Shift4 Porter's Five Forces Analysis

From Overview to Strategy Blueprint

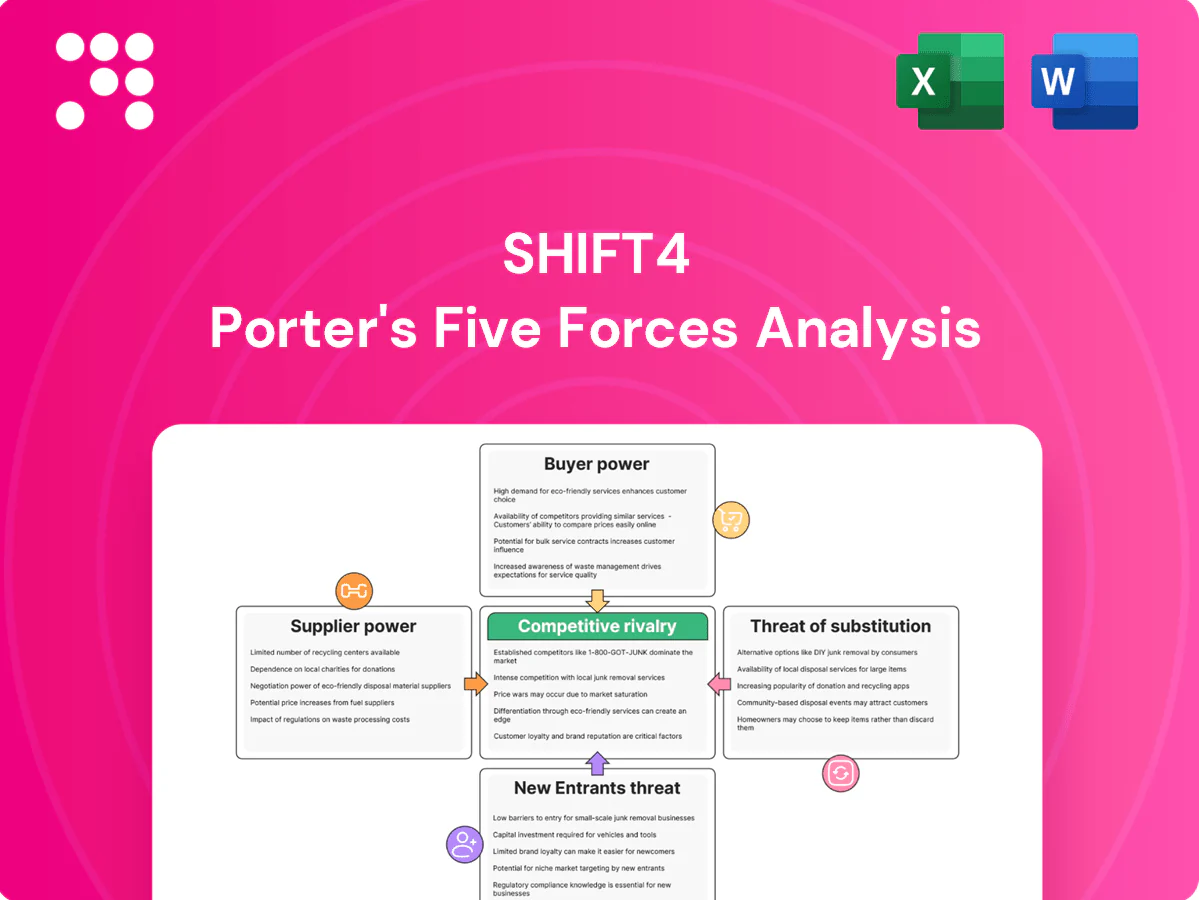

Shift4 faces moderate buyer power, growing substitute threats from fintechs, and scale advantages among incumbents; supplier influence and entry barriers shape its pricing and growth options. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Shift4’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Card networks and issuing banks

Shift4 depends on Visa, Mastercard, American Express and issuing banks for network access and authorization, with Visa and Mastercard together capturing over 80% of U.S. card purchase volume (2023–24), giving these suppliers structural power. Changes in network fees, interchange and rules such as chargeback standards can directly compress merchant margins and Shift4’s processing revenue. Competitive pressure among networks and regulatory transparency measures limit unilateral fee hikes. Long-term certifications and high transaction volumes bolster Shift4’s negotiating leverage with networks and issuers.

Hardware and POS OEMs

Payment terminals, PIN pads and POS peripherals are supplied by a concentrated set of OEMs—Ingenico (now part of Worldline), Verifone and PAX among the largest—creating switching frictions for merchants and processors. Component shortages and lengthy certification cycles routinely delay deployments and raise costs. Shift4 reduces supplier power by offering integrated POS solutions and multi-vendor device support. Vertical integration or proprietary devices can cut dependency but demand significant capital and continuous certification upkeep.

Cloud, data center, and telecom providers

Uptime and latency hinge on cloud/colo and telecom networks, giving suppliers moderate bargaining power since mission-critical options are limited and AWS, Microsoft, Google held roughly 32%, 23%, 10% of IaaS/PaaS market in 2024. Volume commitments and reserved/commit discounts (up to ~72% for long‑term RIs) and multi‑region architectures improve SLAs and pricing. High-profile outages that cost merchants six‑figure hours increase supplier leverage. Diversification and multi‑cloud reduce concentration risk.

ISVs, VARs, and channel partners

Independent software vendors and VARs can command referral fees and integration prioritization, and popular hospitality/retail ISVs often steer transaction volumes, increasing supplier leverage; Shift4 served over 200,000 merchants in 2024, helping mitigate this risk. Shift4’s integrated platform and revenue-sharing arrangements align incentives to reduce dependence, while investing in proprietary software and direct distribution lowers channel power over time.

- ISV/VAR referral fees and prioritization

- Popular ISVs steer volumes

- Shift4 ~200,000 merchants (2024) aids negotiation

- Revenue-share integrations align incentives

- Proprietary software reduces supplier power long-term

Fraud, risk, and data service providers

Third-party tokenization, KYC, AML, and fraud-scoring providers are highly specialized and sticky, with vendor changes typically triggering model re-tuning and recertifications that can take several months and materially raise switching costs; many payments firms report multi-hundred-thousand-dollar integration expenses. Consolidation or building in-house risk capabilities reduces supplier power, while data partnerships and volume can be leveraged for better pricing and fraud-improvement margins.

- sticky integration

- recertification delays

- high switching costs

- consolidation lowers fees

- data scale = pricing leverage

Networks >80% U.S. volume; cloud 32% IaaS; acquirer ~200k merchants

Suppliers (networks, terminals, cloud, ISVs, fraud vendors) exert moderate-to-high power: Visa/Mastercard >80% U.S. volume (2023–24) and top cloud providers hold ~32%/23%/10% (AWS/Microsoft/Google, 2024). Certification, certification delays and switching costs raise stickiness. Shift4 scale (~200,000 merchants, 2024), integrated stack and revenue-share deals materially reduce supplier leverage.

| Supplier | Metric | 2024 Data |

|---|---|---|

| Card networks | Market share | >80% (Visa+MC) |

| Cloud | IaaS share | AWS 32%/MSFT 23%/GCP 10% |

| Merchants | Shift4 scale | ~200,000 |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively for Shift4; detailed assessment of supplier and buyer power, substitutes, and rivalry identifies disruptive forces and barriers protecting incumbents. Fully editable for reports, decks, and investor materials.

A one-sheet Porter's Five Forces for Shift4 that turns complex competitive dynamics into a clear, customizable radar—perfect for quick boardroom decisions and easy integration into decks or dashboards.

Customers Bargaining Power

Enterprise hospitality and retail chains

Large multi-site hospitality and retail chains negotiate aggressively on pricing and service, leveraging centralized RFPs and volume concentration to extract concessions across a $7.94 trillion U.S. retail and food services market in 2023.

Shift4 offsets pure price focus with end-to-end integration, value-added services and customized SLAs that align with enterprise operational KPIs.

Multi-year (commonly 3–5 year) contracts and bespoke integrations materially raise switching costs, reducing churn risk and preserving margin.

SMBs in restaurant and specialty retail

SMBs in restaurant and specialty retail are highly price sensitive yet face notable switching frictions from POS setup and staff training; National Restaurant Association data show 98% of US restaurants are small businesses (2024), concentrating this demand. Shift4’s bundled POS, gateway, and support lowers appeal of multi-vendor mixes, though month-to-month competitor offers can raise churn risk. Focused education on total cost of ownership and reliability preserves Shift4’s margin.

Vertical feature requirements

Buyers demand vertical features like tableside payment, tokenized card-on-file and omni-channel, and when these are must-haves they can push product roadmaps and timelines. Shift4’s purpose-built hospitality stack—serving over 200,000 merchants—narrows credible alternatives and reduces buyer leverage. Deep PMS/POS integrations increase switching costs, often translating to months of redevelopment and lost operational continuity.

Switching costs and contract terms

Data migration, PCI scope changes and staff re-training create meaningful switching costs for Shift4; 2024 industry estimates put merchant migrations at roughly $10,000–$100,000 in direct costs and weeks-months of downtime risk. Early termination fees and device lock-in further reduce buyer power, though aggressive competitor buyouts can neutralize frictions. Transparent pricing and performance guarantees help Shift4 retain clients without deep discounting.

- Data migration cost range: $10k–$100k (2024 industry estimate)

- PCI scope reduction increases lock-in

- ETFs and device lock-in lower buyer power

- Buyout offers can counteract switching frictions

Price transparency and pass-through fees

Centralized RFPs target $7.94T US retail & food market; SMBs price-sensitive

Large chains drive hard bargains via centralized RFPs across a $7.94 trillion US retail & food services market (2023). Shift4 counters with end-to-end integration, multi-year contracts and PMS/POS lock-in raising switching costs. SMBs remain price-sensitive (98% of US restaurants are small businesses, 2024) while processor markups run 0.10%–0.50% (2024).

| Metric | Value |

|---|---|

| US retail & food services | $7.94T (2023) |

| US restaurants small biz | 98% (2024) |

| Processor markup | 0.10%–0.50% (2024) |

Full Version Awaits

Shift4 Porter's Five Forces Analysis

This preview shows the exact Shift4 Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is the full, professionally formatted report, ready to download and use the moment you buy. You’ll get instant access to this exact file with no surprises.

From Overview to Strategy Blueprint

Shift4 faces moderate buyer power, growing substitute threats from fintechs, and scale advantages among incumbents; supplier influence and entry barriers shape its pricing and growth options. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Shift4’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Card networks and issuing banks

Shift4 depends on Visa, Mastercard, American Express and issuing banks for network access and authorization, with Visa and Mastercard together capturing over 80% of U.S. card purchase volume (2023–24), giving these suppliers structural power. Changes in network fees, interchange and rules such as chargeback standards can directly compress merchant margins and Shift4’s processing revenue. Competitive pressure among networks and regulatory transparency measures limit unilateral fee hikes. Long-term certifications and high transaction volumes bolster Shift4’s negotiating leverage with networks and issuers.

Hardware and POS OEMs

Payment terminals, PIN pads and POS peripherals are supplied by a concentrated set of OEMs—Ingenico (now part of Worldline), Verifone and PAX among the largest—creating switching frictions for merchants and processors. Component shortages and lengthy certification cycles routinely delay deployments and raise costs. Shift4 reduces supplier power by offering integrated POS solutions and multi-vendor device support. Vertical integration or proprietary devices can cut dependency but demand significant capital and continuous certification upkeep.

Cloud, data center, and telecom providers

Uptime and latency hinge on cloud/colo and telecom networks, giving suppliers moderate bargaining power since mission-critical options are limited and AWS, Microsoft, Google held roughly 32%, 23%, 10% of IaaS/PaaS market in 2024. Volume commitments and reserved/commit discounts (up to ~72% for long‑term RIs) and multi‑region architectures improve SLAs and pricing. High-profile outages that cost merchants six‑figure hours increase supplier leverage. Diversification and multi‑cloud reduce concentration risk.

ISVs, VARs, and channel partners

Independent software vendors and VARs can command referral fees and integration prioritization, and popular hospitality/retail ISVs often steer transaction volumes, increasing supplier leverage; Shift4 served over 200,000 merchants in 2024, helping mitigate this risk. Shift4’s integrated platform and revenue-sharing arrangements align incentives to reduce dependence, while investing in proprietary software and direct distribution lowers channel power over time.

- ISV/VAR referral fees and prioritization

- Popular ISVs steer volumes

- Shift4 ~200,000 merchants (2024) aids negotiation

- Revenue-share integrations align incentives

- Proprietary software reduces supplier power long-term

Fraud, risk, and data service providers

Third-party tokenization, KYC, AML, and fraud-scoring providers are highly specialized and sticky, with vendor changes typically triggering model re-tuning and recertifications that can take several months and materially raise switching costs; many payments firms report multi-hundred-thousand-dollar integration expenses. Consolidation or building in-house risk capabilities reduces supplier power, while data partnerships and volume can be leveraged for better pricing and fraud-improvement margins.

- sticky integration

- recertification delays

- high switching costs

- consolidation lowers fees

- data scale = pricing leverage

Networks >80% U.S. volume; cloud 32% IaaS; acquirer ~200k merchants

Suppliers (networks, terminals, cloud, ISVs, fraud vendors) exert moderate-to-high power: Visa/Mastercard >80% U.S. volume (2023–24) and top cloud providers hold ~32%/23%/10% (AWS/Microsoft/Google, 2024). Certification, certification delays and switching costs raise stickiness. Shift4 scale (~200,000 merchants, 2024), integrated stack and revenue-share deals materially reduce supplier leverage.

| Supplier | Metric | 2024 Data |

|---|---|---|

| Card networks | Market share | >80% (Visa+MC) |

| Cloud | IaaS share | AWS 32%/MSFT 23%/GCP 10% |

| Merchants | Shift4 scale | ~200,000 |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively for Shift4; detailed assessment of supplier and buyer power, substitutes, and rivalry identifies disruptive forces and barriers protecting incumbents. Fully editable for reports, decks, and investor materials.

A one-sheet Porter's Five Forces for Shift4 that turns complex competitive dynamics into a clear, customizable radar—perfect for quick boardroom decisions and easy integration into decks or dashboards.

Customers Bargaining Power

Enterprise hospitality and retail chains

Large multi-site hospitality and retail chains negotiate aggressively on pricing and service, leveraging centralized RFPs and volume concentration to extract concessions across a $7.94 trillion U.S. retail and food services market in 2023.

Shift4 offsets pure price focus with end-to-end integration, value-added services and customized SLAs that align with enterprise operational KPIs.

Multi-year (commonly 3–5 year) contracts and bespoke integrations materially raise switching costs, reducing churn risk and preserving margin.

SMBs in restaurant and specialty retail

SMBs in restaurant and specialty retail are highly price sensitive yet face notable switching frictions from POS setup and staff training; National Restaurant Association data show 98% of US restaurants are small businesses (2024), concentrating this demand. Shift4’s bundled POS, gateway, and support lowers appeal of multi-vendor mixes, though month-to-month competitor offers can raise churn risk. Focused education on total cost of ownership and reliability preserves Shift4’s margin.

Vertical feature requirements

Buyers demand vertical features like tableside payment, tokenized card-on-file and omni-channel, and when these are must-haves they can push product roadmaps and timelines. Shift4’s purpose-built hospitality stack—serving over 200,000 merchants—narrows credible alternatives and reduces buyer leverage. Deep PMS/POS integrations increase switching costs, often translating to months of redevelopment and lost operational continuity.

Switching costs and contract terms

Data migration, PCI scope changes and staff re-training create meaningful switching costs for Shift4; 2024 industry estimates put merchant migrations at roughly $10,000–$100,000 in direct costs and weeks-months of downtime risk. Early termination fees and device lock-in further reduce buyer power, though aggressive competitor buyouts can neutralize frictions. Transparent pricing and performance guarantees help Shift4 retain clients without deep discounting.

- Data migration cost range: $10k–$100k (2024 industry estimate)

- PCI scope reduction increases lock-in

- ETFs and device lock-in lower buyer power

- Buyout offers can counteract switching frictions

Price transparency and pass-through fees

Centralized RFPs target $7.94T US retail & food market; SMBs price-sensitive

Large chains drive hard bargains via centralized RFPs across a $7.94 trillion US retail & food services market (2023). Shift4 counters with end-to-end integration, multi-year contracts and PMS/POS lock-in raising switching costs. SMBs remain price-sensitive (98% of US restaurants are small businesses, 2024) while processor markups run 0.10%–0.50% (2024).

| Metric | Value |

|---|---|

| US retail & food services | $7.94T (2023) |

| US restaurants small biz | 98% (2024) |

| Processor markup | 0.10%–0.50% (2024) |

Full Version Awaits

Shift4 Porter's Five Forces Analysis

This preview shows the exact Shift4 Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is the full, professionally formatted report, ready to download and use the moment you buy. You’ll get instant access to this exact file with no surprises.

Description

From Overview to Strategy Blueprint

Shift4 faces moderate buyer power, growing substitute threats from fintechs, and scale advantages among incumbents; supplier influence and entry barriers shape its pricing and growth options. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Shift4’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Card networks and issuing banks

Shift4 depends on Visa, Mastercard, American Express and issuing banks for network access and authorization, with Visa and Mastercard together capturing over 80% of U.S. card purchase volume (2023–24), giving these suppliers structural power. Changes in network fees, interchange and rules such as chargeback standards can directly compress merchant margins and Shift4’s processing revenue. Competitive pressure among networks and regulatory transparency measures limit unilateral fee hikes. Long-term certifications and high transaction volumes bolster Shift4’s negotiating leverage with networks and issuers.

Hardware and POS OEMs

Payment terminals, PIN pads and POS peripherals are supplied by a concentrated set of OEMs—Ingenico (now part of Worldline), Verifone and PAX among the largest—creating switching frictions for merchants and processors. Component shortages and lengthy certification cycles routinely delay deployments and raise costs. Shift4 reduces supplier power by offering integrated POS solutions and multi-vendor device support. Vertical integration or proprietary devices can cut dependency but demand significant capital and continuous certification upkeep.

Cloud, data center, and telecom providers

Uptime and latency hinge on cloud/colo and telecom networks, giving suppliers moderate bargaining power since mission-critical options are limited and AWS, Microsoft, Google held roughly 32%, 23%, 10% of IaaS/PaaS market in 2024. Volume commitments and reserved/commit discounts (up to ~72% for long‑term RIs) and multi‑region architectures improve SLAs and pricing. High-profile outages that cost merchants six‑figure hours increase supplier leverage. Diversification and multi‑cloud reduce concentration risk.

ISVs, VARs, and channel partners

Independent software vendors and VARs can command referral fees and integration prioritization, and popular hospitality/retail ISVs often steer transaction volumes, increasing supplier leverage; Shift4 served over 200,000 merchants in 2024, helping mitigate this risk. Shift4’s integrated platform and revenue-sharing arrangements align incentives to reduce dependence, while investing in proprietary software and direct distribution lowers channel power over time.

- ISV/VAR referral fees and prioritization

- Popular ISVs steer volumes

- Shift4 ~200,000 merchants (2024) aids negotiation

- Revenue-share integrations align incentives

- Proprietary software reduces supplier power long-term

Fraud, risk, and data service providers

Third-party tokenization, KYC, AML, and fraud-scoring providers are highly specialized and sticky, with vendor changes typically triggering model re-tuning and recertifications that can take several months and materially raise switching costs; many payments firms report multi-hundred-thousand-dollar integration expenses. Consolidation or building in-house risk capabilities reduces supplier power, while data partnerships and volume can be leveraged for better pricing and fraud-improvement margins.

- sticky integration

- recertification delays

- high switching costs

- consolidation lowers fees

- data scale = pricing leverage

Networks >80% U.S. volume; cloud 32% IaaS; acquirer ~200k merchants

Suppliers (networks, terminals, cloud, ISVs, fraud vendors) exert moderate-to-high power: Visa/Mastercard >80% U.S. volume (2023–24) and top cloud providers hold ~32%/23%/10% (AWS/Microsoft/Google, 2024). Certification, certification delays and switching costs raise stickiness. Shift4 scale (~200,000 merchants, 2024), integrated stack and revenue-share deals materially reduce supplier leverage.

| Supplier | Metric | 2024 Data |

|---|---|---|

| Card networks | Market share | >80% (Visa+MC) |

| Cloud | IaaS share | AWS 32%/MSFT 23%/GCP 10% |

| Merchants | Shift4 scale | ~200,000 |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively for Shift4; detailed assessment of supplier and buyer power, substitutes, and rivalry identifies disruptive forces and barriers protecting incumbents. Fully editable for reports, decks, and investor materials.

A one-sheet Porter's Five Forces for Shift4 that turns complex competitive dynamics into a clear, customizable radar—perfect for quick boardroom decisions and easy integration into decks or dashboards.

Customers Bargaining Power

Enterprise hospitality and retail chains

Large multi-site hospitality and retail chains negotiate aggressively on pricing and service, leveraging centralized RFPs and volume concentration to extract concessions across a $7.94 trillion U.S. retail and food services market in 2023.

Shift4 offsets pure price focus with end-to-end integration, value-added services and customized SLAs that align with enterprise operational KPIs.

Multi-year (commonly 3–5 year) contracts and bespoke integrations materially raise switching costs, reducing churn risk and preserving margin.

SMBs in restaurant and specialty retail

SMBs in restaurant and specialty retail are highly price sensitive yet face notable switching frictions from POS setup and staff training; National Restaurant Association data show 98% of US restaurants are small businesses (2024), concentrating this demand. Shift4’s bundled POS, gateway, and support lowers appeal of multi-vendor mixes, though month-to-month competitor offers can raise churn risk. Focused education on total cost of ownership and reliability preserves Shift4’s margin.

Vertical feature requirements

Buyers demand vertical features like tableside payment, tokenized card-on-file and omni-channel, and when these are must-haves they can push product roadmaps and timelines. Shift4’s purpose-built hospitality stack—serving over 200,000 merchants—narrows credible alternatives and reduces buyer leverage. Deep PMS/POS integrations increase switching costs, often translating to months of redevelopment and lost operational continuity.

Switching costs and contract terms

Data migration, PCI scope changes and staff re-training create meaningful switching costs for Shift4; 2024 industry estimates put merchant migrations at roughly $10,000–$100,000 in direct costs and weeks-months of downtime risk. Early termination fees and device lock-in further reduce buyer power, though aggressive competitor buyouts can neutralize frictions. Transparent pricing and performance guarantees help Shift4 retain clients without deep discounting.

- Data migration cost range: $10k–$100k (2024 industry estimate)

- PCI scope reduction increases lock-in

- ETFs and device lock-in lower buyer power

- Buyout offers can counteract switching frictions

Price transparency and pass-through fees

Centralized RFPs target $7.94T US retail & food market; SMBs price-sensitive

Large chains drive hard bargains via centralized RFPs across a $7.94 trillion US retail & food services market (2023). Shift4 counters with end-to-end integration, multi-year contracts and PMS/POS lock-in raising switching costs. SMBs remain price-sensitive (98% of US restaurants are small businesses, 2024) while processor markups run 0.10%–0.50% (2024).

| Metric | Value |

|---|---|

| US retail & food services | $7.94T (2023) |

| US restaurants small biz | 98% (2024) |

| Processor markup | 0.10%–0.50% (2024) |

Full Version Awaits

Shift4 Porter's Five Forces Analysis

This preview shows the exact Shift4 Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is the full, professionally formatted report, ready to download and use the moment you buy. You’ll get instant access to this exact file with no surprises.