Seven Bank Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

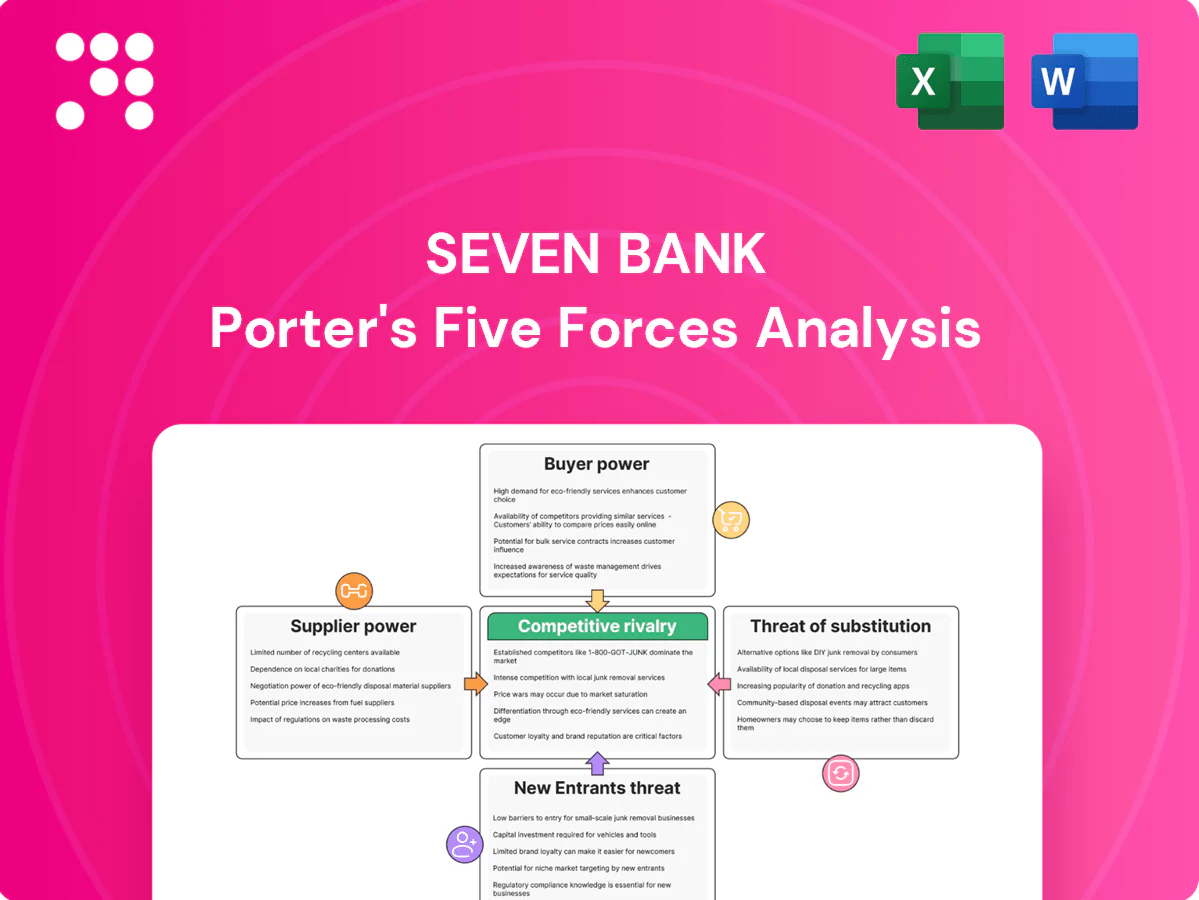

Seven Bank’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, and substitution risks shaping its margins and growth prospects. This concise view teases strategic pressures and key vulnerabilities. Ready for deeper, actionable intelligence? Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and tailored recommendations.

Suppliers Bargaining Power

Dependence on 7‑Eleven footprint

Seven Bank’s prime ATM network depends heavily on access to about 21,000 7‑Eleven stores in Japan (2024), giving Seven & i Holdings meaningful leverage in site renewals and fee negotiation; long‑term placement contracts mitigate short‑term risk but renegotiations—especially around fees split—can compress Seven Bank’s margins. Expanding ATMs beyond convenience stores would dilute this supplier power and reduce concentration risk.

ATM hardware and software vendors

Specialized ATM OEMs and software providers, led by NCR, Diebold Nixdorf and Hyosung, dominate the market and collectively account for the majority of global deployments as of 2024, creating concentrated supplier power. Switching vendors requires certification, integration and operational testing that raises migration risk and dependence. Multi-vendor strategies and adherence to EMV/ISO standards mitigate lock-in. Volume purchasing by large deployers improves negotiating leverage on price and support.

Cash logistics and network connectivity

Cash-in-transit providers, cash centers and telecoms underpin Seven Bank uptime; with ~22,000 ATMs in its network in 2024, regional provider concentration can nudge service pricing and SLAs. Dual-sourcing routes and carriers reduces single-vendor outage risk and supports continuity for high-volume ATM cash replenishment. Seven Bank’s scale and predictable cash flows strengthen its leverage in contract negotiations and volume discounts.

Card schemes and interbank networks

Visa and Mastercard together accounted for roughly 80% of global card purchase volume in 2024, while UnionPay, JCB and domestic networks retain strong regional footprints; all set interchange and compliance rules that directly affect acquirer and merchant economics. Scheme rule changes in 2024 (fee reassessments, security mandates) materially shifted fee mixes and processing costs. Wider scheme participation boosts authorization volume but increases assessed and network fees; negotiated incentives and intelligent routing reduced effective supplier leverage for large acquirers.

- Dominance: Visa+Mastercard ≈80% global volume (2024)

- Impact: 2024 rule changes shifted fee economics and compliance costs

- Mitigation: incentives, routing optimization and scale cut supplier power

Cloud and cybersecurity providers

Cloud and cybersecurity providers supply specialized secure hosting, fraud detection and continuous monitoring where AWS, Azure and GCP held roughly 32%, 23% and 11% global IaaS share in 2024, boosting vendor leverage; certification requirements (ISO 27001, PCI DSS) and high migration costs further raise switching barriers.

Seven Bank can retain architectural portability to curb dependency; regular audits and competitive RFPs (typical vendor cost reductions 10–15%) help contain pricing and mitigate supplier power.

- Specialization: secure hosting, fraud tools, monitoring

- 2024 market share: AWS 32%, Azure 23%, GCP 11%

- Certifications: ISO 27001, PCI DSS increase switching cost

- Mitigants: portability, audits, RFPs → ~10–15% cost pressure

Concentrated supplier leverage: 21,000 stores, 22,000 ATMs

Seven Bank’s supplier power is concentrated: ~21,000 7‑Eleven sites give Seven & i Holdings strong placement leverage but fee renegotiation risk; ~22,000 ATMs heighten regional provider influence. ATM vendors (NCR, Diebold, Hyosung) and schemes (Visa+Mastercard ≈80% global volume, 2024) raise switching costs. Cloud: AWS 32%, Azure 23%, GCP 11% (2024) — certifications and migration costs increase dependence; multi‑sourcing and RFPs mitigate.

| Supplier | 2024 metric | Concentration | Mitigation |

|---|---|---|---|

| Convenience sites | ≈21,000 stores | High | Expand channels |

| ATM OEMs | 3 major vendors | High | Multi‑vendor |

| Card schemes | Visa+MC ≈80% | High | Routing |

| Cloud | AWS32%/AZ23%/GCP11% | Moderate | Portability |

What is included in the product

Concise Porter's Five Forces assessment of Seven Bank highlighting competitive intensity, buyer and supplier bargaining power, threat of new entrants and substitutes, and emerging disruptive forces; includes industry-backed insights to inform pricing, profitability, and strategic barriers to entry.

A concise, one-sheet Porter's Five Forces for Seven Bank—visual radar for instant strategic insight, customizable pressure levels and labels, copy-ready for decks, no macros, easy data swaps, and seamless integration into Excel dashboards or reports to remove analysis friction.

Customers Bargaining Power

Price-sensitive retail users

Price-sensitive retail ATM users compare fees (typical ¥110–220 per withdrawal) and proximity across convenience chains, so small fee shifts can move marginal volumes; Seven Bank’s network in ~21,000 convenience locations (2024) and 24/7 access tempers switching. Multilingual UX and reliability drive repeat use, reducing buyer power despite fee sensitivity.

Partner banks and issuers

Partner banks route cardholders to Seven Bank under interchange agreements; Seven Bank’s network exceeds 20,000 ATMs in 2024, making uptime and reach critical value levers that sustain transaction volumes. Large issuers can extract double-digit concessions on interchange and routing economics. Tiered pricing and premium data services align incentives by rewarding high-volume partners and monetizing uptime and network analytics.

Foreign visitors and tourists

Inbound visitors prioritize international card acceptance and multilingual support; Seven Bank operates over 20,000 ATMs across convenience stores, meeting that need and reducing tourists' price bargaining power. Alternatives thin outside transport hubs, so convenience sustains usage. Clear FX disclosures and low-friction flows keep transaction volumes high amid Japan's post‑pandemic tourist rebound (around 32 million arrivals in 2023, strong 2024 recovery).

Merchants and billers using settlement

Corporate clients evaluate settlement fees, ease of integration, and uptime; global e-commerce reached an estimated 6.3 trillion USD in 2024, raising pressure on fee competitiveness. Large merchants leverage volume to demand discounts, while SLA-backed reliability and sticky API integrations reduce churn. Bundled services further increase switching costs for buyers.

- Fees sensitivity: high

- Integration stickiness: strong

- Volume leverage: significant for top merchants

- SLA impact: lowers churn

- Bundling: raises switching costs

Digital users of app-based services

- High competition — many app rivals, easy switching

- Multi-homing common — price/UX sensitive

- ATM integration — ~19,000 cash-in/out points (2024)

- Loyalty + seamless KYC reduce customer bargaining

Extensive ATM reach ~20,000 and 24/7 access reduce switching despite ¥110–220 fees

Seven Bank’s ~20,000 ATM network in 2024 and 24/7 access reduce switching despite fee sensitivity (¥110–220 per withdrawal). Large issuers and merchants hold volume leverage but face higher switching costs from SLAs, APIs and bundling. Digital users remain highly price/UX sensitive; loyalty and seamless KYC blunt churn.

| Metric | Value |

|---|---|

| ATMs (2024) | ~20,000 |

| Fee range | ¥110–220 |

| Tourist arrivals (2023) | ~32M |

Full Version Awaits

Seven Bank Porter's Five Forces Analysis

This preview displays the exact Seven Bank Porter’s Five Forces analysis you’ll receive upon purchase—no samples, no placeholders. The file shown is the final, professionally formatted document ready for immediate download and use. Purchase grants instant access to this identical deliverable.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Seven Bank’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, and substitution risks shaping its margins and growth prospects. This concise view teases strategic pressures and key vulnerabilities. Ready for deeper, actionable intelligence? Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and tailored recommendations.

Suppliers Bargaining Power

Dependence on 7‑Eleven footprint

Seven Bank’s prime ATM network depends heavily on access to about 21,000 7‑Eleven stores in Japan (2024), giving Seven & i Holdings meaningful leverage in site renewals and fee negotiation; long‑term placement contracts mitigate short‑term risk but renegotiations—especially around fees split—can compress Seven Bank’s margins. Expanding ATMs beyond convenience stores would dilute this supplier power and reduce concentration risk.

ATM hardware and software vendors

Specialized ATM OEMs and software providers, led by NCR, Diebold Nixdorf and Hyosung, dominate the market and collectively account for the majority of global deployments as of 2024, creating concentrated supplier power. Switching vendors requires certification, integration and operational testing that raises migration risk and dependence. Multi-vendor strategies and adherence to EMV/ISO standards mitigate lock-in. Volume purchasing by large deployers improves negotiating leverage on price and support.

Cash logistics and network connectivity

Cash-in-transit providers, cash centers and telecoms underpin Seven Bank uptime; with ~22,000 ATMs in its network in 2024, regional provider concentration can nudge service pricing and SLAs. Dual-sourcing routes and carriers reduces single-vendor outage risk and supports continuity for high-volume ATM cash replenishment. Seven Bank’s scale and predictable cash flows strengthen its leverage in contract negotiations and volume discounts.

Card schemes and interbank networks

Visa and Mastercard together accounted for roughly 80% of global card purchase volume in 2024, while UnionPay, JCB and domestic networks retain strong regional footprints; all set interchange and compliance rules that directly affect acquirer and merchant economics. Scheme rule changes in 2024 (fee reassessments, security mandates) materially shifted fee mixes and processing costs. Wider scheme participation boosts authorization volume but increases assessed and network fees; negotiated incentives and intelligent routing reduced effective supplier leverage for large acquirers.

- Dominance: Visa+Mastercard ≈80% global volume (2024)

- Impact: 2024 rule changes shifted fee economics and compliance costs

- Mitigation: incentives, routing optimization and scale cut supplier power

Cloud and cybersecurity providers

Cloud and cybersecurity providers supply specialized secure hosting, fraud detection and continuous monitoring where AWS, Azure and GCP held roughly 32%, 23% and 11% global IaaS share in 2024, boosting vendor leverage; certification requirements (ISO 27001, PCI DSS) and high migration costs further raise switching barriers.

Seven Bank can retain architectural portability to curb dependency; regular audits and competitive RFPs (typical vendor cost reductions 10–15%) help contain pricing and mitigate supplier power.

- Specialization: secure hosting, fraud tools, monitoring

- 2024 market share: AWS 32%, Azure 23%, GCP 11%

- Certifications: ISO 27001, PCI DSS increase switching cost

- Mitigants: portability, audits, RFPs → ~10–15% cost pressure

Concentrated supplier leverage: 21,000 stores, 22,000 ATMs

Seven Bank’s supplier power is concentrated: ~21,000 7‑Eleven sites give Seven & i Holdings strong placement leverage but fee renegotiation risk; ~22,000 ATMs heighten regional provider influence. ATM vendors (NCR, Diebold, Hyosung) and schemes (Visa+Mastercard ≈80% global volume, 2024) raise switching costs. Cloud: AWS 32%, Azure 23%, GCP 11% (2024) — certifications and migration costs increase dependence; multi‑sourcing and RFPs mitigate.

| Supplier | 2024 metric | Concentration | Mitigation |

|---|---|---|---|

| Convenience sites | ≈21,000 stores | High | Expand channels |

| ATM OEMs | 3 major vendors | High | Multi‑vendor |

| Card schemes | Visa+MC ≈80% | High | Routing |

| Cloud | AWS32%/AZ23%/GCP11% | Moderate | Portability |

What is included in the product

Concise Porter's Five Forces assessment of Seven Bank highlighting competitive intensity, buyer and supplier bargaining power, threat of new entrants and substitutes, and emerging disruptive forces; includes industry-backed insights to inform pricing, profitability, and strategic barriers to entry.

A concise, one-sheet Porter's Five Forces for Seven Bank—visual radar for instant strategic insight, customizable pressure levels and labels, copy-ready for decks, no macros, easy data swaps, and seamless integration into Excel dashboards or reports to remove analysis friction.

Customers Bargaining Power

Price-sensitive retail users

Price-sensitive retail ATM users compare fees (typical ¥110–220 per withdrawal) and proximity across convenience chains, so small fee shifts can move marginal volumes; Seven Bank’s network in ~21,000 convenience locations (2024) and 24/7 access tempers switching. Multilingual UX and reliability drive repeat use, reducing buyer power despite fee sensitivity.

Partner banks and issuers

Partner banks route cardholders to Seven Bank under interchange agreements; Seven Bank’s network exceeds 20,000 ATMs in 2024, making uptime and reach critical value levers that sustain transaction volumes. Large issuers can extract double-digit concessions on interchange and routing economics. Tiered pricing and premium data services align incentives by rewarding high-volume partners and monetizing uptime and network analytics.

Foreign visitors and tourists

Inbound visitors prioritize international card acceptance and multilingual support; Seven Bank operates over 20,000 ATMs across convenience stores, meeting that need and reducing tourists' price bargaining power. Alternatives thin outside transport hubs, so convenience sustains usage. Clear FX disclosures and low-friction flows keep transaction volumes high amid Japan's post‑pandemic tourist rebound (around 32 million arrivals in 2023, strong 2024 recovery).

Merchants and billers using settlement

Corporate clients evaluate settlement fees, ease of integration, and uptime; global e-commerce reached an estimated 6.3 trillion USD in 2024, raising pressure on fee competitiveness. Large merchants leverage volume to demand discounts, while SLA-backed reliability and sticky API integrations reduce churn. Bundled services further increase switching costs for buyers.

- Fees sensitivity: high

- Integration stickiness: strong

- Volume leverage: significant for top merchants

- SLA impact: lowers churn

- Bundling: raises switching costs

Digital users of app-based services

- High competition — many app rivals, easy switching

- Multi-homing common — price/UX sensitive

- ATM integration — ~19,000 cash-in/out points (2024)

- Loyalty + seamless KYC reduce customer bargaining

Extensive ATM reach ~20,000 and 24/7 access reduce switching despite ¥110–220 fees

Seven Bank’s ~20,000 ATM network in 2024 and 24/7 access reduce switching despite fee sensitivity (¥110–220 per withdrawal). Large issuers and merchants hold volume leverage but face higher switching costs from SLAs, APIs and bundling. Digital users remain highly price/UX sensitive; loyalty and seamless KYC blunt churn.

| Metric | Value |

|---|---|

| ATMs (2024) | ~20,000 |

| Fee range | ¥110–220 |

| Tourist arrivals (2023) | ~32M |

Full Version Awaits

Seven Bank Porter's Five Forces Analysis

This preview displays the exact Seven Bank Porter’s Five Forces analysis you’ll receive upon purchase—no samples, no placeholders. The file shown is the final, professionally formatted document ready for immediate download and use. Purchase grants instant access to this identical deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Seven Bank’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, and substitution risks shaping its margins and growth prospects. This concise view teases strategic pressures and key vulnerabilities. Ready for deeper, actionable intelligence? Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and tailored recommendations.

Suppliers Bargaining Power

Dependence on 7‑Eleven footprint

Seven Bank’s prime ATM network depends heavily on access to about 21,000 7‑Eleven stores in Japan (2024), giving Seven & i Holdings meaningful leverage in site renewals and fee negotiation; long‑term placement contracts mitigate short‑term risk but renegotiations—especially around fees split—can compress Seven Bank’s margins. Expanding ATMs beyond convenience stores would dilute this supplier power and reduce concentration risk.

ATM hardware and software vendors

Specialized ATM OEMs and software providers, led by NCR, Diebold Nixdorf and Hyosung, dominate the market and collectively account for the majority of global deployments as of 2024, creating concentrated supplier power. Switching vendors requires certification, integration and operational testing that raises migration risk and dependence. Multi-vendor strategies and adherence to EMV/ISO standards mitigate lock-in. Volume purchasing by large deployers improves negotiating leverage on price and support.

Cash logistics and network connectivity

Cash-in-transit providers, cash centers and telecoms underpin Seven Bank uptime; with ~22,000 ATMs in its network in 2024, regional provider concentration can nudge service pricing and SLAs. Dual-sourcing routes and carriers reduces single-vendor outage risk and supports continuity for high-volume ATM cash replenishment. Seven Bank’s scale and predictable cash flows strengthen its leverage in contract negotiations and volume discounts.

Card schemes and interbank networks

Visa and Mastercard together accounted for roughly 80% of global card purchase volume in 2024, while UnionPay, JCB and domestic networks retain strong regional footprints; all set interchange and compliance rules that directly affect acquirer and merchant economics. Scheme rule changes in 2024 (fee reassessments, security mandates) materially shifted fee mixes and processing costs. Wider scheme participation boosts authorization volume but increases assessed and network fees; negotiated incentives and intelligent routing reduced effective supplier leverage for large acquirers.

- Dominance: Visa+Mastercard ≈80% global volume (2024)

- Impact: 2024 rule changes shifted fee economics and compliance costs

- Mitigation: incentives, routing optimization and scale cut supplier power

Cloud and cybersecurity providers

Cloud and cybersecurity providers supply specialized secure hosting, fraud detection and continuous monitoring where AWS, Azure and GCP held roughly 32%, 23% and 11% global IaaS share in 2024, boosting vendor leverage; certification requirements (ISO 27001, PCI DSS) and high migration costs further raise switching barriers.

Seven Bank can retain architectural portability to curb dependency; regular audits and competitive RFPs (typical vendor cost reductions 10–15%) help contain pricing and mitigate supplier power.

- Specialization: secure hosting, fraud tools, monitoring

- 2024 market share: AWS 32%, Azure 23%, GCP 11%

- Certifications: ISO 27001, PCI DSS increase switching cost

- Mitigants: portability, audits, RFPs → ~10–15% cost pressure

Concentrated supplier leverage: 21,000 stores, 22,000 ATMs

Seven Bank’s supplier power is concentrated: ~21,000 7‑Eleven sites give Seven & i Holdings strong placement leverage but fee renegotiation risk; ~22,000 ATMs heighten regional provider influence. ATM vendors (NCR, Diebold, Hyosung) and schemes (Visa+Mastercard ≈80% global volume, 2024) raise switching costs. Cloud: AWS 32%, Azure 23%, GCP 11% (2024) — certifications and migration costs increase dependence; multi‑sourcing and RFPs mitigate.

| Supplier | 2024 metric | Concentration | Mitigation |

|---|---|---|---|

| Convenience sites | ≈21,000 stores | High | Expand channels |

| ATM OEMs | 3 major vendors | High | Multi‑vendor |

| Card schemes | Visa+MC ≈80% | High | Routing |

| Cloud | AWS32%/AZ23%/GCP11% | Moderate | Portability |

What is included in the product

Concise Porter's Five Forces assessment of Seven Bank highlighting competitive intensity, buyer and supplier bargaining power, threat of new entrants and substitutes, and emerging disruptive forces; includes industry-backed insights to inform pricing, profitability, and strategic barriers to entry.

A concise, one-sheet Porter's Five Forces for Seven Bank—visual radar for instant strategic insight, customizable pressure levels and labels, copy-ready for decks, no macros, easy data swaps, and seamless integration into Excel dashboards or reports to remove analysis friction.

Customers Bargaining Power

Price-sensitive retail users

Price-sensitive retail ATM users compare fees (typical ¥110–220 per withdrawal) and proximity across convenience chains, so small fee shifts can move marginal volumes; Seven Bank’s network in ~21,000 convenience locations (2024) and 24/7 access tempers switching. Multilingual UX and reliability drive repeat use, reducing buyer power despite fee sensitivity.

Partner banks and issuers

Partner banks route cardholders to Seven Bank under interchange agreements; Seven Bank’s network exceeds 20,000 ATMs in 2024, making uptime and reach critical value levers that sustain transaction volumes. Large issuers can extract double-digit concessions on interchange and routing economics. Tiered pricing and premium data services align incentives by rewarding high-volume partners and monetizing uptime and network analytics.

Foreign visitors and tourists

Inbound visitors prioritize international card acceptance and multilingual support; Seven Bank operates over 20,000 ATMs across convenience stores, meeting that need and reducing tourists' price bargaining power. Alternatives thin outside transport hubs, so convenience sustains usage. Clear FX disclosures and low-friction flows keep transaction volumes high amid Japan's post‑pandemic tourist rebound (around 32 million arrivals in 2023, strong 2024 recovery).

Merchants and billers using settlement

Corporate clients evaluate settlement fees, ease of integration, and uptime; global e-commerce reached an estimated 6.3 trillion USD in 2024, raising pressure on fee competitiveness. Large merchants leverage volume to demand discounts, while SLA-backed reliability and sticky API integrations reduce churn. Bundled services further increase switching costs for buyers.

- Fees sensitivity: high

- Integration stickiness: strong

- Volume leverage: significant for top merchants

- SLA impact: lowers churn

- Bundling: raises switching costs

Digital users of app-based services

- High competition — many app rivals, easy switching

- Multi-homing common — price/UX sensitive

- ATM integration — ~19,000 cash-in/out points (2024)

- Loyalty + seamless KYC reduce customer bargaining

Extensive ATM reach ~20,000 and 24/7 access reduce switching despite ¥110–220 fees

Seven Bank’s ~20,000 ATM network in 2024 and 24/7 access reduce switching despite fee sensitivity (¥110–220 per withdrawal). Large issuers and merchants hold volume leverage but face higher switching costs from SLAs, APIs and bundling. Digital users remain highly price/UX sensitive; loyalty and seamless KYC blunt churn.

| Metric | Value |

|---|---|

| ATMs (2024) | ~20,000 |

| Fee range | ¥110–220 |

| Tourist arrivals (2023) | ~32M |

Full Version Awaits

Seven Bank Porter's Five Forces Analysis

This preview displays the exact Seven Bank Porter’s Five Forces analysis you’ll receive upon purchase—no samples, no placeholders. The file shown is the final, professionally formatted document ready for immediate download and use. Purchase grants instant access to this identical deliverable.