SharkNinja SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

SharkNinja's innovative appliances and strong brand momentum mask growing competitive and supply-chain risks; our SWOT preview highlights the key issues and opportunities. Want the full strategic picture and actionable recommendations? Purchase the complete SWOT for a professionally formatted Word report plus an editable Excel matrix to plan, pitch, or invest with confidence.

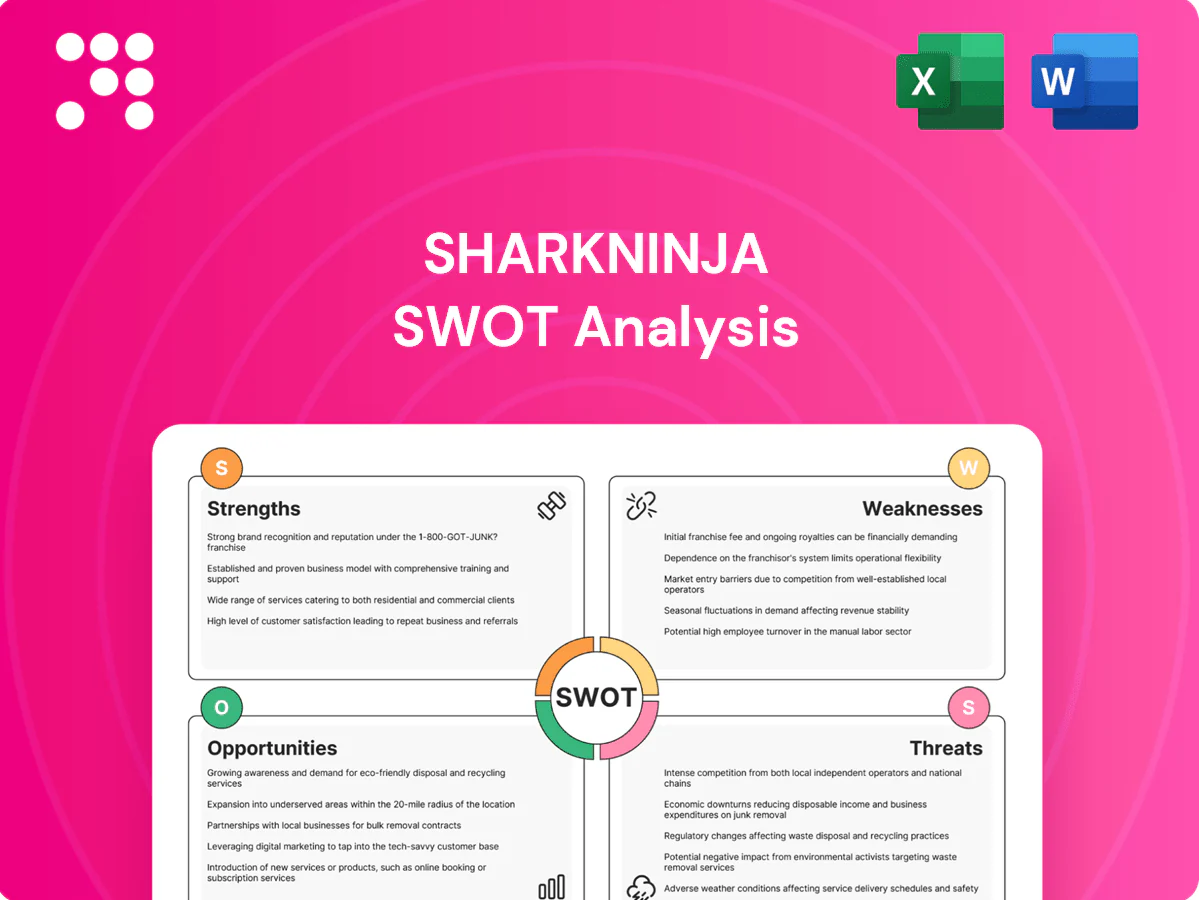

Strengths

Powerful dual-brand portfolio

Shark and Ninja address distinct but complementary household needs—cleaning and kitchen—enabling cross-selling and stronger brand recognition; together they drove approximately $2.2 billion in net sales in FY2024, smoothing seasonality and expanding shelf space. Dual brands allow targeting of varied price points without dilution, strengthening retailer partnerships and boosting repeat purchase loyalty.

Consumer-centric product innovation

SharkNinja emphasizes rapid, insight-driven design to solve clear pain points, using iterative, feature-led improvements that support premium willingness to pay; fast concept-to-market cycles capture trends like air frying and cordless cleaning, and since its Oct 2023 IPO this innovation engine has reinforced repeat purchases and strong word-of-mouth.

Strong retail and e-commerce execution

Broad distribution across mass retail, specialty and direct-to-consumer channels—selling in 100+ countries—boosts SharkNinja visibility and velocity. Data-driven merchandising and pervasive customer reviews improve conversion in both online and offline channels. An omni-channel footprint lowers dependence on any single outlet. It also enables rapid product launches and fast replenishment during demand spikes.

Compelling value-performance positioning

SharkNinja pairs accessible price points with premium features, driving measured share gains; 2024 net sales were about $2.0 billion, reflecting continued strength in home appliances. Clear, quantified performance claims simplify purchase decisions and squeeze both low-cost and high-end rivals, enabling rapid category share growth in mature segments.

- Value-performance sweet spot

- 2024 net sales ~ $2.0B

- Pressures low-cost and premium competitors

- Clear claims aid rapid share gains

Global footprint and scalable supply chain

SharkNinja's global presence across North America, Europe and Asia-Pacific diversifies revenue and boosts brand awareness via major retailers including Amazon, Walmart and Target. Flexible sourcing and contract manufacturing in Asia enable cost control and rapid volume ramps for seasonal demand. Modular product architectures allow platform reuse across vacuum and small-appliance SKUs, driving scale efficiencies that support margin expansion.

- Regional diversification: North America, Europe, Asia-Pacific

- Selling channels: Amazon, Walmart, Target

- Sourcing: contract manufacturing in Asia for rapid ramps

- Design: modular platforms reused across SKUs for scale

Dual-brand group posts $2.2B, global omni-channel scale post-IPO

Dual brands (Shark cleaning, Ninja kitchen) enable cross-selling and drove ~ $2.2B net sales in FY2024, smoothing seasonality. Rapid, insight-led product cycles and modular platforms boost premium features, repeat purchases and fast time-to-market post-Oct 2023 IPO. Omni-channel reach in 100+ countries with Amazon/Walmart/Target and Asian contract manufacturing supports scale and cost control.

| Metric | FY2024 / Scope |

|---|---|

| Net sales | ~ $2.2B |

| Geographic reach | 100+ countries |

| Key retailers | Amazon, Walmart, Target |

| IPO | Oct 2023 |

What is included in the product

Provides a concise SWOT analysis of SharkNinja, highlighting core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decisions.

Provides a concise, visual SharkNinja SWOT matrix that streamlines strategic clarity and stakeholder buy‑in, with an editable format for quick updates and seamless integration into reports and presentations.

Weaknesses

High exposure to retail partners

Reliance on big-box and online marketplaces concentrates channel risk for SharkNinja, with roughly 60% of net sales routed through a few large retailers and e-commerce platforms; in 2024 the company reported about $2.5 billion in revenue, making these partners critical to distribution. Changes in shelf space, platform algorithms, or a push toward private labels can quickly compress margins and erode realized prices. Large retailers often hold stronger negotiating power, constraining SharkNinja’s pricing flexibility and promotional control.

Product recall and quality perception risk

Fast innovation cycles at SharkNinja can introduce reliability issues if not tightly controlled; a single high-profile defect risks eroding trust across Shark and Ninja after generating multi-million-dollar recall expenses (historical consumer-electrics recalls often run into tens of millions). After-sales service costs tend to rise with product complexity, and warranty and returns management is operationally intensive, pressuring margins and working capital.

Limited diversification beyond home appliances

SharkNinja reported roughly $2.2 billion in net sales in fiscal 2024, with over two-thirds of revenue concentrated in cleaning and kitchen appliances. Heavy reliance on these categories means cyclical demand or saturation in core segments can materially slow growth. Expanding into adjacencies—like home electronics or health—requires new R&D, distribution and service capabilities. This concentration heightens vulnerability to category-specific shocks such as supply disruptions or shifting consumer preferences.

Competitive pricing pressure

Mid-premium positioning invites attacks from budget entrants and premium incumbents, squeezing SharkNinja between low-cost rivals and high-end brands.

Frequent promotions can erode average selling prices and train consumers to wait for deals, contributing to margin pressure.

With net sales around $2.6 billion (fiscal 2023) and rising input costs, cost inflation is hard to fully pass through, increasing margin volatility in down cycles.

- Pricing squeeze

- Promotions lower ASPs

- Cost pass-through limits

- Margin volatility

Supply chain and inventory complexity

Multiple SKUs and rapid product launches complicate demand forecasting, where missteps can lead to stockouts or costly excess inventory; global logistics disruptions further risk delaying new product momentum and pressuring margins, while expansions raise working capital requirements and cash conversion strain.

- SKU proliferation increases forecasting error

- Launch cadence risks stockouts or overstock

- Global logistics can delay go-to-market

- Expansions raise working capital needs

60% retail & 66% category mix hits margins, inventory

Heavy channel concentration (~60% of sales through a few retailers) and reliance on cleaning/kitchen categories (~66% of revenue) expose SharkNinja to retail negotiating power, shelf/algorithm shifts and category shocks; frequent promotions and rising input costs squeeze ASPs and margins, while SKU proliferation raises inventory and working-capital risk.

| Metric | Value | Implication |

|---|---|---|

| Fiscal 2024 net sales | $2.5B | Scale but concentration risk |

| Channel concentration | ~60% | Retailer dependency |

| Category concentration | ~66% | Exposure to category cycles |

Same Document Delivered

SharkNinja SWOT Analysis

This is the actual SharkNinja SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, with the same structure and editable content. Buy now to unlock the complete, detailed version ready for download and use.

Dive Deeper Into the Company’s Strategic Blueprint

SharkNinja's innovative appliances and strong brand momentum mask growing competitive and supply-chain risks; our SWOT preview highlights the key issues and opportunities. Want the full strategic picture and actionable recommendations? Purchase the complete SWOT for a professionally formatted Word report plus an editable Excel matrix to plan, pitch, or invest with confidence.

Strengths

Powerful dual-brand portfolio

Shark and Ninja address distinct but complementary household needs—cleaning and kitchen—enabling cross-selling and stronger brand recognition; together they drove approximately $2.2 billion in net sales in FY2024, smoothing seasonality and expanding shelf space. Dual brands allow targeting of varied price points without dilution, strengthening retailer partnerships and boosting repeat purchase loyalty.

Consumer-centric product innovation

SharkNinja emphasizes rapid, insight-driven design to solve clear pain points, using iterative, feature-led improvements that support premium willingness to pay; fast concept-to-market cycles capture trends like air frying and cordless cleaning, and since its Oct 2023 IPO this innovation engine has reinforced repeat purchases and strong word-of-mouth.

Strong retail and e-commerce execution

Broad distribution across mass retail, specialty and direct-to-consumer channels—selling in 100+ countries—boosts SharkNinja visibility and velocity. Data-driven merchandising and pervasive customer reviews improve conversion in both online and offline channels. An omni-channel footprint lowers dependence on any single outlet. It also enables rapid product launches and fast replenishment during demand spikes.

Compelling value-performance positioning

SharkNinja pairs accessible price points with premium features, driving measured share gains; 2024 net sales were about $2.0 billion, reflecting continued strength in home appliances. Clear, quantified performance claims simplify purchase decisions and squeeze both low-cost and high-end rivals, enabling rapid category share growth in mature segments.

- Value-performance sweet spot

- 2024 net sales ~ $2.0B

- Pressures low-cost and premium competitors

- Clear claims aid rapid share gains

Global footprint and scalable supply chain

SharkNinja's global presence across North America, Europe and Asia-Pacific diversifies revenue and boosts brand awareness via major retailers including Amazon, Walmart and Target. Flexible sourcing and contract manufacturing in Asia enable cost control and rapid volume ramps for seasonal demand. Modular product architectures allow platform reuse across vacuum and small-appliance SKUs, driving scale efficiencies that support margin expansion.

- Regional diversification: North America, Europe, Asia-Pacific

- Selling channels: Amazon, Walmart, Target

- Sourcing: contract manufacturing in Asia for rapid ramps

- Design: modular platforms reused across SKUs for scale

Dual-brand group posts $2.2B, global omni-channel scale post-IPO

Dual brands (Shark cleaning, Ninja kitchen) enable cross-selling and drove ~ $2.2B net sales in FY2024, smoothing seasonality. Rapid, insight-led product cycles and modular platforms boost premium features, repeat purchases and fast time-to-market post-Oct 2023 IPO. Omni-channel reach in 100+ countries with Amazon/Walmart/Target and Asian contract manufacturing supports scale and cost control.

| Metric | FY2024 / Scope |

|---|---|

| Net sales | ~ $2.2B |

| Geographic reach | 100+ countries |

| Key retailers | Amazon, Walmart, Target |

| IPO | Oct 2023 |

What is included in the product

Provides a concise SWOT analysis of SharkNinja, highlighting core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decisions.

Provides a concise, visual SharkNinja SWOT matrix that streamlines strategic clarity and stakeholder buy‑in, with an editable format for quick updates and seamless integration into reports and presentations.

Weaknesses

High exposure to retail partners

Reliance on big-box and online marketplaces concentrates channel risk for SharkNinja, with roughly 60% of net sales routed through a few large retailers and e-commerce platforms; in 2024 the company reported about $2.5 billion in revenue, making these partners critical to distribution. Changes in shelf space, platform algorithms, or a push toward private labels can quickly compress margins and erode realized prices. Large retailers often hold stronger negotiating power, constraining SharkNinja’s pricing flexibility and promotional control.

Product recall and quality perception risk

Fast innovation cycles at SharkNinja can introduce reliability issues if not tightly controlled; a single high-profile defect risks eroding trust across Shark and Ninja after generating multi-million-dollar recall expenses (historical consumer-electrics recalls often run into tens of millions). After-sales service costs tend to rise with product complexity, and warranty and returns management is operationally intensive, pressuring margins and working capital.

Limited diversification beyond home appliances

SharkNinja reported roughly $2.2 billion in net sales in fiscal 2024, with over two-thirds of revenue concentrated in cleaning and kitchen appliances. Heavy reliance on these categories means cyclical demand or saturation in core segments can materially slow growth. Expanding into adjacencies—like home electronics or health—requires new R&D, distribution and service capabilities. This concentration heightens vulnerability to category-specific shocks such as supply disruptions or shifting consumer preferences.

Competitive pricing pressure

Mid-premium positioning invites attacks from budget entrants and premium incumbents, squeezing SharkNinja between low-cost rivals and high-end brands.

Frequent promotions can erode average selling prices and train consumers to wait for deals, contributing to margin pressure.

With net sales around $2.6 billion (fiscal 2023) and rising input costs, cost inflation is hard to fully pass through, increasing margin volatility in down cycles.

- Pricing squeeze

- Promotions lower ASPs

- Cost pass-through limits

- Margin volatility

Supply chain and inventory complexity

Multiple SKUs and rapid product launches complicate demand forecasting, where missteps can lead to stockouts or costly excess inventory; global logistics disruptions further risk delaying new product momentum and pressuring margins, while expansions raise working capital requirements and cash conversion strain.

- SKU proliferation increases forecasting error

- Launch cadence risks stockouts or overstock

- Global logistics can delay go-to-market

- Expansions raise working capital needs

60% retail & 66% category mix hits margins, inventory

Heavy channel concentration (~60% of sales through a few retailers) and reliance on cleaning/kitchen categories (~66% of revenue) expose SharkNinja to retail negotiating power, shelf/algorithm shifts and category shocks; frequent promotions and rising input costs squeeze ASPs and margins, while SKU proliferation raises inventory and working-capital risk.

| Metric | Value | Implication |

|---|---|---|

| Fiscal 2024 net sales | $2.5B | Scale but concentration risk |

| Channel concentration | ~60% | Retailer dependency |

| Category concentration | ~66% | Exposure to category cycles |

Same Document Delivered

SharkNinja SWOT Analysis

This is the actual SharkNinja SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, with the same structure and editable content. Buy now to unlock the complete, detailed version ready for download and use.

Description

Dive Deeper Into the Company’s Strategic Blueprint

SharkNinja's innovative appliances and strong brand momentum mask growing competitive and supply-chain risks; our SWOT preview highlights the key issues and opportunities. Want the full strategic picture and actionable recommendations? Purchase the complete SWOT for a professionally formatted Word report plus an editable Excel matrix to plan, pitch, or invest with confidence.

Strengths

Powerful dual-brand portfolio

Shark and Ninja address distinct but complementary household needs—cleaning and kitchen—enabling cross-selling and stronger brand recognition; together they drove approximately $2.2 billion in net sales in FY2024, smoothing seasonality and expanding shelf space. Dual brands allow targeting of varied price points without dilution, strengthening retailer partnerships and boosting repeat purchase loyalty.

Consumer-centric product innovation

SharkNinja emphasizes rapid, insight-driven design to solve clear pain points, using iterative, feature-led improvements that support premium willingness to pay; fast concept-to-market cycles capture trends like air frying and cordless cleaning, and since its Oct 2023 IPO this innovation engine has reinforced repeat purchases and strong word-of-mouth.

Strong retail and e-commerce execution

Broad distribution across mass retail, specialty and direct-to-consumer channels—selling in 100+ countries—boosts SharkNinja visibility and velocity. Data-driven merchandising and pervasive customer reviews improve conversion in both online and offline channels. An omni-channel footprint lowers dependence on any single outlet. It also enables rapid product launches and fast replenishment during demand spikes.

Compelling value-performance positioning

SharkNinja pairs accessible price points with premium features, driving measured share gains; 2024 net sales were about $2.0 billion, reflecting continued strength in home appliances. Clear, quantified performance claims simplify purchase decisions and squeeze both low-cost and high-end rivals, enabling rapid category share growth in mature segments.

- Value-performance sweet spot

- 2024 net sales ~ $2.0B

- Pressures low-cost and premium competitors

- Clear claims aid rapid share gains

Global footprint and scalable supply chain

SharkNinja's global presence across North America, Europe and Asia-Pacific diversifies revenue and boosts brand awareness via major retailers including Amazon, Walmart and Target. Flexible sourcing and contract manufacturing in Asia enable cost control and rapid volume ramps for seasonal demand. Modular product architectures allow platform reuse across vacuum and small-appliance SKUs, driving scale efficiencies that support margin expansion.

- Regional diversification: North America, Europe, Asia-Pacific

- Selling channels: Amazon, Walmart, Target

- Sourcing: contract manufacturing in Asia for rapid ramps

- Design: modular platforms reused across SKUs for scale

Dual-brand group posts $2.2B, global omni-channel scale post-IPO

Dual brands (Shark cleaning, Ninja kitchen) enable cross-selling and drove ~ $2.2B net sales in FY2024, smoothing seasonality. Rapid, insight-led product cycles and modular platforms boost premium features, repeat purchases and fast time-to-market post-Oct 2023 IPO. Omni-channel reach in 100+ countries with Amazon/Walmart/Target and Asian contract manufacturing supports scale and cost control.

| Metric | FY2024 / Scope |

|---|---|

| Net sales | ~ $2.2B |

| Geographic reach | 100+ countries |

| Key retailers | Amazon, Walmart, Target |

| IPO | Oct 2023 |

What is included in the product

Provides a concise SWOT analysis of SharkNinja, highlighting core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decisions.

Provides a concise, visual SharkNinja SWOT matrix that streamlines strategic clarity and stakeholder buy‑in, with an editable format for quick updates and seamless integration into reports and presentations.

Weaknesses

High exposure to retail partners

Reliance on big-box and online marketplaces concentrates channel risk for SharkNinja, with roughly 60% of net sales routed through a few large retailers and e-commerce platforms; in 2024 the company reported about $2.5 billion in revenue, making these partners critical to distribution. Changes in shelf space, platform algorithms, or a push toward private labels can quickly compress margins and erode realized prices. Large retailers often hold stronger negotiating power, constraining SharkNinja’s pricing flexibility and promotional control.

Product recall and quality perception risk

Fast innovation cycles at SharkNinja can introduce reliability issues if not tightly controlled; a single high-profile defect risks eroding trust across Shark and Ninja after generating multi-million-dollar recall expenses (historical consumer-electrics recalls often run into tens of millions). After-sales service costs tend to rise with product complexity, and warranty and returns management is operationally intensive, pressuring margins and working capital.

Limited diversification beyond home appliances

SharkNinja reported roughly $2.2 billion in net sales in fiscal 2024, with over two-thirds of revenue concentrated in cleaning and kitchen appliances. Heavy reliance on these categories means cyclical demand or saturation in core segments can materially slow growth. Expanding into adjacencies—like home electronics or health—requires new R&D, distribution and service capabilities. This concentration heightens vulnerability to category-specific shocks such as supply disruptions or shifting consumer preferences.

Competitive pricing pressure

Mid-premium positioning invites attacks from budget entrants and premium incumbents, squeezing SharkNinja between low-cost rivals and high-end brands.

Frequent promotions can erode average selling prices and train consumers to wait for deals, contributing to margin pressure.

With net sales around $2.6 billion (fiscal 2023) and rising input costs, cost inflation is hard to fully pass through, increasing margin volatility in down cycles.

- Pricing squeeze

- Promotions lower ASPs

- Cost pass-through limits

- Margin volatility

Supply chain and inventory complexity

Multiple SKUs and rapid product launches complicate demand forecasting, where missteps can lead to stockouts or costly excess inventory; global logistics disruptions further risk delaying new product momentum and pressuring margins, while expansions raise working capital requirements and cash conversion strain.

- SKU proliferation increases forecasting error

- Launch cadence risks stockouts or overstock

- Global logistics can delay go-to-market

- Expansions raise working capital needs

60% retail & 66% category mix hits margins, inventory

Heavy channel concentration (~60% of sales through a few retailers) and reliance on cleaning/kitchen categories (~66% of revenue) expose SharkNinja to retail negotiating power, shelf/algorithm shifts and category shocks; frequent promotions and rising input costs squeeze ASPs and margins, while SKU proliferation raises inventory and working-capital risk.

| Metric | Value | Implication |

|---|---|---|

| Fiscal 2024 net sales | $2.5B | Scale but concentration risk |

| Channel concentration | ~60% | Retailer dependency |

| Category concentration | ~66% | Exposure to category cycles |

Same Document Delivered

SharkNinja SWOT Analysis

This is the actual SharkNinja SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, with the same structure and editable content. Buy now to unlock the complete, detailed version ready for download and use.