/GCP share | 32% / 23% / 11% |

| Payment fees | 1.5–3% |

| SMS | $0.005–$0.03/msg |

| Cloud security market | ~$13B (15–30% premium) |

| Senior engineer comp | $150k–$200k+ |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks specific to ServiceTitan, providing a detailed assessment of rivalry, supplier and buyer power, substitutes, and entrant threats. Identifies disruptive forces and strategic levers that impact ServiceTitan’s pricing, profitability, and defensibility within the field service software market.

Actionable Porter's Five Forces for ServiceTitan—clear one-sheet summary with customizable pressure levels and radar visualization, ready to drop into decks and link into Excel dashboards to simplify strategic decisions and relieve analyst workload.

Customers Bargaining Power

Fragmented SMB base with some large accounts

Home service contractors are highly numerous and fragmented—the US had about 33 million small businesses in 2024 (SBA), which limits individual buyer power for ServiceTitan. Multi-location enterprises and franchisors, however, can negotiate discounts and custom features, driving higher per-account value. Losing a few large logos can materially affect ARR concentration for a growing SaaS, while SMB churn risk pressures pricing and demands faster support responsiveness.

High switching costs and data lock-in

Deep workflow embedding, years of historical job and customer data, dozens of integrations and multi-week technician training create high switching costs for ServiceTitan clients, making migration risk and downtime key deterrents to switching and softening price pressure; competitors offer migration tools that partly offset stickiness, while multi-year contracts and prepaid terms further lock in customers as of 2024.

Price sensitivity and ROI scrutiny

Contractors judge software by booked revenue uplift, tech utilization and dispatch efficiency, often expecting 10–20% revenue uplift and 20–40% higher tech utilization from platform adoption. Economic downturns spike discount requests and plan downgrades, with vendors reporting churn pressure rising ~10–15%. Clear ROI proof—faster invoicing (DSO cut up to 30–50%), higher ticket size—reduces price pressure, while tiered packaging lets customers self-select and protects ARPU.

Information transparency and reviews

Peer forums, G2 and Capterra reviews and trade association feeds sharply raise transparency around ServiceTitan features and pricing, lifting buyer expectations and negotiation leverage; proof-of-concept trials and customer references increasingly determine deal wins, while public comparisons amplify urgency to close feature gaps.

- Peer forums boost visibility

- G2/Capterra shape purchase decisions

- Trade associations set benchmarks

- Trials and refs critical to close deals

Demand for integrations and openness

Buyers demand seamless links to accounting, financing, and marketing tools, making integration breadth a clear negotiation lever and potential deal blocker for ServiceTitan; inability to connect elevates churn risk to more open rivals. Open APIs lower buyer anxiety but increase delivery and support commitments, shifting bargaining power toward customers seeking modular stacks. Integration promises are often weighted as heavily as price in renewal decisions.

- Integration breadth = negotiation leverage

- Open APIs reduce anxiety but raise delivery burden

- Poor integration increases churn to open competitors

Chains concentrate ARR; integrations raise switching costs, reviews and migration sway churn

ServiceTitan faces limited individual buyer power given ~33 million US small businesses (SBA 2024), but multi-location chains drive negotiation leverage and ARR concentration risk. High switching costs from integrations, historical data and training soften price pressure; competitors' migration tools and downturns raise churn ~10–15% (vendor reports 2024). Integration breadth and G2/Capterra reviews are primary customer bargaining levers.

| Metric | 2024 value |

|---|---|

| US small businesses | ~33,000,000 (SBA) |

| Churn pressure rise | ~10–15% (vendor reports) |

| Expected revenue uplift | 10–20% (customer benchmarks) |

| DSO reduction | 30–50% (customer ROI cases) |

Preview the Actual Deliverable

ServiceTitan Porter's Five Forces Analysis

This preview shows the exact ServiceTitan Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The file is fully formatted, professionally written and ready for immediate download and use. What you see here is the complete deliverable. Instant access is granted upon payment.

From Overview to Strategy Blueprint

ServiceTitan’s Porter's Five Forces snapshot highlights strong buyer expectations, moderate supplier leverage, and rising competitive and substitute pressures driven by software innovation and consolidation. It flags key strategic risks and pockets of advantage for growth and margin defense. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated cloud and platform dependencies

ServiceTitan depends on hyperscale IaaS and mobile app ecosystems dominated by a few providers (AWS ~32%, Microsoft Azure ~23%, Google Cloud ~11% global market share in 2024 per Synergy), giving suppliers leverage on pricing, roadmap access, and compliance mandates. Adopting multi-cloud can reduce single-vendor risk but typically raises operational complexity and costs by double-digit percentages in total cost of ownership. Committing to long-term contracts secures meaningful discounts yet further entrenches supplier dependency.

Payments, SMS, and mapping API providers

Key ServiceTitan workflows rely on third-party payments, SMS and mapping APIs, with industry payment fees ~1.5–3% per transaction (2024), SMS costs ~$0.005–$0.03/msg and geospatial calls $0.002–$0.01/request, so vendors can raise fees, rate-limit or alter terms and hit unit economics and reliability. Volume-based pricing and scale give ServiceTitan negotiation leverage, but swapping core transaction rails or comms stacks requires substantial engineering time and cost.

Specialized data and integrations

OEM parts catalogs, financing partners and three major credit bureaus (Experian, TransUnion, Equifax) feed critical features like estimates and embedded finance, and because these suppliers are fewer and highly specialized their bargaining power is elevated. Co-marketing and revenue-sharing deals can align incentives but create multi-year lock-ins. Loss or degradation of any feed can materially impair differentiated modules and customer retention.

Talent and third-party implementers

Senior engineers, product talent and certified solution partners are scarce in vertical SaaS, concentrating bargaining power among suppliers. US senior engineer compensation often exceeds 150,000–200,000 USD, and third‑party implementer rates command sizable premiums, raising COGS for platforms like ServiceTitan. Deep knowledge of home‑services workflows further narrows the pool; retention programs and partner enablement cut risk but add ongoing cost.

- Talent scarcity: senior engineers scarce

- Compensation: typically 150k–200k+ USD

- Specialization: home‑services domain narrows suppliers

- Mitigation: retention/enablement reduce risk but increase expense

Security, compliance, and cloud tooling

Security, compliance, and cloud tooling exert high supplier power for ServiceTitan because PCI and SOC 2 tooling, observability, and security stacks are sticky, priced at a premium, and estimated in 2024 to comprise a ~13B USD cloud security tooling market with vendor premiums often 15–30%.

Vendors bundle features to capture share-of-wallet and regulatory shifts can force mandatory upgrades on supplier terms; supplier diversification improves resilience but adds integration and ops overhead.

- sticky-premium: 15–30% pricing uplift

- market-size-2024: ~13B USD

- bundling-increases-share-of-wallet

- diversification-tradeoff: resilience vs ops cost

Hyperscale cloud, payments, SMS and scarce senior engineers elevate supplier power, raising costs

ServiceTitan faces elevated supplier power from hyperscale IaaS (AWS 32%, Azure 23%, GCP 11% 2024), payments (fees 1.5–3%), SMS ($0.005–$0.03/msg), geospatial APIs ($0.002–$0.01/call), cloud security tooling (~$13B market, 15–30% premium) and scarce senior engineers (USD 150k–200k+), making diversification costly and long-term contracts common mitigants.

| Metric | 2024 Value |

|---|---|

| AWS/Azure/GCP share | 32% / 23% / 11% |

| Payment fees | 1.5–3% |

| SMS | $0.005–$0.03/msg |

| Cloud security market | ~$13B (15–30% premium) |

| Senior engineer comp | $150k–$200k+ |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks specific to ServiceTitan, providing a detailed assessment of rivalry, supplier and buyer power, substitutes, and entrant threats. Identifies disruptive forces and strategic levers that impact ServiceTitan’s pricing, profitability, and defensibility within the field service software market.

Actionable Porter's Five Forces for ServiceTitan—clear one-sheet summary with customizable pressure levels and radar visualization, ready to drop into decks and link into Excel dashboards to simplify strategic decisions and relieve analyst workload.

Customers Bargaining Power

Fragmented SMB base with some large accounts

Home service contractors are highly numerous and fragmented—the US had about 33 million small businesses in 2024 (SBA), which limits individual buyer power for ServiceTitan. Multi-location enterprises and franchisors, however, can negotiate discounts and custom features, driving higher per-account value. Losing a few large logos can materially affect ARR concentration for a growing SaaS, while SMB churn risk pressures pricing and demands faster support responsiveness.

High switching costs and data lock-in

Deep workflow embedding, years of historical job and customer data, dozens of integrations and multi-week technician training create high switching costs for ServiceTitan clients, making migration risk and downtime key deterrents to switching and softening price pressure; competitors offer migration tools that partly offset stickiness, while multi-year contracts and prepaid terms further lock in customers as of 2024.

Price sensitivity and ROI scrutiny

Contractors judge software by booked revenue uplift, tech utilization and dispatch efficiency, often expecting 10–20% revenue uplift and 20–40% higher tech utilization from platform adoption. Economic downturns spike discount requests and plan downgrades, with vendors reporting churn pressure rising ~10–15%. Clear ROI proof—faster invoicing (DSO cut up to 30–50%), higher ticket size—reduces price pressure, while tiered packaging lets customers self-select and protects ARPU.

Information transparency and reviews

Peer forums, G2 and Capterra reviews and trade association feeds sharply raise transparency around ServiceTitan features and pricing, lifting buyer expectations and negotiation leverage; proof-of-concept trials and customer references increasingly determine deal wins, while public comparisons amplify urgency to close feature gaps.

- Peer forums boost visibility

- G2/Capterra shape purchase decisions

- Trade associations set benchmarks

- Trials and refs critical to close deals

Demand for integrations and openness

Buyers demand seamless links to accounting, financing, and marketing tools, making integration breadth a clear negotiation lever and potential deal blocker for ServiceTitan; inability to connect elevates churn risk to more open rivals. Open APIs lower buyer anxiety but increase delivery and support commitments, shifting bargaining power toward customers seeking modular stacks. Integration promises are often weighted as heavily as price in renewal decisions.

- Integration breadth = negotiation leverage

- Open APIs reduce anxiety but raise delivery burden

- Poor integration increases churn to open competitors

Chains concentrate ARR; integrations raise switching costs, reviews and migration sway churn

ServiceTitan faces limited individual buyer power given ~33 million US small businesses (SBA 2024), but multi-location chains drive negotiation leverage and ARR concentration risk. High switching costs from integrations, historical data and training soften price pressure; competitors' migration tools and downturns raise churn ~10–15% (vendor reports 2024). Integration breadth and G2/Capterra reviews are primary customer bargaining levers.

| Metric | 2024 value |

|---|---|

| US small businesses | ~33,000,000 (SBA) |

| Churn pressure rise | ~10–15% (vendor reports) |

| Expected revenue uplift | 10–20% (customer benchmarks) |

| DSO reduction | 30–50% (customer ROI cases) |

Preview the Actual Deliverable

ServiceTitan Porter's Five Forces Analysis

This preview shows the exact ServiceTitan Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The file is fully formatted, professionally written and ready for immediate download and use. What you see here is the complete deliverable. Instant access is granted upon payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

ServiceTitan’s Porter's Five Forces snapshot highlights strong buyer expectations, moderate supplier leverage, and rising competitive and substitute pressures driven by software innovation and consolidation. It flags key strategic risks and pockets of advantage for growth and margin defense. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated cloud and platform dependencies

ServiceTitan depends on hyperscale IaaS and mobile app ecosystems dominated by a few providers (AWS ~32%, Microsoft Azure ~23%, Google Cloud ~11% global market share in 2024 per Synergy), giving suppliers leverage on pricing, roadmap access, and compliance mandates. Adopting multi-cloud can reduce single-vendor risk but typically raises operational complexity and costs by double-digit percentages in total cost of ownership. Committing to long-term contracts secures meaningful discounts yet further entrenches supplier dependency.

Payments, SMS, and mapping API providers

Key ServiceTitan workflows rely on third-party payments, SMS and mapping APIs, with industry payment fees ~1.5–3% per transaction (2024), SMS costs ~$0.005–$0.03/msg and geospatial calls $0.002–$0.01/request, so vendors can raise fees, rate-limit or alter terms and hit unit economics and reliability. Volume-based pricing and scale give ServiceTitan negotiation leverage, but swapping core transaction rails or comms stacks requires substantial engineering time and cost.

Specialized data and integrations

OEM parts catalogs, financing partners and three major credit bureaus (Experian, TransUnion, Equifax) feed critical features like estimates and embedded finance, and because these suppliers are fewer and highly specialized their bargaining power is elevated. Co-marketing and revenue-sharing deals can align incentives but create multi-year lock-ins. Loss or degradation of any feed can materially impair differentiated modules and customer retention.

Talent and third-party implementers

Senior engineers, product talent and certified solution partners are scarce in vertical SaaS, concentrating bargaining power among suppliers. US senior engineer compensation often exceeds 150,000–200,000 USD, and third‑party implementer rates command sizable premiums, raising COGS for platforms like ServiceTitan. Deep knowledge of home‑services workflows further narrows the pool; retention programs and partner enablement cut risk but add ongoing cost.

- Talent scarcity: senior engineers scarce

- Compensation: typically 150k–200k+ USD

- Specialization: home‑services domain narrows suppliers

- Mitigation: retention/enablement reduce risk but increase expense

Security, compliance, and cloud tooling

Security, compliance, and cloud tooling exert high supplier power for ServiceTitan because PCI and SOC 2 tooling, observability, and security stacks are sticky, priced at a premium, and estimated in 2024 to comprise a ~13B USD cloud security tooling market with vendor premiums often 15–30%.

Vendors bundle features to capture share-of-wallet and regulatory shifts can force mandatory upgrades on supplier terms; supplier diversification improves resilience but adds integration and ops overhead.

- sticky-premium: 15–30% pricing uplift

- market-size-2024: ~13B USD

- bundling-increases-share-of-wallet

- diversification-tradeoff: resilience vs ops cost

Hyperscale cloud, payments, SMS and scarce senior engineers elevate supplier power, raising costs

ServiceTitan faces elevated supplier power from hyperscale IaaS (AWS 32%, Azure 23%, GCP 11% 2024), payments (fees 1.5–3%), SMS ($0.005–$0.03/msg), geospatial APIs ($0.002–$0.01/call), cloud security tooling (~$13B market, 15–30% premium) and scarce senior engineers (USD 150k–200k+), making diversification costly and long-term contracts common mitigants.

| Metric | 2024 Value |

|---|---|

| AWS/Azure/GCP share | 32% / 23% / 11% |

| Payment fees | 1.5–3% |

| SMS | $0.005–$0.03/msg |

| Cloud security market | ~$13B (15–30% premium) |

| Senior engineer comp | $150k–$200k+ |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks specific to ServiceTitan, providing a detailed assessment of rivalry, supplier and buyer power, substitutes, and entrant threats. Identifies disruptive forces and strategic levers that impact ServiceTitan’s pricing, profitability, and defensibility within the field service software market.

Actionable Porter's Five Forces for ServiceTitan—clear one-sheet summary with customizable pressure levels and radar visualization, ready to drop into decks and link into Excel dashboards to simplify strategic decisions and relieve analyst workload.

Customers Bargaining Power

Fragmented SMB base with some large accounts

Home service contractors are highly numerous and fragmented—the US had about 33 million small businesses in 2024 (SBA), which limits individual buyer power for ServiceTitan. Multi-location enterprises and franchisors, however, can negotiate discounts and custom features, driving higher per-account value. Losing a few large logos can materially affect ARR concentration for a growing SaaS, while SMB churn risk pressures pricing and demands faster support responsiveness.

High switching costs and data lock-in

Deep workflow embedding, years of historical job and customer data, dozens of integrations and multi-week technician training create high switching costs for ServiceTitan clients, making migration risk and downtime key deterrents to switching and softening price pressure; competitors offer migration tools that partly offset stickiness, while multi-year contracts and prepaid terms further lock in customers as of 2024.

Price sensitivity and ROI scrutiny

Contractors judge software by booked revenue uplift, tech utilization and dispatch efficiency, often expecting 10–20% revenue uplift and 20–40% higher tech utilization from platform adoption. Economic downturns spike discount requests and plan downgrades, with vendors reporting churn pressure rising ~10–15%. Clear ROI proof—faster invoicing (DSO cut up to 30–50%), higher ticket size—reduces price pressure, while tiered packaging lets customers self-select and protects ARPU.

Information transparency and reviews

Peer forums, G2 and Capterra reviews and trade association feeds sharply raise transparency around ServiceTitan features and pricing, lifting buyer expectations and negotiation leverage; proof-of-concept trials and customer references increasingly determine deal wins, while public comparisons amplify urgency to close feature gaps.

- Peer forums boost visibility

- G2/Capterra shape purchase decisions

- Trade associations set benchmarks

- Trials and refs critical to close deals

Demand for integrations and openness

Buyers demand seamless links to accounting, financing, and marketing tools, making integration breadth a clear negotiation lever and potential deal blocker for ServiceTitan; inability to connect elevates churn risk to more open rivals. Open APIs lower buyer anxiety but increase delivery and support commitments, shifting bargaining power toward customers seeking modular stacks. Integration promises are often weighted as heavily as price in renewal decisions.

- Integration breadth = negotiation leverage

- Open APIs reduce anxiety but raise delivery burden

- Poor integration increases churn to open competitors

Chains concentrate ARR; integrations raise switching costs, reviews and migration sway churn

ServiceTitan faces limited individual buyer power given ~33 million US small businesses (SBA 2024), but multi-location chains drive negotiation leverage and ARR concentration risk. High switching costs from integrations, historical data and training soften price pressure; competitors' migration tools and downturns raise churn ~10–15% (vendor reports 2024). Integration breadth and G2/Capterra reviews are primary customer bargaining levers.

| Metric | 2024 value |

|---|---|

| US small businesses | ~33,000,000 (SBA) |

| Churn pressure rise | ~10–15% (vendor reports) |

| Expected revenue uplift | 10–20% (customer benchmarks) |

| DSO reduction | 30–50% (customer ROI cases) |

Preview the Actual Deliverable

ServiceTitan Porter's Five Forces Analysis

This preview shows the exact ServiceTitan Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The file is fully formatted, professionally written and ready for immediate download and use. What you see here is the complete deliverable. Instant access is granted upon payment.