Shell Plc SWOT Analysis

Make Insightful Decisions Backed by Expert Research

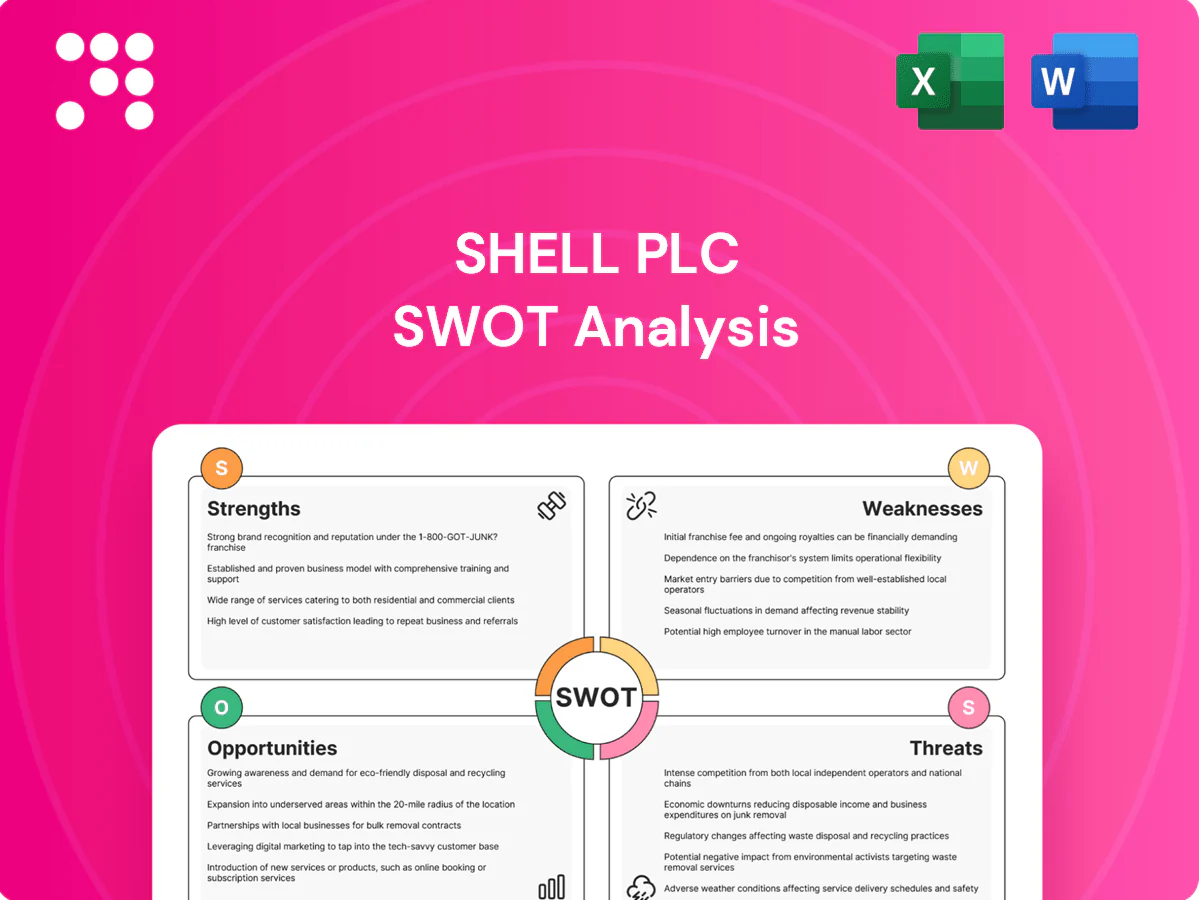

Shell Plc combines global scale, integrated upstream-to-retail capabilities, and robust cash generation—yet faces carbon-intensity challenges and portfolio transition risks. Opportunities include renewables, LNG and low-carbon solutions, while commodity volatility and tightening regulation pose material threats. Purchase the full SWOT analysis to access a detailed, editable report and actionable strategic insights for investors and advisors.

Strengths

Integrated global value chain

Shell's integrated upstream, midstream, downstream and chemicals operations capture margins across the chain, stabilizing cash flow through commodity cycles. Operating in over 70 countries, scale enables advantaged trading, logistics and supply optionality. This integration optimizes feedstock-to-market flows and supports capital allocation toward highest-return segments.

Scale, brand, and market access

Shell’s scale — with over 40,000 retail sites and operations in roughly 70 countries — gives privileged market access across retail, trading and B2B channels. Strong brand equity and long-term customer relationships support premium pricing and cross-selling, with brand value ranking among the industry’s largest. The trading arm, which handles commodity flows worth hundreds of billions annually, boosts marketing margins and enhances risk management.

Diversified energy portfolio

Shell's diversified energy portfolio spans oil and gas, LNG, chemicals, biofuels, hydrogen and power, reducing single-commodity exposure and providing strategic optionality for the energy transition. As a leading LNG trader—handling over 30 million tonnes per year—Shell can supply flexible, lower-carbon gas to shifting markets. Integrated chemicals operations bolster margin resilience and broaden product mix, supporting cash flow stability across cycles.

Robust project execution and capital discipline

Shell has a long track record of delivering large, complex projects and optimizing decline portfolios, with recent strategic divestments and tighter capital allocation improving balance sheet resilience. Recent emphasis on cost control and disciplined capex has prioritized high-return LNG and marketing investments, supporting competitive free cash flow and shareholder distributions. This execution focus underpins sustainable shareholder returns and operational predictability.

- Track record: large-scale project delivery

- Capital discipline: divestments and cost control

- Capex focus: LNG and marketing

- Outcome: stronger free cash flow and shareholder returns

Technology and trading capabilities

Shell leverages advanced subsurface, process and digital capabilities to boost recovery, efficiency and safety, while its leading LNG and power trading franchises provide strong monetization advantages; the company targets $25 billion of low‑carbon investments by 2030 to support new vectors like hydrogen and CCUS.

- Data-driven optimization: higher asset reliability, better margin capture

- Trading scale: LNG and power market leadership

- Innovation pipeline: hydrogen, CCUS, electrification

Upstream-to-retail scale: 40,000+ sites, ~$250bn flow, $25bn low-carbon to 2030

Shell's integrated upstream-to-retail model and scale (40,000+ sites, operations in ~70 countries) stabilise cash flows and enable trading of ~$250bn+ commodity flows annually; LNG volumes ~30 Mtpa. Capital discipline and divestments lift FCF and support $25bn low‑carbon target to 2030.

| Metric | Value |

|---|---|

| Retail sites | 40,000+ |

| Countries | ~70 |

| Trading flow | ~$250bn/yr |

| LNG volume | ~30 Mtpa |

| Low‑carbon capex | $25bn to 2030 |

What is included in the product

Provides a concise strategic overview of Shell Plc’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decisions.

Provides a concise SWOT matrix for Shell Plc, enabling rapid identification of strategic risks and opportunities to ease stakeholder briefings and accelerate executive decision-making.

Weaknesses

High carbon intensity legacy

Shell's large upstream and refining footprints generated about 56 million tonnes of Scope 1–2 CO2e in 2023 and contribute to roughly 1,000 million tonnes of Scope 3 emissions, exposing the company to major climate-related risks.

This high carbon intensity constrains Shell's social license, increases regulatory scrutiny in key markets and risks demand-side pressure from investors and customers.

Decarbonizing heavy assets requires multibillion-dollar investments and long lead times, and capital intensity can dilute returns during transition periods, pressuring margins and free cash flow.

Complex portfolio and governance

Shell's sprawling asset base across oil & gas, chemicals, refining, 43,000 retail sites and operations in over 70 countries raises organizational complexity and overhead. Portfolio heterogeneity complicates KPI alignment and strategy execution, slowing decision-making versus pure-play peers and hampering swift reallocation toward growth areas like renewables and EV charging.

Refining cyclicality and margin volatility

Downstream earnings at Shell remain highly sensitive to crack spreads, utilization and maintenance cycles; global refinery utilization averaged about 82% in 2024 (IEA), exposing margins to commodity price swings. Turnarounds and outages can cut throughput by up to 10%, pressuring cash flow and working capital. Environmental upgrades and compliance have raised sustaining capex, and structural overcapacity in some regions limits pricing power.

Transition execution risk

Shifting capital to biofuels, hydrogen and power exposes Shell to technology, policy and demand uncertainty; returns may trail hydrocarbon benchmarks during rollout and create short-term EPS pressure. Mis-timed investments risk stranded capital and asset write-downs, while divergent stakeholder expectations can pull strategy in conflicting directions.

- Transition execution risk

- Returns lag hydrocarbons

- Stranded-capital potential

- Stakeholder tension

Legal and reputational exposure

Climate litigation, ESG controversies and spill incidents expose Shell to significant financial and brand risk; notably the 2021 Dutch court ordered Shell to cut Group-wide CO2 emissions by 45% from 2019 levels by 2030, setting a legal precedent that amplifies liability. Community opposition can delay or halt projects, while investor scrutiny on emissions targets increases pressure on strategy and capital allocation. Insurance and compliance costs may rise as regulatory and litigation risks grow.

- Legal: 2021 Hague ruling — 45% CO2 cut by 2030

- Operational: community opposition delays projects

- Financial: rising investor scrutiny; higher insurance and compliance costs

Energy major emissions: 56 Mt S1-2, ~1,000 Mt S3 - severe transition risk

Shell's large upstream and refining base emitted about 56 Mt Scope 1–2 CO2e in 2023 and ~1,000 Mt Scope 3, creating major climate and transition risk.

High carbon intensity limits social license, raises regulatory scrutiny and investor pressure, and increases compliance and insurance costs.

Decarbonizing heavy assets needs multibillion-dollar capex, diluting returns and risking stranded capital during the transition.

| Metric | Value | Year/Source |

|---|---|---|

| Scope 1–2 CO2e | 56 Mt | 2023 / Shell |

| Scope 3 CO2e | ~1,000 Mt | 2023 / Shell |

| Refinery utilization | 82% | 2024 / IEA |

| Legal ruling | 45% cut by 2030 | 2021 / Hague court |

Same Document Delivered

Shell Plc SWOT Analysis

This is the actual SWOT analysis document you'll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete, editable file. Unlock the entire detailed SWOT for Shell Plc immediately after checkout.

Make Insightful Decisions Backed by Expert Research

Shell Plc combines global scale, integrated upstream-to-retail capabilities, and robust cash generation—yet faces carbon-intensity challenges and portfolio transition risks. Opportunities include renewables, LNG and low-carbon solutions, while commodity volatility and tightening regulation pose material threats. Purchase the full SWOT analysis to access a detailed, editable report and actionable strategic insights for investors and advisors.

Strengths

Integrated global value chain

Shell's integrated upstream, midstream, downstream and chemicals operations capture margins across the chain, stabilizing cash flow through commodity cycles. Operating in over 70 countries, scale enables advantaged trading, logistics and supply optionality. This integration optimizes feedstock-to-market flows and supports capital allocation toward highest-return segments.

Scale, brand, and market access

Shell’s scale — with over 40,000 retail sites and operations in roughly 70 countries — gives privileged market access across retail, trading and B2B channels. Strong brand equity and long-term customer relationships support premium pricing and cross-selling, with brand value ranking among the industry’s largest. The trading arm, which handles commodity flows worth hundreds of billions annually, boosts marketing margins and enhances risk management.

Diversified energy portfolio

Shell's diversified energy portfolio spans oil and gas, LNG, chemicals, biofuels, hydrogen and power, reducing single-commodity exposure and providing strategic optionality for the energy transition. As a leading LNG trader—handling over 30 million tonnes per year—Shell can supply flexible, lower-carbon gas to shifting markets. Integrated chemicals operations bolster margin resilience and broaden product mix, supporting cash flow stability across cycles.

Robust project execution and capital discipline

Shell has a long track record of delivering large, complex projects and optimizing decline portfolios, with recent strategic divestments and tighter capital allocation improving balance sheet resilience. Recent emphasis on cost control and disciplined capex has prioritized high-return LNG and marketing investments, supporting competitive free cash flow and shareholder distributions. This execution focus underpins sustainable shareholder returns and operational predictability.

- Track record: large-scale project delivery

- Capital discipline: divestments and cost control

- Capex focus: LNG and marketing

- Outcome: stronger free cash flow and shareholder returns

Technology and trading capabilities

Shell leverages advanced subsurface, process and digital capabilities to boost recovery, efficiency and safety, while its leading LNG and power trading franchises provide strong monetization advantages; the company targets $25 billion of low‑carbon investments by 2030 to support new vectors like hydrogen and CCUS.

- Data-driven optimization: higher asset reliability, better margin capture

- Trading scale: LNG and power market leadership

- Innovation pipeline: hydrogen, CCUS, electrification

Upstream-to-retail scale: 40,000+ sites, ~$250bn flow, $25bn low-carbon to 2030

Shell's integrated upstream-to-retail model and scale (40,000+ sites, operations in ~70 countries) stabilise cash flows and enable trading of ~$250bn+ commodity flows annually; LNG volumes ~30 Mtpa. Capital discipline and divestments lift FCF and support $25bn low‑carbon target to 2030.

| Metric | Value |

|---|---|

| Retail sites | 40,000+ |

| Countries | ~70 |

| Trading flow | ~$250bn/yr |

| LNG volume | ~30 Mtpa |

| Low‑carbon capex | $25bn to 2030 |

What is included in the product

Provides a concise strategic overview of Shell Plc’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decisions.

Provides a concise SWOT matrix for Shell Plc, enabling rapid identification of strategic risks and opportunities to ease stakeholder briefings and accelerate executive decision-making.

Weaknesses

High carbon intensity legacy

Shell's large upstream and refining footprints generated about 56 million tonnes of Scope 1–2 CO2e in 2023 and contribute to roughly 1,000 million tonnes of Scope 3 emissions, exposing the company to major climate-related risks.

This high carbon intensity constrains Shell's social license, increases regulatory scrutiny in key markets and risks demand-side pressure from investors and customers.

Decarbonizing heavy assets requires multibillion-dollar investments and long lead times, and capital intensity can dilute returns during transition periods, pressuring margins and free cash flow.

Complex portfolio and governance

Shell's sprawling asset base across oil & gas, chemicals, refining, 43,000 retail sites and operations in over 70 countries raises organizational complexity and overhead. Portfolio heterogeneity complicates KPI alignment and strategy execution, slowing decision-making versus pure-play peers and hampering swift reallocation toward growth areas like renewables and EV charging.

Refining cyclicality and margin volatility

Downstream earnings at Shell remain highly sensitive to crack spreads, utilization and maintenance cycles; global refinery utilization averaged about 82% in 2024 (IEA), exposing margins to commodity price swings. Turnarounds and outages can cut throughput by up to 10%, pressuring cash flow and working capital. Environmental upgrades and compliance have raised sustaining capex, and structural overcapacity in some regions limits pricing power.

Transition execution risk

Shifting capital to biofuels, hydrogen and power exposes Shell to technology, policy and demand uncertainty; returns may trail hydrocarbon benchmarks during rollout and create short-term EPS pressure. Mis-timed investments risk stranded capital and asset write-downs, while divergent stakeholder expectations can pull strategy in conflicting directions.

- Transition execution risk

- Returns lag hydrocarbons

- Stranded-capital potential

- Stakeholder tension

Legal and reputational exposure

Climate litigation, ESG controversies and spill incidents expose Shell to significant financial and brand risk; notably the 2021 Dutch court ordered Shell to cut Group-wide CO2 emissions by 45% from 2019 levels by 2030, setting a legal precedent that amplifies liability. Community opposition can delay or halt projects, while investor scrutiny on emissions targets increases pressure on strategy and capital allocation. Insurance and compliance costs may rise as regulatory and litigation risks grow.

- Legal: 2021 Hague ruling — 45% CO2 cut by 2030

- Operational: community opposition delays projects

- Financial: rising investor scrutiny; higher insurance and compliance costs

Energy major emissions: 56 Mt S1-2, ~1,000 Mt S3 - severe transition risk

Shell's large upstream and refining base emitted about 56 Mt Scope 1–2 CO2e in 2023 and ~1,000 Mt Scope 3, creating major climate and transition risk.

High carbon intensity limits social license, raises regulatory scrutiny and investor pressure, and increases compliance and insurance costs.

Decarbonizing heavy assets needs multibillion-dollar capex, diluting returns and risking stranded capital during the transition.

| Metric | Value | Year/Source |

|---|---|---|

| Scope 1–2 CO2e | 56 Mt | 2023 / Shell |

| Scope 3 CO2e | ~1,000 Mt | 2023 / Shell |

| Refinery utilization | 82% | 2024 / IEA |

| Legal ruling | 45% cut by 2030 | 2021 / Hague court |

Same Document Delivered

Shell Plc SWOT Analysis

This is the actual SWOT analysis document you'll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete, editable file. Unlock the entire detailed SWOT for Shell Plc immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

Shell Plc combines global scale, integrated upstream-to-retail capabilities, and robust cash generation—yet faces carbon-intensity challenges and portfolio transition risks. Opportunities include renewables, LNG and low-carbon solutions, while commodity volatility and tightening regulation pose material threats. Purchase the full SWOT analysis to access a detailed, editable report and actionable strategic insights for investors and advisors.

Strengths

Integrated global value chain

Shell's integrated upstream, midstream, downstream and chemicals operations capture margins across the chain, stabilizing cash flow through commodity cycles. Operating in over 70 countries, scale enables advantaged trading, logistics and supply optionality. This integration optimizes feedstock-to-market flows and supports capital allocation toward highest-return segments.

Scale, brand, and market access

Shell’s scale — with over 40,000 retail sites and operations in roughly 70 countries — gives privileged market access across retail, trading and B2B channels. Strong brand equity and long-term customer relationships support premium pricing and cross-selling, with brand value ranking among the industry’s largest. The trading arm, which handles commodity flows worth hundreds of billions annually, boosts marketing margins and enhances risk management.

Diversified energy portfolio

Shell's diversified energy portfolio spans oil and gas, LNG, chemicals, biofuels, hydrogen and power, reducing single-commodity exposure and providing strategic optionality for the energy transition. As a leading LNG trader—handling over 30 million tonnes per year—Shell can supply flexible, lower-carbon gas to shifting markets. Integrated chemicals operations bolster margin resilience and broaden product mix, supporting cash flow stability across cycles.

Robust project execution and capital discipline

Shell has a long track record of delivering large, complex projects and optimizing decline portfolios, with recent strategic divestments and tighter capital allocation improving balance sheet resilience. Recent emphasis on cost control and disciplined capex has prioritized high-return LNG and marketing investments, supporting competitive free cash flow and shareholder distributions. This execution focus underpins sustainable shareholder returns and operational predictability.

- Track record: large-scale project delivery

- Capital discipline: divestments and cost control

- Capex focus: LNG and marketing

- Outcome: stronger free cash flow and shareholder returns

Technology and trading capabilities

Shell leverages advanced subsurface, process and digital capabilities to boost recovery, efficiency and safety, while its leading LNG and power trading franchises provide strong monetization advantages; the company targets $25 billion of low‑carbon investments by 2030 to support new vectors like hydrogen and CCUS.

- Data-driven optimization: higher asset reliability, better margin capture

- Trading scale: LNG and power market leadership

- Innovation pipeline: hydrogen, CCUS, electrification

Upstream-to-retail scale: 40,000+ sites, ~$250bn flow, $25bn low-carbon to 2030

Shell's integrated upstream-to-retail model and scale (40,000+ sites, operations in ~70 countries) stabilise cash flows and enable trading of ~$250bn+ commodity flows annually; LNG volumes ~30 Mtpa. Capital discipline and divestments lift FCF and support $25bn low‑carbon target to 2030.

| Metric | Value |

|---|---|

| Retail sites | 40,000+ |

| Countries | ~70 |

| Trading flow | ~$250bn/yr |

| LNG volume | ~30 Mtpa |

| Low‑carbon capex | $25bn to 2030 |

What is included in the product

Provides a concise strategic overview of Shell Plc’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decisions.

Provides a concise SWOT matrix for Shell Plc, enabling rapid identification of strategic risks and opportunities to ease stakeholder briefings and accelerate executive decision-making.

Weaknesses

High carbon intensity legacy

Shell's large upstream and refining footprints generated about 56 million tonnes of Scope 1–2 CO2e in 2023 and contribute to roughly 1,000 million tonnes of Scope 3 emissions, exposing the company to major climate-related risks.

This high carbon intensity constrains Shell's social license, increases regulatory scrutiny in key markets and risks demand-side pressure from investors and customers.

Decarbonizing heavy assets requires multibillion-dollar investments and long lead times, and capital intensity can dilute returns during transition periods, pressuring margins and free cash flow.

Complex portfolio and governance

Shell's sprawling asset base across oil & gas, chemicals, refining, 43,000 retail sites and operations in over 70 countries raises organizational complexity and overhead. Portfolio heterogeneity complicates KPI alignment and strategy execution, slowing decision-making versus pure-play peers and hampering swift reallocation toward growth areas like renewables and EV charging.

Refining cyclicality and margin volatility

Downstream earnings at Shell remain highly sensitive to crack spreads, utilization and maintenance cycles; global refinery utilization averaged about 82% in 2024 (IEA), exposing margins to commodity price swings. Turnarounds and outages can cut throughput by up to 10%, pressuring cash flow and working capital. Environmental upgrades and compliance have raised sustaining capex, and structural overcapacity in some regions limits pricing power.

Transition execution risk

Shifting capital to biofuels, hydrogen and power exposes Shell to technology, policy and demand uncertainty; returns may trail hydrocarbon benchmarks during rollout and create short-term EPS pressure. Mis-timed investments risk stranded capital and asset write-downs, while divergent stakeholder expectations can pull strategy in conflicting directions.

- Transition execution risk

- Returns lag hydrocarbons

- Stranded-capital potential

- Stakeholder tension

Legal and reputational exposure

Climate litigation, ESG controversies and spill incidents expose Shell to significant financial and brand risk; notably the 2021 Dutch court ordered Shell to cut Group-wide CO2 emissions by 45% from 2019 levels by 2030, setting a legal precedent that amplifies liability. Community opposition can delay or halt projects, while investor scrutiny on emissions targets increases pressure on strategy and capital allocation. Insurance and compliance costs may rise as regulatory and litigation risks grow.

- Legal: 2021 Hague ruling — 45% CO2 cut by 2030

- Operational: community opposition delays projects

- Financial: rising investor scrutiny; higher insurance and compliance costs

Energy major emissions: 56 Mt S1-2, ~1,000 Mt S3 - severe transition risk

Shell's large upstream and refining base emitted about 56 Mt Scope 1–2 CO2e in 2023 and ~1,000 Mt Scope 3, creating major climate and transition risk.

High carbon intensity limits social license, raises regulatory scrutiny and investor pressure, and increases compliance and insurance costs.

Decarbonizing heavy assets needs multibillion-dollar capex, diluting returns and risking stranded capital during the transition.

| Metric | Value | Year/Source |

|---|---|---|

| Scope 1–2 CO2e | 56 Mt | 2023 / Shell |

| Scope 3 CO2e | ~1,000 Mt | 2023 / Shell |

| Refinery utilization | 82% | 2024 / IEA |

| Legal ruling | 45% cut by 2030 | 2021 / Hague court |

Same Document Delivered

Shell Plc SWOT Analysis

This is the actual SWOT analysis document you'll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete, editable file. Unlock the entire detailed SWOT for Shell Plc immediately after checkout.