Shanghai Electric Group Co. Porter's Five Forces Analysis

Don't Miss the Bigger Picture

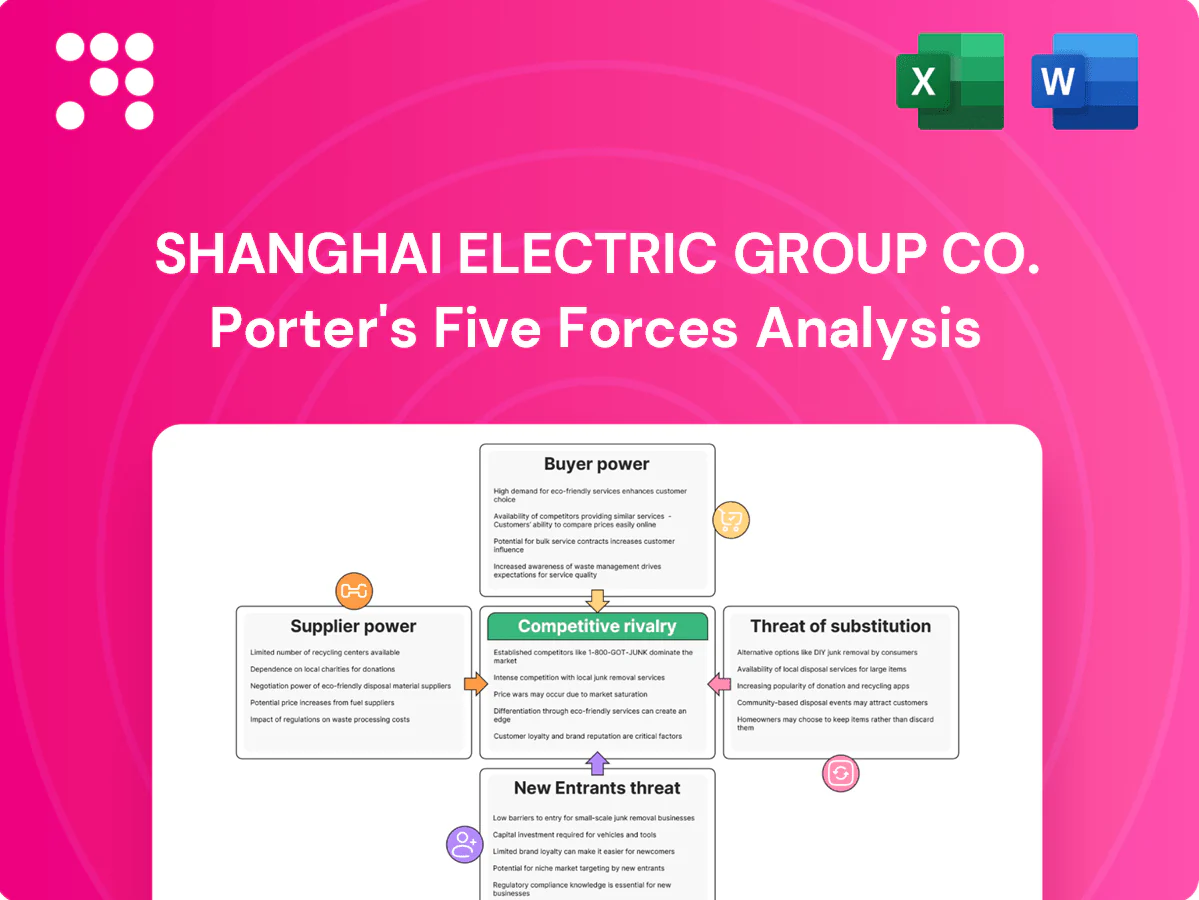

Shanghai Electric faces intense industry rivalry driven by large state-backed competitors and cyclical demand; supplier power is moderate due to specialized components but mitigated by long-term contracts; capital and tech intensity create high barriers to entry while renewable alternatives raise substitution risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Shanghai Electric Group Co.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical materials

Shanghai Electric depends on concentrated inputs—steel, copper, power electronics, large bearings and rare-earths—where upstream supply can be highly concentrated; China supplies about 60% of global rare-earths (2023–24), making export curbs a real risk. Shortages or controls can spike input costs and lead times, giving key suppliers pricing and allocation leverage. Dual-sourcing and larger inventory buffers partially mitigate exposure.

Specialized components and IP

Turbomachinery parts, control systems and high-voltage components for Shanghai Electric rely on certified, IP-heavy suppliers, with qualification cycles commonly taking 12–24 months and raising switching costs. Vendors owning proprietary technology command stronger commercial terms and can sustain price premiums. Co-development agreements help rebalance leverage by securing custom supply but create technical and contractual lock-in.

Commodity price volatility

Global swings in metals and energy raised BOM costs for Shanghai Electric, with major metal price volatility exceeding 20% in 2024, prompting suppliers to push surcharges in spot markets. Long-term contracts and hedging reduced exposure but left residual basis risk. Fixed-price project bids were squeezed when input costs jumped mid-contract, compressing EPC margins.

Localization and policy effects

Scale and integration counterweight

Shanghai Electric’s massive purchasing scale and deep engineering capabilities strengthen its negotiating leverage with suppliers, enabling volume discounts and tighter technical specifications. Vendor development programs, framework agreements and partial in-house fabrication reduce supplier dependence while long-term volume visibility secures concessions and favorable payment terms. Active qualification of alternate vendors sustains competitive pressure on incumbents.

- Scale + engineering = stronger leverage

- Frameworks + in-house work lower dependence

- Long-term volumes yield concessions

- Alternate qualification maintains pressure

Supplier concentration + >20% metal swings raise BOM risk; rare-earths~60%

Suppliers hold moderate-to-high leverage for Shanghai Electric due to concentrated inputs (steel, rare-earths) and certified, IP-heavy components; China supplied ~60% of global rare-earths (2023–24). 2024 metal price swings exceeded 20%, raising BOM risk while qualification cycles of key vendors run 12–24 months. Shanghai Electric’s scale, framework agreements and partial in-house fabrication partially offset supplier power.

| Metric | 2024 |

|---|---|

| China rare-earth share | ~60% |

| Metal price volatility | >20% |

| Vendor qualification | 12–24 months |

What is included in the product

Tailored exclusively for Shanghai Electric Group Co., this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive forces and market dynamics shaping pricing and profitability.

A concise one-sheet Porter’s Five Forces for Shanghai Electric Group Co.—visual spider/radar chart and customizable pressure levels to pinpoint regulatory, supplier, and competitor risks, ready to drop into pitch decks or Excel dashboards for fast, boardroom-ready decision-making.

Customers Bargaining Power

Large, sophisticated buyers

Utilities, IPPs and industrial SOEs run competitive tenders with strict specs—China’s power system exceeds 2,400 GW of installed capacity and state players control over 70% of large procurements, driving scale-based leverage. Buyers’ procurement expertise forces aggressive pricing and firm performance bonds, with framework contracts and penalty clauses often reaching 5–10% of contract value. Benchmarking across multiple global OEMs is routine, compressing margins for suppliers like Shanghai Electric.

High stakes, long life-cycle deals

As of 2024, Shanghai Electric faces high bargaining power from customers because capital intensity and 20–30 year asset lives create large switching costs after installation. Pre-award buyers use competitive tendering to push for extended warranties and vendor financing. Post-award dependence on service and spare parts moderates buyer leverage, while bundled O&M lowers price sensitivity but increases scrutiny on performance and SLA compliance.

Standardization increases comparability

IEC and GB standardization plus modular designs make bids highly comparable, shifting procurement toward price competition and strengthening buyer bargaining power. Tenders increasingly prioritize lifecycle cost, forcing suppliers to differentiate via measurable efficiency, proven reliability, and integrated digital services. Any temporary spec edge is rapidly eroded as rivals adopt the same standards and modules.

Financing and EPC packaging

Buyers increasingly demand turnkey EPC plus vendor financing to de-risk projects, using the ability to mobilize capital as a key bargaining lever; vendors that bundle financing and EPC often win contracts despite price premiums because tied credit limits buyers' future options and increases switching costs.

- Buyers: seek turnkey EPC + vendor finance

- Leverage: financing mobilization as bargaining power

- Vendors: integrated packages win despite price gaps

- Risk: tied credit reduces later buyer options

Aftermarket leverage varies

In-warranty phases give buyers strong leverage through KPIs and acceptance tests, constraining Shanghai Electric Group Co. on delivery terms and penalties; mid-life overhauls see OEM parts and proprietary software limit alternatives, raising lifecycle costs. Third-party service providers restored buyer leverage for mature fleets, capturing roughly 25% of global turbine servicing by 2024, while performance-based contracts increasingly rebalance incentives.

- Buyers: KPI/acceptance tests

- Mid-life: OEM parts/software lock-in

- Third-party: ~25% market share (2024)

- Contracts: performance-based rebalance

Buyers wield leverage: China >2,400 GW, state >70%, penalties 5–10%

Buyers exert high bargaining power via strict competitive tenders, with China’s power fleet >2,400 GW and state players capturing >70% of large procurements (2024). Contract penalties and bonds commonly reach 5–10% of value, compressing supplier margins. Post-award OEM lock-in raises lifecycle costs, though third-party servicing reached ~25% of turbine servicing globally in 2024, softening buyer leverage.

| Metric | Value (2024) |

|---|---|

| China installed capacity | >2,400 GW |

| State procurement share | >70% |

| Penalty clauses | 5–10% contract value |

| Third-party service share | ~25% global |

Preview the Actual Deliverable

Shanghai Electric Group Co. Porter's Five Forces Analysis

This Porter's Five Forces analysis of Shanghai Electric Group Co. assesses industry rivalry, supplier and buyer power, threat of new entrants, and substitutes, and the document you see here is the exact, fully formatted file you’ll receive instantly after purchase—no samples, no placeholders.

Don't Miss the Bigger Picture

Shanghai Electric faces intense industry rivalry driven by large state-backed competitors and cyclical demand; supplier power is moderate due to specialized components but mitigated by long-term contracts; capital and tech intensity create high barriers to entry while renewable alternatives raise substitution risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Shanghai Electric Group Co.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical materials

Shanghai Electric depends on concentrated inputs—steel, copper, power electronics, large bearings and rare-earths—where upstream supply can be highly concentrated; China supplies about 60% of global rare-earths (2023–24), making export curbs a real risk. Shortages or controls can spike input costs and lead times, giving key suppliers pricing and allocation leverage. Dual-sourcing and larger inventory buffers partially mitigate exposure.

Specialized components and IP

Turbomachinery parts, control systems and high-voltage components for Shanghai Electric rely on certified, IP-heavy suppliers, with qualification cycles commonly taking 12–24 months and raising switching costs. Vendors owning proprietary technology command stronger commercial terms and can sustain price premiums. Co-development agreements help rebalance leverage by securing custom supply but create technical and contractual lock-in.

Commodity price volatility

Global swings in metals and energy raised BOM costs for Shanghai Electric, with major metal price volatility exceeding 20% in 2024, prompting suppliers to push surcharges in spot markets. Long-term contracts and hedging reduced exposure but left residual basis risk. Fixed-price project bids were squeezed when input costs jumped mid-contract, compressing EPC margins.

Localization and policy effects

Scale and integration counterweight

Shanghai Electric’s massive purchasing scale and deep engineering capabilities strengthen its negotiating leverage with suppliers, enabling volume discounts and tighter technical specifications. Vendor development programs, framework agreements and partial in-house fabrication reduce supplier dependence while long-term volume visibility secures concessions and favorable payment terms. Active qualification of alternate vendors sustains competitive pressure on incumbents.

- Scale + engineering = stronger leverage

- Frameworks + in-house work lower dependence

- Long-term volumes yield concessions

- Alternate qualification maintains pressure

Supplier concentration + >20% metal swings raise BOM risk; rare-earths~60%

Suppliers hold moderate-to-high leverage for Shanghai Electric due to concentrated inputs (steel, rare-earths) and certified, IP-heavy components; China supplied ~60% of global rare-earths (2023–24). 2024 metal price swings exceeded 20%, raising BOM risk while qualification cycles of key vendors run 12–24 months. Shanghai Electric’s scale, framework agreements and partial in-house fabrication partially offset supplier power.

| Metric | 2024 |

|---|---|

| China rare-earth share | ~60% |

| Metal price volatility | >20% |

| Vendor qualification | 12–24 months |

What is included in the product

Tailored exclusively for Shanghai Electric Group Co., this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive forces and market dynamics shaping pricing and profitability.

A concise one-sheet Porter’s Five Forces for Shanghai Electric Group Co.—visual spider/radar chart and customizable pressure levels to pinpoint regulatory, supplier, and competitor risks, ready to drop into pitch decks or Excel dashboards for fast, boardroom-ready decision-making.

Customers Bargaining Power

Large, sophisticated buyers

Utilities, IPPs and industrial SOEs run competitive tenders with strict specs—China’s power system exceeds 2,400 GW of installed capacity and state players control over 70% of large procurements, driving scale-based leverage. Buyers’ procurement expertise forces aggressive pricing and firm performance bonds, with framework contracts and penalty clauses often reaching 5–10% of contract value. Benchmarking across multiple global OEMs is routine, compressing margins for suppliers like Shanghai Electric.

High stakes, long life-cycle deals

As of 2024, Shanghai Electric faces high bargaining power from customers because capital intensity and 20–30 year asset lives create large switching costs after installation. Pre-award buyers use competitive tendering to push for extended warranties and vendor financing. Post-award dependence on service and spare parts moderates buyer leverage, while bundled O&M lowers price sensitivity but increases scrutiny on performance and SLA compliance.

Standardization increases comparability

IEC and GB standardization plus modular designs make bids highly comparable, shifting procurement toward price competition and strengthening buyer bargaining power. Tenders increasingly prioritize lifecycle cost, forcing suppliers to differentiate via measurable efficiency, proven reliability, and integrated digital services. Any temporary spec edge is rapidly eroded as rivals adopt the same standards and modules.

Financing and EPC packaging

Buyers increasingly demand turnkey EPC plus vendor financing to de-risk projects, using the ability to mobilize capital as a key bargaining lever; vendors that bundle financing and EPC often win contracts despite price premiums because tied credit limits buyers' future options and increases switching costs.

- Buyers: seek turnkey EPC + vendor finance

- Leverage: financing mobilization as bargaining power

- Vendors: integrated packages win despite price gaps

- Risk: tied credit reduces later buyer options

Aftermarket leverage varies

In-warranty phases give buyers strong leverage through KPIs and acceptance tests, constraining Shanghai Electric Group Co. on delivery terms and penalties; mid-life overhauls see OEM parts and proprietary software limit alternatives, raising lifecycle costs. Third-party service providers restored buyer leverage for mature fleets, capturing roughly 25% of global turbine servicing by 2024, while performance-based contracts increasingly rebalance incentives.

- Buyers: KPI/acceptance tests

- Mid-life: OEM parts/software lock-in

- Third-party: ~25% market share (2024)

- Contracts: performance-based rebalance

Buyers wield leverage: China >2,400 GW, state >70%, penalties 5–10%

Buyers exert high bargaining power via strict competitive tenders, with China’s power fleet >2,400 GW and state players capturing >70% of large procurements (2024). Contract penalties and bonds commonly reach 5–10% of value, compressing supplier margins. Post-award OEM lock-in raises lifecycle costs, though third-party servicing reached ~25% of turbine servicing globally in 2024, softening buyer leverage.

| Metric | Value (2024) |

|---|---|

| China installed capacity | >2,400 GW |

| State procurement share | >70% |

| Penalty clauses | 5–10% contract value |

| Third-party service share | ~25% global |

Preview the Actual Deliverable

Shanghai Electric Group Co. Porter's Five Forces Analysis

This Porter's Five Forces analysis of Shanghai Electric Group Co. assesses industry rivalry, supplier and buyer power, threat of new entrants, and substitutes, and the document you see here is the exact, fully formatted file you’ll receive instantly after purchase—no samples, no placeholders.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Shanghai Electric faces intense industry rivalry driven by large state-backed competitors and cyclical demand; supplier power is moderate due to specialized components but mitigated by long-term contracts; capital and tech intensity create high barriers to entry while renewable alternatives raise substitution risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Shanghai Electric Group Co.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical materials

Shanghai Electric depends on concentrated inputs—steel, copper, power electronics, large bearings and rare-earths—where upstream supply can be highly concentrated; China supplies about 60% of global rare-earths (2023–24), making export curbs a real risk. Shortages or controls can spike input costs and lead times, giving key suppliers pricing and allocation leverage. Dual-sourcing and larger inventory buffers partially mitigate exposure.

Specialized components and IP

Turbomachinery parts, control systems and high-voltage components for Shanghai Electric rely on certified, IP-heavy suppliers, with qualification cycles commonly taking 12–24 months and raising switching costs. Vendors owning proprietary technology command stronger commercial terms and can sustain price premiums. Co-development agreements help rebalance leverage by securing custom supply but create technical and contractual lock-in.

Commodity price volatility

Global swings in metals and energy raised BOM costs for Shanghai Electric, with major metal price volatility exceeding 20% in 2024, prompting suppliers to push surcharges in spot markets. Long-term contracts and hedging reduced exposure but left residual basis risk. Fixed-price project bids were squeezed when input costs jumped mid-contract, compressing EPC margins.

Localization and policy effects

Scale and integration counterweight

Shanghai Electric’s massive purchasing scale and deep engineering capabilities strengthen its negotiating leverage with suppliers, enabling volume discounts and tighter technical specifications. Vendor development programs, framework agreements and partial in-house fabrication reduce supplier dependence while long-term volume visibility secures concessions and favorable payment terms. Active qualification of alternate vendors sustains competitive pressure on incumbents.

- Scale + engineering = stronger leverage

- Frameworks + in-house work lower dependence

- Long-term volumes yield concessions

- Alternate qualification maintains pressure

Supplier concentration + >20% metal swings raise BOM risk; rare-earths~60%

Suppliers hold moderate-to-high leverage for Shanghai Electric due to concentrated inputs (steel, rare-earths) and certified, IP-heavy components; China supplied ~60% of global rare-earths (2023–24). 2024 metal price swings exceeded 20%, raising BOM risk while qualification cycles of key vendors run 12–24 months. Shanghai Electric’s scale, framework agreements and partial in-house fabrication partially offset supplier power.

| Metric | 2024 |

|---|---|

| China rare-earth share | ~60% |

| Metal price volatility | >20% |

| Vendor qualification | 12–24 months |

What is included in the product

Tailored exclusively for Shanghai Electric Group Co., this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive forces and market dynamics shaping pricing and profitability.

A concise one-sheet Porter’s Five Forces for Shanghai Electric Group Co.—visual spider/radar chart and customizable pressure levels to pinpoint regulatory, supplier, and competitor risks, ready to drop into pitch decks or Excel dashboards for fast, boardroom-ready decision-making.

Customers Bargaining Power

Large, sophisticated buyers

Utilities, IPPs and industrial SOEs run competitive tenders with strict specs—China’s power system exceeds 2,400 GW of installed capacity and state players control over 70% of large procurements, driving scale-based leverage. Buyers’ procurement expertise forces aggressive pricing and firm performance bonds, with framework contracts and penalty clauses often reaching 5–10% of contract value. Benchmarking across multiple global OEMs is routine, compressing margins for suppliers like Shanghai Electric.

High stakes, long life-cycle deals

As of 2024, Shanghai Electric faces high bargaining power from customers because capital intensity and 20–30 year asset lives create large switching costs after installation. Pre-award buyers use competitive tendering to push for extended warranties and vendor financing. Post-award dependence on service and spare parts moderates buyer leverage, while bundled O&M lowers price sensitivity but increases scrutiny on performance and SLA compliance.

Standardization increases comparability

IEC and GB standardization plus modular designs make bids highly comparable, shifting procurement toward price competition and strengthening buyer bargaining power. Tenders increasingly prioritize lifecycle cost, forcing suppliers to differentiate via measurable efficiency, proven reliability, and integrated digital services. Any temporary spec edge is rapidly eroded as rivals adopt the same standards and modules.

Financing and EPC packaging

Buyers increasingly demand turnkey EPC plus vendor financing to de-risk projects, using the ability to mobilize capital as a key bargaining lever; vendors that bundle financing and EPC often win contracts despite price premiums because tied credit limits buyers' future options and increases switching costs.

- Buyers: seek turnkey EPC + vendor finance

- Leverage: financing mobilization as bargaining power

- Vendors: integrated packages win despite price gaps

- Risk: tied credit reduces later buyer options

Aftermarket leverage varies

In-warranty phases give buyers strong leverage through KPIs and acceptance tests, constraining Shanghai Electric Group Co. on delivery terms and penalties; mid-life overhauls see OEM parts and proprietary software limit alternatives, raising lifecycle costs. Third-party service providers restored buyer leverage for mature fleets, capturing roughly 25% of global turbine servicing by 2024, while performance-based contracts increasingly rebalance incentives.

- Buyers: KPI/acceptance tests

- Mid-life: OEM parts/software lock-in

- Third-party: ~25% market share (2024)

- Contracts: performance-based rebalance

Buyers wield leverage: China >2,400 GW, state >70%, penalties 5–10%

Buyers exert high bargaining power via strict competitive tenders, with China’s power fleet >2,400 GW and state players capturing >70% of large procurements (2024). Contract penalties and bonds commonly reach 5–10% of value, compressing supplier margins. Post-award OEM lock-in raises lifecycle costs, though third-party servicing reached ~25% of turbine servicing globally in 2024, softening buyer leverage.

| Metric | Value (2024) |

|---|---|

| China installed capacity | >2,400 GW |

| State procurement share | >70% |

| Penalty clauses | 5–10% contract value |

| Third-party service share | ~25% global |

Preview the Actual Deliverable

Shanghai Electric Group Co. Porter's Five Forces Analysis

This Porter's Five Forces analysis of Shanghai Electric Group Co. assesses industry rivalry, supplier and buyer power, threat of new entrants, and substitutes, and the document you see here is the exact, fully formatted file you’ll receive instantly after purchase—no samples, no placeholders.