Sherwin-Williams Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

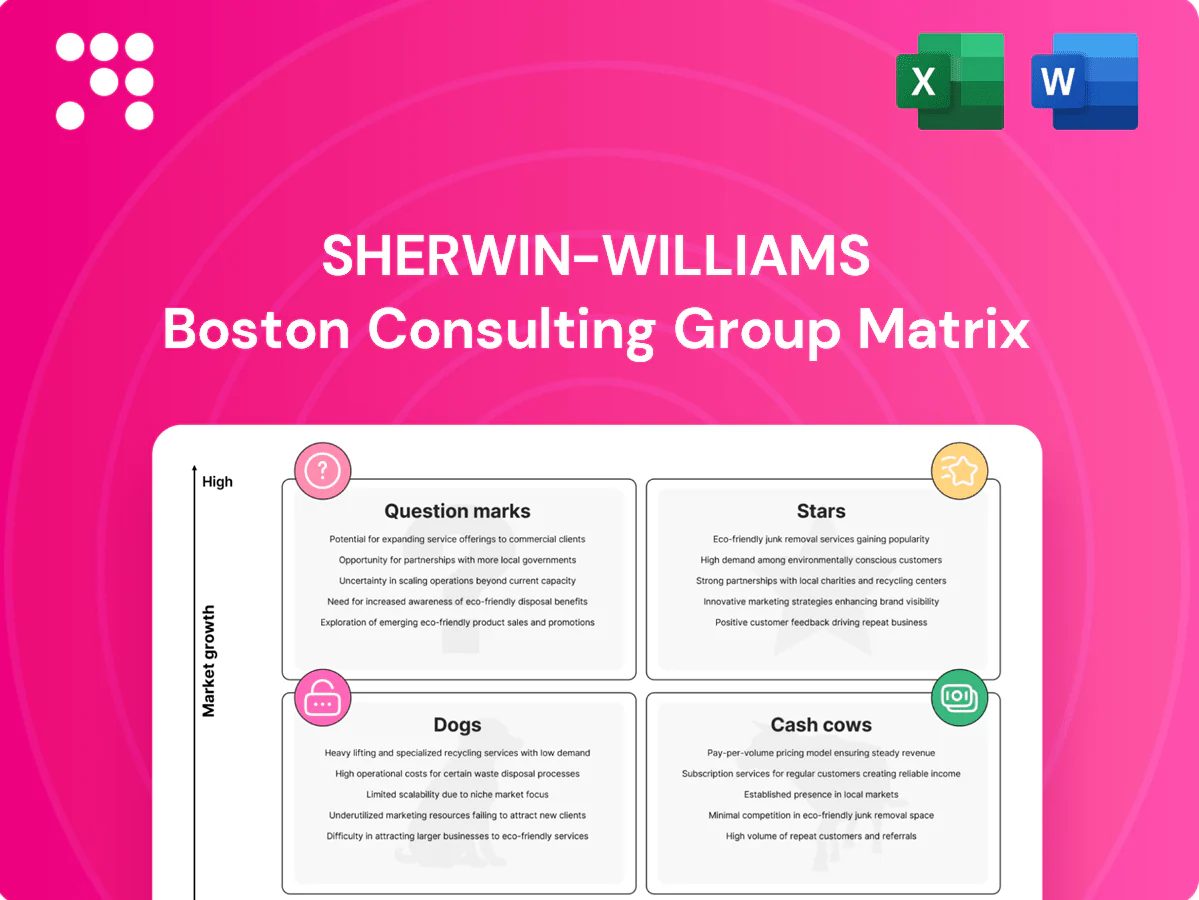

Sherwin‑Williams’ BCG Matrix preview shows which paint lines lead the market and which may be draining resources, but it’s only the tip of the iceberg. Get the full BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and clear moves on investment, divestment, or focus. Purchase now and receive a ready-to-use Word report plus a high-level Excel summary—strategic clarity you can present and act on immediately.

Stars

Pro paint stores in The Americas Group

Pro repaint and construction cycles drive high store traffic and Sherwin-Williams dominates the pro channel through its dense store network, sustaining market share and contractor relationships.

Share is strong and the service model is sticky, but the segment consumes significant cash for new openings, staffing and last-mile delivery investments.

Maintain investments in geographic coverage, contractor loyalty programs and trade credit to lock the lead; as industry growth normalizes this engine can migrate into Cash Cow status.

Protective & marine coatings for infrastructure

Public and industrial capex is accelerating—U.S. Bipartisan Infrastructure Law alone authorized $1.2 trillion total (about $550 billion in new spending), driving demand for proven protective and marine coatings on bridges, plants and ports. Sherwin-Williams is a leading North American supplier with high regional share; projects are large and technical service differentiates wins. Bid cycles, certification needs and fund-application support require heavy selling effort to secure spec wins and long-term dominance.

Automotive refinish systems

Collision volumes and insurer networks are driving steady demand for turnkey automotive refinish systems in 2024, with body shops favoring integrated products, color tools and training. Sherwin-Williams maintains a meaningful seat at the table through its product set, digital color-matching and technical education, though field technicians, equipment financing and tint inventory remain necessary. Continue pressing partnerships and multi-shop operators as the repair market expands.

Industrial wood and OEM coatings

Furniture, cabinets and building products are rebounding and OEMs are prioritizing throughput and sustainability; Sherwin-Williams’ national scale, color consistency and line-side service give it real share to defend, while growth requires cash for labs, trials and shop-floor conversions.

- Defend: scale and color consistency

- Threat: capital intensity of trials

- Opportunity: double down conversion teams

- Action: fast-sampling to win switches

Latin America architectural coatings

As a BCG Stars entry, Latin America architectural coatings benefit from continued housing formation and a 2024 population near 660 million with urbanization above 80, keeping demand growth steady; Sherwin-Williams leverages strong brand awareness and a mixed store/distributor network to scale share quickly. The business still needs targeted investment in retail footprint, trade credit solutions, and local R&D to capture long-term value before markets mature.

- Growth drivers: 660 million population (2024), urbanization >80%

- Strength: brand + store/distributor leverage

- Gaps: footprint, credit, local innovation

- Strategy: invest to scale now and lock share

Stars scale with $550B infra tail - pro-channel investments create Cash Cows

Pro repaint/construction and industrial capex (U.S. Bipartisan Infrastructure Law ~550 billion new spending) keep Stars growing; strong pro channel share and contractor stickiness sustain pricing power. These segments demand heavy cash for new stores, last-mile delivery, specs and certification. Targeted investments in coverage, trade credit and conversion teams should convert Stars into future Cash Cows.

| Metric | Value |

|---|---|

| U.S. infra new spend (2024) | $550B |

| LatAm pop (2024) | 660M |

What is included in the product

Clear BCG Matrix breakdown of Sherwin-Williams products—Stars, Cash Cows, Question Marks, Dogs—with strategic investment and divestment guidance.

One-page BCG matrix placing Sherwin-Williams units into clear quadrants for faster portfolio decisions.

Cash Cows

U.S. architectural repaint (pro core)

U.S. architectural repaint (Pro Core) is a mature cash cow with recurring demand, high share among contractors and strong loyalty; Sherwin‑Williams reported approximately $22.6 billion in FY2024 net sales, underpining its pro channel strength. Margins remain robust from service, tint accuracy and convenience, supporting gross-margin resilience. Low incremental promotion needs shift focus to ops and delivery efficiency; prioritize improving route density and inventory turns while protecting service SLAs.

Consumer Brands in big-box retail

DIY growth is modest (~low-single-digit annually), but Sherwin-Williams leverages entrenched shelf space and plus-size relationships in big-box channels; company net sales were about $20.9 billion in 2023, with Consumer Brands delivering stable cash flow. Private label and owned brands drive predictable promo cycles and margins, so investments focus on supply-chain efficiency and category management rather than awareness. Maintain assortments, reduce SKU complexity, and harvest cash.

Flagship interior latex lines

Flagship interior latex lines are everyday repaint staples with premium tiers that deliver fat mix, accounting for roughly 25% of Sherwin‑Williams consumer segment volume in FY2024 (company net sales $20.6B). Low innovation burden and color/consistency drive high repeat rates, keeping churn low and lifetime value high. Minimal marketing lift beyond seasonal pushes; margins preserved by SKU rationalization and optimized raw‑material yields, supporting above‑average gross margins.

Traffic-bearing and floor coatings

Traffic-bearing and floor coatings show steady 7–10 year replacement cycles, high spec stickiness (typical retention >80%) and efficient service-call economics; Sherwin‑Williams held an estimated ~25% share of U.S. commercial maintenance coatings in 2024, yielding dependable mid‑teens margins despite limited growth.

- Replacement cycles: 7–10 years

- Spec retention: >80%

- 2024 U.S. commercial maintenance share: ~25%

- Margins: mid‑teens EBITDA

- Priority: application training and bundled systems to reduce churn

Aerosols, sundries, and ancillaries

Aerosols, sundries, and ancillaries are high-attachment cash cows tied to core paint sales with predictable, recurring volumes; Sherwin-Williams reported roughly $21.6 billion in FY2024 net sales, underpinning stable demand for consumables. Mature category needs limited promotion, is cash-positive via scale purchasing, and small sourcing and packaging tweaks can add incremental margin points.

- High attachment to paint sales

- Predictable volumes, low promo need

- Cash-positive via bulk sourcing

- Packaging/sourcing tweaks boost margins

Repaint and DIY cash cows: steady high-margin cash flow ripe for harvest

Sherwin‑Williams cash cows (Pro Core U.S. repaint, DIY consumer lines, interior latex, commercial maintenance, aerosols/ancillaries) deliver steady, high‑margin cash flow with low growth, driven by repeat demand, spec stickiness and service efficiency; company net sales ~22.6B in FY2024, enabling harvest and operational optimization.

| Category | 2024 metric | Margin |

|---|---|---|

| Pro/Pro Core | High share, repeat | Above avg |

| Consumer/DIY | Stable, low‑SDG | Stable |

Delivered as Shown

Sherwin-Williams BCG Matrix

The Sherwin‑Williams BCG Matrix you're previewing is the exact, final file you'll receive after purchase. No watermarks, no placeholders—just a fully formatted strategic matrix ready for use. It’s crafted for clarity so you can present or edit immediately. After checkout the same document is delivered to your inbox—no surprises, no revisions needed.

Visual. Strategic. Downloadable.

Sherwin‑Williams’ BCG Matrix preview shows which paint lines lead the market and which may be draining resources, but it’s only the tip of the iceberg. Get the full BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and clear moves on investment, divestment, or focus. Purchase now and receive a ready-to-use Word report plus a high-level Excel summary—strategic clarity you can present and act on immediately.

Stars

Pro paint stores in The Americas Group

Pro repaint and construction cycles drive high store traffic and Sherwin-Williams dominates the pro channel through its dense store network, sustaining market share and contractor relationships.

Share is strong and the service model is sticky, but the segment consumes significant cash for new openings, staffing and last-mile delivery investments.

Maintain investments in geographic coverage, contractor loyalty programs and trade credit to lock the lead; as industry growth normalizes this engine can migrate into Cash Cow status.

Protective & marine coatings for infrastructure

Public and industrial capex is accelerating—U.S. Bipartisan Infrastructure Law alone authorized $1.2 trillion total (about $550 billion in new spending), driving demand for proven protective and marine coatings on bridges, plants and ports. Sherwin-Williams is a leading North American supplier with high regional share; projects are large and technical service differentiates wins. Bid cycles, certification needs and fund-application support require heavy selling effort to secure spec wins and long-term dominance.

Automotive refinish systems

Collision volumes and insurer networks are driving steady demand for turnkey automotive refinish systems in 2024, with body shops favoring integrated products, color tools and training. Sherwin-Williams maintains a meaningful seat at the table through its product set, digital color-matching and technical education, though field technicians, equipment financing and tint inventory remain necessary. Continue pressing partnerships and multi-shop operators as the repair market expands.

Industrial wood and OEM coatings

Furniture, cabinets and building products are rebounding and OEMs are prioritizing throughput and sustainability; Sherwin-Williams’ national scale, color consistency and line-side service give it real share to defend, while growth requires cash for labs, trials and shop-floor conversions.

- Defend: scale and color consistency

- Threat: capital intensity of trials

- Opportunity: double down conversion teams

- Action: fast-sampling to win switches

Latin America architectural coatings

As a BCG Stars entry, Latin America architectural coatings benefit from continued housing formation and a 2024 population near 660 million with urbanization above 80, keeping demand growth steady; Sherwin-Williams leverages strong brand awareness and a mixed store/distributor network to scale share quickly. The business still needs targeted investment in retail footprint, trade credit solutions, and local R&D to capture long-term value before markets mature.

- Growth drivers: 660 million population (2024), urbanization >80%

- Strength: brand + store/distributor leverage

- Gaps: footprint, credit, local innovation

- Strategy: invest to scale now and lock share

Stars scale with $550B infra tail - pro-channel investments create Cash Cows

Pro repaint/construction and industrial capex (U.S. Bipartisan Infrastructure Law ~550 billion new spending) keep Stars growing; strong pro channel share and contractor stickiness sustain pricing power. These segments demand heavy cash for new stores, last-mile delivery, specs and certification. Targeted investments in coverage, trade credit and conversion teams should convert Stars into future Cash Cows.

| Metric | Value |

|---|---|

| U.S. infra new spend (2024) | $550B |

| LatAm pop (2024) | 660M |

What is included in the product

Clear BCG Matrix breakdown of Sherwin-Williams products—Stars, Cash Cows, Question Marks, Dogs—with strategic investment and divestment guidance.

One-page BCG matrix placing Sherwin-Williams units into clear quadrants for faster portfolio decisions.

Cash Cows

U.S. architectural repaint (pro core)

U.S. architectural repaint (Pro Core) is a mature cash cow with recurring demand, high share among contractors and strong loyalty; Sherwin‑Williams reported approximately $22.6 billion in FY2024 net sales, underpining its pro channel strength. Margins remain robust from service, tint accuracy and convenience, supporting gross-margin resilience. Low incremental promotion needs shift focus to ops and delivery efficiency; prioritize improving route density and inventory turns while protecting service SLAs.

Consumer Brands in big-box retail

DIY growth is modest (~low-single-digit annually), but Sherwin-Williams leverages entrenched shelf space and plus-size relationships in big-box channels; company net sales were about $20.9 billion in 2023, with Consumer Brands delivering stable cash flow. Private label and owned brands drive predictable promo cycles and margins, so investments focus on supply-chain efficiency and category management rather than awareness. Maintain assortments, reduce SKU complexity, and harvest cash.

Flagship interior latex lines

Flagship interior latex lines are everyday repaint staples with premium tiers that deliver fat mix, accounting for roughly 25% of Sherwin‑Williams consumer segment volume in FY2024 (company net sales $20.6B). Low innovation burden and color/consistency drive high repeat rates, keeping churn low and lifetime value high. Minimal marketing lift beyond seasonal pushes; margins preserved by SKU rationalization and optimized raw‑material yields, supporting above‑average gross margins.

Traffic-bearing and floor coatings

Traffic-bearing and floor coatings show steady 7–10 year replacement cycles, high spec stickiness (typical retention >80%) and efficient service-call economics; Sherwin‑Williams held an estimated ~25% share of U.S. commercial maintenance coatings in 2024, yielding dependable mid‑teens margins despite limited growth.

- Replacement cycles: 7–10 years

- Spec retention: >80%

- 2024 U.S. commercial maintenance share: ~25%

- Margins: mid‑teens EBITDA

- Priority: application training and bundled systems to reduce churn

Aerosols, sundries, and ancillaries

Aerosols, sundries, and ancillaries are high-attachment cash cows tied to core paint sales with predictable, recurring volumes; Sherwin-Williams reported roughly $21.6 billion in FY2024 net sales, underpinning stable demand for consumables. Mature category needs limited promotion, is cash-positive via scale purchasing, and small sourcing and packaging tweaks can add incremental margin points.

- High attachment to paint sales

- Predictable volumes, low promo need

- Cash-positive via bulk sourcing

- Packaging/sourcing tweaks boost margins

Repaint and DIY cash cows: steady high-margin cash flow ripe for harvest

Sherwin‑Williams cash cows (Pro Core U.S. repaint, DIY consumer lines, interior latex, commercial maintenance, aerosols/ancillaries) deliver steady, high‑margin cash flow with low growth, driven by repeat demand, spec stickiness and service efficiency; company net sales ~22.6B in FY2024, enabling harvest and operational optimization.

| Category | 2024 metric | Margin |

|---|---|---|

| Pro/Pro Core | High share, repeat | Above avg |

| Consumer/DIY | Stable, low‑SDG | Stable |

Delivered as Shown

Sherwin-Williams BCG Matrix

The Sherwin‑Williams BCG Matrix you're previewing is the exact, final file you'll receive after purchase. No watermarks, no placeholders—just a fully formatted strategic matrix ready for use. It’s crafted for clarity so you can present or edit immediately. After checkout the same document is delivered to your inbox—no surprises, no revisions needed.

Description

Visual. Strategic. Downloadable.

Sherwin‑Williams’ BCG Matrix preview shows which paint lines lead the market and which may be draining resources, but it’s only the tip of the iceberg. Get the full BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and clear moves on investment, divestment, or focus. Purchase now and receive a ready-to-use Word report plus a high-level Excel summary—strategic clarity you can present and act on immediately.

Stars

Pro paint stores in The Americas Group

Pro repaint and construction cycles drive high store traffic and Sherwin-Williams dominates the pro channel through its dense store network, sustaining market share and contractor relationships.

Share is strong and the service model is sticky, but the segment consumes significant cash for new openings, staffing and last-mile delivery investments.

Maintain investments in geographic coverage, contractor loyalty programs and trade credit to lock the lead; as industry growth normalizes this engine can migrate into Cash Cow status.

Protective & marine coatings for infrastructure

Public and industrial capex is accelerating—U.S. Bipartisan Infrastructure Law alone authorized $1.2 trillion total (about $550 billion in new spending), driving demand for proven protective and marine coatings on bridges, plants and ports. Sherwin-Williams is a leading North American supplier with high regional share; projects are large and technical service differentiates wins. Bid cycles, certification needs and fund-application support require heavy selling effort to secure spec wins and long-term dominance.

Automotive refinish systems

Collision volumes and insurer networks are driving steady demand for turnkey automotive refinish systems in 2024, with body shops favoring integrated products, color tools and training. Sherwin-Williams maintains a meaningful seat at the table through its product set, digital color-matching and technical education, though field technicians, equipment financing and tint inventory remain necessary. Continue pressing partnerships and multi-shop operators as the repair market expands.

Industrial wood and OEM coatings

Furniture, cabinets and building products are rebounding and OEMs are prioritizing throughput and sustainability; Sherwin-Williams’ national scale, color consistency and line-side service give it real share to defend, while growth requires cash for labs, trials and shop-floor conversions.

- Defend: scale and color consistency

- Threat: capital intensity of trials

- Opportunity: double down conversion teams

- Action: fast-sampling to win switches

Latin America architectural coatings

As a BCG Stars entry, Latin America architectural coatings benefit from continued housing formation and a 2024 population near 660 million with urbanization above 80, keeping demand growth steady; Sherwin-Williams leverages strong brand awareness and a mixed store/distributor network to scale share quickly. The business still needs targeted investment in retail footprint, trade credit solutions, and local R&D to capture long-term value before markets mature.

- Growth drivers: 660 million population (2024), urbanization >80%

- Strength: brand + store/distributor leverage

- Gaps: footprint, credit, local innovation

- Strategy: invest to scale now and lock share

Stars scale with $550B infra tail - pro-channel investments create Cash Cows

Pro repaint/construction and industrial capex (U.S. Bipartisan Infrastructure Law ~550 billion new spending) keep Stars growing; strong pro channel share and contractor stickiness sustain pricing power. These segments demand heavy cash for new stores, last-mile delivery, specs and certification. Targeted investments in coverage, trade credit and conversion teams should convert Stars into future Cash Cows.

| Metric | Value |

|---|---|

| U.S. infra new spend (2024) | $550B |

| LatAm pop (2024) | 660M |

What is included in the product

Clear BCG Matrix breakdown of Sherwin-Williams products—Stars, Cash Cows, Question Marks, Dogs—with strategic investment and divestment guidance.

One-page BCG matrix placing Sherwin-Williams units into clear quadrants for faster portfolio decisions.

Cash Cows

U.S. architectural repaint (pro core)

U.S. architectural repaint (Pro Core) is a mature cash cow with recurring demand, high share among contractors and strong loyalty; Sherwin‑Williams reported approximately $22.6 billion in FY2024 net sales, underpining its pro channel strength. Margins remain robust from service, tint accuracy and convenience, supporting gross-margin resilience. Low incremental promotion needs shift focus to ops and delivery efficiency; prioritize improving route density and inventory turns while protecting service SLAs.

Consumer Brands in big-box retail

DIY growth is modest (~low-single-digit annually), but Sherwin-Williams leverages entrenched shelf space and plus-size relationships in big-box channels; company net sales were about $20.9 billion in 2023, with Consumer Brands delivering stable cash flow. Private label and owned brands drive predictable promo cycles and margins, so investments focus on supply-chain efficiency and category management rather than awareness. Maintain assortments, reduce SKU complexity, and harvest cash.

Flagship interior latex lines

Flagship interior latex lines are everyday repaint staples with premium tiers that deliver fat mix, accounting for roughly 25% of Sherwin‑Williams consumer segment volume in FY2024 (company net sales $20.6B). Low innovation burden and color/consistency drive high repeat rates, keeping churn low and lifetime value high. Minimal marketing lift beyond seasonal pushes; margins preserved by SKU rationalization and optimized raw‑material yields, supporting above‑average gross margins.

Traffic-bearing and floor coatings

Traffic-bearing and floor coatings show steady 7–10 year replacement cycles, high spec stickiness (typical retention >80%) and efficient service-call economics; Sherwin‑Williams held an estimated ~25% share of U.S. commercial maintenance coatings in 2024, yielding dependable mid‑teens margins despite limited growth.

- Replacement cycles: 7–10 years

- Spec retention: >80%

- 2024 U.S. commercial maintenance share: ~25%

- Margins: mid‑teens EBITDA

- Priority: application training and bundled systems to reduce churn

Aerosols, sundries, and ancillaries

Aerosols, sundries, and ancillaries are high-attachment cash cows tied to core paint sales with predictable, recurring volumes; Sherwin-Williams reported roughly $21.6 billion in FY2024 net sales, underpinning stable demand for consumables. Mature category needs limited promotion, is cash-positive via scale purchasing, and small sourcing and packaging tweaks can add incremental margin points.

- High attachment to paint sales

- Predictable volumes, low promo need

- Cash-positive via bulk sourcing

- Packaging/sourcing tweaks boost margins

Repaint and DIY cash cows: steady high-margin cash flow ripe for harvest

Sherwin‑Williams cash cows (Pro Core U.S. repaint, DIY consumer lines, interior latex, commercial maintenance, aerosols/ancillaries) deliver steady, high‑margin cash flow with low growth, driven by repeat demand, spec stickiness and service efficiency; company net sales ~22.6B in FY2024, enabling harvest and operational optimization.

| Category | 2024 metric | Margin |

|---|---|---|

| Pro/Pro Core | High share, repeat | Above avg |

| Consumer/DIY | Stable, low‑SDG | Stable |

Delivered as Shown

Sherwin-Williams BCG Matrix

The Sherwin‑Williams BCG Matrix you're previewing is the exact, final file you'll receive after purchase. No watermarks, no placeholders—just a fully formatted strategic matrix ready for use. It’s crafted for clarity so you can present or edit immediately. After checkout the same document is delivered to your inbox—no surprises, no revisions needed.