Samsung Fire & Marine Business Model Canvas

Insurer Business Model Canvas — Segments, Value Props, Channels & Revenue Mechanics

Unlock the full strategic blueprint behind Samsung Fire & Marine with our Business Model Canvas — detailing customer segments, value propositions, channels, and revenue mechanics. This concise, company-specific canvas reveals how the firm scales, manages risk, and captures market share. Ideal for investors, consultants, and strategists seeking actionable insights. Download the editable Word and Excel files to start benchmarking today.

Partnerships

Global reinsurers

Global reinsurers absorb peak risks and stabilize Samsung Fire & Marine’s loss ratios across catastrophe and large commercial exposures, with the reinsurance market providing roughly USD 320 billion in premium capacity in 2023–24. They enable capacity expansion and product innovation by sharing underwriting insights and co-developing bespoke covers. Long-term treaty arrangements and facultative placements improve capital efficiency and support regulatory solvency metrics. Strategic treaties reduce earnings volatility and free up balance-sheet capacity.

Auto OEMs and dealerships

Tie-ups with automakers and dealer networks let Samsung Fire & Marine sell policies at point of purchase, lifting conversion rates by an industry-range 20–30% and accelerating premium capture. Integrated claims and repair flows cut cycle times and leakage by roughly 15–25%, improving loss control. Co-marketing with OEMs boosts awareness and sales; telematics partnerships enhance pricing accuracy and can lower claim frequency/loss ratios by about 10–20% per 2024 industry studies.

Healthcare providers and repair networks

Preferred hospital and clinic networks allow Samsung Fire & Marine, South Korea's largest non-life insurer, to better control medical claims and improve member experience, serving over 10 million customers with focused pathways that lower unnecessary costs. Authorized auto repair shops secure quality, negotiated rates and about 15–20% faster turnaround on average. Data sharing across partners improves fraud detection—addressing roughly 10% of claim leakage—and supports outcomes management and readmission reductions.

Banks, brokers, and aggregators

Banks, brokers, and aggregators broaden Samsung Fire & Marine’s access to diversified retail and SME segments, enabling scale across touchpoints. In 2024 bancassurance and comparison platforms boosted digital lead volumes and reduced acquisition costs, with industry reports citing mid‑20% uplifts in online lead generation. Structured referral agreements enable systematic cross‑sell of savings and protection products, improving persistency and margin.

- Partners: banks, brokers, aggregators

- 2024 impact: ~mid‑20% digital lead uplift

- Benefit: lower acquisition cost, higher cross‑sell

- Mechanism: structured referral agreements

Technology and data vendors

Technology and data vendors — insurtech, analytics, and cloud partners — accelerate Samsung Fire & Marine’s digital transformation and AI-driven underwriting, with global insurtech investment about $5.6B in 2024 and cloud spend enabling real-time pricing and claims automation.

Cybersecurity vendors protect sensitive policyholder data amid rising threats; telematics, IoT, and geospatial providers improve risk models and loss prevention, boosting predictive accuracy and reducing claims frequency.

- Insurtech: $5.6B global funding (2024)

- Cloud: real-time underwriting & claims automation

- Cybersecurity: data protection for customer PII

- Telematics/IoT/Geospatial: enhanced risk scoring, loss prevention

Reinsurers, OEMs, Banks and Insurtech: Boosting conversions, cutting claims and costs

Global reinsurers (market ~USD 320B in 2023–24) stabilize catastrophe and large-loss volatility and free capital. OEM/dealer tie‑ups lift policy conversion ~20–30% and cut claims leakage via integrated repairs (15–25% faster). Bancassurance/aggregators drove mid‑20% digital lead uplifts in 2024, lowering acquisition cost. Insurtech funding $5.6B (2024) and telematics (10–20% claim reduction) boost pricing and fraud control.

| Partner | 2024/2023–24 data | Primary benefit |

|---|---|---|

| Reinsurers | ~USD 320B capacity | Loss stabilization, capital relief |

| OEMs/Dealers | Conversion +20–30% | Point‑of‑sale sales, faster repairs |

| Banks/Aggregators | Digital leads +~mid‑20% | Lower acquisition, cross‑sell |

| Insurtech/Cloud | $5.6B funding | Real‑time pricing, automation |

| Telematics/IoT | Claims -10–20% | Risk scoring, loss prevention |

What is included in the product

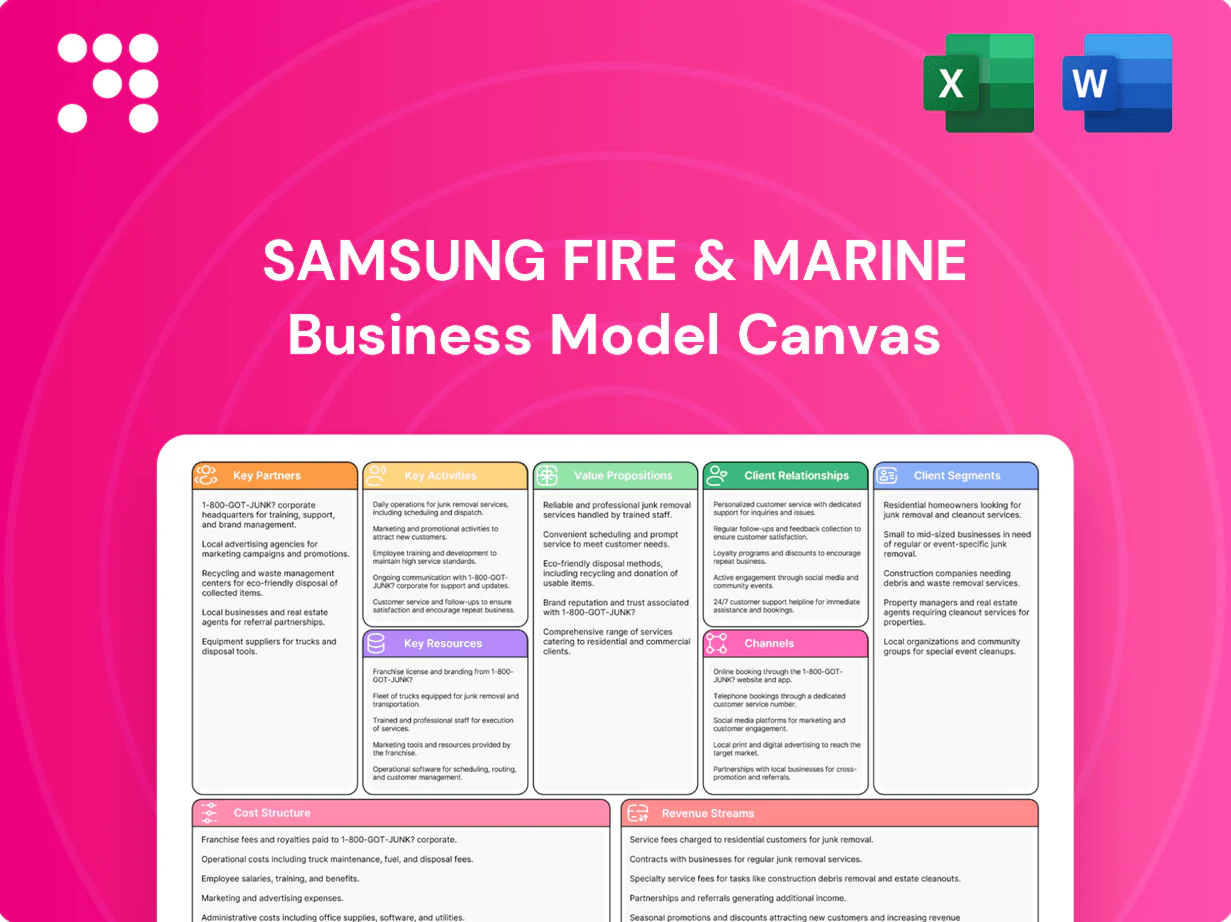

A comprehensive Business Model Canvas for Samsung Fire & Marine outlining customer segments, channels, value propositions, revenue streams, key resources/partners, activities and cost structure across the 9 BMC blocks, with linked competitive advantages, SWOT insights and polished narrative for presentations, investor review and strategic planning.

High-level snapshot of Samsung Fire & Marine’s insurance business with editable cells to quickly pinpoint underwriting, distribution and risk-management gaps.

Activities

Risk underwriting and pricing

Assessing risk profiles, calibrating rates and setting terms underpin portfolio profitability at Samsung Fire & Marine, South Korea’s largest non-life insurer with about 30% domestic market share. Actuarial modeling and predictive analytics drive selection and coverage design, integrating granular exposure data and scenario testing. Continuous monitoring of loss trends and real-time signals adjusts appetites and pricing as claims patterns evolve.

Claims handling and recovery

Fast, fair claims settlement drives retention and brand trust, with Samsung Fire & Marine using customer-centric SLAs to reduce churn and protect market share. Fraud analytics, subrogation and salvage programs raised recovery rates, supporting loss-cost control and profitability. Industry studies in 2024 showed digital FNOL and network steering can cut cycle times ~40% and lower claims costs substantially.

Product development and innovation

Designing modular P&C, auto, long-term savings and personal accident products lets Samsung Fire & Marine, Korea's largest non-life insurer, tailor coverage across customer segments and channels in 2024. Embedded and usage-based insurance initiatives expand addressable markets and distribution partnerships. IFRS 17 (effective 2023) and local regulatory rules guide product features to ensure compliance and capital efficiency.

Asset management of insurance float

Prudent investment of insurance float converts premiums into stable investment income by prioritizing high-quality fixed income and diversified credit exposure while opportunistically allocating to alternatives to enhance returns.

Strategic asset allocation balances yield, liquidity, and risk; ALM aligns asset duration with liability profiles and regulatory capital requirements to control solvency volatility.

- tag:investment-income

- tag:asset-allocation

- tag:liquidity-risk

- tag:ALM-duration

Distribution and partner management

Distribution and partner management coordinates multi-channel sales—direct, bancassurance and brokers—to maximize coverage of retail and corporate segments, supporting Samsung Fire & Marine’s >20% Korean non-life market share (2024) and a 40,000+ agent/broker network. Training and incentive programs raised agent productivity and persistency, while strict partner governance enforces service quality and regulatory compliance.

- Multi-channel coordination: retail + corporate coverage

- Training & incentives: uplift agent/broker productivity

- Governance: service quality & compliance

Risk pricing, ≈30% share; FNOL cuts cycles ≈40%

Samsung Fire & Marine focuses on risk selection and pricing (≈30% domestic market share), fast digital claims (digital FNOL cuts cycle times ~40% in 2024), modular product design under IFRS 17 (effective 2023) and float management aligned with ALM. Multi-channel distribution (40,000+ agents/brokers) and partner governance sustain growth and persistency.

| Metric | 2024 |

|---|---|

| Market share | ≈30% |

| Agents/Brokers | 40,000+ |

| Digital FNOL impact | ≈−40% cycle time |

Preview Before You Purchase

Business Model Canvas

The document you’re previewing is the exact Samsung Fire & Marine Business Model Canvas you’ll receive after purchase. It’s not a mockup—this live preview reflects the full, professionally formatted deliverable. Upon purchase you’ll instantly download the complete file, ready to edit, present, and share in Word and Excel formats. No surprises—what you see is what you’ll own.

Insurer Business Model Canvas — Segments, Value Props, Channels & Revenue Mechanics

Unlock the full strategic blueprint behind Samsung Fire & Marine with our Business Model Canvas — detailing customer segments, value propositions, channels, and revenue mechanics. This concise, company-specific canvas reveals how the firm scales, manages risk, and captures market share. Ideal for investors, consultants, and strategists seeking actionable insights. Download the editable Word and Excel files to start benchmarking today.

Partnerships

Global reinsurers

Global reinsurers absorb peak risks and stabilize Samsung Fire & Marine’s loss ratios across catastrophe and large commercial exposures, with the reinsurance market providing roughly USD 320 billion in premium capacity in 2023–24. They enable capacity expansion and product innovation by sharing underwriting insights and co-developing bespoke covers. Long-term treaty arrangements and facultative placements improve capital efficiency and support regulatory solvency metrics. Strategic treaties reduce earnings volatility and free up balance-sheet capacity.

Auto OEMs and dealerships

Tie-ups with automakers and dealer networks let Samsung Fire & Marine sell policies at point of purchase, lifting conversion rates by an industry-range 20–30% and accelerating premium capture. Integrated claims and repair flows cut cycle times and leakage by roughly 15–25%, improving loss control. Co-marketing with OEMs boosts awareness and sales; telematics partnerships enhance pricing accuracy and can lower claim frequency/loss ratios by about 10–20% per 2024 industry studies.

Healthcare providers and repair networks

Preferred hospital and clinic networks allow Samsung Fire & Marine, South Korea's largest non-life insurer, to better control medical claims and improve member experience, serving over 10 million customers with focused pathways that lower unnecessary costs. Authorized auto repair shops secure quality, negotiated rates and about 15–20% faster turnaround on average. Data sharing across partners improves fraud detection—addressing roughly 10% of claim leakage—and supports outcomes management and readmission reductions.

Banks, brokers, and aggregators

Banks, brokers, and aggregators broaden Samsung Fire & Marine’s access to diversified retail and SME segments, enabling scale across touchpoints. In 2024 bancassurance and comparison platforms boosted digital lead volumes and reduced acquisition costs, with industry reports citing mid‑20% uplifts in online lead generation. Structured referral agreements enable systematic cross‑sell of savings and protection products, improving persistency and margin.

- Partners: banks, brokers, aggregators

- 2024 impact: ~mid‑20% digital lead uplift

- Benefit: lower acquisition cost, higher cross‑sell

- Mechanism: structured referral agreements

Technology and data vendors

Technology and data vendors — insurtech, analytics, and cloud partners — accelerate Samsung Fire & Marine’s digital transformation and AI-driven underwriting, with global insurtech investment about $5.6B in 2024 and cloud spend enabling real-time pricing and claims automation.

Cybersecurity vendors protect sensitive policyholder data amid rising threats; telematics, IoT, and geospatial providers improve risk models and loss prevention, boosting predictive accuracy and reducing claims frequency.

- Insurtech: $5.6B global funding (2024)

- Cloud: real-time underwriting & claims automation

- Cybersecurity: data protection for customer PII

- Telematics/IoT/Geospatial: enhanced risk scoring, loss prevention

Reinsurers, OEMs, Banks and Insurtech: Boosting conversions, cutting claims and costs

Global reinsurers (market ~USD 320B in 2023–24) stabilize catastrophe and large-loss volatility and free capital. OEM/dealer tie‑ups lift policy conversion ~20–30% and cut claims leakage via integrated repairs (15–25% faster). Bancassurance/aggregators drove mid‑20% digital lead uplifts in 2024, lowering acquisition cost. Insurtech funding $5.6B (2024) and telematics (10–20% claim reduction) boost pricing and fraud control.

| Partner | 2024/2023–24 data | Primary benefit |

|---|---|---|

| Reinsurers | ~USD 320B capacity | Loss stabilization, capital relief |

| OEMs/Dealers | Conversion +20–30% | Point‑of‑sale sales, faster repairs |

| Banks/Aggregators | Digital leads +~mid‑20% | Lower acquisition, cross‑sell |

| Insurtech/Cloud | $5.6B funding | Real‑time pricing, automation |

| Telematics/IoT | Claims -10–20% | Risk scoring, loss prevention |

What is included in the product

A comprehensive Business Model Canvas for Samsung Fire & Marine outlining customer segments, channels, value propositions, revenue streams, key resources/partners, activities and cost structure across the 9 BMC blocks, with linked competitive advantages, SWOT insights and polished narrative for presentations, investor review and strategic planning.

High-level snapshot of Samsung Fire & Marine’s insurance business with editable cells to quickly pinpoint underwriting, distribution and risk-management gaps.

Activities

Risk underwriting and pricing

Assessing risk profiles, calibrating rates and setting terms underpin portfolio profitability at Samsung Fire & Marine, South Korea’s largest non-life insurer with about 30% domestic market share. Actuarial modeling and predictive analytics drive selection and coverage design, integrating granular exposure data and scenario testing. Continuous monitoring of loss trends and real-time signals adjusts appetites and pricing as claims patterns evolve.

Claims handling and recovery

Fast, fair claims settlement drives retention and brand trust, with Samsung Fire & Marine using customer-centric SLAs to reduce churn and protect market share. Fraud analytics, subrogation and salvage programs raised recovery rates, supporting loss-cost control and profitability. Industry studies in 2024 showed digital FNOL and network steering can cut cycle times ~40% and lower claims costs substantially.

Product development and innovation

Designing modular P&C, auto, long-term savings and personal accident products lets Samsung Fire & Marine, Korea's largest non-life insurer, tailor coverage across customer segments and channels in 2024. Embedded and usage-based insurance initiatives expand addressable markets and distribution partnerships. IFRS 17 (effective 2023) and local regulatory rules guide product features to ensure compliance and capital efficiency.

Asset management of insurance float

Prudent investment of insurance float converts premiums into stable investment income by prioritizing high-quality fixed income and diversified credit exposure while opportunistically allocating to alternatives to enhance returns.

Strategic asset allocation balances yield, liquidity, and risk; ALM aligns asset duration with liability profiles and regulatory capital requirements to control solvency volatility.

- tag:investment-income

- tag:asset-allocation

- tag:liquidity-risk

- tag:ALM-duration

Distribution and partner management

Distribution and partner management coordinates multi-channel sales—direct, bancassurance and brokers—to maximize coverage of retail and corporate segments, supporting Samsung Fire & Marine’s >20% Korean non-life market share (2024) and a 40,000+ agent/broker network. Training and incentive programs raised agent productivity and persistency, while strict partner governance enforces service quality and regulatory compliance.

- Multi-channel coordination: retail + corporate coverage

- Training & incentives: uplift agent/broker productivity

- Governance: service quality & compliance

Risk pricing, ≈30% share; FNOL cuts cycles ≈40%

Samsung Fire & Marine focuses on risk selection and pricing (≈30% domestic market share), fast digital claims (digital FNOL cuts cycle times ~40% in 2024), modular product design under IFRS 17 (effective 2023) and float management aligned with ALM. Multi-channel distribution (40,000+ agents/brokers) and partner governance sustain growth and persistency.

| Metric | 2024 |

|---|---|

| Market share | ≈30% |

| Agents/Brokers | 40,000+ |

| Digital FNOL impact | ≈−40% cycle time |

Preview Before You Purchase

Business Model Canvas

The document you’re previewing is the exact Samsung Fire & Marine Business Model Canvas you’ll receive after purchase. It’s not a mockup—this live preview reflects the full, professionally formatted deliverable. Upon purchase you’ll instantly download the complete file, ready to edit, present, and share in Word and Excel formats. No surprises—what you see is what you’ll own.

Description

Insurer Business Model Canvas — Segments, Value Props, Channels & Revenue Mechanics

Unlock the full strategic blueprint behind Samsung Fire & Marine with our Business Model Canvas — detailing customer segments, value propositions, channels, and revenue mechanics. This concise, company-specific canvas reveals how the firm scales, manages risk, and captures market share. Ideal for investors, consultants, and strategists seeking actionable insights. Download the editable Word and Excel files to start benchmarking today.

Partnerships

Global reinsurers

Global reinsurers absorb peak risks and stabilize Samsung Fire & Marine’s loss ratios across catastrophe and large commercial exposures, with the reinsurance market providing roughly USD 320 billion in premium capacity in 2023–24. They enable capacity expansion and product innovation by sharing underwriting insights and co-developing bespoke covers. Long-term treaty arrangements and facultative placements improve capital efficiency and support regulatory solvency metrics. Strategic treaties reduce earnings volatility and free up balance-sheet capacity.

Auto OEMs and dealerships

Tie-ups with automakers and dealer networks let Samsung Fire & Marine sell policies at point of purchase, lifting conversion rates by an industry-range 20–30% and accelerating premium capture. Integrated claims and repair flows cut cycle times and leakage by roughly 15–25%, improving loss control. Co-marketing with OEMs boosts awareness and sales; telematics partnerships enhance pricing accuracy and can lower claim frequency/loss ratios by about 10–20% per 2024 industry studies.

Healthcare providers and repair networks

Preferred hospital and clinic networks allow Samsung Fire & Marine, South Korea's largest non-life insurer, to better control medical claims and improve member experience, serving over 10 million customers with focused pathways that lower unnecessary costs. Authorized auto repair shops secure quality, negotiated rates and about 15–20% faster turnaround on average. Data sharing across partners improves fraud detection—addressing roughly 10% of claim leakage—and supports outcomes management and readmission reductions.

Banks, brokers, and aggregators

Banks, brokers, and aggregators broaden Samsung Fire & Marine’s access to diversified retail and SME segments, enabling scale across touchpoints. In 2024 bancassurance and comparison platforms boosted digital lead volumes and reduced acquisition costs, with industry reports citing mid‑20% uplifts in online lead generation. Structured referral agreements enable systematic cross‑sell of savings and protection products, improving persistency and margin.

- Partners: banks, brokers, aggregators

- 2024 impact: ~mid‑20% digital lead uplift

- Benefit: lower acquisition cost, higher cross‑sell

- Mechanism: structured referral agreements

Technology and data vendors

Technology and data vendors — insurtech, analytics, and cloud partners — accelerate Samsung Fire & Marine’s digital transformation and AI-driven underwriting, with global insurtech investment about $5.6B in 2024 and cloud spend enabling real-time pricing and claims automation.

Cybersecurity vendors protect sensitive policyholder data amid rising threats; telematics, IoT, and geospatial providers improve risk models and loss prevention, boosting predictive accuracy and reducing claims frequency.

- Insurtech: $5.6B global funding (2024)

- Cloud: real-time underwriting & claims automation

- Cybersecurity: data protection for customer PII

- Telematics/IoT/Geospatial: enhanced risk scoring, loss prevention

Reinsurers, OEMs, Banks and Insurtech: Boosting conversions, cutting claims and costs

Global reinsurers (market ~USD 320B in 2023–24) stabilize catastrophe and large-loss volatility and free capital. OEM/dealer tie‑ups lift policy conversion ~20–30% and cut claims leakage via integrated repairs (15–25% faster). Bancassurance/aggregators drove mid‑20% digital lead uplifts in 2024, lowering acquisition cost. Insurtech funding $5.6B (2024) and telematics (10–20% claim reduction) boost pricing and fraud control.

| Partner | 2024/2023–24 data | Primary benefit |

|---|---|---|

| Reinsurers | ~USD 320B capacity | Loss stabilization, capital relief |

| OEMs/Dealers | Conversion +20–30% | Point‑of‑sale sales, faster repairs |

| Banks/Aggregators | Digital leads +~mid‑20% | Lower acquisition, cross‑sell |

| Insurtech/Cloud | $5.6B funding | Real‑time pricing, automation |

| Telematics/IoT | Claims -10–20% | Risk scoring, loss prevention |

What is included in the product

A comprehensive Business Model Canvas for Samsung Fire & Marine outlining customer segments, channels, value propositions, revenue streams, key resources/partners, activities and cost structure across the 9 BMC blocks, with linked competitive advantages, SWOT insights and polished narrative for presentations, investor review and strategic planning.

High-level snapshot of Samsung Fire & Marine’s insurance business with editable cells to quickly pinpoint underwriting, distribution and risk-management gaps.

Activities

Risk underwriting and pricing

Assessing risk profiles, calibrating rates and setting terms underpin portfolio profitability at Samsung Fire & Marine, South Korea’s largest non-life insurer with about 30% domestic market share. Actuarial modeling and predictive analytics drive selection and coverage design, integrating granular exposure data and scenario testing. Continuous monitoring of loss trends and real-time signals adjusts appetites and pricing as claims patterns evolve.

Claims handling and recovery

Fast, fair claims settlement drives retention and brand trust, with Samsung Fire & Marine using customer-centric SLAs to reduce churn and protect market share. Fraud analytics, subrogation and salvage programs raised recovery rates, supporting loss-cost control and profitability. Industry studies in 2024 showed digital FNOL and network steering can cut cycle times ~40% and lower claims costs substantially.

Product development and innovation

Designing modular P&C, auto, long-term savings and personal accident products lets Samsung Fire & Marine, Korea's largest non-life insurer, tailor coverage across customer segments and channels in 2024. Embedded and usage-based insurance initiatives expand addressable markets and distribution partnerships. IFRS 17 (effective 2023) and local regulatory rules guide product features to ensure compliance and capital efficiency.

Asset management of insurance float

Prudent investment of insurance float converts premiums into stable investment income by prioritizing high-quality fixed income and diversified credit exposure while opportunistically allocating to alternatives to enhance returns.

Strategic asset allocation balances yield, liquidity, and risk; ALM aligns asset duration with liability profiles and regulatory capital requirements to control solvency volatility.

- tag:investment-income

- tag:asset-allocation

- tag:liquidity-risk

- tag:ALM-duration

Distribution and partner management

Distribution and partner management coordinates multi-channel sales—direct, bancassurance and brokers—to maximize coverage of retail and corporate segments, supporting Samsung Fire & Marine’s >20% Korean non-life market share (2024) and a 40,000+ agent/broker network. Training and incentive programs raised agent productivity and persistency, while strict partner governance enforces service quality and regulatory compliance.

- Multi-channel coordination: retail + corporate coverage

- Training & incentives: uplift agent/broker productivity

- Governance: service quality & compliance

Risk pricing, ≈30% share; FNOL cuts cycles ≈40%

Samsung Fire & Marine focuses on risk selection and pricing (≈30% domestic market share), fast digital claims (digital FNOL cuts cycle times ~40% in 2024), modular product design under IFRS 17 (effective 2023) and float management aligned with ALM. Multi-channel distribution (40,000+ agents/brokers) and partner governance sustain growth and persistency.

| Metric | 2024 |

|---|---|

| Market share | ≈30% |

| Agents/Brokers | 40,000+ |

| Digital FNOL impact | ≈−40% cycle time |

Preview Before You Purchase

Business Model Canvas

The document you’re previewing is the exact Samsung Fire & Marine Business Model Canvas you’ll receive after purchase. It’s not a mockup—this live preview reflects the full, professionally formatted deliverable. Upon purchase you’ll instantly download the complete file, ready to edit, present, and share in Word and Excel formats. No surprises—what you see is what you’ll own.