Jiangsu Eastern Shenghong PESTLE Analysis

Skip the Research. Get the Strategy.

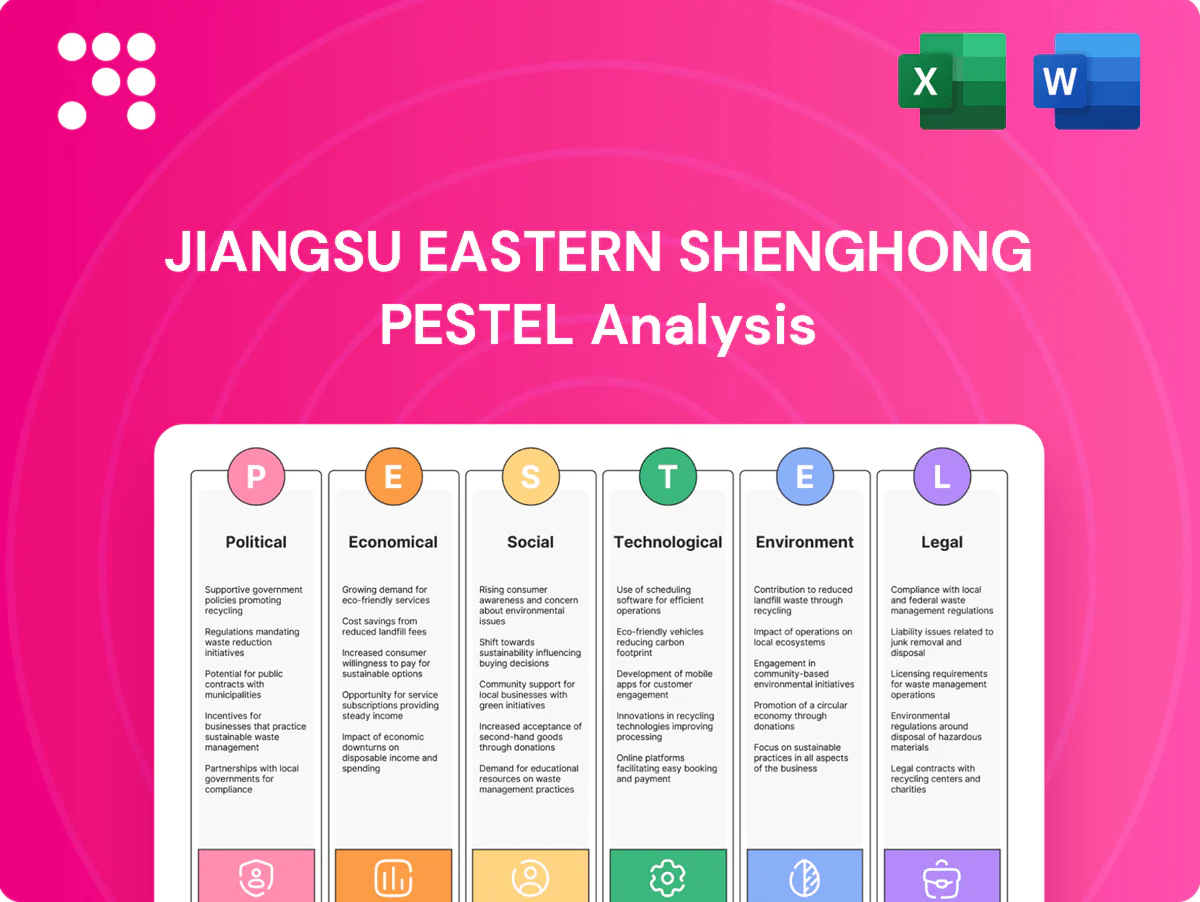

Gain strategic clarity with our concise PESTLE analysis of Jiangsu Eastern Shenghong. We map political, economic, social, technological, legal and environmental drivers affecting operations and margins. Use these insights to anticipate risks and spot growth levers. Buy the full report for the complete, actionable breakdown.

Political factors

China industrial policy support

Alignment with national strategies such as Made in China 2025 and the 14th Five-Year Plan can unlock tax breaks, grants and preferential land for advanced materials and new energy projects. Fiber-to-petrochemical integration aligns with manufacturing-upgrading agendas and can accelerate access to incentives. Policy shifts favoring green materials are re-weighting capex toward low-carbon tech. Close coordination with Jiangsu authorities is pivotal given the province's 2023 GDP of ~12.7 trillion RMB.

Energy security priorities

Refining and petrochemicals at Jiangsu Eastern Shenghong benefit from policies to bolster domestic feedstock resilience, supporting its ~10 mtpa refinery throughput. Crude import quotas and strategic reserve operations, with China importing about 70% of crude, materially influence utilization and margins. Government price mechanisms for fuels and utilities compress spreads versus global peers. Diversification into new energy aligns with China’s 2030 carbon peak and 2060 neutrality goals.

Geopolitical trade tensions

Geopolitical trade tensions can hit Jiangsu Eastern Shenghong via US/EU trade remedies—US Section 301 tariffs (7.5–25% on many Chinese imports) and EU anti-dumping cases raise compliance costs and constrain polymer/textile exports. Sanctions or disruptions in energy corridors like the Strait of Hormuz (carries ~20% of seaborne crude) threaten crude/naphtha sourcing. Rules-of-origin under RCEP (15 members, ~30% of global GDP) materially shape duty-free access, while rapid diplomatic shifts can promptly reset tariff and non-tariff barriers.

Local environmental enforcement

Stricter provincial inspections in Jiangsu can force retrofits, temporary shutdowns or fines, raising capex and downtime risk for Eastern Shenghong; Jiangsu's 2023 GDP ~13 trillion RMB underscores regulatory focus on industrial emissions. Compliance on VOCs, wastewater and solid waste is increasingly tied to operating permits, while park-level environmental infrastructure and transparent reporting reduce enforcement exposure.

- Inspections: enforcement-triggered retrofits/shutdowns

- Permits: VOCs/waste linked to operating status

- Park infra: lowers compliance risk

- Reporting: builds regulatory goodwill

Belt and Road logistics links

Belt and Road port, rail and pipeline investments strengthen feedstock inflow and product outflow for Jiangsu Eastern Shenghong; China-Europe rail cuts transit to about 12–18 days, improving turnaround. Preferential bonded zone policies lower duties and handling time, trimming costs and lead times. Cross-border logistics rules influence inventory levels and working capital needs, while political stability along routes determines reliability; BRI covers 140+ countries as of 2024.

14th Plan fuels new energy; Jiangsu GDP ~13T RMB, crude imports ~70%

Political support for advanced materials and new energy (14th Five-Year Plan, Made in China 2025) drives incentives and land preference; Jiangsu 2023 GDP ~13 trillion RMB raises regulatory scrutiny. Crude import dependence (~70% of demand) and ~10 mtpa refinery throughput expose margins to quotas, reserves and trade measures. BRI logistics and RCEP shape trade costs and market access.

| Metric | Value |

|---|---|

| Jiangsu GDP (2023) | ~13 trillion RMB |

| China crude import share (2024) | ~70% |

| Eastern Shenghong refinery | ~10 mtpa |

| BRI coverage (2024) | 140+ countries |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental and Legal—specifically impact Jiangsu Eastern Shenghong, with data-backed trends and region/industry examples to highlight risks and opportunities. Designed for executives and investors, the analysis offers forward-looking insights and clean, ready-to-use formatting for strategy, funding or reporting.

A concise PESTLE snapshot of Jiangsu Eastern Shenghong that distills regulatory, environmental, economic and market risks into a single reference, easing prep for meetings and decision-making.

Economic factors

Feedstock and spread volatility

Brent averaged about 85 USD/bbl in H1 2025 while naphtha traded roughly 650–850 USD/ton and PX/PTA ranged near 900–1,200 USD/ton and 650–850 USD/ton respectively, driving polyester margin swings from about -50 to +320 USD/ton in 2024–25. Vertical integration cushions but cannot prevent global spread compression. Hedging and long-term contracts (often covering up to ~50% of exposure) stabilize cash flow. Rapid spread reversals complicate capacity ramp decisions and investment timing.

Domestic demand cycles

Apparel, home-textile and industrial-fabric demand in China forms the baseline offtake for Jiangsu Eastern Shenghong, with domestic textile consumption concentrated in urban household and industrial procurement channels. Inventory cycles among downstream converters commonly amplify order volatility, creating sharp swings in monthly resin and filament demand. Targeted government stimulus and consumption-coupon campaigns in dozens of cities during 2023–24 have periodically lifted volumes. During slowdowns intensified price competition amid already high domestic capacity pressures margins.

Export market exposure

RMB volatility in 2024–H1 2025 (around 7.1–7.4 per USD) pressures export pricing and margins, forcing pass-through or hedging. Container freight rates fell over 80% from 2021 peaks to near pre‑pandemic levels by 2024, yet spot swings and container shortages still raise delivered costs. Growing share in ASEAN (China's largest trading partner since 2023), South Asia and Africa diversifies demand while trade remedies in developed markets demand rapid reallocation.

Capacity overhang risk

China’s recent polyester/nylon capacity build means China now represents roughly 60% of global polyester capacity, risking utilization drops and weaker pricing; rationalization will hinge on relative cost curves, energy intensity and feedstock integration at plants like Jiangsu Eastern Shenghong. Delayed start-ups or phased debottlenecking have preserved margins in prior cycles; consolidation waves (M&A/scale) can restore pricing power.

- capacity-share: China ~60% of global polyester

- key drivers: feedstock cost, energy intensity, integration depth

- mitigants: delayed projects/phased debottlenecking

- outcome: consolidation creates scale advantages

Capital intensity and financing

Refining-petrochemical and chemical-recycling lines at Jiangsu Eastern Shenghong require heavy upfront capex, with projects often needing multi-hundred-million to billion-yuan investments; access to onshore credit and policy-backed funding (policy banks, provincial support) reduces WACC and eases financing. Shifts in benchmark rates and the 1Y LPR (around 3.65% in 2024) directly move IRR hurdles, while strong cash flow from integrated refining-to-petchem chains funds diversification and recycling rollouts.

- Capex: large-scale, multi-hundred-million–to–billion CNY projects

- Financing: onshore credit + policy banks lower WACC

- Rates: 1Y LPR ~3.65% (2024) alters IRR thresholds

- Cash: integrated chain cash generation supports diversification

14th Plan fuels new energy; Jiangsu GDP ~13T RMB, crude imports ~70%

Brent ~85 USD/bbl, naphtha 650–850 USD/t, PX/PTA 900–1,200 / 650–850 USD/t drove polyester spreads -50 to +320 USD/t; vertical integration and ~50% hedged contracts stabilise cash flow. RMB 7.1–7.4/USD (2024–H1 2025) and 1Y LPR ~3.65% affect export pricing and IRRs. China ~60% of global polyester capacity pressures utilisation, while policy bank financing lowers WACC.

| Metric | Value |

|---|---|

| Brent (H1 2025) | ~85 USD/bbl |

| Naphtha | 650–850 USD/t |

| PX/PTA | 900–1,200 / 650–850 USD/t |

| RMB | 7.1–7.4 per USD |

| China polyester share | ~60% |

| 1Y LPR (2024) | ~3.65% |

Full Version Awaits

Jiangsu Eastern Shenghong PESTLE Analysis

The preview of the Jiangsu Eastern Shenghong PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This real file contains the complete political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or teasers—what you see is the finished, downloadable report.

Skip the Research. Get the Strategy.

Gain strategic clarity with our concise PESTLE analysis of Jiangsu Eastern Shenghong. We map political, economic, social, technological, legal and environmental drivers affecting operations and margins. Use these insights to anticipate risks and spot growth levers. Buy the full report for the complete, actionable breakdown.

Political factors

China industrial policy support

Alignment with national strategies such as Made in China 2025 and the 14th Five-Year Plan can unlock tax breaks, grants and preferential land for advanced materials and new energy projects. Fiber-to-petrochemical integration aligns with manufacturing-upgrading agendas and can accelerate access to incentives. Policy shifts favoring green materials are re-weighting capex toward low-carbon tech. Close coordination with Jiangsu authorities is pivotal given the province's 2023 GDP of ~12.7 trillion RMB.

Energy security priorities

Refining and petrochemicals at Jiangsu Eastern Shenghong benefit from policies to bolster domestic feedstock resilience, supporting its ~10 mtpa refinery throughput. Crude import quotas and strategic reserve operations, with China importing about 70% of crude, materially influence utilization and margins. Government price mechanisms for fuels and utilities compress spreads versus global peers. Diversification into new energy aligns with China’s 2030 carbon peak and 2060 neutrality goals.

Geopolitical trade tensions

Geopolitical trade tensions can hit Jiangsu Eastern Shenghong via US/EU trade remedies—US Section 301 tariffs (7.5–25% on many Chinese imports) and EU anti-dumping cases raise compliance costs and constrain polymer/textile exports. Sanctions or disruptions in energy corridors like the Strait of Hormuz (carries ~20% of seaborne crude) threaten crude/naphtha sourcing. Rules-of-origin under RCEP (15 members, ~30% of global GDP) materially shape duty-free access, while rapid diplomatic shifts can promptly reset tariff and non-tariff barriers.

Local environmental enforcement

Stricter provincial inspections in Jiangsu can force retrofits, temporary shutdowns or fines, raising capex and downtime risk for Eastern Shenghong; Jiangsu's 2023 GDP ~13 trillion RMB underscores regulatory focus on industrial emissions. Compliance on VOCs, wastewater and solid waste is increasingly tied to operating permits, while park-level environmental infrastructure and transparent reporting reduce enforcement exposure.

- Inspections: enforcement-triggered retrofits/shutdowns

- Permits: VOCs/waste linked to operating status

- Park infra: lowers compliance risk

- Reporting: builds regulatory goodwill

Belt and Road logistics links

Belt and Road port, rail and pipeline investments strengthen feedstock inflow and product outflow for Jiangsu Eastern Shenghong; China-Europe rail cuts transit to about 12–18 days, improving turnaround. Preferential bonded zone policies lower duties and handling time, trimming costs and lead times. Cross-border logistics rules influence inventory levels and working capital needs, while political stability along routes determines reliability; BRI covers 140+ countries as of 2024.

14th Plan fuels new energy; Jiangsu GDP ~13T RMB, crude imports ~70%

Political support for advanced materials and new energy (14th Five-Year Plan, Made in China 2025) drives incentives and land preference; Jiangsu 2023 GDP ~13 trillion RMB raises regulatory scrutiny. Crude import dependence (~70% of demand) and ~10 mtpa refinery throughput expose margins to quotas, reserves and trade measures. BRI logistics and RCEP shape trade costs and market access.

| Metric | Value |

|---|---|

| Jiangsu GDP (2023) | ~13 trillion RMB |

| China crude import share (2024) | ~70% |

| Eastern Shenghong refinery | ~10 mtpa |

| BRI coverage (2024) | 140+ countries |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental and Legal—specifically impact Jiangsu Eastern Shenghong, with data-backed trends and region/industry examples to highlight risks and opportunities. Designed for executives and investors, the analysis offers forward-looking insights and clean, ready-to-use formatting for strategy, funding or reporting.

A concise PESTLE snapshot of Jiangsu Eastern Shenghong that distills regulatory, environmental, economic and market risks into a single reference, easing prep for meetings and decision-making.

Economic factors

Feedstock and spread volatility

Brent averaged about 85 USD/bbl in H1 2025 while naphtha traded roughly 650–850 USD/ton and PX/PTA ranged near 900–1,200 USD/ton and 650–850 USD/ton respectively, driving polyester margin swings from about -50 to +320 USD/ton in 2024–25. Vertical integration cushions but cannot prevent global spread compression. Hedging and long-term contracts (often covering up to ~50% of exposure) stabilize cash flow. Rapid spread reversals complicate capacity ramp decisions and investment timing.

Domestic demand cycles

Apparel, home-textile and industrial-fabric demand in China forms the baseline offtake for Jiangsu Eastern Shenghong, with domestic textile consumption concentrated in urban household and industrial procurement channels. Inventory cycles among downstream converters commonly amplify order volatility, creating sharp swings in monthly resin and filament demand. Targeted government stimulus and consumption-coupon campaigns in dozens of cities during 2023–24 have periodically lifted volumes. During slowdowns intensified price competition amid already high domestic capacity pressures margins.

Export market exposure

RMB volatility in 2024–H1 2025 (around 7.1–7.4 per USD) pressures export pricing and margins, forcing pass-through or hedging. Container freight rates fell over 80% from 2021 peaks to near pre‑pandemic levels by 2024, yet spot swings and container shortages still raise delivered costs. Growing share in ASEAN (China's largest trading partner since 2023), South Asia and Africa diversifies demand while trade remedies in developed markets demand rapid reallocation.

Capacity overhang risk

China’s recent polyester/nylon capacity build means China now represents roughly 60% of global polyester capacity, risking utilization drops and weaker pricing; rationalization will hinge on relative cost curves, energy intensity and feedstock integration at plants like Jiangsu Eastern Shenghong. Delayed start-ups or phased debottlenecking have preserved margins in prior cycles; consolidation waves (M&A/scale) can restore pricing power.

- capacity-share: China ~60% of global polyester

- key drivers: feedstock cost, energy intensity, integration depth

- mitigants: delayed projects/phased debottlenecking

- outcome: consolidation creates scale advantages

Capital intensity and financing

Refining-petrochemical and chemical-recycling lines at Jiangsu Eastern Shenghong require heavy upfront capex, with projects often needing multi-hundred-million to billion-yuan investments; access to onshore credit and policy-backed funding (policy banks, provincial support) reduces WACC and eases financing. Shifts in benchmark rates and the 1Y LPR (around 3.65% in 2024) directly move IRR hurdles, while strong cash flow from integrated refining-to-petchem chains funds diversification and recycling rollouts.

- Capex: large-scale, multi-hundred-million–to–billion CNY projects

- Financing: onshore credit + policy banks lower WACC

- Rates: 1Y LPR ~3.65% (2024) alters IRR thresholds

- Cash: integrated chain cash generation supports diversification

14th Plan fuels new energy; Jiangsu GDP ~13T RMB, crude imports ~70%

Brent ~85 USD/bbl, naphtha 650–850 USD/t, PX/PTA 900–1,200 / 650–850 USD/t drove polyester spreads -50 to +320 USD/t; vertical integration and ~50% hedged contracts stabilise cash flow. RMB 7.1–7.4/USD (2024–H1 2025) and 1Y LPR ~3.65% affect export pricing and IRRs. China ~60% of global polyester capacity pressures utilisation, while policy bank financing lowers WACC.

| Metric | Value |

|---|---|

| Brent (H1 2025) | ~85 USD/bbl |

| Naphtha | 650–850 USD/t |

| PX/PTA | 900–1,200 / 650–850 USD/t |

| RMB | 7.1–7.4 per USD |

| China polyester share | ~60% |

| 1Y LPR (2024) | ~3.65% |

Full Version Awaits

Jiangsu Eastern Shenghong PESTLE Analysis

The preview of the Jiangsu Eastern Shenghong PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This real file contains the complete political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or teasers—what you see is the finished, downloadable report.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Gain strategic clarity with our concise PESTLE analysis of Jiangsu Eastern Shenghong. We map political, economic, social, technological, legal and environmental drivers affecting operations and margins. Use these insights to anticipate risks and spot growth levers. Buy the full report for the complete, actionable breakdown.

Political factors

China industrial policy support

Alignment with national strategies such as Made in China 2025 and the 14th Five-Year Plan can unlock tax breaks, grants and preferential land for advanced materials and new energy projects. Fiber-to-petrochemical integration aligns with manufacturing-upgrading agendas and can accelerate access to incentives. Policy shifts favoring green materials are re-weighting capex toward low-carbon tech. Close coordination with Jiangsu authorities is pivotal given the province's 2023 GDP of ~12.7 trillion RMB.

Energy security priorities

Refining and petrochemicals at Jiangsu Eastern Shenghong benefit from policies to bolster domestic feedstock resilience, supporting its ~10 mtpa refinery throughput. Crude import quotas and strategic reserve operations, with China importing about 70% of crude, materially influence utilization and margins. Government price mechanisms for fuels and utilities compress spreads versus global peers. Diversification into new energy aligns with China’s 2030 carbon peak and 2060 neutrality goals.

Geopolitical trade tensions

Geopolitical trade tensions can hit Jiangsu Eastern Shenghong via US/EU trade remedies—US Section 301 tariffs (7.5–25% on many Chinese imports) and EU anti-dumping cases raise compliance costs and constrain polymer/textile exports. Sanctions or disruptions in energy corridors like the Strait of Hormuz (carries ~20% of seaborne crude) threaten crude/naphtha sourcing. Rules-of-origin under RCEP (15 members, ~30% of global GDP) materially shape duty-free access, while rapid diplomatic shifts can promptly reset tariff and non-tariff barriers.

Local environmental enforcement

Stricter provincial inspections in Jiangsu can force retrofits, temporary shutdowns or fines, raising capex and downtime risk for Eastern Shenghong; Jiangsu's 2023 GDP ~13 trillion RMB underscores regulatory focus on industrial emissions. Compliance on VOCs, wastewater and solid waste is increasingly tied to operating permits, while park-level environmental infrastructure and transparent reporting reduce enforcement exposure.

- Inspections: enforcement-triggered retrofits/shutdowns

- Permits: VOCs/waste linked to operating status

- Park infra: lowers compliance risk

- Reporting: builds regulatory goodwill

Belt and Road logistics links

Belt and Road port, rail and pipeline investments strengthen feedstock inflow and product outflow for Jiangsu Eastern Shenghong; China-Europe rail cuts transit to about 12–18 days, improving turnaround. Preferential bonded zone policies lower duties and handling time, trimming costs and lead times. Cross-border logistics rules influence inventory levels and working capital needs, while political stability along routes determines reliability; BRI covers 140+ countries as of 2024.

14th Plan fuels new energy; Jiangsu GDP ~13T RMB, crude imports ~70%

Political support for advanced materials and new energy (14th Five-Year Plan, Made in China 2025) drives incentives and land preference; Jiangsu 2023 GDP ~13 trillion RMB raises regulatory scrutiny. Crude import dependence (~70% of demand) and ~10 mtpa refinery throughput expose margins to quotas, reserves and trade measures. BRI logistics and RCEP shape trade costs and market access.

| Metric | Value |

|---|---|

| Jiangsu GDP (2023) | ~13 trillion RMB |

| China crude import share (2024) | ~70% |

| Eastern Shenghong refinery | ~10 mtpa |

| BRI coverage (2024) | 140+ countries |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental and Legal—specifically impact Jiangsu Eastern Shenghong, with data-backed trends and region/industry examples to highlight risks and opportunities. Designed for executives and investors, the analysis offers forward-looking insights and clean, ready-to-use formatting for strategy, funding or reporting.

A concise PESTLE snapshot of Jiangsu Eastern Shenghong that distills regulatory, environmental, economic and market risks into a single reference, easing prep for meetings and decision-making.

Economic factors

Feedstock and spread volatility

Brent averaged about 85 USD/bbl in H1 2025 while naphtha traded roughly 650–850 USD/ton and PX/PTA ranged near 900–1,200 USD/ton and 650–850 USD/ton respectively, driving polyester margin swings from about -50 to +320 USD/ton in 2024–25. Vertical integration cushions but cannot prevent global spread compression. Hedging and long-term contracts (often covering up to ~50% of exposure) stabilize cash flow. Rapid spread reversals complicate capacity ramp decisions and investment timing.

Domestic demand cycles

Apparel, home-textile and industrial-fabric demand in China forms the baseline offtake for Jiangsu Eastern Shenghong, with domestic textile consumption concentrated in urban household and industrial procurement channels. Inventory cycles among downstream converters commonly amplify order volatility, creating sharp swings in monthly resin and filament demand. Targeted government stimulus and consumption-coupon campaigns in dozens of cities during 2023–24 have periodically lifted volumes. During slowdowns intensified price competition amid already high domestic capacity pressures margins.

Export market exposure

RMB volatility in 2024–H1 2025 (around 7.1–7.4 per USD) pressures export pricing and margins, forcing pass-through or hedging. Container freight rates fell over 80% from 2021 peaks to near pre‑pandemic levels by 2024, yet spot swings and container shortages still raise delivered costs. Growing share in ASEAN (China's largest trading partner since 2023), South Asia and Africa diversifies demand while trade remedies in developed markets demand rapid reallocation.

Capacity overhang risk

China’s recent polyester/nylon capacity build means China now represents roughly 60% of global polyester capacity, risking utilization drops and weaker pricing; rationalization will hinge on relative cost curves, energy intensity and feedstock integration at plants like Jiangsu Eastern Shenghong. Delayed start-ups or phased debottlenecking have preserved margins in prior cycles; consolidation waves (M&A/scale) can restore pricing power.

- capacity-share: China ~60% of global polyester

- key drivers: feedstock cost, energy intensity, integration depth

- mitigants: delayed projects/phased debottlenecking

- outcome: consolidation creates scale advantages

Capital intensity and financing

Refining-petrochemical and chemical-recycling lines at Jiangsu Eastern Shenghong require heavy upfront capex, with projects often needing multi-hundred-million to billion-yuan investments; access to onshore credit and policy-backed funding (policy banks, provincial support) reduces WACC and eases financing. Shifts in benchmark rates and the 1Y LPR (around 3.65% in 2024) directly move IRR hurdles, while strong cash flow from integrated refining-to-petchem chains funds diversification and recycling rollouts.

- Capex: large-scale, multi-hundred-million–to–billion CNY projects

- Financing: onshore credit + policy banks lower WACC

- Rates: 1Y LPR ~3.65% (2024) alters IRR thresholds

- Cash: integrated chain cash generation supports diversification

14th Plan fuels new energy; Jiangsu GDP ~13T RMB, crude imports ~70%

Brent ~85 USD/bbl, naphtha 650–850 USD/t, PX/PTA 900–1,200 / 650–850 USD/t drove polyester spreads -50 to +320 USD/t; vertical integration and ~50% hedged contracts stabilise cash flow. RMB 7.1–7.4/USD (2024–H1 2025) and 1Y LPR ~3.65% affect export pricing and IRRs. China ~60% of global polyester capacity pressures utilisation, while policy bank financing lowers WACC.

| Metric | Value |

|---|---|

| Brent (H1 2025) | ~85 USD/bbl |

| Naphtha | 650–850 USD/t |

| PX/PTA | 900–1,200 / 650–850 USD/t |

| RMB | 7.1–7.4 per USD |

| China polyester share | ~60% |

| 1Y LPR (2024) | ~3.65% |

Full Version Awaits

Jiangsu Eastern Shenghong PESTLE Analysis

The preview of the Jiangsu Eastern Shenghong PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This real file contains the complete political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or teasers—what you see is the finished, downloadable report.