SGH Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

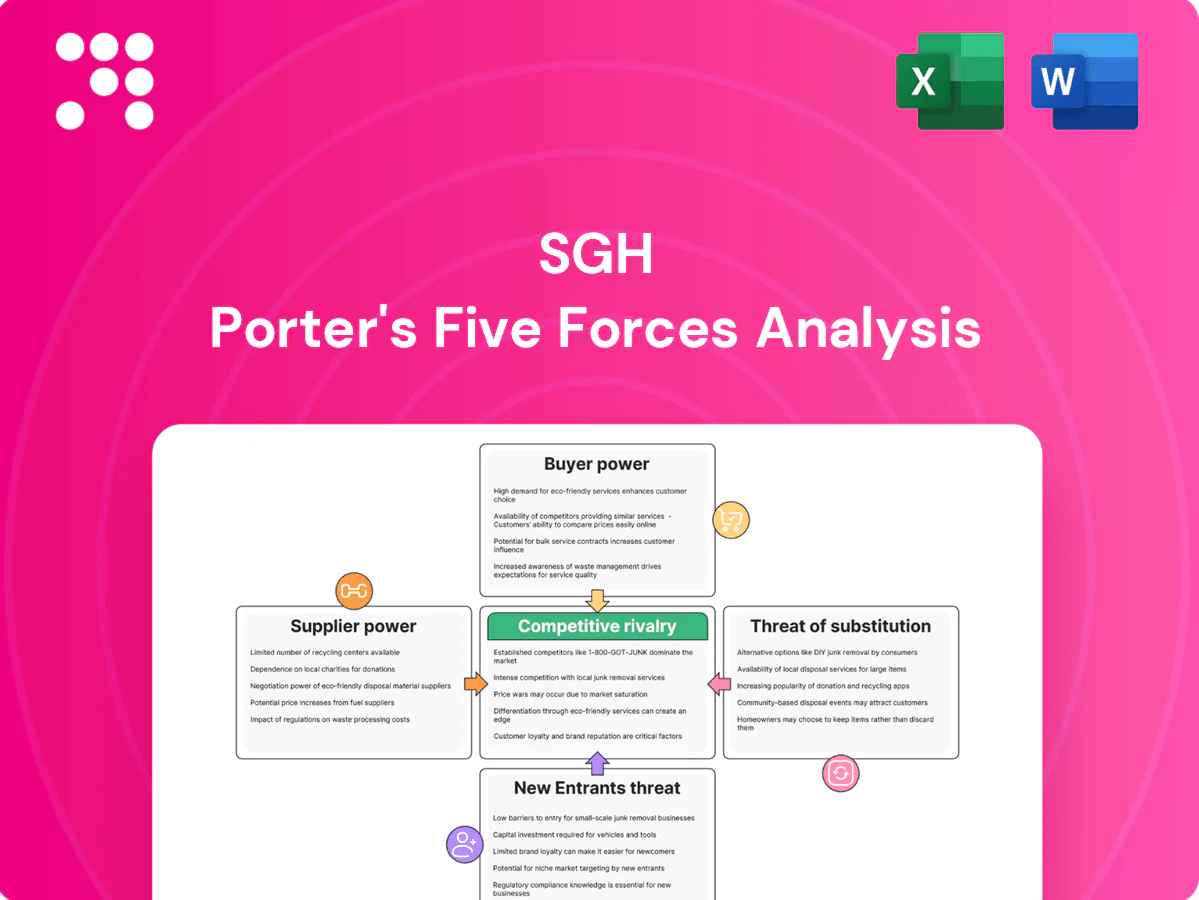

SGH faces a nuanced mix of supplier leverage, buyer sensitivity, and competitive rivalry that shapes its strategic options; substitute threats and entry barriers further complicate the picture. This concise snapshot highlights key pressures but only scratches the surface. Unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

OEM dependence on Caterpillar

SGH’s equipment arm relies heavily on Caterpillar as a sole-source OEM for machines and critical parts, and Caterpillar reported approximately $63.0 billion revenue in 2024, amplifying its pricing and delivery leverage over SGH. Contractual territory protections partially mitigate risk, but CAT’s design control and proprietary parts constrains substitution and aftermarket competition. Any supply disruption or policy shift at CAT can directly compress SGH margins and degrade service levels.

Specialized component and tech vendors

High-spec engines, hydraulics, telemetry and software updates come from few qualified vendors, raising switching costs and supplier leverage; long-term volume and service-level agreements help stabilize pricing and availability. Cybersecurity and software licensing further tilt power to vendors: the 2024 IBM Cost of a Data Breach Report cites an average breach cost of $4.45 million, increasing vendor negotiating weight.

Energy field services and drilling contractors

Beach Energy (ASX:BPT) upstream activity relies on rigs, tubulars, seismic and specialist contractors, and tight capacity cycles in 2024 have pushed day-rates and input costs materially higher. Multi-year frameworks, typically spanning 3–5 years, and counter-cyclical contracting have moderated cost spikes for Beach. Local content rules and remote-basin logistics in Australia reinforce supplier leverage and can extend lead times.

Media content and rights holders

Seven West Media faces strong negotiating power from sports leagues, studios and talent agencies; in 2024 escalating bids for premium sports and studio rights tightened margins as broadcasters globally spent tens of billions on rights and bundled digital packages, complicating economics.

Co-production deals and in-house content initiatives in 2024 partially offset dependency by lowering external commissioning costs and improving margin control.

- Suppliers: sports leagues, studios, talent agencies

- 2024 trend: premium/bundled digital rights drove higher fees

- Impact: margin compression for broadcasters

- Mitigation: co-production and in-house content reduced external spend

Skilled labor and safety-critical capabilities

Technicians, engineers and OH&S-qualified staff are scarce in mining and energy regions, giving suppliers strong leverage. Wage inflation and retention bonuses—often 20–40% of base for critical roles in 2024—raise operating costs and switching barriers. Apprenticeships and training pipelines mitigate shortages but require 3–4 years to deliver skilled staff. Project surges can push premiums another 15–30%, intensifying competition.

- High scarcity: concentrated in mining hubs

- Retention premiums: 20–40% in 2024

- Training lead time: 3–4 years

- Project surge premium: +15–30%

Supplier dominance: ~$63bn vendor scale, $4.45m breach risk, 20-40% staff premiums

Suppliers hold strong power: Caterpillar’s ~$63.0bn 2024 revenue and proprietary parts create pricing/leverage risk for SGH, while limited engine/software vendors raise switching costs. Cybersecurity/license costs (avg breach cost $4.45m in 2024) and skilled-staff premiums (20–40% in 2024) further tighten supplier leverage.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Caterpillar | $63.0bn revenue | Pricing/delivery leverage |

| Cyber/vendors | $4.45m breach cost | Negotiating weight |

| Skilled staff | 20–40% premium | Higher operating costs |

What is included in the product

Provides a tailored Porter's Five Forces analysis for SGH, uncovering competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and highlighting disruptive forces and strategic levers to protect and grow market share.

SGH’s Porter’s Five Forces one-sheet pinpoints competitive pain points and recommends targeted strategic levers to relieve pressure, enabling faster, evidence-based decisions. Clean visuals and editable inputs make it easy to tailor scenarios for boards, investors, or strategy sessions.

Customers Bargaining Power

Mining majors and contractors

Major miners and contractors (the Big 4 account for roughly 60% of seaborne iron ore) buy fleets and services at scale, with individual procurement rounds and fleet deals often exceeding US$100m, driving aggressive tendering and global benchmark pricing. Standardization and benchmarked tenders exert clear price pressure, but installed-base lock-in, uptime guarantees and long-term maintenance contracts (often 20–30% of lifecycle spend) limit switching and balance bargaining power.

Construction and infrastructure customers

Construction and infrastructure customers wield strong bargaining power as Coates Hire users can multi-source from competing hire firms; Coates is Australia's largest hire firm with 170+ depots, intensifying competition. Project-based demand drives rate negotiation and flexible terms, while bundled solutions, site services and digital fleet visibility raise stickiness. Effective utilization management is critical to defend price and margins.

Advertisers and media agencies

Ad buyers can fluidly shift spend across TV, BVOD, social and search as digital reached roughly 70% of global ad spend in 2024, increasing leverage over incumbent rates. Measurability and performance options (CPC/CPA) intensify pricing pressure on publishers. Premium live sport and news still command scarcity value, often commanding 2–3x CPMs that temper buyer power. Data-driven targeting and cross-platform packages can raise advertiser retention by ~20%, locking in budgets.

Energy offtakers and gas buyers

Industrial buyers and retailers in 2024 pressed SGH on volumes versus alternative gas and renewables, with TTF hub volatility (2024 avg ~€34/MWh) and Henry Hub (~$3.0/MMBtu) shaping negotiations; contract tenor, hub pricing and transport tariffs determined outcomes, while SGH’s portfolio optionality (covering >50% of supply) strengthens its position; regulatory price caps in some markets cut margins by up to ~20%.

- Buyers: leverage from alternatives

- Pricing: hub-driven (TTF €34/MWh 2024)

- Tenor & tariffs: key to terms

- SGH strength: >50% portfolio optionality

- Risk: price caps can cut ~20% margins

Aftermarket service customers

Maintenance buyers prioritize rapid parts availability and certified repairs, with 2024 surveys showing about 75% rank lead time as a top decision factor.

Non-OEM parts and independents, often 15–30% cheaper, compress aftermarket rates, while machine warranties and performance guarantees—with OEM retention around 70%—limit switching; predictive maintenance and uptime SLAs (market growth ~20% in 2024) differentiate providers and reduce buyer power.

Concentrated buyers and ad leverage; predictive maintenance up +20%

Large buyers (Big 4 ~60% seaborne iron ore) buy at scale (fleet deals >US$100m) forcing benchmarked pricing, but installed-base lock-in and 20–30% lifecycle maintenance contracts limit switching. Digital ad spend ~70% (2024) raises buyer leverage though premium sport/news command 2–3x CPMs. Energy buyers saw TTF ~€34/MWh (2024); SGH portfolio optionality >50% reduces exposure. Maintenance: 75% cite lead time; non-OEMs 15–30% cheaper; OEM retention ≈70%; predictive maintenance market +20% (2024).

| Metric | Value (2024) |

|---|---|

| Big 4 seaborne iron ore | ~60% |

| Fleet deal size | >US$100m |

| Digital ad spend | ~70% |

| TTF | €34/MWh |

| SGH optionality | >50% |

| Lead time priority | 75% |

| Non-OEM price delta | 15–30% |

| OEM retention | ≈70% |

| Predictive maintenance growth | +20% |

What You See Is What You Get

SGH Porter's Five Forces Analysis

This preview shows the exact SGH Porter's Five Forces analysis you'll receive upon purchase—no placeholders or mockups. The document displayed is the fully formatted, ready-to-use file available for immediate download and use. You're looking at the final deliverable; once payment is completed you’ll get instant access to this identical document.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

SGH faces a nuanced mix of supplier leverage, buyer sensitivity, and competitive rivalry that shapes its strategic options; substitute threats and entry barriers further complicate the picture. This concise snapshot highlights key pressures but only scratches the surface. Unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

OEM dependence on Caterpillar

SGH’s equipment arm relies heavily on Caterpillar as a sole-source OEM for machines and critical parts, and Caterpillar reported approximately $63.0 billion revenue in 2024, amplifying its pricing and delivery leverage over SGH. Contractual territory protections partially mitigate risk, but CAT’s design control and proprietary parts constrains substitution and aftermarket competition. Any supply disruption or policy shift at CAT can directly compress SGH margins and degrade service levels.

Specialized component and tech vendors

High-spec engines, hydraulics, telemetry and software updates come from few qualified vendors, raising switching costs and supplier leverage; long-term volume and service-level agreements help stabilize pricing and availability. Cybersecurity and software licensing further tilt power to vendors: the 2024 IBM Cost of a Data Breach Report cites an average breach cost of $4.45 million, increasing vendor negotiating weight.

Energy field services and drilling contractors

Beach Energy (ASX:BPT) upstream activity relies on rigs, tubulars, seismic and specialist contractors, and tight capacity cycles in 2024 have pushed day-rates and input costs materially higher. Multi-year frameworks, typically spanning 3–5 years, and counter-cyclical contracting have moderated cost spikes for Beach. Local content rules and remote-basin logistics in Australia reinforce supplier leverage and can extend lead times.

Media content and rights holders

Seven West Media faces strong negotiating power from sports leagues, studios and talent agencies; in 2024 escalating bids for premium sports and studio rights tightened margins as broadcasters globally spent tens of billions on rights and bundled digital packages, complicating economics.

Co-production deals and in-house content initiatives in 2024 partially offset dependency by lowering external commissioning costs and improving margin control.

- Suppliers: sports leagues, studios, talent agencies

- 2024 trend: premium/bundled digital rights drove higher fees

- Impact: margin compression for broadcasters

- Mitigation: co-production and in-house content reduced external spend

Skilled labor and safety-critical capabilities

Technicians, engineers and OH&S-qualified staff are scarce in mining and energy regions, giving suppliers strong leverage. Wage inflation and retention bonuses—often 20–40% of base for critical roles in 2024—raise operating costs and switching barriers. Apprenticeships and training pipelines mitigate shortages but require 3–4 years to deliver skilled staff. Project surges can push premiums another 15–30%, intensifying competition.

- High scarcity: concentrated in mining hubs

- Retention premiums: 20–40% in 2024

- Training lead time: 3–4 years

- Project surge premium: +15–30%

Supplier dominance: ~$63bn vendor scale, $4.45m breach risk, 20-40% staff premiums

Suppliers hold strong power: Caterpillar’s ~$63.0bn 2024 revenue and proprietary parts create pricing/leverage risk for SGH, while limited engine/software vendors raise switching costs. Cybersecurity/license costs (avg breach cost $4.45m in 2024) and skilled-staff premiums (20–40% in 2024) further tighten supplier leverage.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Caterpillar | $63.0bn revenue | Pricing/delivery leverage |

| Cyber/vendors | $4.45m breach cost | Negotiating weight |

| Skilled staff | 20–40% premium | Higher operating costs |

What is included in the product

Provides a tailored Porter's Five Forces analysis for SGH, uncovering competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and highlighting disruptive forces and strategic levers to protect and grow market share.

SGH’s Porter’s Five Forces one-sheet pinpoints competitive pain points and recommends targeted strategic levers to relieve pressure, enabling faster, evidence-based decisions. Clean visuals and editable inputs make it easy to tailor scenarios for boards, investors, or strategy sessions.

Customers Bargaining Power

Mining majors and contractors

Major miners and contractors (the Big 4 account for roughly 60% of seaborne iron ore) buy fleets and services at scale, with individual procurement rounds and fleet deals often exceeding US$100m, driving aggressive tendering and global benchmark pricing. Standardization and benchmarked tenders exert clear price pressure, but installed-base lock-in, uptime guarantees and long-term maintenance contracts (often 20–30% of lifecycle spend) limit switching and balance bargaining power.

Construction and infrastructure customers

Construction and infrastructure customers wield strong bargaining power as Coates Hire users can multi-source from competing hire firms; Coates is Australia's largest hire firm with 170+ depots, intensifying competition. Project-based demand drives rate negotiation and flexible terms, while bundled solutions, site services and digital fleet visibility raise stickiness. Effective utilization management is critical to defend price and margins.

Advertisers and media agencies

Ad buyers can fluidly shift spend across TV, BVOD, social and search as digital reached roughly 70% of global ad spend in 2024, increasing leverage over incumbent rates. Measurability and performance options (CPC/CPA) intensify pricing pressure on publishers. Premium live sport and news still command scarcity value, often commanding 2–3x CPMs that temper buyer power. Data-driven targeting and cross-platform packages can raise advertiser retention by ~20%, locking in budgets.

Energy offtakers and gas buyers

Industrial buyers and retailers in 2024 pressed SGH on volumes versus alternative gas and renewables, with TTF hub volatility (2024 avg ~€34/MWh) and Henry Hub (~$3.0/MMBtu) shaping negotiations; contract tenor, hub pricing and transport tariffs determined outcomes, while SGH’s portfolio optionality (covering >50% of supply) strengthens its position; regulatory price caps in some markets cut margins by up to ~20%.

- Buyers: leverage from alternatives

- Pricing: hub-driven (TTF €34/MWh 2024)

- Tenor & tariffs: key to terms

- SGH strength: >50% portfolio optionality

- Risk: price caps can cut ~20% margins

Aftermarket service customers

Maintenance buyers prioritize rapid parts availability and certified repairs, with 2024 surveys showing about 75% rank lead time as a top decision factor.

Non-OEM parts and independents, often 15–30% cheaper, compress aftermarket rates, while machine warranties and performance guarantees—with OEM retention around 70%—limit switching; predictive maintenance and uptime SLAs (market growth ~20% in 2024) differentiate providers and reduce buyer power.

Concentrated buyers and ad leverage; predictive maintenance up +20%

Large buyers (Big 4 ~60% seaborne iron ore) buy at scale (fleet deals >US$100m) forcing benchmarked pricing, but installed-base lock-in and 20–30% lifecycle maintenance contracts limit switching. Digital ad spend ~70% (2024) raises buyer leverage though premium sport/news command 2–3x CPMs. Energy buyers saw TTF ~€34/MWh (2024); SGH portfolio optionality >50% reduces exposure. Maintenance: 75% cite lead time; non-OEMs 15–30% cheaper; OEM retention ≈70%; predictive maintenance market +20% (2024).

| Metric | Value (2024) |

|---|---|

| Big 4 seaborne iron ore | ~60% |

| Fleet deal size | >US$100m |

| Digital ad spend | ~70% |

| TTF | €34/MWh |

| SGH optionality | >50% |

| Lead time priority | 75% |

| Non-OEM price delta | 15–30% |

| OEM retention | ≈70% |

| Predictive maintenance growth | +20% |

What You See Is What You Get

SGH Porter's Five Forces Analysis

This preview shows the exact SGH Porter's Five Forces analysis you'll receive upon purchase—no placeholders or mockups. The document displayed is the fully formatted, ready-to-use file available for immediate download and use. You're looking at the final deliverable; once payment is completed you’ll get instant access to this identical document.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

SGH faces a nuanced mix of supplier leverage, buyer sensitivity, and competitive rivalry that shapes its strategic options; substitute threats and entry barriers further complicate the picture. This concise snapshot highlights key pressures but only scratches the surface. Unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

OEM dependence on Caterpillar

SGH’s equipment arm relies heavily on Caterpillar as a sole-source OEM for machines and critical parts, and Caterpillar reported approximately $63.0 billion revenue in 2024, amplifying its pricing and delivery leverage over SGH. Contractual territory protections partially mitigate risk, but CAT’s design control and proprietary parts constrains substitution and aftermarket competition. Any supply disruption or policy shift at CAT can directly compress SGH margins and degrade service levels.

Specialized component and tech vendors

High-spec engines, hydraulics, telemetry and software updates come from few qualified vendors, raising switching costs and supplier leverage; long-term volume and service-level agreements help stabilize pricing and availability. Cybersecurity and software licensing further tilt power to vendors: the 2024 IBM Cost of a Data Breach Report cites an average breach cost of $4.45 million, increasing vendor negotiating weight.

Energy field services and drilling contractors

Beach Energy (ASX:BPT) upstream activity relies on rigs, tubulars, seismic and specialist contractors, and tight capacity cycles in 2024 have pushed day-rates and input costs materially higher. Multi-year frameworks, typically spanning 3–5 years, and counter-cyclical contracting have moderated cost spikes for Beach. Local content rules and remote-basin logistics in Australia reinforce supplier leverage and can extend lead times.

Media content and rights holders

Seven West Media faces strong negotiating power from sports leagues, studios and talent agencies; in 2024 escalating bids for premium sports and studio rights tightened margins as broadcasters globally spent tens of billions on rights and bundled digital packages, complicating economics.

Co-production deals and in-house content initiatives in 2024 partially offset dependency by lowering external commissioning costs and improving margin control.

- Suppliers: sports leagues, studios, talent agencies

- 2024 trend: premium/bundled digital rights drove higher fees

- Impact: margin compression for broadcasters

- Mitigation: co-production and in-house content reduced external spend

Skilled labor and safety-critical capabilities

Technicians, engineers and OH&S-qualified staff are scarce in mining and energy regions, giving suppliers strong leverage. Wage inflation and retention bonuses—often 20–40% of base for critical roles in 2024—raise operating costs and switching barriers. Apprenticeships and training pipelines mitigate shortages but require 3–4 years to deliver skilled staff. Project surges can push premiums another 15–30%, intensifying competition.

- High scarcity: concentrated in mining hubs

- Retention premiums: 20–40% in 2024

- Training lead time: 3–4 years

- Project surge premium: +15–30%

Supplier dominance: ~$63bn vendor scale, $4.45m breach risk, 20-40% staff premiums

Suppliers hold strong power: Caterpillar’s ~$63.0bn 2024 revenue and proprietary parts create pricing/leverage risk for SGH, while limited engine/software vendors raise switching costs. Cybersecurity/license costs (avg breach cost $4.45m in 2024) and skilled-staff premiums (20–40% in 2024) further tighten supplier leverage.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Caterpillar | $63.0bn revenue | Pricing/delivery leverage |

| Cyber/vendors | $4.45m breach cost | Negotiating weight |

| Skilled staff | 20–40% premium | Higher operating costs |

What is included in the product

Provides a tailored Porter's Five Forces analysis for SGH, uncovering competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and highlighting disruptive forces and strategic levers to protect and grow market share.

SGH’s Porter’s Five Forces one-sheet pinpoints competitive pain points and recommends targeted strategic levers to relieve pressure, enabling faster, evidence-based decisions. Clean visuals and editable inputs make it easy to tailor scenarios for boards, investors, or strategy sessions.

Customers Bargaining Power

Mining majors and contractors

Major miners and contractors (the Big 4 account for roughly 60% of seaborne iron ore) buy fleets and services at scale, with individual procurement rounds and fleet deals often exceeding US$100m, driving aggressive tendering and global benchmark pricing. Standardization and benchmarked tenders exert clear price pressure, but installed-base lock-in, uptime guarantees and long-term maintenance contracts (often 20–30% of lifecycle spend) limit switching and balance bargaining power.

Construction and infrastructure customers

Construction and infrastructure customers wield strong bargaining power as Coates Hire users can multi-source from competing hire firms; Coates is Australia's largest hire firm with 170+ depots, intensifying competition. Project-based demand drives rate negotiation and flexible terms, while bundled solutions, site services and digital fleet visibility raise stickiness. Effective utilization management is critical to defend price and margins.

Advertisers and media agencies

Ad buyers can fluidly shift spend across TV, BVOD, social and search as digital reached roughly 70% of global ad spend in 2024, increasing leverage over incumbent rates. Measurability and performance options (CPC/CPA) intensify pricing pressure on publishers. Premium live sport and news still command scarcity value, often commanding 2–3x CPMs that temper buyer power. Data-driven targeting and cross-platform packages can raise advertiser retention by ~20%, locking in budgets.

Energy offtakers and gas buyers

Industrial buyers and retailers in 2024 pressed SGH on volumes versus alternative gas and renewables, with TTF hub volatility (2024 avg ~€34/MWh) and Henry Hub (~$3.0/MMBtu) shaping negotiations; contract tenor, hub pricing and transport tariffs determined outcomes, while SGH’s portfolio optionality (covering >50% of supply) strengthens its position; regulatory price caps in some markets cut margins by up to ~20%.

- Buyers: leverage from alternatives

- Pricing: hub-driven (TTF €34/MWh 2024)

- Tenor & tariffs: key to terms

- SGH strength: >50% portfolio optionality

- Risk: price caps can cut ~20% margins

Aftermarket service customers

Maintenance buyers prioritize rapid parts availability and certified repairs, with 2024 surveys showing about 75% rank lead time as a top decision factor.

Non-OEM parts and independents, often 15–30% cheaper, compress aftermarket rates, while machine warranties and performance guarantees—with OEM retention around 70%—limit switching; predictive maintenance and uptime SLAs (market growth ~20% in 2024) differentiate providers and reduce buyer power.

Concentrated buyers and ad leverage; predictive maintenance up +20%

Large buyers (Big 4 ~60% seaborne iron ore) buy at scale (fleet deals >US$100m) forcing benchmarked pricing, but installed-base lock-in and 20–30% lifecycle maintenance contracts limit switching. Digital ad spend ~70% (2024) raises buyer leverage though premium sport/news command 2–3x CPMs. Energy buyers saw TTF ~€34/MWh (2024); SGH portfolio optionality >50% reduces exposure. Maintenance: 75% cite lead time; non-OEMs 15–30% cheaper; OEM retention ≈70%; predictive maintenance market +20% (2024).

| Metric | Value (2024) |

|---|---|

| Big 4 seaborne iron ore | ~60% |

| Fleet deal size | >US$100m |

| Digital ad spend | ~70% |

| TTF | €34/MWh |

| SGH optionality | >50% |

| Lead time priority | 75% |

| Non-OEM price delta | 15–30% |

| OEM retention | ≈70% |

| Predictive maintenance growth | +20% |

What You See Is What You Get

SGH Porter's Five Forces Analysis

This preview shows the exact SGH Porter's Five Forces analysis you'll receive upon purchase—no placeholders or mockups. The document displayed is the fully formatted, ready-to-use file available for immediate download and use. You're looking at the final deliverable; once payment is completed you’ll get instant access to this identical document.