Sumitomo Heavy Industries Porter's Five Forces Analysis

From Overview to Strategy Blueprint

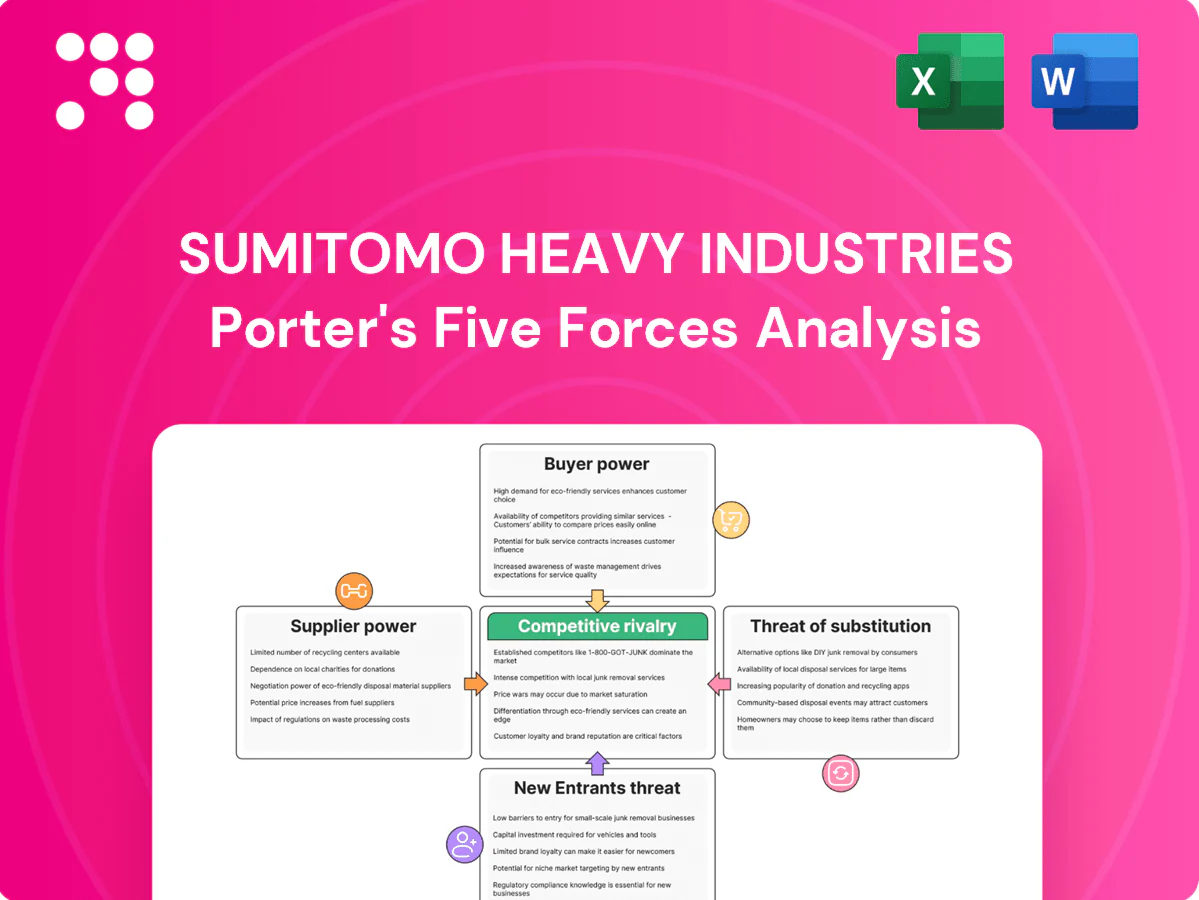

Sumitomo Heavy Industries faces intense industry rivalry driven by global shipbuilding, industrial machinery, and energy markets, with moderate supplier leverage but rising buyer sophistication and cost pressure. Threats from substitutes and new entrants vary by division, while high capital intensity and regulatory barriers provide some protection. This snapshot highlights strategic hotspots and risk vectors. Unlock the full Porter's Five Forces Analysis for a detailed, actionable breakdown tailored to Sumitomo Heavy Industries.

Suppliers Bargaining Power

Specialized component dependency

Sumitomo Heavy Industries depends on niche suppliers for precision bearings, power electronics, hydraulics and specialty alloys, creating reliance on a small pool of qualified vendors. Long, costly qualification cycles raise switching frictions and amplify supplier leverage. Recent supplier consolidation in these critical categories further concentrates bargaining power, limiting SHI’s procurement flexibility and cost negotiation room.

Commodity input volatility

Steel, copper and energy price swings—with LME copper and Brent crude showing double-digit volatility in 2024—can compress SMI margins if costs cannot be passed through. Long-term supply contracts and hedging reduced but did not eliminate exposure, leaving residual mark-to-market risk. Global sourcing arbitrages input cost differences but raises logistics and lead-time risk, while index-linked pricing in some contracts partially rebalances supplier power.

Dual-sourcing and localization

Sumitomo Heavy Industries leverages diversified global operations to implement multi-vendor strategies that dilute supplier control and reduce dependency on single sources. Localizing key components near factories shortens lead times and weakens bargaining leverage of distant vendors. Technical equivalence and certification requirements, however, constrain interchangeability. Geopolitical tensions can further narrow viable local supplier options.

Aftermarket parts influence

OEM-spec spares for installed Sumitomo equipment secure approved suppliers durable revenue and leverage, as 2024 industry estimates place aftermarket parts at roughly 25% of lifecycle revenue; customers insist on OEM-quality spares, anchoring supplier selection. Sumitomo can standardize components to broaden supplier pools and reduce supplier leverage, while SLAs convert price talks into performance-based negotiations.

- OEM-revenue: durable supplier rents

- Customer-expectation: OEM-quality anchors choice

- Standardization: expands supplier pool, lowers leverage

- SLA: shifts to performance-based terms

Technology co-development

Joint R&D with key suppliers embeds proprietary interfaces that raise mutual dependence, securing priority component allocation and clarified cost roadmaps for Sumitomo Heavy Industries while increasing lock-in and switching costs. IP ownership and exclusivity clauses in co-development agreements materially shape supplier leverage. Structured VAVE programs can rebalance cost-sharing and reduce supplier bargaining power.

- Joint R&D: embeds proprietary interfaces

- IP terms: determine supplier leverage

- VAVE: tool to realign costs

Concentrated suppliers and volatile commodities erode margins despite hedges and localization

Sumitomo Heavy Industries faces concentrated, qualified suppliers for bearings, power electronics and alloys, raising switching costs and supplier leverage. Commodity swings eroded margins in 2024 (LME copper ±15%, Brent ±20%) despite hedging and long-term contracts. Diversified sourcing, localization and joint R&D/VAVE partially mitigate but do not eliminate supplier power.

| Metric | 2024 |

|---|---|

| Aftermarket share of lifecycle revenue | 25% |

| LME copper volatility | ±15% |

| Brent crude volatility | ±20% |

What is included in the product

Tailored Porter’s Five Forces analysis of Sumitomo Heavy Industries uncovers competitive intensity, supplier and buyer leverage, threat of substitutes and new entrants, and identifies industry-specific disruptive threats and strategic barriers protecting incumbency to inform pricing, profitability and strategic planning.

A concise, one-sheet Porter's Five Forces for Sumitomo Heavy Industries — customizable pressure levels, spider chart visualization, and clean layout ready for decks, dashboards or boardroom decisions.

Customers Bargaining Power

Large, sophisticated buyers

Shipyards, EPCs, utilities and industrial majors buy via formal tenders with stringent technical specs, driving suppliers to meet tight compliance and warranty standards. Professional procurement teams press for lower prices and tougher payment/penalty terms, using global competitive benchmarking to increase transparency across OEMs. Multi-year framework agreements commonly secure volume-for-discount deals, typically yielding 5–10% price reductions in 2024 procurement practice.

High switching costs

Installed-base integration, operator training and spare-parts ecosystems create strong lock-in for Sumitomo Heavy Industries; OEM aftersales and spare parts represent roughly 20–40% of lifecycle revenue (2024 S&P Global/Margins data). Downtime risk and re-certification deter switching despite price incentives—unplanned downtime can cost ~260,000 USD/hour (2024 ARC Advisory Group). Digital monitoring and proprietary controls, with predictive-maintenance cutting downtime up to ~40% (2024 Deloitte), further increase customer stickiness, tempering buyer power post-installation.

Lifecycle value focus

Buyers at Sumitomo Heavy Industries increasingly optimize total cost of ownership, weighing energy efficiency and uptime; McKinsey (2024) finds digital solutions can cut downtime 20–50% and maintenance costs 10–40%, shifting negotiations beyond upfront price via performance guarantees and outcome contracts. Predictive maintenance and remote support enable 5–15% premium pricing when clear ROI cases reduce pure price bargaining.

Segment variability

Commoditized gearboxes and standard machinery face high price sensitivity as buyers compare multiple suppliers, driving margin pressure for Sumitomo Heavy Industries in commodity segments.

Custom engineered systems and environmental solutions have lower comparability and reduced buyer power; regional public-sector contracts often prioritize regulatory compliance and lifecycle performance over lowest bid, while cyclical construction downturns amplify discount demands.

Alternative procurement channels

Alternative procurement channels in 2024—rental fleets, used equipment, and remanufactured parts—expanded buyer options and intensified price pressure on Sumitomo Heavy Industries new-equipment sales. Sumitomo’s certified reman program and in-house financing help recapture value and protect margins. Bundled service contracts reduce leakage to third-party channels.

- 2024 trend: greater buyer choice from rentals/used/reman

- Certified reman + financing: recapture resale value

- Bundled service contracts: lower third-party churn

Tenders cut 5-10%; aftersales 20-40%

Buyers exert strong pre-sale price pressure via formal tenders and procurement teams, yielding typical 5–10% price reductions in 2024; installed-base lock-in (aftersales 20–40% lifecycle revenue) and predictive maintenance (reduces downtime ~20–40%) limit post-sale switching. Commoditized lines face high price sensitivity; reman/rental options expanded buyer choice in 2024.

| Metric | 2024 Value |

|---|---|

| Price reduction in tenders | 5–10% |

| Aftersales share | 20–40% |

| Downtime cost reduction (predictive) | 20–40% |

| Premium for digital/outscome contracts | 5–15% |

Preview the Actual Deliverable

Sumitomo Heavy Industries Porter's Five Forces Analysis

This preview is the exact Porter’s Five Forces analysis of Sumitomo Heavy Industries you’ll receive—no placeholders or samples. Once purchased, you get immediate access to this fully formatted, ready-to-use document. It contains professional insights on competitive rivalry, buyer/supplier power, threats of entry/substitution.

From Overview to Strategy Blueprint

Sumitomo Heavy Industries faces intense industry rivalry driven by global shipbuilding, industrial machinery, and energy markets, with moderate supplier leverage but rising buyer sophistication and cost pressure. Threats from substitutes and new entrants vary by division, while high capital intensity and regulatory barriers provide some protection. This snapshot highlights strategic hotspots and risk vectors. Unlock the full Porter's Five Forces Analysis for a detailed, actionable breakdown tailored to Sumitomo Heavy Industries.

Suppliers Bargaining Power

Specialized component dependency

Sumitomo Heavy Industries depends on niche suppliers for precision bearings, power electronics, hydraulics and specialty alloys, creating reliance on a small pool of qualified vendors. Long, costly qualification cycles raise switching frictions and amplify supplier leverage. Recent supplier consolidation in these critical categories further concentrates bargaining power, limiting SHI’s procurement flexibility and cost negotiation room.

Commodity input volatility

Steel, copper and energy price swings—with LME copper and Brent crude showing double-digit volatility in 2024—can compress SMI margins if costs cannot be passed through. Long-term supply contracts and hedging reduced but did not eliminate exposure, leaving residual mark-to-market risk. Global sourcing arbitrages input cost differences but raises logistics and lead-time risk, while index-linked pricing in some contracts partially rebalances supplier power.

Dual-sourcing and localization

Sumitomo Heavy Industries leverages diversified global operations to implement multi-vendor strategies that dilute supplier control and reduce dependency on single sources. Localizing key components near factories shortens lead times and weakens bargaining leverage of distant vendors. Technical equivalence and certification requirements, however, constrain interchangeability. Geopolitical tensions can further narrow viable local supplier options.

Aftermarket parts influence

OEM-spec spares for installed Sumitomo equipment secure approved suppliers durable revenue and leverage, as 2024 industry estimates place aftermarket parts at roughly 25% of lifecycle revenue; customers insist on OEM-quality spares, anchoring supplier selection. Sumitomo can standardize components to broaden supplier pools and reduce supplier leverage, while SLAs convert price talks into performance-based negotiations.

- OEM-revenue: durable supplier rents

- Customer-expectation: OEM-quality anchors choice

- Standardization: expands supplier pool, lowers leverage

- SLA: shifts to performance-based terms

Technology co-development

Joint R&D with key suppliers embeds proprietary interfaces that raise mutual dependence, securing priority component allocation and clarified cost roadmaps for Sumitomo Heavy Industries while increasing lock-in and switching costs. IP ownership and exclusivity clauses in co-development agreements materially shape supplier leverage. Structured VAVE programs can rebalance cost-sharing and reduce supplier bargaining power.

- Joint R&D: embeds proprietary interfaces

- IP terms: determine supplier leverage

- VAVE: tool to realign costs

Concentrated suppliers and volatile commodities erode margins despite hedges and localization

Sumitomo Heavy Industries faces concentrated, qualified suppliers for bearings, power electronics and alloys, raising switching costs and supplier leverage. Commodity swings eroded margins in 2024 (LME copper ±15%, Brent ±20%) despite hedging and long-term contracts. Diversified sourcing, localization and joint R&D/VAVE partially mitigate but do not eliminate supplier power.

| Metric | 2024 |

|---|---|

| Aftermarket share of lifecycle revenue | 25% |

| LME copper volatility | ±15% |

| Brent crude volatility | ±20% |

What is included in the product

Tailored Porter’s Five Forces analysis of Sumitomo Heavy Industries uncovers competitive intensity, supplier and buyer leverage, threat of substitutes and new entrants, and identifies industry-specific disruptive threats and strategic barriers protecting incumbency to inform pricing, profitability and strategic planning.

A concise, one-sheet Porter's Five Forces for Sumitomo Heavy Industries — customizable pressure levels, spider chart visualization, and clean layout ready for decks, dashboards or boardroom decisions.

Customers Bargaining Power

Large, sophisticated buyers

Shipyards, EPCs, utilities and industrial majors buy via formal tenders with stringent technical specs, driving suppliers to meet tight compliance and warranty standards. Professional procurement teams press for lower prices and tougher payment/penalty terms, using global competitive benchmarking to increase transparency across OEMs. Multi-year framework agreements commonly secure volume-for-discount deals, typically yielding 5–10% price reductions in 2024 procurement practice.

High switching costs

Installed-base integration, operator training and spare-parts ecosystems create strong lock-in for Sumitomo Heavy Industries; OEM aftersales and spare parts represent roughly 20–40% of lifecycle revenue (2024 S&P Global/Margins data). Downtime risk and re-certification deter switching despite price incentives—unplanned downtime can cost ~260,000 USD/hour (2024 ARC Advisory Group). Digital monitoring and proprietary controls, with predictive-maintenance cutting downtime up to ~40% (2024 Deloitte), further increase customer stickiness, tempering buyer power post-installation.

Lifecycle value focus

Buyers at Sumitomo Heavy Industries increasingly optimize total cost of ownership, weighing energy efficiency and uptime; McKinsey (2024) finds digital solutions can cut downtime 20–50% and maintenance costs 10–40%, shifting negotiations beyond upfront price via performance guarantees and outcome contracts. Predictive maintenance and remote support enable 5–15% premium pricing when clear ROI cases reduce pure price bargaining.

Segment variability

Commoditized gearboxes and standard machinery face high price sensitivity as buyers compare multiple suppliers, driving margin pressure for Sumitomo Heavy Industries in commodity segments.

Custom engineered systems and environmental solutions have lower comparability and reduced buyer power; regional public-sector contracts often prioritize regulatory compliance and lifecycle performance over lowest bid, while cyclical construction downturns amplify discount demands.

Alternative procurement channels

Alternative procurement channels in 2024—rental fleets, used equipment, and remanufactured parts—expanded buyer options and intensified price pressure on Sumitomo Heavy Industries new-equipment sales. Sumitomo’s certified reman program and in-house financing help recapture value and protect margins. Bundled service contracts reduce leakage to third-party channels.

- 2024 trend: greater buyer choice from rentals/used/reman

- Certified reman + financing: recapture resale value

- Bundled service contracts: lower third-party churn

Tenders cut 5-10%; aftersales 20-40%

Buyers exert strong pre-sale price pressure via formal tenders and procurement teams, yielding typical 5–10% price reductions in 2024; installed-base lock-in (aftersales 20–40% lifecycle revenue) and predictive maintenance (reduces downtime ~20–40%) limit post-sale switching. Commoditized lines face high price sensitivity; reman/rental options expanded buyer choice in 2024.

| Metric | 2024 Value |

|---|---|

| Price reduction in tenders | 5–10% |

| Aftersales share | 20–40% |

| Downtime cost reduction (predictive) | 20–40% |

| Premium for digital/outscome contracts | 5–15% |

Preview the Actual Deliverable

Sumitomo Heavy Industries Porter's Five Forces Analysis

This preview is the exact Porter’s Five Forces analysis of Sumitomo Heavy Industries you’ll receive—no placeholders or samples. Once purchased, you get immediate access to this fully formatted, ready-to-use document. It contains professional insights on competitive rivalry, buyer/supplier power, threats of entry/substitution.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Sumitomo Heavy Industries faces intense industry rivalry driven by global shipbuilding, industrial machinery, and energy markets, with moderate supplier leverage but rising buyer sophistication and cost pressure. Threats from substitutes and new entrants vary by division, while high capital intensity and regulatory barriers provide some protection. This snapshot highlights strategic hotspots and risk vectors. Unlock the full Porter's Five Forces Analysis for a detailed, actionable breakdown tailored to Sumitomo Heavy Industries.

Suppliers Bargaining Power

Specialized component dependency

Sumitomo Heavy Industries depends on niche suppliers for precision bearings, power electronics, hydraulics and specialty alloys, creating reliance on a small pool of qualified vendors. Long, costly qualification cycles raise switching frictions and amplify supplier leverage. Recent supplier consolidation in these critical categories further concentrates bargaining power, limiting SHI’s procurement flexibility and cost negotiation room.

Commodity input volatility

Steel, copper and energy price swings—with LME copper and Brent crude showing double-digit volatility in 2024—can compress SMI margins if costs cannot be passed through. Long-term supply contracts and hedging reduced but did not eliminate exposure, leaving residual mark-to-market risk. Global sourcing arbitrages input cost differences but raises logistics and lead-time risk, while index-linked pricing in some contracts partially rebalances supplier power.

Dual-sourcing and localization

Sumitomo Heavy Industries leverages diversified global operations to implement multi-vendor strategies that dilute supplier control and reduce dependency on single sources. Localizing key components near factories shortens lead times and weakens bargaining leverage of distant vendors. Technical equivalence and certification requirements, however, constrain interchangeability. Geopolitical tensions can further narrow viable local supplier options.

Aftermarket parts influence

OEM-spec spares for installed Sumitomo equipment secure approved suppliers durable revenue and leverage, as 2024 industry estimates place aftermarket parts at roughly 25% of lifecycle revenue; customers insist on OEM-quality spares, anchoring supplier selection. Sumitomo can standardize components to broaden supplier pools and reduce supplier leverage, while SLAs convert price talks into performance-based negotiations.

- OEM-revenue: durable supplier rents

- Customer-expectation: OEM-quality anchors choice

- Standardization: expands supplier pool, lowers leverage

- SLA: shifts to performance-based terms

Technology co-development

Joint R&D with key suppliers embeds proprietary interfaces that raise mutual dependence, securing priority component allocation and clarified cost roadmaps for Sumitomo Heavy Industries while increasing lock-in and switching costs. IP ownership and exclusivity clauses in co-development agreements materially shape supplier leverage. Structured VAVE programs can rebalance cost-sharing and reduce supplier bargaining power.

- Joint R&D: embeds proprietary interfaces

- IP terms: determine supplier leverage

- VAVE: tool to realign costs

Concentrated suppliers and volatile commodities erode margins despite hedges and localization

Sumitomo Heavy Industries faces concentrated, qualified suppliers for bearings, power electronics and alloys, raising switching costs and supplier leverage. Commodity swings eroded margins in 2024 (LME copper ±15%, Brent ±20%) despite hedging and long-term contracts. Diversified sourcing, localization and joint R&D/VAVE partially mitigate but do not eliminate supplier power.

| Metric | 2024 |

|---|---|

| Aftermarket share of lifecycle revenue | 25% |

| LME copper volatility | ±15% |

| Brent crude volatility | ±20% |

What is included in the product

Tailored Porter’s Five Forces analysis of Sumitomo Heavy Industries uncovers competitive intensity, supplier and buyer leverage, threat of substitutes and new entrants, and identifies industry-specific disruptive threats and strategic barriers protecting incumbency to inform pricing, profitability and strategic planning.

A concise, one-sheet Porter's Five Forces for Sumitomo Heavy Industries — customizable pressure levels, spider chart visualization, and clean layout ready for decks, dashboards or boardroom decisions.

Customers Bargaining Power

Large, sophisticated buyers

Shipyards, EPCs, utilities and industrial majors buy via formal tenders with stringent technical specs, driving suppliers to meet tight compliance and warranty standards. Professional procurement teams press for lower prices and tougher payment/penalty terms, using global competitive benchmarking to increase transparency across OEMs. Multi-year framework agreements commonly secure volume-for-discount deals, typically yielding 5–10% price reductions in 2024 procurement practice.

High switching costs

Installed-base integration, operator training and spare-parts ecosystems create strong lock-in for Sumitomo Heavy Industries; OEM aftersales and spare parts represent roughly 20–40% of lifecycle revenue (2024 S&P Global/Margins data). Downtime risk and re-certification deter switching despite price incentives—unplanned downtime can cost ~260,000 USD/hour (2024 ARC Advisory Group). Digital monitoring and proprietary controls, with predictive-maintenance cutting downtime up to ~40% (2024 Deloitte), further increase customer stickiness, tempering buyer power post-installation.

Lifecycle value focus

Buyers at Sumitomo Heavy Industries increasingly optimize total cost of ownership, weighing energy efficiency and uptime; McKinsey (2024) finds digital solutions can cut downtime 20–50% and maintenance costs 10–40%, shifting negotiations beyond upfront price via performance guarantees and outcome contracts. Predictive maintenance and remote support enable 5–15% premium pricing when clear ROI cases reduce pure price bargaining.

Segment variability

Commoditized gearboxes and standard machinery face high price sensitivity as buyers compare multiple suppliers, driving margin pressure for Sumitomo Heavy Industries in commodity segments.

Custom engineered systems and environmental solutions have lower comparability and reduced buyer power; regional public-sector contracts often prioritize regulatory compliance and lifecycle performance over lowest bid, while cyclical construction downturns amplify discount demands.

Alternative procurement channels

Alternative procurement channels in 2024—rental fleets, used equipment, and remanufactured parts—expanded buyer options and intensified price pressure on Sumitomo Heavy Industries new-equipment sales. Sumitomo’s certified reman program and in-house financing help recapture value and protect margins. Bundled service contracts reduce leakage to third-party channels.

- 2024 trend: greater buyer choice from rentals/used/reman

- Certified reman + financing: recapture resale value

- Bundled service contracts: lower third-party churn

Tenders cut 5-10%; aftersales 20-40%

Buyers exert strong pre-sale price pressure via formal tenders and procurement teams, yielding typical 5–10% price reductions in 2024; installed-base lock-in (aftersales 20–40% lifecycle revenue) and predictive maintenance (reduces downtime ~20–40%) limit post-sale switching. Commoditized lines face high price sensitivity; reman/rental options expanded buyer choice in 2024.

| Metric | 2024 Value |

|---|---|

| Price reduction in tenders | 5–10% |

| Aftersales share | 20–40% |

| Downtime cost reduction (predictive) | 20–40% |

| Premium for digital/outscome contracts | 5–15% |

Preview the Actual Deliverable

Sumitomo Heavy Industries Porter's Five Forces Analysis

This preview is the exact Porter’s Five Forces analysis of Sumitomo Heavy Industries you’ll receive—no placeholders or samples. Once purchased, you get immediate access to this fully formatted, ready-to-use document. It contains professional insights on competitive rivalry, buyer/supplier power, threats of entry/substitution.