Servier Porter's Five Forces Analysis

From Overview to Strategy Blueprint

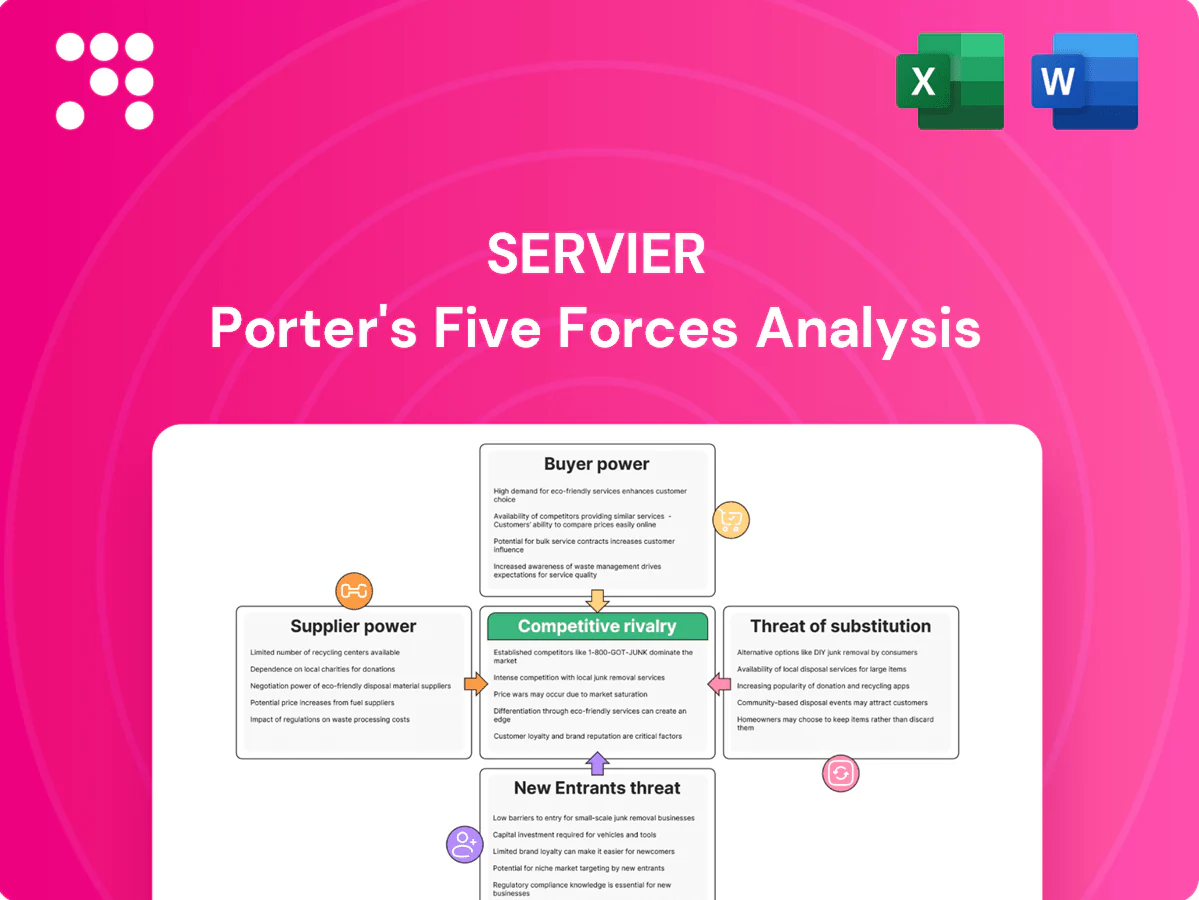

Servier’s Porter's Five Forces analysis outlines supplier and buyer power, rivalry intensity, threat of substitutes and new entrants, highlighting the regulatory and innovation-driven pressures shaping its pharma position. This snapshot shows key dynamics and strategic implications. Unlock the full Porter's Five Forces Analysis to explore Servier’s competitive dynamics and market pressures in detail.

Suppliers Bargaining Power

Specialty APIs and biologics

Servier depends on complex APIs and biologics with few qualified sources, raising supplier leverage as biologics represented about 30% of global pharma sales in 2024; switching requires supplier validation (commonly 6–18 months) plus regulatory filings often taking 6–24 months. Concentration increases risk, but multi-sourcing across 2–3 qualified suppliers and long-term contracts reduce disruption; Servier's vertical integration in key steps further limits exposure.

GMP compliance and quality

Suppliers must meet stringent GMP and regulatory standards, narrowing the pool to certified manufacturers; audit-related compliance costs often exceed €100,000 annually per supplier, raising their bargaining leverage. Frequent regulatory audits and remediation increase supplier negotiating power, but the risk of suspension, recalls or multi-million euro fines for non-compliance constrains opportunistic pricing. Servier’s certified quality systems and supplier KPIs enable benchmarking and phased substitution, reducing long-term supplier dependence.

Equipment and CDMO capacity

Single-use systems, sterile fill-finish lines and high-potency suites remain key bottlenecks for Servier, with oncology CDMO utilization exceeding 90% in 2024 and industry lead times of 12–18 months. Tight global CDMO capacity in oncology elevates supplier influence and raises effective switching costs due to complex tech transfers. Strategic capacity reservations and dual-sourcing materially reduce supplier leverage.

Proprietary tech and reagents

Some manufacturing steps require proprietary enzymes, vectors or catalysts, creating high dependency on IP-protected vendors; licensing and supply agreements often include price-escalation clauses that favor suppliers, while co-development partnerships increasingly serve to share value and secure supply continuity, with 2024 industry reports noting growing supplier consolidation in key reagent categories.

- IP dependence

- Escalation clauses

- Supply concentration

- Co-development as mitigation

Logistics and cold chain

Temperature-controlled distribution and specialized packaging add critical vendor nodes, raising dependency on carriers and packaging firms. Disruptions pushed pharma cold-chain costs up about 12% in 2023–24, strengthening key providers' leverage. Competitive logistics markets and framework agreements limit pricing pressure, while redundant lanes and inventory buffers reduce vulnerability.

- Critical nodes: carriers, cold-pack suppliers

- Cost rise: ~12% (2023–24)

- Mitigants: framework agreements, competition

- Resilience: redundant lanes, inventory buffers

Biologics 30%, CDMO util. >90% heighten supplier leverage

Servier faces high supplier leverage from concentrated API/biologics supply (biologics ≈30% of global pharma sales in 2024), IP-protected reagents and oncology CDMO utilization >90% in 2024, elevating switching costs and lead times; mitigants include multi-sourcing, long-term contracts, co-development and vertical integration.

| Metric | 2024 | Implication |

|---|---|---|

| Biologics share | ≈30% | High supplier value |

| CDMO oncology util. | >90% | Capacity tightness |

| Audit cost/supplier | >€100k/yr | Raises supplier leverage |

| Cold-chain cost rise | ~12% (2023–24) | Higher logistics dependence |

What is included in the product

Tailored Porter's Five Forces analysis for Servier that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and intensity of rivalry, highlighting disruptive forces and strategic implications for pricing, market share, and defensive barriers.

A concise one-sheet summarizing Servier's Five Forces—relieves analysis bottlenecks so teams can make fast, confident strategic decisions and drop-ready slides for investors or board meetings.

Customers Bargaining Power

Payers and HTA bodies

National payers and HTA bodies negotiate aggressively on price and access as value frameworks tighten margins; NICE historically uses a £20,000–£30,000 per QALY threshold. With the global pharma market near $1.6 trillion in 2024, payers increasingly demand outcome-linked pricing that squeezes non-differentiated therapies. Demonstrable clinical and real-world outcomes are essential to defend price, and Servier’s R&D focus supports the evidence generation needed to counter buyer power.

Hospital and GPO consolidation

Hospital systems and GPO consolidation concentrates buying power—top GPOs control about 70% of acute-care purchasing—so bundled tenders drive deeper discounts and squeeze margins. Preferred formulary placement is now decisive to sustain volumes. Servier must compete on contracting value, patient-support services and rock-solid supply reliability to win commitments.

Physician and patient influence

Prescribers and patients prioritize efficacy, safety and convenience over price, tempering pure price-based bargaining; the global pharmaceutical market was estimated at about $1.4 trillion in 2024, so clinical value often trumps discounting. Strong clinical differentiation lowers price elasticity and strengthens supplier leverage, while patient support programs—rising across specialty products—improve adherence and brand perception. In crowded classes, brand loyalty erodes and buyer leverage increases.

International reference pricing

International reference pricing used by over 30 countries in 2024 lets payers anchor negotiations to lower-price markets, forcing downward pressure on list and net prices; launch sequencing and managed entry agreements are therefore deployed to protect price corridors and preserve revenue. Parallel trade in the EU intensifies spillover risk across member states, so Servier must tailor pricing by indication and market and use indication-based contracts to mitigate cross-border leakage.

- IRP reach: over 30 countries (2024)

- Mitigation: launch sequencing + managed entry agreements

- EU pressure: parallel trade increases spillover risk

- Strategy: indication- and market-specific pricing + contracts

Biosimilar and generic options

Availability of biosimilar and generic alternatives strengthens buyer bargaining: EU tender-driven markets saw biologic prices fall up to 60% post-LOE (infliximab/adalimumab), with typical post-LOE erosion of 30–70% within 12 months. Tender switches accelerate volume loss for originators. Differentiated formulations or combination regimens and lifecycle evidence updates can preserve a 10–30% premium.

- Buyer leverage: lower-cost alternatives increase negotiation power

- Tenders: drive faster switches and steep price erosion

- Differentiation: formulations/regimens slow substitution

- Lifecycle: evidence updates sustain value (≈10–30% premium)

Outcome pricing grows; $1.6T market tightens, GPOs ~70%

Payers and HTA bodies (NICE £20,000–30,000/QALY) enforce outcome-linked pricing as the $1.6T pharma market (2024) tightens margins; IRP in >30 countries and EU parallel trade depress prices. GPOs control ~70% acute purchasing, driving tender discounts; biosimilar LOE cuts reach up to 60%. Servier must deploy indication-based pricing, managed entry and strong real-world evidence to protect value.

| Metric | 2024 Value |

|---|---|

| Global pharma market | $1.6T |

| GPO acute purchasing | ~70% |

| IRP reach | >30 countries |

| Biosimilar LOE price fall | up to 60% |

What You See Is What You Get

Servier Porter's Five Forces Analysis

This preview shows the exact Servier Porter's Five Forces Analysis you'll receive—no placeholders or samples. The document displayed is the final, fully formatted file ready for download immediately after purchase. You're viewing the same comprehensive analysis that will be available to you upon payment.

From Overview to Strategy Blueprint

Servier’s Porter's Five Forces analysis outlines supplier and buyer power, rivalry intensity, threat of substitutes and new entrants, highlighting the regulatory and innovation-driven pressures shaping its pharma position. This snapshot shows key dynamics and strategic implications. Unlock the full Porter's Five Forces Analysis to explore Servier’s competitive dynamics and market pressures in detail.

Suppliers Bargaining Power

Specialty APIs and biologics

Servier depends on complex APIs and biologics with few qualified sources, raising supplier leverage as biologics represented about 30% of global pharma sales in 2024; switching requires supplier validation (commonly 6–18 months) plus regulatory filings often taking 6–24 months. Concentration increases risk, but multi-sourcing across 2–3 qualified suppliers and long-term contracts reduce disruption; Servier's vertical integration in key steps further limits exposure.

GMP compliance and quality

Suppliers must meet stringent GMP and regulatory standards, narrowing the pool to certified manufacturers; audit-related compliance costs often exceed €100,000 annually per supplier, raising their bargaining leverage. Frequent regulatory audits and remediation increase supplier negotiating power, but the risk of suspension, recalls or multi-million euro fines for non-compliance constrains opportunistic pricing. Servier’s certified quality systems and supplier KPIs enable benchmarking and phased substitution, reducing long-term supplier dependence.

Equipment and CDMO capacity

Single-use systems, sterile fill-finish lines and high-potency suites remain key bottlenecks for Servier, with oncology CDMO utilization exceeding 90% in 2024 and industry lead times of 12–18 months. Tight global CDMO capacity in oncology elevates supplier influence and raises effective switching costs due to complex tech transfers. Strategic capacity reservations and dual-sourcing materially reduce supplier leverage.

Proprietary tech and reagents

Some manufacturing steps require proprietary enzymes, vectors or catalysts, creating high dependency on IP-protected vendors; licensing and supply agreements often include price-escalation clauses that favor suppliers, while co-development partnerships increasingly serve to share value and secure supply continuity, with 2024 industry reports noting growing supplier consolidation in key reagent categories.

- IP dependence

- Escalation clauses

- Supply concentration

- Co-development as mitigation

Logistics and cold chain

Temperature-controlled distribution and specialized packaging add critical vendor nodes, raising dependency on carriers and packaging firms. Disruptions pushed pharma cold-chain costs up about 12% in 2023–24, strengthening key providers' leverage. Competitive logistics markets and framework agreements limit pricing pressure, while redundant lanes and inventory buffers reduce vulnerability.

- Critical nodes: carriers, cold-pack suppliers

- Cost rise: ~12% (2023–24)

- Mitigants: framework agreements, competition

- Resilience: redundant lanes, inventory buffers

Biologics 30%, CDMO util. >90% heighten supplier leverage

Servier faces high supplier leverage from concentrated API/biologics supply (biologics ≈30% of global pharma sales in 2024), IP-protected reagents and oncology CDMO utilization >90% in 2024, elevating switching costs and lead times; mitigants include multi-sourcing, long-term contracts, co-development and vertical integration.

| Metric | 2024 | Implication |

|---|---|---|

| Biologics share | ≈30% | High supplier value |

| CDMO oncology util. | >90% | Capacity tightness |

| Audit cost/supplier | >€100k/yr | Raises supplier leverage |

| Cold-chain cost rise | ~12% (2023–24) | Higher logistics dependence |

What is included in the product

Tailored Porter's Five Forces analysis for Servier that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and intensity of rivalry, highlighting disruptive forces and strategic implications for pricing, market share, and defensive barriers.

A concise one-sheet summarizing Servier's Five Forces—relieves analysis bottlenecks so teams can make fast, confident strategic decisions and drop-ready slides for investors or board meetings.

Customers Bargaining Power

Payers and HTA bodies

National payers and HTA bodies negotiate aggressively on price and access as value frameworks tighten margins; NICE historically uses a £20,000–£30,000 per QALY threshold. With the global pharma market near $1.6 trillion in 2024, payers increasingly demand outcome-linked pricing that squeezes non-differentiated therapies. Demonstrable clinical and real-world outcomes are essential to defend price, and Servier’s R&D focus supports the evidence generation needed to counter buyer power.

Hospital and GPO consolidation

Hospital systems and GPO consolidation concentrates buying power—top GPOs control about 70% of acute-care purchasing—so bundled tenders drive deeper discounts and squeeze margins. Preferred formulary placement is now decisive to sustain volumes. Servier must compete on contracting value, patient-support services and rock-solid supply reliability to win commitments.

Physician and patient influence

Prescribers and patients prioritize efficacy, safety and convenience over price, tempering pure price-based bargaining; the global pharmaceutical market was estimated at about $1.4 trillion in 2024, so clinical value often trumps discounting. Strong clinical differentiation lowers price elasticity and strengthens supplier leverage, while patient support programs—rising across specialty products—improve adherence and brand perception. In crowded classes, brand loyalty erodes and buyer leverage increases.

International reference pricing

International reference pricing used by over 30 countries in 2024 lets payers anchor negotiations to lower-price markets, forcing downward pressure on list and net prices; launch sequencing and managed entry agreements are therefore deployed to protect price corridors and preserve revenue. Parallel trade in the EU intensifies spillover risk across member states, so Servier must tailor pricing by indication and market and use indication-based contracts to mitigate cross-border leakage.

- IRP reach: over 30 countries (2024)

- Mitigation: launch sequencing + managed entry agreements

- EU pressure: parallel trade increases spillover risk

- Strategy: indication- and market-specific pricing + contracts

Biosimilar and generic options

Availability of biosimilar and generic alternatives strengthens buyer bargaining: EU tender-driven markets saw biologic prices fall up to 60% post-LOE (infliximab/adalimumab), with typical post-LOE erosion of 30–70% within 12 months. Tender switches accelerate volume loss for originators. Differentiated formulations or combination regimens and lifecycle evidence updates can preserve a 10–30% premium.

- Buyer leverage: lower-cost alternatives increase negotiation power

- Tenders: drive faster switches and steep price erosion

- Differentiation: formulations/regimens slow substitution

- Lifecycle: evidence updates sustain value (≈10–30% premium)

Outcome pricing grows; $1.6T market tightens, GPOs ~70%

Payers and HTA bodies (NICE £20,000–30,000/QALY) enforce outcome-linked pricing as the $1.6T pharma market (2024) tightens margins; IRP in >30 countries and EU parallel trade depress prices. GPOs control ~70% acute purchasing, driving tender discounts; biosimilar LOE cuts reach up to 60%. Servier must deploy indication-based pricing, managed entry and strong real-world evidence to protect value.

| Metric | 2024 Value |

|---|---|

| Global pharma market | $1.6T |

| GPO acute purchasing | ~70% |

| IRP reach | >30 countries |

| Biosimilar LOE price fall | up to 60% |

What You See Is What You Get

Servier Porter's Five Forces Analysis

This preview shows the exact Servier Porter's Five Forces Analysis you'll receive—no placeholders or samples. The document displayed is the final, fully formatted file ready for download immediately after purchase. You're viewing the same comprehensive analysis that will be available to you upon payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Servier’s Porter's Five Forces analysis outlines supplier and buyer power, rivalry intensity, threat of substitutes and new entrants, highlighting the regulatory and innovation-driven pressures shaping its pharma position. This snapshot shows key dynamics and strategic implications. Unlock the full Porter's Five Forces Analysis to explore Servier’s competitive dynamics and market pressures in detail.

Suppliers Bargaining Power

Specialty APIs and biologics

Servier depends on complex APIs and biologics with few qualified sources, raising supplier leverage as biologics represented about 30% of global pharma sales in 2024; switching requires supplier validation (commonly 6–18 months) plus regulatory filings often taking 6–24 months. Concentration increases risk, but multi-sourcing across 2–3 qualified suppliers and long-term contracts reduce disruption; Servier's vertical integration in key steps further limits exposure.

GMP compliance and quality

Suppliers must meet stringent GMP and regulatory standards, narrowing the pool to certified manufacturers; audit-related compliance costs often exceed €100,000 annually per supplier, raising their bargaining leverage. Frequent regulatory audits and remediation increase supplier negotiating power, but the risk of suspension, recalls or multi-million euro fines for non-compliance constrains opportunistic pricing. Servier’s certified quality systems and supplier KPIs enable benchmarking and phased substitution, reducing long-term supplier dependence.

Equipment and CDMO capacity

Single-use systems, sterile fill-finish lines and high-potency suites remain key bottlenecks for Servier, with oncology CDMO utilization exceeding 90% in 2024 and industry lead times of 12–18 months. Tight global CDMO capacity in oncology elevates supplier influence and raises effective switching costs due to complex tech transfers. Strategic capacity reservations and dual-sourcing materially reduce supplier leverage.

Proprietary tech and reagents

Some manufacturing steps require proprietary enzymes, vectors or catalysts, creating high dependency on IP-protected vendors; licensing and supply agreements often include price-escalation clauses that favor suppliers, while co-development partnerships increasingly serve to share value and secure supply continuity, with 2024 industry reports noting growing supplier consolidation in key reagent categories.

- IP dependence

- Escalation clauses

- Supply concentration

- Co-development as mitigation

Logistics and cold chain

Temperature-controlled distribution and specialized packaging add critical vendor nodes, raising dependency on carriers and packaging firms. Disruptions pushed pharma cold-chain costs up about 12% in 2023–24, strengthening key providers' leverage. Competitive logistics markets and framework agreements limit pricing pressure, while redundant lanes and inventory buffers reduce vulnerability.

- Critical nodes: carriers, cold-pack suppliers

- Cost rise: ~12% (2023–24)

- Mitigants: framework agreements, competition

- Resilience: redundant lanes, inventory buffers

Biologics 30%, CDMO util. >90% heighten supplier leverage

Servier faces high supplier leverage from concentrated API/biologics supply (biologics ≈30% of global pharma sales in 2024), IP-protected reagents and oncology CDMO utilization >90% in 2024, elevating switching costs and lead times; mitigants include multi-sourcing, long-term contracts, co-development and vertical integration.

| Metric | 2024 | Implication |

|---|---|---|

| Biologics share | ≈30% | High supplier value |

| CDMO oncology util. | >90% | Capacity tightness |

| Audit cost/supplier | >€100k/yr | Raises supplier leverage |

| Cold-chain cost rise | ~12% (2023–24) | Higher logistics dependence |

What is included in the product

Tailored Porter's Five Forces analysis for Servier that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and intensity of rivalry, highlighting disruptive forces and strategic implications for pricing, market share, and defensive barriers.

A concise one-sheet summarizing Servier's Five Forces—relieves analysis bottlenecks so teams can make fast, confident strategic decisions and drop-ready slides for investors or board meetings.

Customers Bargaining Power

Payers and HTA bodies

National payers and HTA bodies negotiate aggressively on price and access as value frameworks tighten margins; NICE historically uses a £20,000–£30,000 per QALY threshold. With the global pharma market near $1.6 trillion in 2024, payers increasingly demand outcome-linked pricing that squeezes non-differentiated therapies. Demonstrable clinical and real-world outcomes are essential to defend price, and Servier’s R&D focus supports the evidence generation needed to counter buyer power.

Hospital and GPO consolidation

Hospital systems and GPO consolidation concentrates buying power—top GPOs control about 70% of acute-care purchasing—so bundled tenders drive deeper discounts and squeeze margins. Preferred formulary placement is now decisive to sustain volumes. Servier must compete on contracting value, patient-support services and rock-solid supply reliability to win commitments.

Physician and patient influence

Prescribers and patients prioritize efficacy, safety and convenience over price, tempering pure price-based bargaining; the global pharmaceutical market was estimated at about $1.4 trillion in 2024, so clinical value often trumps discounting. Strong clinical differentiation lowers price elasticity and strengthens supplier leverage, while patient support programs—rising across specialty products—improve adherence and brand perception. In crowded classes, brand loyalty erodes and buyer leverage increases.

International reference pricing

International reference pricing used by over 30 countries in 2024 lets payers anchor negotiations to lower-price markets, forcing downward pressure on list and net prices; launch sequencing and managed entry agreements are therefore deployed to protect price corridors and preserve revenue. Parallel trade in the EU intensifies spillover risk across member states, so Servier must tailor pricing by indication and market and use indication-based contracts to mitigate cross-border leakage.

- IRP reach: over 30 countries (2024)

- Mitigation: launch sequencing + managed entry agreements

- EU pressure: parallel trade increases spillover risk

- Strategy: indication- and market-specific pricing + contracts

Biosimilar and generic options

Availability of biosimilar and generic alternatives strengthens buyer bargaining: EU tender-driven markets saw biologic prices fall up to 60% post-LOE (infliximab/adalimumab), with typical post-LOE erosion of 30–70% within 12 months. Tender switches accelerate volume loss for originators. Differentiated formulations or combination regimens and lifecycle evidence updates can preserve a 10–30% premium.

- Buyer leverage: lower-cost alternatives increase negotiation power

- Tenders: drive faster switches and steep price erosion

- Differentiation: formulations/regimens slow substitution

- Lifecycle: evidence updates sustain value (≈10–30% premium)

Outcome pricing grows; $1.6T market tightens, GPOs ~70%

Payers and HTA bodies (NICE £20,000–30,000/QALY) enforce outcome-linked pricing as the $1.6T pharma market (2024) tightens margins; IRP in >30 countries and EU parallel trade depress prices. GPOs control ~70% acute purchasing, driving tender discounts; biosimilar LOE cuts reach up to 60%. Servier must deploy indication-based pricing, managed entry and strong real-world evidence to protect value.

| Metric | 2024 Value |

|---|---|

| Global pharma market | $1.6T |

| GPO acute purchasing | ~70% |

| IRP reach | >30 countries |

| Biosimilar LOE price fall | up to 60% |

What You See Is What You Get

Servier Porter's Five Forces Analysis

This preview shows the exact Servier Porter's Five Forces Analysis you'll receive—no placeholders or samples. The document displayed is the final, fully formatted file ready for download immediately after purchase. You're viewing the same comprehensive analysis that will be available to you upon payment.