St. Galler Kantonalbank PESTLE Analysis

Your Competitive Advantage Starts with This Report

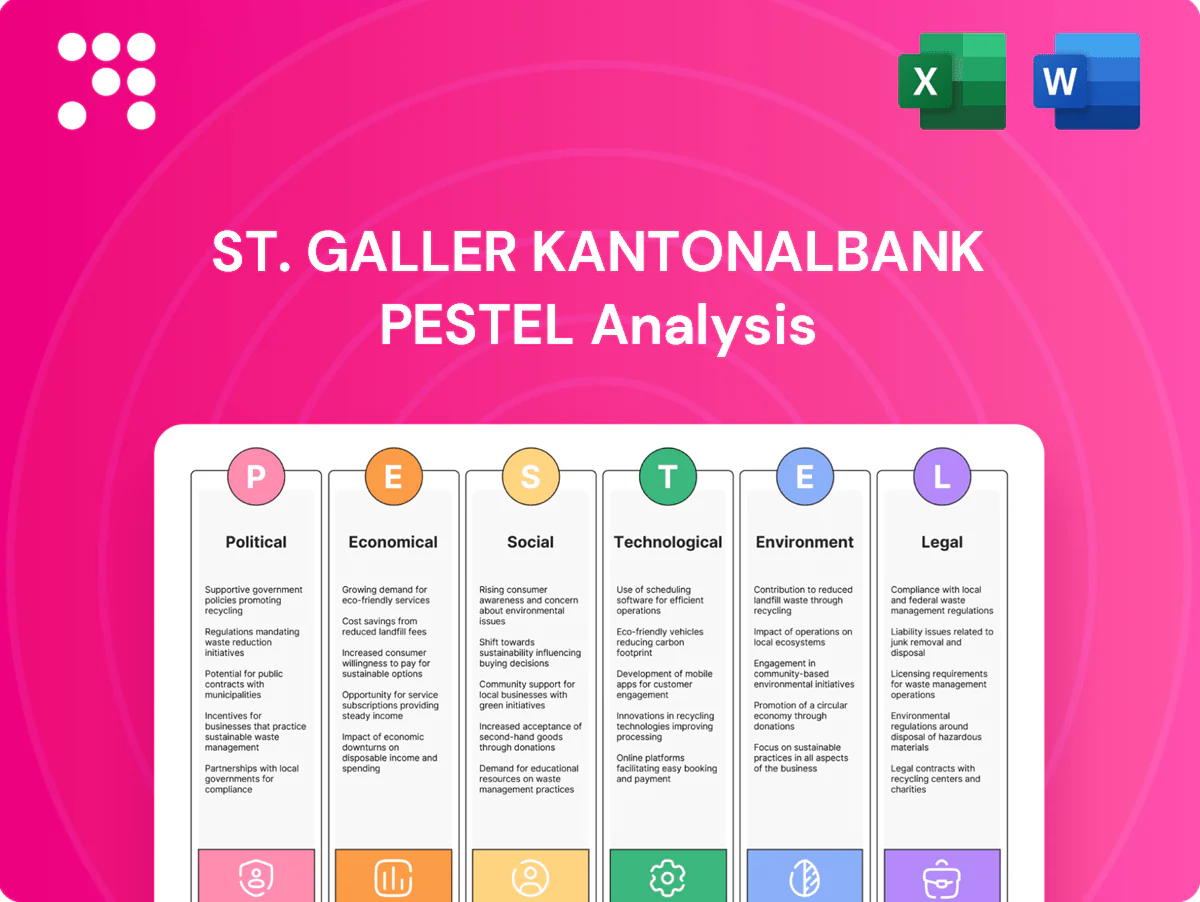

Our PESTLE analysis for St. Galler Kantonalbank reveals how political regulation, Swiss economic stability, shifting social trust, technological banking trends and environmental compliance shape its strategic risks and opportunities. Ideal for investors and strategists. Purchase the full, downloadable report for actionable insights.

Political factors

Cantonal ownership influence

Majority public ownership by the Canton of St. Gallen shapes SGKBs strategy, constraining risk appetite and emphasizing community obligations over aggressive expansion. Political stakeholders expect preferential local lending and stability, pressuring management to prioritize credit availability for regional SMEs and public projects. Governance must balance profitability with explicit public-interest mandates. Shifts in cantonal priorities can reallocate capital and strategic focus.

Swiss federal stability

Switzerland’s consensus-driven federal politics deliver predictable policy and budgets, enabling St. Galler Kantonalbank to plan long-term with confidence; public debt remains modest at roughly 40% of GDP (2024), supporting fiscal headroom. Low geopolitical risk and a strong sovereign profile keep funding costs competitive and client trust high. Policy shifts are gradual, allowing the bank proactive adaptation and reliable countercyclical support if needed.

EU relations and market access

Switzerland's non-EU status prevents passporting, constraining seamless cross-border banking despite the EU accounting for roughly 50% of Swiss trade. Ongoing bilateral framework tensions make equivalence decisions uncertain, directly affecting wealth management and corporate client access. SGKB must therefore implement country-by-country onboarding and tailor product permissions, with political outcomes materially influencing future cross-border growth.

Sanctions and foreign policy alignment

Switzerland continued aligning with major EU and US sanctions regimes in 2024, expanding SECO-maintained consolidated lists and heightening screening and reporting obligations for banks; St. Galler Kantonalbank faces increased compliance complexity and operational overhead as political shifts can abruptly affect specific client segments.

- Compliance scope: alignment with EU/US sanctions (2024)

- Operational impact: higher screening/reporting workload

- Risk: sudden client segmentation changes from political moves

- Mitigation: robust policies to avoid enforcement and reputational harm

Local public policy expectations

St. Galler Kantonalbank faces cantonal expectations to support SMEs, housing and regional development in a canton of about 511,000 residents (2023); Swiss SMEs constitute over 99% of companies, underscoring political pressure to prioritize local lending. Political scrutiny rises in downturns or restructurings, and stakeholder pushback can constrain branch closures or price changes. Transparent, frequent communication preserves its license to operate.

- SME support: over 99% of Swiss firms

- Canton pop: ~511,000 (2023)

- High scrutiny in downturns

- Transparency = sustained license

Canton majority ownership: conservative SME & housing focus; ~40% debt

Public majority ownership by Canton of St. Gallen (pop ~511,000 in 2023) forces conservative strategy, SME and housing support (>99% of Swiss firms) and limits risk appetite. Stable federal politics and ~40% public debt (2024) enable long-term planning, while non-EU status and 2024 alignment with EU/US sanctions raise cross-border and compliance costs.

| Metric | Value |

|---|---|

| Canton pop (2023) | ~511,000 |

| Public debt (CH, 2024) | ~40% GDP |

| SME share | >99% |

| EU trade share | ~50% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect St. Galler Kantonalbank, with data-driven, region-specific insights and forward-looking scenarios to identify threats, opportunities and strategic responses for executives, investors and advisors.

Concise, visually segmented PESTLE summary for St. Galler Kantonalbank that’s easy to slot into presentations or strategy sessions, share across teams, and customize with notes to support quick alignment on external risks and market positioning.

Economic factors

SNB rate cycle and NIM

SNB policy—at 1.75% (July 2025)—materially drives St. Galler Kantonalbank NIM: rate hikes raise deposit beta risks but boost asset yields, while cuts can compress NIM by several dozen basis points; balance‑sheet repricing speed and a deposit mix skewed to sight deposits increase earnings sensitivity. Hedging and fee‑rich product mix are key levers to protect margins.

Regional SME dynamics

St. Gallen’s SME base, reflecting Switzerland’s SME sector which comprises over 99% of firms and employs about 67% of the workforce, anchors SGKB’s lending and fee income through broad business banking relationships. Cyclical slowdowns elevate credit risk particularly in manufacturing, construction and services where regional order books dipped in 2023–24. Industry concentration in textiles and machinery necessitates prudent underwriting and sector limits. Close relationship banking enables early risk identification and workout coordination.

Housing and mortgage market

High home prices and affordability rules—including a statutory minimum downpayment of 20%—constrain demand and keep average mortgage LTVs conservative while Switzerland's mortgage stock exceeds CHF 1.2 trillion. Real estate cycles drive volatile provisioning needs and can materially increase capital consumption during corrections. Rising demand for energy‑efficient renovations opens green‑lending niches, and conservative Swiss underwriting supports strong asset quality.

CHF strength and wealth flows

Strong CHF acts as a safe‑haven magnet—supporting inflows that bolstered Swiss banking deposits during 2024—while weighing on exporters among SKB clients and compressing margin opportunities; currency swings also change reported AUM and fee income when translated to CHF, with Swiss banks holding over CHF 10 trillion in client assets (2024).

- Safe‑haven inflows: positive for deposits

- Export pressure: margin and credit risk for corporates

- Translation risk: AUM and fee volatility

- Rising hedging demand: private and corporate clients

Inflation and cost discipline

Generally low Swiss inflation (CPI 2024: ~1.1%) has kept wage and vendor cost growth muted, but 2025 YTD inflation (~2.0%) and SNB policy rate 1.75% are squeezing budgets; efficiency programs and digitization are used to offset margin pressure. Pricing power remains limited versus larger banks and neobanks, so emphasis on advisory value underpins fee income.

- Swiss CPI 2024 ~1.1%

- 2025 YTD inflation ~2.0%

- SNB policy rate 1.75% (Jul 2025)

- Digitization and efficiencies reduce costs, preserve fees

Canton majority ownership: conservative SME & housing focus; ~40% debt

SNB rate 1.75% (Jul 2025) drives NIM volatility; deposit beta and sight‑deposit mix raise earnings sensitivity. Swiss CPI 2024 ~1.1% (2025 YTD ~2.0%) pressures costs; mortgage stock CHF 1.2tn and CHF 10tn client assets shape balance‑sheet risks and fee volatility.

| Metric | Value |

|---|---|

| SNB policy rate | 1.75% (Jul 2025) |

| CPI | 2024: ~1.1% · 2025 YTD: ~2.0% |

| Mortgage stock | CHF 1.2tn |

| Swiss client assets | CHF 10tn (2024) |

Preview the Actual Deliverable

St. Galler Kantonalbank PESTLE Analysis

The preview shown here is the exact St. Galler Kantonalbank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured and ready to use. The layout, content and conclusions match the downloadable file; no placeholders, no surprises.

Your Competitive Advantage Starts with This Report

Our PESTLE analysis for St. Galler Kantonalbank reveals how political regulation, Swiss economic stability, shifting social trust, technological banking trends and environmental compliance shape its strategic risks and opportunities. Ideal for investors and strategists. Purchase the full, downloadable report for actionable insights.

Political factors

Cantonal ownership influence

Majority public ownership by the Canton of St. Gallen shapes SGKBs strategy, constraining risk appetite and emphasizing community obligations over aggressive expansion. Political stakeholders expect preferential local lending and stability, pressuring management to prioritize credit availability for regional SMEs and public projects. Governance must balance profitability with explicit public-interest mandates. Shifts in cantonal priorities can reallocate capital and strategic focus.

Swiss federal stability

Switzerland’s consensus-driven federal politics deliver predictable policy and budgets, enabling St. Galler Kantonalbank to plan long-term with confidence; public debt remains modest at roughly 40% of GDP (2024), supporting fiscal headroom. Low geopolitical risk and a strong sovereign profile keep funding costs competitive and client trust high. Policy shifts are gradual, allowing the bank proactive adaptation and reliable countercyclical support if needed.

EU relations and market access

Switzerland's non-EU status prevents passporting, constraining seamless cross-border banking despite the EU accounting for roughly 50% of Swiss trade. Ongoing bilateral framework tensions make equivalence decisions uncertain, directly affecting wealth management and corporate client access. SGKB must therefore implement country-by-country onboarding and tailor product permissions, with political outcomes materially influencing future cross-border growth.

Sanctions and foreign policy alignment

Switzerland continued aligning with major EU and US sanctions regimes in 2024, expanding SECO-maintained consolidated lists and heightening screening and reporting obligations for banks; St. Galler Kantonalbank faces increased compliance complexity and operational overhead as political shifts can abruptly affect specific client segments.

- Compliance scope: alignment with EU/US sanctions (2024)

- Operational impact: higher screening/reporting workload

- Risk: sudden client segmentation changes from political moves

- Mitigation: robust policies to avoid enforcement and reputational harm

Local public policy expectations

St. Galler Kantonalbank faces cantonal expectations to support SMEs, housing and regional development in a canton of about 511,000 residents (2023); Swiss SMEs constitute over 99% of companies, underscoring political pressure to prioritize local lending. Political scrutiny rises in downturns or restructurings, and stakeholder pushback can constrain branch closures or price changes. Transparent, frequent communication preserves its license to operate.

- SME support: over 99% of Swiss firms

- Canton pop: ~511,000 (2023)

- High scrutiny in downturns

- Transparency = sustained license

Canton majority ownership: conservative SME & housing focus; ~40% debt

Public majority ownership by Canton of St. Gallen (pop ~511,000 in 2023) forces conservative strategy, SME and housing support (>99% of Swiss firms) and limits risk appetite. Stable federal politics and ~40% public debt (2024) enable long-term planning, while non-EU status and 2024 alignment with EU/US sanctions raise cross-border and compliance costs.

| Metric | Value |

|---|---|

| Canton pop (2023) | ~511,000 |

| Public debt (CH, 2024) | ~40% GDP |

| SME share | >99% |

| EU trade share | ~50% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect St. Galler Kantonalbank, with data-driven, region-specific insights and forward-looking scenarios to identify threats, opportunities and strategic responses for executives, investors and advisors.

Concise, visually segmented PESTLE summary for St. Galler Kantonalbank that’s easy to slot into presentations or strategy sessions, share across teams, and customize with notes to support quick alignment on external risks and market positioning.

Economic factors

SNB rate cycle and NIM

SNB policy—at 1.75% (July 2025)—materially drives St. Galler Kantonalbank NIM: rate hikes raise deposit beta risks but boost asset yields, while cuts can compress NIM by several dozen basis points; balance‑sheet repricing speed and a deposit mix skewed to sight deposits increase earnings sensitivity. Hedging and fee‑rich product mix are key levers to protect margins.

Regional SME dynamics

St. Gallen’s SME base, reflecting Switzerland’s SME sector which comprises over 99% of firms and employs about 67% of the workforce, anchors SGKB’s lending and fee income through broad business banking relationships. Cyclical slowdowns elevate credit risk particularly in manufacturing, construction and services where regional order books dipped in 2023–24. Industry concentration in textiles and machinery necessitates prudent underwriting and sector limits. Close relationship banking enables early risk identification and workout coordination.

Housing and mortgage market

High home prices and affordability rules—including a statutory minimum downpayment of 20%—constrain demand and keep average mortgage LTVs conservative while Switzerland's mortgage stock exceeds CHF 1.2 trillion. Real estate cycles drive volatile provisioning needs and can materially increase capital consumption during corrections. Rising demand for energy‑efficient renovations opens green‑lending niches, and conservative Swiss underwriting supports strong asset quality.

CHF strength and wealth flows

Strong CHF acts as a safe‑haven magnet—supporting inflows that bolstered Swiss banking deposits during 2024—while weighing on exporters among SKB clients and compressing margin opportunities; currency swings also change reported AUM and fee income when translated to CHF, with Swiss banks holding over CHF 10 trillion in client assets (2024).

- Safe‑haven inflows: positive for deposits

- Export pressure: margin and credit risk for corporates

- Translation risk: AUM and fee volatility

- Rising hedging demand: private and corporate clients

Inflation and cost discipline

Generally low Swiss inflation (CPI 2024: ~1.1%) has kept wage and vendor cost growth muted, but 2025 YTD inflation (~2.0%) and SNB policy rate 1.75% are squeezing budgets; efficiency programs and digitization are used to offset margin pressure. Pricing power remains limited versus larger banks and neobanks, so emphasis on advisory value underpins fee income.

- Swiss CPI 2024 ~1.1%

- 2025 YTD inflation ~2.0%

- SNB policy rate 1.75% (Jul 2025)

- Digitization and efficiencies reduce costs, preserve fees

Canton majority ownership: conservative SME & housing focus; ~40% debt

SNB rate 1.75% (Jul 2025) drives NIM volatility; deposit beta and sight‑deposit mix raise earnings sensitivity. Swiss CPI 2024 ~1.1% (2025 YTD ~2.0%) pressures costs; mortgage stock CHF 1.2tn and CHF 10tn client assets shape balance‑sheet risks and fee volatility.

| Metric | Value |

|---|---|

| SNB policy rate | 1.75% (Jul 2025) |

| CPI | 2024: ~1.1% · 2025 YTD: ~2.0% |

| Mortgage stock | CHF 1.2tn |

| Swiss client assets | CHF 10tn (2024) |

Preview the Actual Deliverable

St. Galler Kantonalbank PESTLE Analysis

The preview shown here is the exact St. Galler Kantonalbank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured and ready to use. The layout, content and conclusions match the downloadable file; no placeholders, no surprises.

Description

Your Competitive Advantage Starts with This Report

Our PESTLE analysis for St. Galler Kantonalbank reveals how political regulation, Swiss economic stability, shifting social trust, technological banking trends and environmental compliance shape its strategic risks and opportunities. Ideal for investors and strategists. Purchase the full, downloadable report for actionable insights.

Political factors

Cantonal ownership influence

Majority public ownership by the Canton of St. Gallen shapes SGKBs strategy, constraining risk appetite and emphasizing community obligations over aggressive expansion. Political stakeholders expect preferential local lending and stability, pressuring management to prioritize credit availability for regional SMEs and public projects. Governance must balance profitability with explicit public-interest mandates. Shifts in cantonal priorities can reallocate capital and strategic focus.

Swiss federal stability

Switzerland’s consensus-driven federal politics deliver predictable policy and budgets, enabling St. Galler Kantonalbank to plan long-term with confidence; public debt remains modest at roughly 40% of GDP (2024), supporting fiscal headroom. Low geopolitical risk and a strong sovereign profile keep funding costs competitive and client trust high. Policy shifts are gradual, allowing the bank proactive adaptation and reliable countercyclical support if needed.

EU relations and market access

Switzerland's non-EU status prevents passporting, constraining seamless cross-border banking despite the EU accounting for roughly 50% of Swiss trade. Ongoing bilateral framework tensions make equivalence decisions uncertain, directly affecting wealth management and corporate client access. SGKB must therefore implement country-by-country onboarding and tailor product permissions, with political outcomes materially influencing future cross-border growth.

Sanctions and foreign policy alignment

Switzerland continued aligning with major EU and US sanctions regimes in 2024, expanding SECO-maintained consolidated lists and heightening screening and reporting obligations for banks; St. Galler Kantonalbank faces increased compliance complexity and operational overhead as political shifts can abruptly affect specific client segments.

- Compliance scope: alignment with EU/US sanctions (2024)

- Operational impact: higher screening/reporting workload

- Risk: sudden client segmentation changes from political moves

- Mitigation: robust policies to avoid enforcement and reputational harm

Local public policy expectations

St. Galler Kantonalbank faces cantonal expectations to support SMEs, housing and regional development in a canton of about 511,000 residents (2023); Swiss SMEs constitute over 99% of companies, underscoring political pressure to prioritize local lending. Political scrutiny rises in downturns or restructurings, and stakeholder pushback can constrain branch closures or price changes. Transparent, frequent communication preserves its license to operate.

- SME support: over 99% of Swiss firms

- Canton pop: ~511,000 (2023)

- High scrutiny in downturns

- Transparency = sustained license

Canton majority ownership: conservative SME & housing focus; ~40% debt

Public majority ownership by Canton of St. Gallen (pop ~511,000 in 2023) forces conservative strategy, SME and housing support (>99% of Swiss firms) and limits risk appetite. Stable federal politics and ~40% public debt (2024) enable long-term planning, while non-EU status and 2024 alignment with EU/US sanctions raise cross-border and compliance costs.

| Metric | Value |

|---|---|

| Canton pop (2023) | ~511,000 |

| Public debt (CH, 2024) | ~40% GDP |

| SME share | >99% |

| EU trade share | ~50% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect St. Galler Kantonalbank, with data-driven, region-specific insights and forward-looking scenarios to identify threats, opportunities and strategic responses for executives, investors and advisors.

Concise, visually segmented PESTLE summary for St. Galler Kantonalbank that’s easy to slot into presentations or strategy sessions, share across teams, and customize with notes to support quick alignment on external risks and market positioning.

Economic factors

SNB rate cycle and NIM

SNB policy—at 1.75% (July 2025)—materially drives St. Galler Kantonalbank NIM: rate hikes raise deposit beta risks but boost asset yields, while cuts can compress NIM by several dozen basis points; balance‑sheet repricing speed and a deposit mix skewed to sight deposits increase earnings sensitivity. Hedging and fee‑rich product mix are key levers to protect margins.

Regional SME dynamics

St. Gallen’s SME base, reflecting Switzerland’s SME sector which comprises over 99% of firms and employs about 67% of the workforce, anchors SGKB’s lending and fee income through broad business banking relationships. Cyclical slowdowns elevate credit risk particularly in manufacturing, construction and services where regional order books dipped in 2023–24. Industry concentration in textiles and machinery necessitates prudent underwriting and sector limits. Close relationship banking enables early risk identification and workout coordination.

Housing and mortgage market

High home prices and affordability rules—including a statutory minimum downpayment of 20%—constrain demand and keep average mortgage LTVs conservative while Switzerland's mortgage stock exceeds CHF 1.2 trillion. Real estate cycles drive volatile provisioning needs and can materially increase capital consumption during corrections. Rising demand for energy‑efficient renovations opens green‑lending niches, and conservative Swiss underwriting supports strong asset quality.

CHF strength and wealth flows

Strong CHF acts as a safe‑haven magnet—supporting inflows that bolstered Swiss banking deposits during 2024—while weighing on exporters among SKB clients and compressing margin opportunities; currency swings also change reported AUM and fee income when translated to CHF, with Swiss banks holding over CHF 10 trillion in client assets (2024).

- Safe‑haven inflows: positive for deposits

- Export pressure: margin and credit risk for corporates

- Translation risk: AUM and fee volatility

- Rising hedging demand: private and corporate clients

Inflation and cost discipline

Generally low Swiss inflation (CPI 2024: ~1.1%) has kept wage and vendor cost growth muted, but 2025 YTD inflation (~2.0%) and SNB policy rate 1.75% are squeezing budgets; efficiency programs and digitization are used to offset margin pressure. Pricing power remains limited versus larger banks and neobanks, so emphasis on advisory value underpins fee income.

- Swiss CPI 2024 ~1.1%

- 2025 YTD inflation ~2.0%

- SNB policy rate 1.75% (Jul 2025)

- Digitization and efficiencies reduce costs, preserve fees

Canton majority ownership: conservative SME & housing focus; ~40% debt

SNB rate 1.75% (Jul 2025) drives NIM volatility; deposit beta and sight‑deposit mix raise earnings sensitivity. Swiss CPI 2024 ~1.1% (2025 YTD ~2.0%) pressures costs; mortgage stock CHF 1.2tn and CHF 10tn client assets shape balance‑sheet risks and fee volatility.

| Metric | Value |

|---|---|

| SNB policy rate | 1.75% (Jul 2025) |

| CPI | 2024: ~1.1% · 2025 YTD: ~2.0% |

| Mortgage stock | CHF 1.2tn |

| Swiss client assets | CHF 10tn (2024) |

Preview the Actual Deliverable

St. Galler Kantonalbank PESTLE Analysis

The preview shown here is the exact St. Galler Kantonalbank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured and ready to use. The layout, content and conclusions match the downloadable file; no placeholders, no surprises.