Seven Bank SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

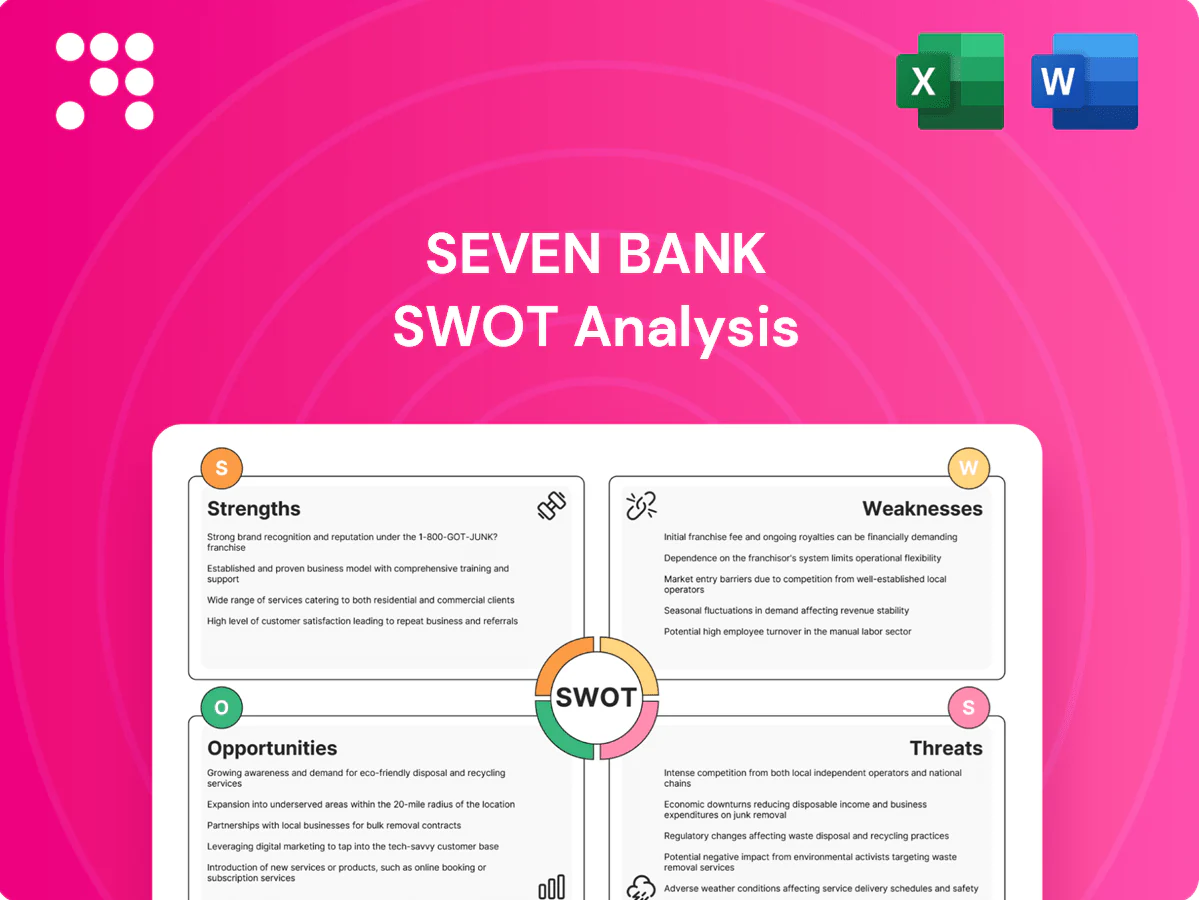

Explore Seven Bank's strategic strengths, risks, and market opportunities in this concise SWOT preview. Purchase the full SWOT analysis to access a research-backed, editable Word report and Excel matrix with actionable insights and financial context. Ideal for investors, analysts, and strategists who need ready-to-use, investor-quality deliverables.

Strengths

Dominant ATM footprint

Seven Bank’s dominant ATM footprint places about 20,000 ATMs inside roughly 21,000 7-Eleven stores across Japan (2024), delivering unmatched convenience and nationwide coverage. High foot traffic at these locations drives frequent transactions and steady fee income, supporting predictable cash flows. The ubiquitous presence boosts brand visibility and trust while cutting customer acquisition costs by leveraging natural store traffic.

24/7 availability uptime

Seven Bank’s network of about 20,000 ATMs and always-on digital channels deliver true 24/7 access, meeting consumer demand for instant banking and supporting millions of monthly transactions. Rigorous operational processes target industry-leading availability (near 99.99% uptime), ensuring high reliability. Consistent round-the-clock service boosts loyalty among retail and foreign card users and differentiates Seven Bank from banks limited by branch hours.

Partnership-driven model

Partnerships with retailers such as 7-Eleven and global card networks (Visa, Mastercard, UnionPay) broaden Seven Bank’s service reach, linking banks and payment networks into one platform. The partnership-driven model monetizes interoperability via interchange and settlement services, generating steady fee income. Partners gain distribution while Seven Bank scales with over 20,000 ATMs in Japan without heavy branch investment, building a defensible convenience-payments ecosystem.

Efficient cost structure

Seven Bank’s ATM-centric model avoids branch and staffing costs of traditional banks, enabling lean operations. As of March 2024 Seven Bank operated about 21,000 ATMs, driving scale effects that lower per-transaction costs and boost operating leverage. Standardized hardware and centralized processing further reduce unit costs, supporting competitive pricing while preserving margins.

- ~21,000 ATMs (Mar 2024)

- High operating leverage → lower per-transaction cost

- Standardized hardware + centralized ops

- Competitive pricing with preserved margins

Foreign user friendliness

Multilingual interfaces and wide international card acceptance make Seven Bank ATMs a top choice for tourists and expatriates; Japan welcomed over 30 million inbound visitors in 2023, supporting higher non-domestic cash usage. Cross-border access has boosted foreign transaction volume, diversifying revenue beyond domestic customers and reinforcing Seven Bank as Japan’s visitor-friendly cash access point.

- Multilingual ATMs

- Global card acceptance

- Over 30M inbound visitors (2023)

- Diversified non-domestic revenue

21,000 ATMs: 24/7 access, 99.99% uptime

Seven Bank’s ~21,000 ATMs in 7-Eleven stores (Mar 2024) deliver nationwide 24/7 access and high visibility. High foot traffic plus multilingual/global card acceptance (over 30M inbound visitors in 2023) generate steady fee income and diversify revenue. Lean ATM-centric model, standardized hardware and centralized ops lower per-transaction costs and achieve near-99.99% uptime.

| Metric | Value |

|---|---|

| ATMs (Mar 2024) | ~21,000 |

| Inbound visitors (2023) | >30M |

| Uptime | ~99.99% |

What is included in the product

Provides a concise strategic overview of Seven Bank’s internal strengths and weaknesses and its external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decision-making.

Provides a concise, high-level SWOT matrix for Seven Bank to streamline stakeholder alignment and rapid decision-making, while enabling quick edits to reflect shifting market priorities.

Weaknesses

Reliance on cash usage

Core revenues at Seven Bank still rely heavily on ATM withdrawals and deposits from its network of about 20,000 ATMs, but rising cashless adoption—Japan set a governmental cashless target of 40% by 2025—threatens transaction volumes. Falling cash frequency creates structural headwinds for ATM-centric fee income, so diversification into digital payments and partnerships is required to offset declining cash transactions.

Concentration in 7-Eleven

Seven Bank is heavily tied to the 7-Eleven network, which comprises roughly 21,000 stores in Japan, making the retailer the primary distribution channel for the bank’s ATMs. Any reduction or strategic shift in that footprint would directly affect ATM placement and customer traffic. This dependence concentrates counterparty and concentration risk with a single retail partner. Negotiating leverage likely favors the anchor partner, limiting Seven Bank’s pricing and placement flexibility.

Narrow product breadth

Compared with megabanks, Seven Bank offers limited wealth, lending and corporate services, which caps wallet share per customer and constrains revenue mix. This narrow product breadth increases vulnerability to fee-pressure in core deposit and ATM services. Cross-sell potential remains underexploited despite Seven Bank’s roughly 20,000 ATMs nationwide.

Fee sensitivity and low margins

Seven Bank faces intense fee sensitivity as ATM and settlement fees in Japan came under public and regulatory scrutiny in 2024, pressuring rates and risking caps that would thin margins.

Price competition from convenience-store ATMs compresses spreads while high fixed costs per machine amplify volume risk; profitability depends on sustaining high utilization and transaction density.

- Fee caps/pressure — 2024 regulatory scrutiny

- Compressed spreads vs convenience ATMs

- High fixed cost per ATM magnifies volume risk

- Profitability tied to sustained high utilization

Cyber and fraud exposure

ATMs and digital rails face persistent threats from skimming, malware, and social engineering, increasing operational loss and customer trust erosion for Seven Bank. Security incidents can trigger direct financial losses and long-lasting reputational damage that depress transaction volumes. Continuous investment in cybersecurity and tight compliance requirements strain Seven Bank’s lean cost structure and margins.

- ATMs vulnerable to skimming/malware

- Social engineering targets retail customers

- High defensive and compliance costs

- Reputational risk reduces transaction revenue

Retail ATM concentration, cashless push and fee scrutiny threaten ATM revenue and margins

Seven Bank depends on ~20,000 ATMs and the 7‑Eleven channel (~21,000 stores), exposing it to retail partner concentration and placement risk. Japan’s 40% cashless target by 2025 and 2024 regulatory fee scrutiny threaten ATM volumes and fee revenue. High fixed ATM costs, compressed spreads vs convenience ATMs, and rising cyberfraud raise margin and reputational risks.

| Metric | Value |

|---|---|

| ATMs | ~20,000 |

| 7‑Eleven stores | ~21,000 |

| Cashless target | 40% by 2025 |

| Regulatory pressure | Fee scrutiny in 2024 |

Same Document Delivered

Seven Bank SWOT Analysis

This is the actual Seven Bank SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, covering strengths, weaknesses, opportunities, and threats. Buy now to unlock the complete, editable version.

Elevate Your Analysis with the Complete SWOT Report

Explore Seven Bank's strategic strengths, risks, and market opportunities in this concise SWOT preview. Purchase the full SWOT analysis to access a research-backed, editable Word report and Excel matrix with actionable insights and financial context. Ideal for investors, analysts, and strategists who need ready-to-use, investor-quality deliverables.

Strengths

Dominant ATM footprint

Seven Bank’s dominant ATM footprint places about 20,000 ATMs inside roughly 21,000 7-Eleven stores across Japan (2024), delivering unmatched convenience and nationwide coverage. High foot traffic at these locations drives frequent transactions and steady fee income, supporting predictable cash flows. The ubiquitous presence boosts brand visibility and trust while cutting customer acquisition costs by leveraging natural store traffic.

24/7 availability uptime

Seven Bank’s network of about 20,000 ATMs and always-on digital channels deliver true 24/7 access, meeting consumer demand for instant banking and supporting millions of monthly transactions. Rigorous operational processes target industry-leading availability (near 99.99% uptime), ensuring high reliability. Consistent round-the-clock service boosts loyalty among retail and foreign card users and differentiates Seven Bank from banks limited by branch hours.

Partnership-driven model

Partnerships with retailers such as 7-Eleven and global card networks (Visa, Mastercard, UnionPay) broaden Seven Bank’s service reach, linking banks and payment networks into one platform. The partnership-driven model monetizes interoperability via interchange and settlement services, generating steady fee income. Partners gain distribution while Seven Bank scales with over 20,000 ATMs in Japan without heavy branch investment, building a defensible convenience-payments ecosystem.

Efficient cost structure

Seven Bank’s ATM-centric model avoids branch and staffing costs of traditional banks, enabling lean operations. As of March 2024 Seven Bank operated about 21,000 ATMs, driving scale effects that lower per-transaction costs and boost operating leverage. Standardized hardware and centralized processing further reduce unit costs, supporting competitive pricing while preserving margins.

- ~21,000 ATMs (Mar 2024)

- High operating leverage → lower per-transaction cost

- Standardized hardware + centralized ops

- Competitive pricing with preserved margins

Foreign user friendliness

Multilingual interfaces and wide international card acceptance make Seven Bank ATMs a top choice for tourists and expatriates; Japan welcomed over 30 million inbound visitors in 2023, supporting higher non-domestic cash usage. Cross-border access has boosted foreign transaction volume, diversifying revenue beyond domestic customers and reinforcing Seven Bank as Japan’s visitor-friendly cash access point.

- Multilingual ATMs

- Global card acceptance

- Over 30M inbound visitors (2023)

- Diversified non-domestic revenue

21,000 ATMs: 24/7 access, 99.99% uptime

Seven Bank’s ~21,000 ATMs in 7-Eleven stores (Mar 2024) deliver nationwide 24/7 access and high visibility. High foot traffic plus multilingual/global card acceptance (over 30M inbound visitors in 2023) generate steady fee income and diversify revenue. Lean ATM-centric model, standardized hardware and centralized ops lower per-transaction costs and achieve near-99.99% uptime.

| Metric | Value |

|---|---|

| ATMs (Mar 2024) | ~21,000 |

| Inbound visitors (2023) | >30M |

| Uptime | ~99.99% |

What is included in the product

Provides a concise strategic overview of Seven Bank’s internal strengths and weaknesses and its external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decision-making.

Provides a concise, high-level SWOT matrix for Seven Bank to streamline stakeholder alignment and rapid decision-making, while enabling quick edits to reflect shifting market priorities.

Weaknesses

Reliance on cash usage

Core revenues at Seven Bank still rely heavily on ATM withdrawals and deposits from its network of about 20,000 ATMs, but rising cashless adoption—Japan set a governmental cashless target of 40% by 2025—threatens transaction volumes. Falling cash frequency creates structural headwinds for ATM-centric fee income, so diversification into digital payments and partnerships is required to offset declining cash transactions.

Concentration in 7-Eleven

Seven Bank is heavily tied to the 7-Eleven network, which comprises roughly 21,000 stores in Japan, making the retailer the primary distribution channel for the bank’s ATMs. Any reduction or strategic shift in that footprint would directly affect ATM placement and customer traffic. This dependence concentrates counterparty and concentration risk with a single retail partner. Negotiating leverage likely favors the anchor partner, limiting Seven Bank’s pricing and placement flexibility.

Narrow product breadth

Compared with megabanks, Seven Bank offers limited wealth, lending and corporate services, which caps wallet share per customer and constrains revenue mix. This narrow product breadth increases vulnerability to fee-pressure in core deposit and ATM services. Cross-sell potential remains underexploited despite Seven Bank’s roughly 20,000 ATMs nationwide.

Fee sensitivity and low margins

Seven Bank faces intense fee sensitivity as ATM and settlement fees in Japan came under public and regulatory scrutiny in 2024, pressuring rates and risking caps that would thin margins.

Price competition from convenience-store ATMs compresses spreads while high fixed costs per machine amplify volume risk; profitability depends on sustaining high utilization and transaction density.

- Fee caps/pressure — 2024 regulatory scrutiny

- Compressed spreads vs convenience ATMs

- High fixed cost per ATM magnifies volume risk

- Profitability tied to sustained high utilization

Cyber and fraud exposure

ATMs and digital rails face persistent threats from skimming, malware, and social engineering, increasing operational loss and customer trust erosion for Seven Bank. Security incidents can trigger direct financial losses and long-lasting reputational damage that depress transaction volumes. Continuous investment in cybersecurity and tight compliance requirements strain Seven Bank’s lean cost structure and margins.

- ATMs vulnerable to skimming/malware

- Social engineering targets retail customers

- High defensive and compliance costs

- Reputational risk reduces transaction revenue

Retail ATM concentration, cashless push and fee scrutiny threaten ATM revenue and margins

Seven Bank depends on ~20,000 ATMs and the 7‑Eleven channel (~21,000 stores), exposing it to retail partner concentration and placement risk. Japan’s 40% cashless target by 2025 and 2024 regulatory fee scrutiny threaten ATM volumes and fee revenue. High fixed ATM costs, compressed spreads vs convenience ATMs, and rising cyberfraud raise margin and reputational risks.

| Metric | Value |

|---|---|

| ATMs | ~20,000 |

| 7‑Eleven stores | ~21,000 |

| Cashless target | 40% by 2025 |

| Regulatory pressure | Fee scrutiny in 2024 |

Same Document Delivered

Seven Bank SWOT Analysis

This is the actual Seven Bank SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, covering strengths, weaknesses, opportunities, and threats. Buy now to unlock the complete, editable version.

Description

Elevate Your Analysis with the Complete SWOT Report

Explore Seven Bank's strategic strengths, risks, and market opportunities in this concise SWOT preview. Purchase the full SWOT analysis to access a research-backed, editable Word report and Excel matrix with actionable insights and financial context. Ideal for investors, analysts, and strategists who need ready-to-use, investor-quality deliverables.

Strengths

Dominant ATM footprint

Seven Bank’s dominant ATM footprint places about 20,000 ATMs inside roughly 21,000 7-Eleven stores across Japan (2024), delivering unmatched convenience and nationwide coverage. High foot traffic at these locations drives frequent transactions and steady fee income, supporting predictable cash flows. The ubiquitous presence boosts brand visibility and trust while cutting customer acquisition costs by leveraging natural store traffic.

24/7 availability uptime

Seven Bank’s network of about 20,000 ATMs and always-on digital channels deliver true 24/7 access, meeting consumer demand for instant banking and supporting millions of monthly transactions. Rigorous operational processes target industry-leading availability (near 99.99% uptime), ensuring high reliability. Consistent round-the-clock service boosts loyalty among retail and foreign card users and differentiates Seven Bank from banks limited by branch hours.

Partnership-driven model

Partnerships with retailers such as 7-Eleven and global card networks (Visa, Mastercard, UnionPay) broaden Seven Bank’s service reach, linking banks and payment networks into one platform. The partnership-driven model monetizes interoperability via interchange and settlement services, generating steady fee income. Partners gain distribution while Seven Bank scales with over 20,000 ATMs in Japan without heavy branch investment, building a defensible convenience-payments ecosystem.

Efficient cost structure

Seven Bank’s ATM-centric model avoids branch and staffing costs of traditional banks, enabling lean operations. As of March 2024 Seven Bank operated about 21,000 ATMs, driving scale effects that lower per-transaction costs and boost operating leverage. Standardized hardware and centralized processing further reduce unit costs, supporting competitive pricing while preserving margins.

- ~21,000 ATMs (Mar 2024)

- High operating leverage → lower per-transaction cost

- Standardized hardware + centralized ops

- Competitive pricing with preserved margins

Foreign user friendliness

Multilingual interfaces and wide international card acceptance make Seven Bank ATMs a top choice for tourists and expatriates; Japan welcomed over 30 million inbound visitors in 2023, supporting higher non-domestic cash usage. Cross-border access has boosted foreign transaction volume, diversifying revenue beyond domestic customers and reinforcing Seven Bank as Japan’s visitor-friendly cash access point.

- Multilingual ATMs

- Global card acceptance

- Over 30M inbound visitors (2023)

- Diversified non-domestic revenue

21,000 ATMs: 24/7 access, 99.99% uptime

Seven Bank’s ~21,000 ATMs in 7-Eleven stores (Mar 2024) deliver nationwide 24/7 access and high visibility. High foot traffic plus multilingual/global card acceptance (over 30M inbound visitors in 2023) generate steady fee income and diversify revenue. Lean ATM-centric model, standardized hardware and centralized ops lower per-transaction costs and achieve near-99.99% uptime.

| Metric | Value |

|---|---|

| ATMs (Mar 2024) | ~21,000 |

| Inbound visitors (2023) | >30M |

| Uptime | ~99.99% |

What is included in the product

Provides a concise strategic overview of Seven Bank’s internal strengths and weaknesses and its external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decision-making.

Provides a concise, high-level SWOT matrix for Seven Bank to streamline stakeholder alignment and rapid decision-making, while enabling quick edits to reflect shifting market priorities.

Weaknesses

Reliance on cash usage

Core revenues at Seven Bank still rely heavily on ATM withdrawals and deposits from its network of about 20,000 ATMs, but rising cashless adoption—Japan set a governmental cashless target of 40% by 2025—threatens transaction volumes. Falling cash frequency creates structural headwinds for ATM-centric fee income, so diversification into digital payments and partnerships is required to offset declining cash transactions.

Concentration in 7-Eleven

Seven Bank is heavily tied to the 7-Eleven network, which comprises roughly 21,000 stores in Japan, making the retailer the primary distribution channel for the bank’s ATMs. Any reduction or strategic shift in that footprint would directly affect ATM placement and customer traffic. This dependence concentrates counterparty and concentration risk with a single retail partner. Negotiating leverage likely favors the anchor partner, limiting Seven Bank’s pricing and placement flexibility.

Narrow product breadth

Compared with megabanks, Seven Bank offers limited wealth, lending and corporate services, which caps wallet share per customer and constrains revenue mix. This narrow product breadth increases vulnerability to fee-pressure in core deposit and ATM services. Cross-sell potential remains underexploited despite Seven Bank’s roughly 20,000 ATMs nationwide.

Fee sensitivity and low margins

Seven Bank faces intense fee sensitivity as ATM and settlement fees in Japan came under public and regulatory scrutiny in 2024, pressuring rates and risking caps that would thin margins.

Price competition from convenience-store ATMs compresses spreads while high fixed costs per machine amplify volume risk; profitability depends on sustaining high utilization and transaction density.

- Fee caps/pressure — 2024 regulatory scrutiny

- Compressed spreads vs convenience ATMs

- High fixed cost per ATM magnifies volume risk

- Profitability tied to sustained high utilization

Cyber and fraud exposure

ATMs and digital rails face persistent threats from skimming, malware, and social engineering, increasing operational loss and customer trust erosion for Seven Bank. Security incidents can trigger direct financial losses and long-lasting reputational damage that depress transaction volumes. Continuous investment in cybersecurity and tight compliance requirements strain Seven Bank’s lean cost structure and margins.

- ATMs vulnerable to skimming/malware

- Social engineering targets retail customers

- High defensive and compliance costs

- Reputational risk reduces transaction revenue

Retail ATM concentration, cashless push and fee scrutiny threaten ATM revenue and margins

Seven Bank depends on ~20,000 ATMs and the 7‑Eleven channel (~21,000 stores), exposing it to retail partner concentration and placement risk. Japan’s 40% cashless target by 2025 and 2024 regulatory fee scrutiny threaten ATM volumes and fee revenue. High fixed ATM costs, compressed spreads vs convenience ATMs, and rising cyberfraud raise margin and reputational risks.

| Metric | Value |

|---|---|

| ATMs | ~20,000 |

| 7‑Eleven stores | ~21,000 |

| Cashless target | 40% by 2025 |

| Regulatory pressure | Fee scrutiny in 2024 |

Same Document Delivered

Seven Bank SWOT Analysis

This is the actual Seven Bank SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, covering strengths, weaknesses, opportunities, and threats. Buy now to unlock the complete, editable version.