St. Galler Kantonalbank Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

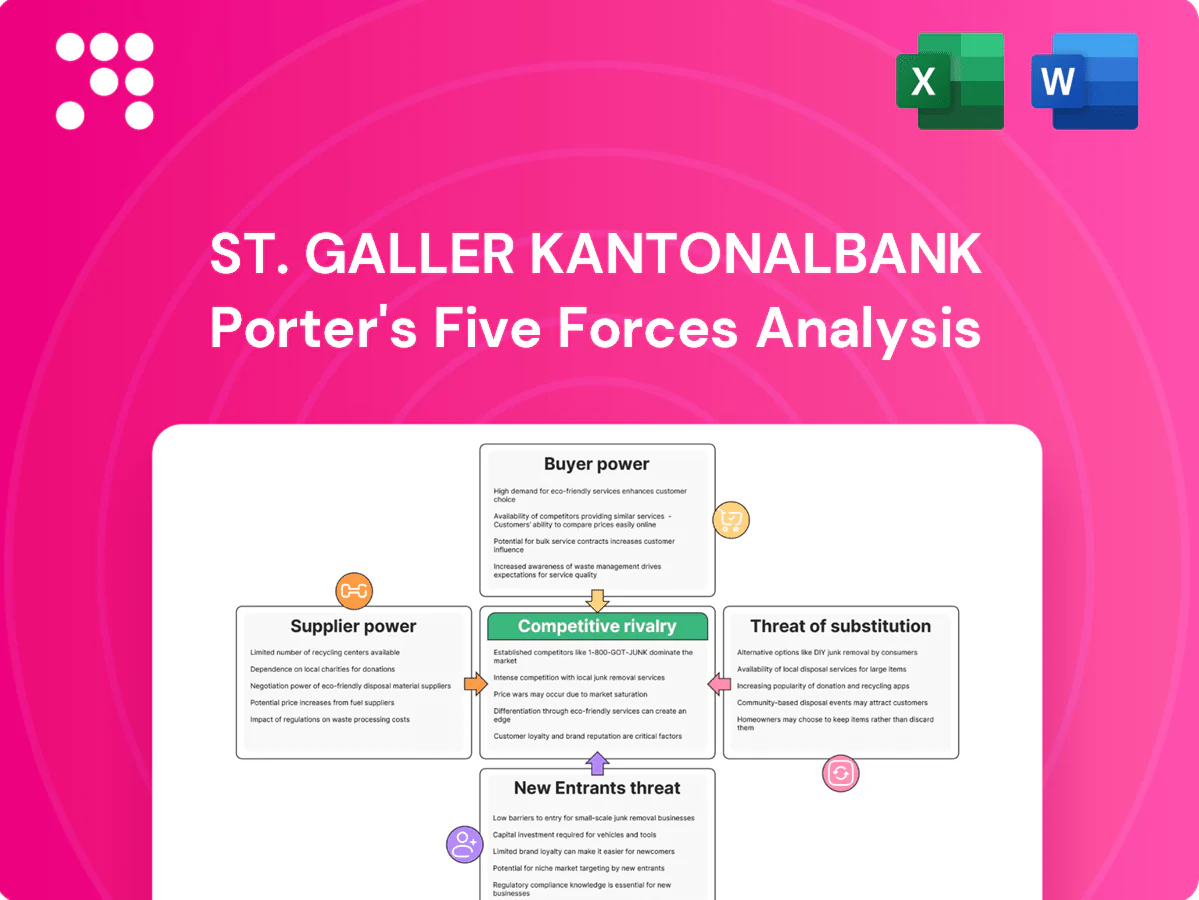

St. Galler Kantonalbank faces moderate rivalry driven by strong local incumbents and cost pressures from larger Swiss banks, while customer loyalty and cantonal guarantees limit new entrants. Digital challengers and fintechs raise substitute risks, and supplier power is muted by standardized banking services. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to St. Galler Kantonalbank.

Suppliers Bargaining Power

Dependence on tech platforms

Core banking, payments and cybersecurity vendors are highly concentrated, giving suppliers pricing and switching leverage; long implementation cycles—typically 24–36 months—increase lock‑in and integration risk. Vendor roadmaps therefore materially shape SGKB’s digital pace and cost base, while consortium buying and multi‑vendor strategies can improve negotiation power and have been shown to reduce procurement and licence costs by up to 20% in industry case studies (2024).

Wholesale funding providers

Wholesale funding providers — covered bond investors, interbank lines and repo markets — drive SGKB’s funding costs in rate-tight cycles; access depends directly on credit ratings, collateral quality and liquidity buffers. Market stress can widen spreads rapidly and squeeze NIM. Stable retail deposits reduce but do not remove reliance on wholesale markets.

Payments and card networks

For St. Galler Kantonalbank, dominant schemes like Visa/Mastercard and Swiss rails (SIX) set interchange and scheme fees—typically around 0.2–1.5% interchange and 0.3–1.2% acquirer fees in Europe/Switzerland in 2024—limiting supplier negotiation. Certification and compliance (PCI DSS) create fixed costs often around CHF 50k–100k initially plus annual audits. Few true alternatives constrain bargaining power, though multi-year volume commitments can secure marginal price relief of roughly 5–20%.

Regulatory and capital “suppliers”

FINMA, the SNB and Basel rules effectively supply SGKB with license and balance-sheet capacity: Basel III sets CET1 minimum 4.5%, a capital conservation buffer 2.5%, a leverage ratio floor 3% and an LCR requirement of 100%, while FINMA/SNB supervision enforces national buffers and liquidity expectations. Higher capital and liquidity demands directly raise funding and ROE pressure; regulatory shifts can reprioritize IT and credit investments and compress returns. Strong, proactive risk governance and capital planning reduce supervisory frictions and costly remediation.

- CET1 minimum 4.5%

- Conservation buffer 2.5%

- Leverage ratio floor 3%, LCR 100%

Skilled talent and advisors

Skilled quant, IT, risk and relationship talent is regionally scarce, exacerbated by a tight Swiss labor market (unemployment ~2.0% in 2024), increasing recruitment difficulty. Wage inflation and poaching by larger banks and fintechs lift compensation costs. Dependency on specialized legal and compliance advisers raises outsourcer power, while a strong employer brand and training pipelines can mitigate supplier leverage.

- Talent scarcity

- Wage inflation

- Advisor dependency

- Brand & training

Concentrated IT/vendor power, 24–36 month rollouts raise supplier leverage; consortium buys cut ~20%

Concentrated IT/vendors and 24–36 month implementations increase supplier leverage; consortium buying can cut costs ~20% (2024). Wholesale funding costs driven by ratings and repo spreads; retail deposits reduce but do not eliminate reliance. Scheme fees ~0.2–1.5% interchange (2024); regulatory buffers (CET1 4.5% +2.5% CB, LCR 100%) and Swiss unemployment ~2.0% tighten talent supply.

| Metric | 2024 Value |

|---|---|

| IT implementation | 24–36 months |

| Procurement saving (case studies) | up to 20% |

| Interchange fees | 0.2–1.5% |

| CET1 min + buffer | 4.5% + 2.5% |

| LCR | 100% |

| Swiss unemployment | ~2.0% |

What is included in the product

Concise Porter’s Five Forces analysis for St. Galler Kantonalbank that identifies competitive intensity, customer and supplier bargaining power, threat of new entrants and substitutes, and regulatory/market barriers to protect regional market share and profitability.

St. Galler Kantonalbank Porter's Five Forces one-sheet — a clear, ready-to-use summary of competitive pressures to speed board-level decisions and cut analysis time. Swap in latest data or duplicate tabs for scenario comparisons without macros, making strategic planning fast and accessible.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors can instantly compare yields, increasing repricing pressure when the SNB policy rate stood at 1.75% in 2024; digital onboarding cuts switching friction to minutes, boosting churn risk. SGKB must balance retention with net interest margin protection by avoiding blanket rate matching. Tiered pricing and loyalty bundles—targeting high-balance segments—can materially reduce outflows.

SMEs and public institutions

SMEs and public institutions (SMEs = 99.7% of Swiss firms, employing ~66% of the workforce) exert bargaining power by negotiating lending margins, fees and covenants. Their multi-banking behaviour—common, with many SMEs maintaining two or more banking relationships—increases leverage in negotiations. Deep local relationships and high-quality service, plus tailored cash-management and guarantee packages, can lock value despite price pressure.

Wealth and affluent clients

Transparent fee benchmarking raises bargaining power among wealthy clients, with 2024 surveys showing about 68% of Swiss affluent investors comparing advisory fees; retention hinges on net-of-fee performance and a broad product shelf. Distinctive advisory models—high-touch, goals-based planning—can justify premium fees, while hybrid and robo-advice options help segment and serve price-sensitive cohorts without diluting core margins.

Digital-first retail customers

Digital-first retail customers demand 24/7, low-fee services shaped by neobanks; by 2024 neobanks held over 200 million global accounts, resetting expectations. Frictionless UX is a purchasing criterion, not a bonus, and outages or clunky flows trigger rapid churn for Swiss regional banks like St. Galler Kantonalbank. Ongoing UX investment reduces sensitivity to minor price differences and improves retention.

- 24/7 low-fee expectation

- UX = purchase criterion

- Outages drive churn

- UX lowers price sensitivity

Mortgage borrowers

Mortgage borrowers exert strong bargaining power: highly comparable offers via brokers and platforms intensify price pressure, while rapid shifts between fixed and SARON-linked loans follow short-term rate moves. Ancillary cross-sell (insurance, accounts) can defend margins; speed and certainty of approval often win business even with small price gaps.

- ≈CHF 1.25tn Swiss mortgage stock (2024)

- Platform/broker distribution rising, increasing price transparency

- Approval speed & cross-sell lift retention and NIMs

Customers pressure banks: SNB 1.75%, neobanks, SMEs and mortgages

Customers wield high bargaining power: rate-sensitive depositors (SNB policy rate 1.75% in 2024) and digital-first retail clients (neobanks >200m accounts globally) pressure yields and fees; SMEs (99.7% of firms, ~66% workforce) and mortgage borrowers (~CHF 1.25tn stock) leverage multi-banking and platforms to demand better margins, fees and speed. Segmented pricing, loyalty bundles and fast approvals defend NIMs.

| Segment | Metric (2024) | Impact |

|---|---|---|

| Depositors | SNB 1.75% | Repricing pressure |

| SMEs | 99.7% firms; ~66% workforce | Negotiation leverage |

| Mortgages | ≈CHF 1.25tn | Price transparency |

What You See Is What You Get

St. Galler Kantonalbank Porter's Five Forces Analysis

This preview displays the exact St. Galler Kantonalbank Porter's Five Forces analysis you’ll receive upon purchase—no samples, no placeholders. The full, professionally formatted document is ready for immediate download and use. What you see is precisely what will be delivered to you.

Go Beyond the Preview—Access the Full Strategic Report

St. Galler Kantonalbank faces moderate rivalry driven by strong local incumbents and cost pressures from larger Swiss banks, while customer loyalty and cantonal guarantees limit new entrants. Digital challengers and fintechs raise substitute risks, and supplier power is muted by standardized banking services. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to St. Galler Kantonalbank.

Suppliers Bargaining Power

Dependence on tech platforms

Core banking, payments and cybersecurity vendors are highly concentrated, giving suppliers pricing and switching leverage; long implementation cycles—typically 24–36 months—increase lock‑in and integration risk. Vendor roadmaps therefore materially shape SGKB’s digital pace and cost base, while consortium buying and multi‑vendor strategies can improve negotiation power and have been shown to reduce procurement and licence costs by up to 20% in industry case studies (2024).

Wholesale funding providers

Wholesale funding providers — covered bond investors, interbank lines and repo markets — drive SGKB’s funding costs in rate-tight cycles; access depends directly on credit ratings, collateral quality and liquidity buffers. Market stress can widen spreads rapidly and squeeze NIM. Stable retail deposits reduce but do not remove reliance on wholesale markets.

Payments and card networks

For St. Galler Kantonalbank, dominant schemes like Visa/Mastercard and Swiss rails (SIX) set interchange and scheme fees—typically around 0.2–1.5% interchange and 0.3–1.2% acquirer fees in Europe/Switzerland in 2024—limiting supplier negotiation. Certification and compliance (PCI DSS) create fixed costs often around CHF 50k–100k initially plus annual audits. Few true alternatives constrain bargaining power, though multi-year volume commitments can secure marginal price relief of roughly 5–20%.

Regulatory and capital “suppliers”

FINMA, the SNB and Basel rules effectively supply SGKB with license and balance-sheet capacity: Basel III sets CET1 minimum 4.5%, a capital conservation buffer 2.5%, a leverage ratio floor 3% and an LCR requirement of 100%, while FINMA/SNB supervision enforces national buffers and liquidity expectations. Higher capital and liquidity demands directly raise funding and ROE pressure; regulatory shifts can reprioritize IT and credit investments and compress returns. Strong, proactive risk governance and capital planning reduce supervisory frictions and costly remediation.

- CET1 minimum 4.5%

- Conservation buffer 2.5%

- Leverage ratio floor 3%, LCR 100%

Skilled talent and advisors

Skilled quant, IT, risk and relationship talent is regionally scarce, exacerbated by a tight Swiss labor market (unemployment ~2.0% in 2024), increasing recruitment difficulty. Wage inflation and poaching by larger banks and fintechs lift compensation costs. Dependency on specialized legal and compliance advisers raises outsourcer power, while a strong employer brand and training pipelines can mitigate supplier leverage.

- Talent scarcity

- Wage inflation

- Advisor dependency

- Brand & training

Concentrated IT/vendor power, 24–36 month rollouts raise supplier leverage; consortium buys cut ~20%

Concentrated IT/vendors and 24–36 month implementations increase supplier leverage; consortium buying can cut costs ~20% (2024). Wholesale funding costs driven by ratings and repo spreads; retail deposits reduce but do not eliminate reliance. Scheme fees ~0.2–1.5% interchange (2024); regulatory buffers (CET1 4.5% +2.5% CB, LCR 100%) and Swiss unemployment ~2.0% tighten talent supply.

| Metric | 2024 Value |

|---|---|

| IT implementation | 24–36 months |

| Procurement saving (case studies) | up to 20% |

| Interchange fees | 0.2–1.5% |

| CET1 min + buffer | 4.5% + 2.5% |

| LCR | 100% |

| Swiss unemployment | ~2.0% |

What is included in the product

Concise Porter’s Five Forces analysis for St. Galler Kantonalbank that identifies competitive intensity, customer and supplier bargaining power, threat of new entrants and substitutes, and regulatory/market barriers to protect regional market share and profitability.

St. Galler Kantonalbank Porter's Five Forces one-sheet — a clear, ready-to-use summary of competitive pressures to speed board-level decisions and cut analysis time. Swap in latest data or duplicate tabs for scenario comparisons without macros, making strategic planning fast and accessible.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors can instantly compare yields, increasing repricing pressure when the SNB policy rate stood at 1.75% in 2024; digital onboarding cuts switching friction to minutes, boosting churn risk. SGKB must balance retention with net interest margin protection by avoiding blanket rate matching. Tiered pricing and loyalty bundles—targeting high-balance segments—can materially reduce outflows.

SMEs and public institutions

SMEs and public institutions (SMEs = 99.7% of Swiss firms, employing ~66% of the workforce) exert bargaining power by negotiating lending margins, fees and covenants. Their multi-banking behaviour—common, with many SMEs maintaining two or more banking relationships—increases leverage in negotiations. Deep local relationships and high-quality service, plus tailored cash-management and guarantee packages, can lock value despite price pressure.

Wealth and affluent clients

Transparent fee benchmarking raises bargaining power among wealthy clients, with 2024 surveys showing about 68% of Swiss affluent investors comparing advisory fees; retention hinges on net-of-fee performance and a broad product shelf. Distinctive advisory models—high-touch, goals-based planning—can justify premium fees, while hybrid and robo-advice options help segment and serve price-sensitive cohorts without diluting core margins.

Digital-first retail customers

Digital-first retail customers demand 24/7, low-fee services shaped by neobanks; by 2024 neobanks held over 200 million global accounts, resetting expectations. Frictionless UX is a purchasing criterion, not a bonus, and outages or clunky flows trigger rapid churn for Swiss regional banks like St. Galler Kantonalbank. Ongoing UX investment reduces sensitivity to minor price differences and improves retention.

- 24/7 low-fee expectation

- UX = purchase criterion

- Outages drive churn

- UX lowers price sensitivity

Mortgage borrowers

Mortgage borrowers exert strong bargaining power: highly comparable offers via brokers and platforms intensify price pressure, while rapid shifts between fixed and SARON-linked loans follow short-term rate moves. Ancillary cross-sell (insurance, accounts) can defend margins; speed and certainty of approval often win business even with small price gaps.

- ≈CHF 1.25tn Swiss mortgage stock (2024)

- Platform/broker distribution rising, increasing price transparency

- Approval speed & cross-sell lift retention and NIMs

Customers pressure banks: SNB 1.75%, neobanks, SMEs and mortgages

Customers wield high bargaining power: rate-sensitive depositors (SNB policy rate 1.75% in 2024) and digital-first retail clients (neobanks >200m accounts globally) pressure yields and fees; SMEs (99.7% of firms, ~66% workforce) and mortgage borrowers (~CHF 1.25tn stock) leverage multi-banking and platforms to demand better margins, fees and speed. Segmented pricing, loyalty bundles and fast approvals defend NIMs.

| Segment | Metric (2024) | Impact |

|---|---|---|

| Depositors | SNB 1.75% | Repricing pressure |

| SMEs | 99.7% firms; ~66% workforce | Negotiation leverage |

| Mortgages | ≈CHF 1.25tn | Price transparency |

What You See Is What You Get

St. Galler Kantonalbank Porter's Five Forces Analysis

This preview displays the exact St. Galler Kantonalbank Porter's Five Forces analysis you’ll receive upon purchase—no samples, no placeholders. The full, professionally formatted document is ready for immediate download and use. What you see is precisely what will be delivered to you.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

St. Galler Kantonalbank faces moderate rivalry driven by strong local incumbents and cost pressures from larger Swiss banks, while customer loyalty and cantonal guarantees limit new entrants. Digital challengers and fintechs raise substitute risks, and supplier power is muted by standardized banking services. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to St. Galler Kantonalbank.

Suppliers Bargaining Power

Dependence on tech platforms

Core banking, payments and cybersecurity vendors are highly concentrated, giving suppliers pricing and switching leverage; long implementation cycles—typically 24–36 months—increase lock‑in and integration risk. Vendor roadmaps therefore materially shape SGKB’s digital pace and cost base, while consortium buying and multi‑vendor strategies can improve negotiation power and have been shown to reduce procurement and licence costs by up to 20% in industry case studies (2024).

Wholesale funding providers

Wholesale funding providers — covered bond investors, interbank lines and repo markets — drive SGKB’s funding costs in rate-tight cycles; access depends directly on credit ratings, collateral quality and liquidity buffers. Market stress can widen spreads rapidly and squeeze NIM. Stable retail deposits reduce but do not remove reliance on wholesale markets.

Payments and card networks

For St. Galler Kantonalbank, dominant schemes like Visa/Mastercard and Swiss rails (SIX) set interchange and scheme fees—typically around 0.2–1.5% interchange and 0.3–1.2% acquirer fees in Europe/Switzerland in 2024—limiting supplier negotiation. Certification and compliance (PCI DSS) create fixed costs often around CHF 50k–100k initially plus annual audits. Few true alternatives constrain bargaining power, though multi-year volume commitments can secure marginal price relief of roughly 5–20%.

Regulatory and capital “suppliers”

FINMA, the SNB and Basel rules effectively supply SGKB with license and balance-sheet capacity: Basel III sets CET1 minimum 4.5%, a capital conservation buffer 2.5%, a leverage ratio floor 3% and an LCR requirement of 100%, while FINMA/SNB supervision enforces national buffers and liquidity expectations. Higher capital and liquidity demands directly raise funding and ROE pressure; regulatory shifts can reprioritize IT and credit investments and compress returns. Strong, proactive risk governance and capital planning reduce supervisory frictions and costly remediation.

- CET1 minimum 4.5%

- Conservation buffer 2.5%

- Leverage ratio floor 3%, LCR 100%

Skilled talent and advisors

Skilled quant, IT, risk and relationship talent is regionally scarce, exacerbated by a tight Swiss labor market (unemployment ~2.0% in 2024), increasing recruitment difficulty. Wage inflation and poaching by larger banks and fintechs lift compensation costs. Dependency on specialized legal and compliance advisers raises outsourcer power, while a strong employer brand and training pipelines can mitigate supplier leverage.

- Talent scarcity

- Wage inflation

- Advisor dependency

- Brand & training

Concentrated IT/vendor power, 24–36 month rollouts raise supplier leverage; consortium buys cut ~20%

Concentrated IT/vendors and 24–36 month implementations increase supplier leverage; consortium buying can cut costs ~20% (2024). Wholesale funding costs driven by ratings and repo spreads; retail deposits reduce but do not eliminate reliance. Scheme fees ~0.2–1.5% interchange (2024); regulatory buffers (CET1 4.5% +2.5% CB, LCR 100%) and Swiss unemployment ~2.0% tighten talent supply.

| Metric | 2024 Value |

|---|---|

| IT implementation | 24–36 months |

| Procurement saving (case studies) | up to 20% |

| Interchange fees | 0.2–1.5% |

| CET1 min + buffer | 4.5% + 2.5% |

| LCR | 100% |

| Swiss unemployment | ~2.0% |

What is included in the product

Concise Porter’s Five Forces analysis for St. Galler Kantonalbank that identifies competitive intensity, customer and supplier bargaining power, threat of new entrants and substitutes, and regulatory/market barriers to protect regional market share and profitability.

St. Galler Kantonalbank Porter's Five Forces one-sheet — a clear, ready-to-use summary of competitive pressures to speed board-level decisions and cut analysis time. Swap in latest data or duplicate tabs for scenario comparisons without macros, making strategic planning fast and accessible.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors can instantly compare yields, increasing repricing pressure when the SNB policy rate stood at 1.75% in 2024; digital onboarding cuts switching friction to minutes, boosting churn risk. SGKB must balance retention with net interest margin protection by avoiding blanket rate matching. Tiered pricing and loyalty bundles—targeting high-balance segments—can materially reduce outflows.

SMEs and public institutions

SMEs and public institutions (SMEs = 99.7% of Swiss firms, employing ~66% of the workforce) exert bargaining power by negotiating lending margins, fees and covenants. Their multi-banking behaviour—common, with many SMEs maintaining two or more banking relationships—increases leverage in negotiations. Deep local relationships and high-quality service, plus tailored cash-management and guarantee packages, can lock value despite price pressure.

Wealth and affluent clients

Transparent fee benchmarking raises bargaining power among wealthy clients, with 2024 surveys showing about 68% of Swiss affluent investors comparing advisory fees; retention hinges on net-of-fee performance and a broad product shelf. Distinctive advisory models—high-touch, goals-based planning—can justify premium fees, while hybrid and robo-advice options help segment and serve price-sensitive cohorts without diluting core margins.

Digital-first retail customers

Digital-first retail customers demand 24/7, low-fee services shaped by neobanks; by 2024 neobanks held over 200 million global accounts, resetting expectations. Frictionless UX is a purchasing criterion, not a bonus, and outages or clunky flows trigger rapid churn for Swiss regional banks like St. Galler Kantonalbank. Ongoing UX investment reduces sensitivity to minor price differences and improves retention.

- 24/7 low-fee expectation

- UX = purchase criterion

- Outages drive churn

- UX lowers price sensitivity

Mortgage borrowers

Mortgage borrowers exert strong bargaining power: highly comparable offers via brokers and platforms intensify price pressure, while rapid shifts between fixed and SARON-linked loans follow short-term rate moves. Ancillary cross-sell (insurance, accounts) can defend margins; speed and certainty of approval often win business even with small price gaps.

- ≈CHF 1.25tn Swiss mortgage stock (2024)

- Platform/broker distribution rising, increasing price transparency

- Approval speed & cross-sell lift retention and NIMs

Customers pressure banks: SNB 1.75%, neobanks, SMEs and mortgages

Customers wield high bargaining power: rate-sensitive depositors (SNB policy rate 1.75% in 2024) and digital-first retail clients (neobanks >200m accounts globally) pressure yields and fees; SMEs (99.7% of firms, ~66% workforce) and mortgage borrowers (~CHF 1.25tn stock) leverage multi-banking and platforms to demand better margins, fees and speed. Segmented pricing, loyalty bundles and fast approvals defend NIMs.

| Segment | Metric (2024) | Impact |

|---|---|---|

| Depositors | SNB 1.75% | Repricing pressure |

| SMEs | 99.7% firms; ~66% workforce | Negotiation leverage |

| Mortgages | ≈CHF 1.25tn | Price transparency |

What You See Is What You Get

St. Galler Kantonalbank Porter's Five Forces Analysis

This preview displays the exact St. Galler Kantonalbank Porter's Five Forces analysis you’ll receive upon purchase—no samples, no placeholders. The full, professionally formatted document is ready for immediate download and use. What you see is precisely what will be delivered to you.