Shanghai Shenda SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Shanghai Shenda stands at the crossroads of strong domestic brand recognition and growing export opportunities, yet faces margin pressure from rising input costs and intense competition; our SWOT highlights actionable moves to protect margins and expand channels. Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain a professionally written, editable report for strategy, pitches, and investment decisions.

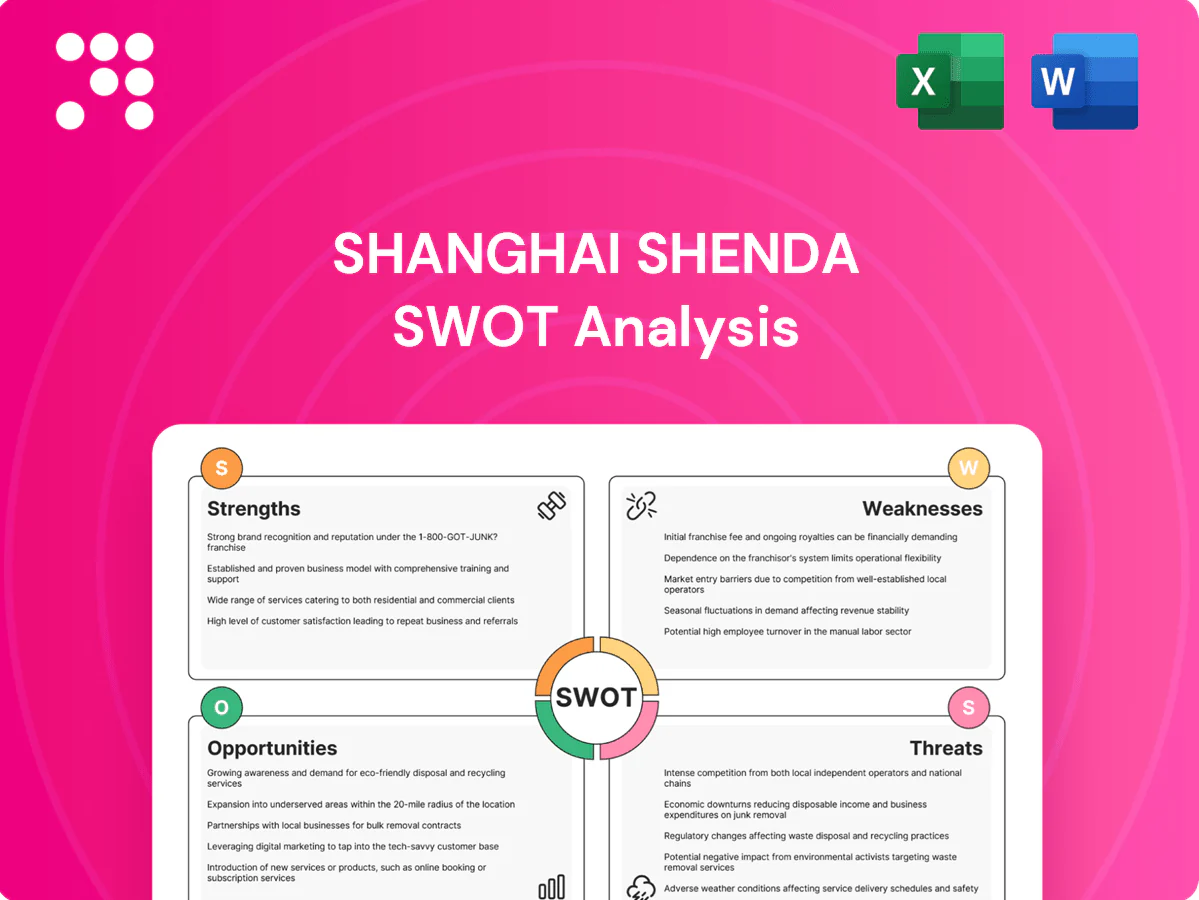

Strengths

Integrated trade-and-manufacturing model

Combining import/export trading with in-house production lets Shanghai Shenda tighten cost control and shorten lead times, with vertically integrated apparel firms often cutting turnaround by up to 30% and improving gross margins by several percentage points. Vertical integration enhances quality assurance and product customization for clients, reducing dependency on third-party suppliers. The model also boosts responsiveness to rapid demand shifts in China’s textile market.

Global sourcing and sales footprint

Operating across domestic and international markets diversifies Shanghai Shenda’s revenue and supply risks by spreading exposure across multiple geographies, reducing dependence on any single market. Access to varied markets supports scale economies and stronger procurement leverage through larger aggregated volumes and supplier competition. A broad sourcing and sales network enhances resilience against localized downturns and enables faster market entry when high-growth regions emerge.

Established textile and garment expertise

Established textile and garment expertise improves fabric selection, process efficiency, and compliance with buyer standards, reducing rejects and supporting consistent audit performance. Experience lowers defect rates and enhances on-time delivery for complex production schedules. The capability to handle complex orders and smaller batch flexibility creates a practical barrier to entry for less seasoned rivals.

Diversified product portfolio

Shanghai Shenda’s diversified product portfolio spanning textiles, garments and related goods spreads demand risk across categories, reducing reliance on any single segment and smoothing revenue volatility. Cross-selling between apparel and home textiles can raise average order value and deepen customer relationships. Diversification also stabilizes factory utilization and helps match capacity to seasonal and segment-specific demand patterns.

- Spreads demand risk

- Boosts average order value via cross-sell

- Stabilizes manufacturing utilization

- Addresses varied segments and seasonality

Brand expansion focus

- Higher-margin branded mix

- Improved pricing power

- Entry to premium channels

- Reduced price competition

Integrated manufacturing and multi-market brands shorten lead times, reduce costs, boost margins

Vertical integration shortens lead times and tightens cost control, multi-market presence diversifies revenue and sourcing risk, deep textile expertise ensures quality and complex-order capability, and a diversified branded portfolio raises margins and pricing power.

| Metric | Value |

|---|---|

| Vertical integration | Yes |

| International revenue share | N/A |

| Branded mix | N/A |

What is included in the product

Provides a concise SWOT overview of Shanghai Shenda, identifying internal strengths and weaknesses and external opportunities and threats that shape its competitive position and strategic prospects.

Provides a concise Shanghai Shenda SWOT matrix for fast, visual strategy alignment, surfacing core pain points and targeted remedies for quick executive action.

Weaknesses

Thin margins in commoditized textiles

Core categories often face price-driven competition and limited differentiation, forcing Shanghai Shenda into thin-margin commodity segments that limit scope for premium pricing.

Exposure to trade policy and tariffs

An import–export model leaves Shanghai Shenda exposed to quota changes, tariffs and sanctions that in past US–China tensions imposed duties up to 25%, raising landed costs and disrupting routes. Sudden policy shifts can force rerouting and inventory build-up, as China recorded roughly $3.6 trillion in goods exports in 2023, amplifying scale risk. Growing customs and rules-of-origin complexity increases administrative burden and may push customers to re-source to avoid tariff impacts.

Capex and utilization risk in manufacturing

High fixed-asset base at Shanghai Shenda demands sustained high utilization to protect margins; textile-plant utilization in China averaged about 78% in 2024, so dips quickly erode ROIC. Demand volatility can create idle capacity and overhead-absorption strain, while periodic capex for new-fabric equipment (scheduled across 2024–25) raises cash needs. Misalignment between trading demand and plant capacity reduces throughput and raises unit costs.

Brand recognition still developing

Transitioning from OEM/trading to brand-led sales typically takes 3–5 years and requires sustained capex and marketing; industry experience by 2024 shows marketing spends often reach around 8% of revenue during brand launches. Limited brand equity can cap pricing power, with initial retail premiums frequently under 5%, and marketing spend may outpace near-term revenue gains. Retail channel access can remain constrained without strong brand pull.

- Transition timeline: 3–5 years

- Marketing spend: ≈8% of revenue (2024 benchmark)

- Initial pricing premium: <5%

- Retail traction: limited without brand pull

Working-capital intensity

Shanghai Shenda's working-capital intensity ties up cash through extended inventory, receivables, and logistics cycles, while longer export payment terms frequently strain near-term liquidity; FX settlement timing adds volatility to cash planning, and scaling volumes likely requires more factoring or expanded credit lines.

- Inventory and receivables lock cash

- Export terms increase liquidity pressure

- FX settlement timing complicates planning

- Growth may force factoring or bigger credit lines

Tariffs, low margins and capex strain force 3–5 year brand pivots in textiles

Price-driven, low differentiation forces thin margins and exposure to tariff risk (US duties up to 25%; China goods exports $3.6T in 2023). High fixed assets need ~78% utilization (textile 2024 avg) and capex 2024–25 strains cash. Brand shift requires ~3–5 years and ~8% revenue marketing spend; working-capital intensity and FX timing squeeze liquidity.

| Risk | Metric |

|---|---|

| Tariff exposure | Up to 25% duties; $3.6T exports (2023) |

| Utilization | ~78% avg (2024) |

| Brand transition | 3–5 yrs; ~8% rev marketing |

Full Version Awaits

Shanghai Shenda SWOT Analysis

This is the actual Shanghai Shenda SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the entire in-depth, editable version. You’re viewing a live excerpt of the real file, ready for download after checkout.

Go Beyond the Preview—Access the Full Strategic Report

Shanghai Shenda stands at the crossroads of strong domestic brand recognition and growing export opportunities, yet faces margin pressure from rising input costs and intense competition; our SWOT highlights actionable moves to protect margins and expand channels. Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain a professionally written, editable report for strategy, pitches, and investment decisions.

Strengths

Integrated trade-and-manufacturing model

Combining import/export trading with in-house production lets Shanghai Shenda tighten cost control and shorten lead times, with vertically integrated apparel firms often cutting turnaround by up to 30% and improving gross margins by several percentage points. Vertical integration enhances quality assurance and product customization for clients, reducing dependency on third-party suppliers. The model also boosts responsiveness to rapid demand shifts in China’s textile market.

Global sourcing and sales footprint

Operating across domestic and international markets diversifies Shanghai Shenda’s revenue and supply risks by spreading exposure across multiple geographies, reducing dependence on any single market. Access to varied markets supports scale economies and stronger procurement leverage through larger aggregated volumes and supplier competition. A broad sourcing and sales network enhances resilience against localized downturns and enables faster market entry when high-growth regions emerge.

Established textile and garment expertise

Established textile and garment expertise improves fabric selection, process efficiency, and compliance with buyer standards, reducing rejects and supporting consistent audit performance. Experience lowers defect rates and enhances on-time delivery for complex production schedules. The capability to handle complex orders and smaller batch flexibility creates a practical barrier to entry for less seasoned rivals.

Diversified product portfolio

Shanghai Shenda’s diversified product portfolio spanning textiles, garments and related goods spreads demand risk across categories, reducing reliance on any single segment and smoothing revenue volatility. Cross-selling between apparel and home textiles can raise average order value and deepen customer relationships. Diversification also stabilizes factory utilization and helps match capacity to seasonal and segment-specific demand patterns.

- Spreads demand risk

- Boosts average order value via cross-sell

- Stabilizes manufacturing utilization

- Addresses varied segments and seasonality

Brand expansion focus

- Higher-margin branded mix

- Improved pricing power

- Entry to premium channels

- Reduced price competition

Integrated manufacturing and multi-market brands shorten lead times, reduce costs, boost margins

Vertical integration shortens lead times and tightens cost control, multi-market presence diversifies revenue and sourcing risk, deep textile expertise ensures quality and complex-order capability, and a diversified branded portfolio raises margins and pricing power.

| Metric | Value |

|---|---|

| Vertical integration | Yes |

| International revenue share | N/A |

| Branded mix | N/A |

What is included in the product

Provides a concise SWOT overview of Shanghai Shenda, identifying internal strengths and weaknesses and external opportunities and threats that shape its competitive position and strategic prospects.

Provides a concise Shanghai Shenda SWOT matrix for fast, visual strategy alignment, surfacing core pain points and targeted remedies for quick executive action.

Weaknesses

Thin margins in commoditized textiles

Core categories often face price-driven competition and limited differentiation, forcing Shanghai Shenda into thin-margin commodity segments that limit scope for premium pricing.

Exposure to trade policy and tariffs

An import–export model leaves Shanghai Shenda exposed to quota changes, tariffs and sanctions that in past US–China tensions imposed duties up to 25%, raising landed costs and disrupting routes. Sudden policy shifts can force rerouting and inventory build-up, as China recorded roughly $3.6 trillion in goods exports in 2023, amplifying scale risk. Growing customs and rules-of-origin complexity increases administrative burden and may push customers to re-source to avoid tariff impacts.

Capex and utilization risk in manufacturing

High fixed-asset base at Shanghai Shenda demands sustained high utilization to protect margins; textile-plant utilization in China averaged about 78% in 2024, so dips quickly erode ROIC. Demand volatility can create idle capacity and overhead-absorption strain, while periodic capex for new-fabric equipment (scheduled across 2024–25) raises cash needs. Misalignment between trading demand and plant capacity reduces throughput and raises unit costs.

Brand recognition still developing

Transitioning from OEM/trading to brand-led sales typically takes 3–5 years and requires sustained capex and marketing; industry experience by 2024 shows marketing spends often reach around 8% of revenue during brand launches. Limited brand equity can cap pricing power, with initial retail premiums frequently under 5%, and marketing spend may outpace near-term revenue gains. Retail channel access can remain constrained without strong brand pull.

- Transition timeline: 3–5 years

- Marketing spend: ≈8% of revenue (2024 benchmark)

- Initial pricing premium: <5%

- Retail traction: limited without brand pull

Working-capital intensity

Shanghai Shenda's working-capital intensity ties up cash through extended inventory, receivables, and logistics cycles, while longer export payment terms frequently strain near-term liquidity; FX settlement timing adds volatility to cash planning, and scaling volumes likely requires more factoring or expanded credit lines.

- Inventory and receivables lock cash

- Export terms increase liquidity pressure

- FX settlement timing complicates planning

- Growth may force factoring or bigger credit lines

Tariffs, low margins and capex strain force 3–5 year brand pivots in textiles

Price-driven, low differentiation forces thin margins and exposure to tariff risk (US duties up to 25%; China goods exports $3.6T in 2023). High fixed assets need ~78% utilization (textile 2024 avg) and capex 2024–25 strains cash. Brand shift requires ~3–5 years and ~8% revenue marketing spend; working-capital intensity and FX timing squeeze liquidity.

| Risk | Metric |

|---|---|

| Tariff exposure | Up to 25% duties; $3.6T exports (2023) |

| Utilization | ~78% avg (2024) |

| Brand transition | 3–5 yrs; ~8% rev marketing |

Full Version Awaits

Shanghai Shenda SWOT Analysis

This is the actual Shanghai Shenda SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the entire in-depth, editable version. You’re viewing a live excerpt of the real file, ready for download after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Shanghai Shenda stands at the crossroads of strong domestic brand recognition and growing export opportunities, yet faces margin pressure from rising input costs and intense competition; our SWOT highlights actionable moves to protect margins and expand channels. Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain a professionally written, editable report for strategy, pitches, and investment decisions.

Strengths

Integrated trade-and-manufacturing model

Combining import/export trading with in-house production lets Shanghai Shenda tighten cost control and shorten lead times, with vertically integrated apparel firms often cutting turnaround by up to 30% and improving gross margins by several percentage points. Vertical integration enhances quality assurance and product customization for clients, reducing dependency on third-party suppliers. The model also boosts responsiveness to rapid demand shifts in China’s textile market.

Global sourcing and sales footprint

Operating across domestic and international markets diversifies Shanghai Shenda’s revenue and supply risks by spreading exposure across multiple geographies, reducing dependence on any single market. Access to varied markets supports scale economies and stronger procurement leverage through larger aggregated volumes and supplier competition. A broad sourcing and sales network enhances resilience against localized downturns and enables faster market entry when high-growth regions emerge.

Established textile and garment expertise

Established textile and garment expertise improves fabric selection, process efficiency, and compliance with buyer standards, reducing rejects and supporting consistent audit performance. Experience lowers defect rates and enhances on-time delivery for complex production schedules. The capability to handle complex orders and smaller batch flexibility creates a practical barrier to entry for less seasoned rivals.

Diversified product portfolio

Shanghai Shenda’s diversified product portfolio spanning textiles, garments and related goods spreads demand risk across categories, reducing reliance on any single segment and smoothing revenue volatility. Cross-selling between apparel and home textiles can raise average order value and deepen customer relationships. Diversification also stabilizes factory utilization and helps match capacity to seasonal and segment-specific demand patterns.

- Spreads demand risk

- Boosts average order value via cross-sell

- Stabilizes manufacturing utilization

- Addresses varied segments and seasonality

Brand expansion focus

- Higher-margin branded mix

- Improved pricing power

- Entry to premium channels

- Reduced price competition

Integrated manufacturing and multi-market brands shorten lead times, reduce costs, boost margins

Vertical integration shortens lead times and tightens cost control, multi-market presence diversifies revenue and sourcing risk, deep textile expertise ensures quality and complex-order capability, and a diversified branded portfolio raises margins and pricing power.

| Metric | Value |

|---|---|

| Vertical integration | Yes |

| International revenue share | N/A |

| Branded mix | N/A |

What is included in the product

Provides a concise SWOT overview of Shanghai Shenda, identifying internal strengths and weaknesses and external opportunities and threats that shape its competitive position and strategic prospects.

Provides a concise Shanghai Shenda SWOT matrix for fast, visual strategy alignment, surfacing core pain points and targeted remedies for quick executive action.

Weaknesses

Thin margins in commoditized textiles

Core categories often face price-driven competition and limited differentiation, forcing Shanghai Shenda into thin-margin commodity segments that limit scope for premium pricing.

Exposure to trade policy and tariffs

An import–export model leaves Shanghai Shenda exposed to quota changes, tariffs and sanctions that in past US–China tensions imposed duties up to 25%, raising landed costs and disrupting routes. Sudden policy shifts can force rerouting and inventory build-up, as China recorded roughly $3.6 trillion in goods exports in 2023, amplifying scale risk. Growing customs and rules-of-origin complexity increases administrative burden and may push customers to re-source to avoid tariff impacts.

Capex and utilization risk in manufacturing

High fixed-asset base at Shanghai Shenda demands sustained high utilization to protect margins; textile-plant utilization in China averaged about 78% in 2024, so dips quickly erode ROIC. Demand volatility can create idle capacity and overhead-absorption strain, while periodic capex for new-fabric equipment (scheduled across 2024–25) raises cash needs. Misalignment between trading demand and plant capacity reduces throughput and raises unit costs.

Brand recognition still developing

Transitioning from OEM/trading to brand-led sales typically takes 3–5 years and requires sustained capex and marketing; industry experience by 2024 shows marketing spends often reach around 8% of revenue during brand launches. Limited brand equity can cap pricing power, with initial retail premiums frequently under 5%, and marketing spend may outpace near-term revenue gains. Retail channel access can remain constrained without strong brand pull.

- Transition timeline: 3–5 years

- Marketing spend: ≈8% of revenue (2024 benchmark)

- Initial pricing premium: <5%

- Retail traction: limited without brand pull

Working-capital intensity

Shanghai Shenda's working-capital intensity ties up cash through extended inventory, receivables, and logistics cycles, while longer export payment terms frequently strain near-term liquidity; FX settlement timing adds volatility to cash planning, and scaling volumes likely requires more factoring or expanded credit lines.

- Inventory and receivables lock cash

- Export terms increase liquidity pressure

- FX settlement timing complicates planning

- Growth may force factoring or bigger credit lines

Tariffs, low margins and capex strain force 3–5 year brand pivots in textiles

Price-driven, low differentiation forces thin margins and exposure to tariff risk (US duties up to 25%; China goods exports $3.6T in 2023). High fixed assets need ~78% utilization (textile 2024 avg) and capex 2024–25 strains cash. Brand shift requires ~3–5 years and ~8% revenue marketing spend; working-capital intensity and FX timing squeeze liquidity.

| Risk | Metric |

|---|---|

| Tariff exposure | Up to 25% duties; $3.6T exports (2023) |

| Utilization | ~78% avg (2024) |

| Brand transition | 3–5 yrs; ~8% rev marketing |

Full Version Awaits

Shanghai Shenda SWOT Analysis

This is the actual Shanghai Shenda SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the entire in-depth, editable version. You’re viewing a live excerpt of the real file, ready for download after checkout.