Shiji Porter's Five Forces Analysis

From Overview to Strategy Blueprint

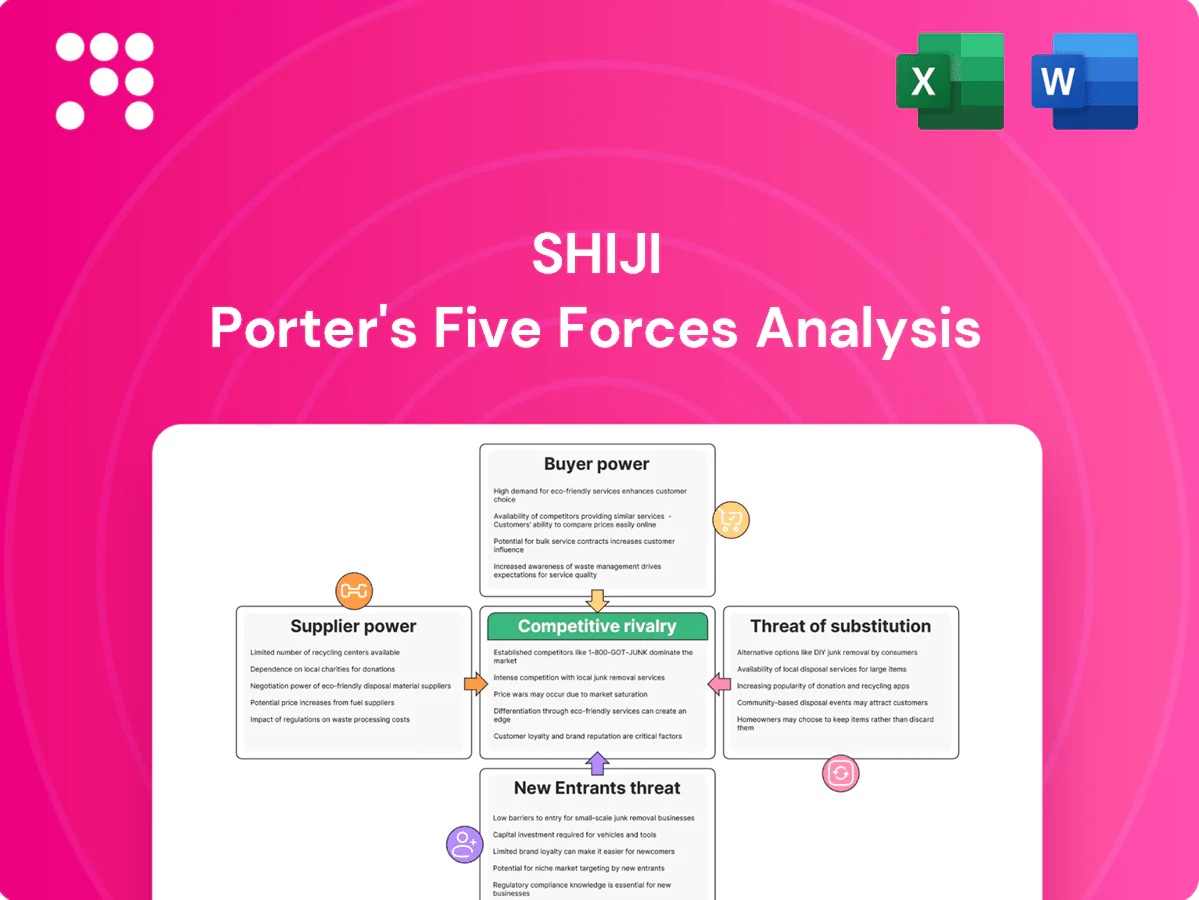

Shiji faces nuanced competitive pressures across suppliers, buyers, new entrants, substitutes, and existing rivals that shape pricing power and growth potential. This snapshot outlines key tensions but skips force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to get detailed ratings, strategic implications, and ready-to-use slides for decision-making.

Suppliers Bargaining Power

Dependence on hyperscale cloud

Shiji’s platforms depend on hyperscalers (AWS ~32%, Azure ~23%, Google ~11% market share in 2024), giving those providers pricing and technical leverage over uptime, latency, and global reach. Long-term commitments can cut costs by up to ~40% via reservations but increase vendor lock-in. Multicloud reduces single-supplier power but typically raises integration and ops costs by ~10–20%.

Payment networks and gateways

Card schemes and acquirers (Visa and Mastercard roughly 80% of global card volume in 2024) and gateway partners control critical rails for hospitality and retail, creating high supplier power. Compliance, certification and tokenization requirements (tokenization used in >60% of mobile transactions in 2024) raise switching frictions and implementation costs. Merchant fees typically run 1.5–3%, and scheme updates/PCI mandates shift compliance costs upstream. Multi-currency needs and alternative payment support add FX spreads (~0.5–2%) and further limit optionality.

Specialized hardware and OEMs

POS peripherals, terminals and kiosks for Shiji are sourced from a narrow pool of certified OEMs (Verifone, Ingenico/Worldline, PAX, Sunmi), concentrating supplier power and limiting alternatives as of 2024.

Component shortages and EOL cycles have repeatedly extended lead times and increased procurement costs, while certification and firmware compatibility raise replacement and integration expenses.

OEM vertical bundles can bundle-lock software providers, constraining negotiation leverage and raising switching costs for Shiji.

Data, maps, and third‑party content

Data, maps and third-party content — covering rate, distribution, identity verification, tax and mapping feeds — underpin Shiji workflows and can drive 10–25% of variable operating costs; in 2024 the location-data market was estimated at $52 billion. API terms, throttling and usage fees shift economics, while partner SLA or schema changes force costly rework. Exclusive rival partnerships can restrict access to strategic datasets.

- API terms & fees — margin volatility

- SLA/schema churn — integration cost driver

- Exclusive deals — dataset access risk

Skilled software talent and SI partners

Senior engineers, cybersecurity experts and domain consultants are scarce in hospitality tech; ISC2 reported a 3.4 million global cybersecurity workforce gap in 2024, boosting supplier power and wage inflation. Poaching pushed experienced engineer pay up by double digits in many markets, tightening hiring timelines. Regional SI partners shape deployment speed and quality, while knowledge concentration creates key-person risk in large rollouts.

- senior engineers: high demand, limited supply

- cybersecurity: 3.4 million global gap (ISC2 2024)

- wage inflation: double-digit uplifts in hotspots

- si partners: control timelines/quality

- key-person risk: concentrated expertise

Hyperscaler and card-scheme dominance squeezes merchants: multicloud costs 10–20%, fees 1.5–3%

Shiji faces concentrated supplier power: hyperscalers (AWS 32%, Azure 23%, Google 11% in 2024) and card schemes (Visa+Mastercard ~80% vol) drive pricing, uptime and compliance risk.

Multicloud reduces single-vendor control but raises ops costs ~10–20%; merchant fees 1.5–3% and tokenization (>60% mobile tx 2024) increase switching friction.

Data feeds ($52B location market 2024), certified OEMs, and a 3.4M cybersecurity workforce gap (ISC2 2024) further constrain leverage.

| Supplier | 2024 stat | Impact |

|---|---|---|

| Hyperscalers | AWS 32%/Azure 23%/GCP 11% | Pricing/uptime leverage |

| Card schemes | Visa+MC ~80% | Fees/compliance lock |

| Data & content | Location market $52B | Variable ops cost 10–25% |

| Cybersecurity talent | 3.4M gap | Wage inflation, key-person risk |

What is included in the product

Tailored Porter's Five Forces analysis for Shiji that uncovers key drivers of competition, buyer and supplier power, entry barriers and substitutes, and identifies disruptive threats and strategic levers to protect market share and inform investor or management decisions.

A one-sheet Shiji Porter's Five Forces summary that visualizes strategic pressure with an editable radar chart and simple layout—ready for pitch decks, dashboards, or scenario tabs without macros so non‑finance teams can update and act fast.

Customers Bargaining Power

Large chains and enterprises

Global hotel groups (Marriott operates ~8,400 properties/1.4M rooms in 2024), QSRs and big-box retailers (Walmart reported $611B revenue in FY2024) buy at scale and demand custom terms; their consolidation concentrates negotiating power over price and product roadmap. RFP-driven procurement cycles force competitive concessions and discounts, while complex multinational deployments and integration needs raise switching costs, reducing pure take-it-or-leave-it pressure.

High switching and integration costs

Deep integrations with PMS, POS, CRS, loyalty and payments make Shiji replacements risky, with typical integration projects costing $50k–$250k and multi-week migrations that amplify downtime exposure. Data migration, staff retraining and certification periods deter churn and give buyers leverage to secure extended support and feature SLAs. Once embedded, vendors defend ARPU via value-led upsells like channel management, payments and loyalty modules.

Preference for open APIs and interoperability

Buyers increasingly mandate open, well-documented APIs to avoid vendor lock-in, with 2024 surveys showing over 60% of enterprise hospitality buyers ranking API openness as a critical procurement criterion. Compliance with HTNG/OTA standards and event-driven architectures is now table stakes for RFPs. High API quality and partner marketplace presence can sway procurement and accelerate time-to-live; poor interoperability often triggers shortlist elimination and squeezes pricing.

Outcome-based expectations

Clients now demand outcome-based contracts focused on measurable lifts in RevPAR, table turn, labor efficiency and payment approval rates, shifting negotiations from licenses to ROI and SLA terms; buyers increasingly require credits for missed KPIs and tie renewals to performance. Clear telemetry and 2024 benchmarking data improve vendor defensibility and reduce dispute rates.

- RevPAR/SLA-driven buying

- Credits for missed KPIs

- Telemetry + benchmarking = stronger defense

- Negotiations centered on ROI not licenses

Global compliance and localization demands

Enterprises demand GDPR, PCI DSS, PSD2/SCA and country fiscalization support, forcing vendors to absorb localization costs or lose deals; country-by-country tax and e-invoicing rules—by 2024 adopted in over 130 jurisdictions—raise implementation complexity and OPEX. Buyers use localization scope to push costs onto vendors, but suppliers with proven compliance footprints can resist discounting, often commanding single-digit to low-double-digit premiums.

- Compliance required: GDPR, PCI DSS, PSD2/SCA, fiscalization

- Global e-invoicing mandates: >130 countries (2024)

- Localization shifts cost leverage to buyers

- Compliant vendors capture price premium

Major buyers (8,400 hotels; $611B retail) demand ROI/SLA; 60% value APIs

Large consolidated buyers (Marriott ~8,400 properties/1.4M rooms; Walmart $611B FY2024) exert strong price and terms pressure, but high integration costs ($50k–$250k) and complex global compliance (>130 e-invoicing jurisdictions, GDPR/PCI) raise switching costs. 60% of enterprise buyers rate API openness critical (2024), shifting negotiations to ROI/SLA outcomes and credit-for-KPI models.

| Metric | 2024 Value |

|---|---|

| Marriott properties | ~8,400 / 1.4M rooms |

| Walmart revenue | $611B FY2024 |

| API importance | 60% enterprises |

What You See Is What You Get

Shiji Porter's Five Forces Analysis

This preview shows the exact Shiji Porter's Five Forces Analysis you’ll receive after purchase—no placeholders, no samples. The document is fully formatted and ready for immediate download and use the moment you buy. You’re viewing the final deliverable; what you see is precisely what will be available to you instantly after payment.

From Overview to Strategy Blueprint

Shiji faces nuanced competitive pressures across suppliers, buyers, new entrants, substitutes, and existing rivals that shape pricing power and growth potential. This snapshot outlines key tensions but skips force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to get detailed ratings, strategic implications, and ready-to-use slides for decision-making.

Suppliers Bargaining Power

Dependence on hyperscale cloud

Shiji’s platforms depend on hyperscalers (AWS ~32%, Azure ~23%, Google ~11% market share in 2024), giving those providers pricing and technical leverage over uptime, latency, and global reach. Long-term commitments can cut costs by up to ~40% via reservations but increase vendor lock-in. Multicloud reduces single-supplier power but typically raises integration and ops costs by ~10–20%.

Payment networks and gateways

Card schemes and acquirers (Visa and Mastercard roughly 80% of global card volume in 2024) and gateway partners control critical rails for hospitality and retail, creating high supplier power. Compliance, certification and tokenization requirements (tokenization used in >60% of mobile transactions in 2024) raise switching frictions and implementation costs. Merchant fees typically run 1.5–3%, and scheme updates/PCI mandates shift compliance costs upstream. Multi-currency needs and alternative payment support add FX spreads (~0.5–2%) and further limit optionality.

Specialized hardware and OEMs

POS peripherals, terminals and kiosks for Shiji are sourced from a narrow pool of certified OEMs (Verifone, Ingenico/Worldline, PAX, Sunmi), concentrating supplier power and limiting alternatives as of 2024.

Component shortages and EOL cycles have repeatedly extended lead times and increased procurement costs, while certification and firmware compatibility raise replacement and integration expenses.

OEM vertical bundles can bundle-lock software providers, constraining negotiation leverage and raising switching costs for Shiji.

Data, maps, and third‑party content

Data, maps and third-party content — covering rate, distribution, identity verification, tax and mapping feeds — underpin Shiji workflows and can drive 10–25% of variable operating costs; in 2024 the location-data market was estimated at $52 billion. API terms, throttling and usage fees shift economics, while partner SLA or schema changes force costly rework. Exclusive rival partnerships can restrict access to strategic datasets.

- API terms & fees — margin volatility

- SLA/schema churn — integration cost driver

- Exclusive deals — dataset access risk

Skilled software talent and SI partners

Senior engineers, cybersecurity experts and domain consultants are scarce in hospitality tech; ISC2 reported a 3.4 million global cybersecurity workforce gap in 2024, boosting supplier power and wage inflation. Poaching pushed experienced engineer pay up by double digits in many markets, tightening hiring timelines. Regional SI partners shape deployment speed and quality, while knowledge concentration creates key-person risk in large rollouts.

- senior engineers: high demand, limited supply

- cybersecurity: 3.4 million global gap (ISC2 2024)

- wage inflation: double-digit uplifts in hotspots

- si partners: control timelines/quality

- key-person risk: concentrated expertise

Hyperscaler and card-scheme dominance squeezes merchants: multicloud costs 10–20%, fees 1.5–3%

Shiji faces concentrated supplier power: hyperscalers (AWS 32%, Azure 23%, Google 11% in 2024) and card schemes (Visa+Mastercard ~80% vol) drive pricing, uptime and compliance risk.

Multicloud reduces single-vendor control but raises ops costs ~10–20%; merchant fees 1.5–3% and tokenization (>60% mobile tx 2024) increase switching friction.

Data feeds ($52B location market 2024), certified OEMs, and a 3.4M cybersecurity workforce gap (ISC2 2024) further constrain leverage.

| Supplier | 2024 stat | Impact |

|---|---|---|

| Hyperscalers | AWS 32%/Azure 23%/GCP 11% | Pricing/uptime leverage |

| Card schemes | Visa+MC ~80% | Fees/compliance lock |

| Data & content | Location market $52B | Variable ops cost 10–25% |

| Cybersecurity talent | 3.4M gap | Wage inflation, key-person risk |

What is included in the product

Tailored Porter's Five Forces analysis for Shiji that uncovers key drivers of competition, buyer and supplier power, entry barriers and substitutes, and identifies disruptive threats and strategic levers to protect market share and inform investor or management decisions.

A one-sheet Shiji Porter's Five Forces summary that visualizes strategic pressure with an editable radar chart and simple layout—ready for pitch decks, dashboards, or scenario tabs without macros so non‑finance teams can update and act fast.

Customers Bargaining Power

Large chains and enterprises

Global hotel groups (Marriott operates ~8,400 properties/1.4M rooms in 2024), QSRs and big-box retailers (Walmart reported $611B revenue in FY2024) buy at scale and demand custom terms; their consolidation concentrates negotiating power over price and product roadmap. RFP-driven procurement cycles force competitive concessions and discounts, while complex multinational deployments and integration needs raise switching costs, reducing pure take-it-or-leave-it pressure.

High switching and integration costs

Deep integrations with PMS, POS, CRS, loyalty and payments make Shiji replacements risky, with typical integration projects costing $50k–$250k and multi-week migrations that amplify downtime exposure. Data migration, staff retraining and certification periods deter churn and give buyers leverage to secure extended support and feature SLAs. Once embedded, vendors defend ARPU via value-led upsells like channel management, payments and loyalty modules.

Preference for open APIs and interoperability

Buyers increasingly mandate open, well-documented APIs to avoid vendor lock-in, with 2024 surveys showing over 60% of enterprise hospitality buyers ranking API openness as a critical procurement criterion. Compliance with HTNG/OTA standards and event-driven architectures is now table stakes for RFPs. High API quality and partner marketplace presence can sway procurement and accelerate time-to-live; poor interoperability often triggers shortlist elimination and squeezes pricing.

Outcome-based expectations

Clients now demand outcome-based contracts focused on measurable lifts in RevPAR, table turn, labor efficiency and payment approval rates, shifting negotiations from licenses to ROI and SLA terms; buyers increasingly require credits for missed KPIs and tie renewals to performance. Clear telemetry and 2024 benchmarking data improve vendor defensibility and reduce dispute rates.

- RevPAR/SLA-driven buying

- Credits for missed KPIs

- Telemetry + benchmarking = stronger defense

- Negotiations centered on ROI not licenses

Global compliance and localization demands

Enterprises demand GDPR, PCI DSS, PSD2/SCA and country fiscalization support, forcing vendors to absorb localization costs or lose deals; country-by-country tax and e-invoicing rules—by 2024 adopted in over 130 jurisdictions—raise implementation complexity and OPEX. Buyers use localization scope to push costs onto vendors, but suppliers with proven compliance footprints can resist discounting, often commanding single-digit to low-double-digit premiums.

- Compliance required: GDPR, PCI DSS, PSD2/SCA, fiscalization

- Global e-invoicing mandates: >130 countries (2024)

- Localization shifts cost leverage to buyers

- Compliant vendors capture price premium

Major buyers (8,400 hotels; $611B retail) demand ROI/SLA; 60% value APIs

Large consolidated buyers (Marriott ~8,400 properties/1.4M rooms; Walmart $611B FY2024) exert strong price and terms pressure, but high integration costs ($50k–$250k) and complex global compliance (>130 e-invoicing jurisdictions, GDPR/PCI) raise switching costs. 60% of enterprise buyers rate API openness critical (2024), shifting negotiations to ROI/SLA outcomes and credit-for-KPI models.

| Metric | 2024 Value |

|---|---|

| Marriott properties | ~8,400 / 1.4M rooms |

| Walmart revenue | $611B FY2024 |

| API importance | 60% enterprises |

What You See Is What You Get

Shiji Porter's Five Forces Analysis

This preview shows the exact Shiji Porter's Five Forces Analysis you’ll receive after purchase—no placeholders, no samples. The document is fully formatted and ready for immediate download and use the moment you buy. You’re viewing the final deliverable; what you see is precisely what will be available to you instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Shiji faces nuanced competitive pressures across suppliers, buyers, new entrants, substitutes, and existing rivals that shape pricing power and growth potential. This snapshot outlines key tensions but skips force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to get detailed ratings, strategic implications, and ready-to-use slides for decision-making.

Suppliers Bargaining Power

Dependence on hyperscale cloud

Shiji’s platforms depend on hyperscalers (AWS ~32%, Azure ~23%, Google ~11% market share in 2024), giving those providers pricing and technical leverage over uptime, latency, and global reach. Long-term commitments can cut costs by up to ~40% via reservations but increase vendor lock-in. Multicloud reduces single-supplier power but typically raises integration and ops costs by ~10–20%.

Payment networks and gateways

Card schemes and acquirers (Visa and Mastercard roughly 80% of global card volume in 2024) and gateway partners control critical rails for hospitality and retail, creating high supplier power. Compliance, certification and tokenization requirements (tokenization used in >60% of mobile transactions in 2024) raise switching frictions and implementation costs. Merchant fees typically run 1.5–3%, and scheme updates/PCI mandates shift compliance costs upstream. Multi-currency needs and alternative payment support add FX spreads (~0.5–2%) and further limit optionality.

Specialized hardware and OEMs

POS peripherals, terminals and kiosks for Shiji are sourced from a narrow pool of certified OEMs (Verifone, Ingenico/Worldline, PAX, Sunmi), concentrating supplier power and limiting alternatives as of 2024.

Component shortages and EOL cycles have repeatedly extended lead times and increased procurement costs, while certification and firmware compatibility raise replacement and integration expenses.

OEM vertical bundles can bundle-lock software providers, constraining negotiation leverage and raising switching costs for Shiji.

Data, maps, and third‑party content

Data, maps and third-party content — covering rate, distribution, identity verification, tax and mapping feeds — underpin Shiji workflows and can drive 10–25% of variable operating costs; in 2024 the location-data market was estimated at $52 billion. API terms, throttling and usage fees shift economics, while partner SLA or schema changes force costly rework. Exclusive rival partnerships can restrict access to strategic datasets.

- API terms & fees — margin volatility

- SLA/schema churn — integration cost driver

- Exclusive deals — dataset access risk

Skilled software talent and SI partners

Senior engineers, cybersecurity experts and domain consultants are scarce in hospitality tech; ISC2 reported a 3.4 million global cybersecurity workforce gap in 2024, boosting supplier power and wage inflation. Poaching pushed experienced engineer pay up by double digits in many markets, tightening hiring timelines. Regional SI partners shape deployment speed and quality, while knowledge concentration creates key-person risk in large rollouts.

- senior engineers: high demand, limited supply

- cybersecurity: 3.4 million global gap (ISC2 2024)

- wage inflation: double-digit uplifts in hotspots

- si partners: control timelines/quality

- key-person risk: concentrated expertise

Hyperscaler and card-scheme dominance squeezes merchants: multicloud costs 10–20%, fees 1.5–3%

Shiji faces concentrated supplier power: hyperscalers (AWS 32%, Azure 23%, Google 11% in 2024) and card schemes (Visa+Mastercard ~80% vol) drive pricing, uptime and compliance risk.

Multicloud reduces single-vendor control but raises ops costs ~10–20%; merchant fees 1.5–3% and tokenization (>60% mobile tx 2024) increase switching friction.

Data feeds ($52B location market 2024), certified OEMs, and a 3.4M cybersecurity workforce gap (ISC2 2024) further constrain leverage.

| Supplier | 2024 stat | Impact |

|---|---|---|

| Hyperscalers | AWS 32%/Azure 23%/GCP 11% | Pricing/uptime leverage |

| Card schemes | Visa+MC ~80% | Fees/compliance lock |

| Data & content | Location market $52B | Variable ops cost 10–25% |

| Cybersecurity talent | 3.4M gap | Wage inflation, key-person risk |

What is included in the product

Tailored Porter's Five Forces analysis for Shiji that uncovers key drivers of competition, buyer and supplier power, entry barriers and substitutes, and identifies disruptive threats and strategic levers to protect market share and inform investor or management decisions.

A one-sheet Shiji Porter's Five Forces summary that visualizes strategic pressure with an editable radar chart and simple layout—ready for pitch decks, dashboards, or scenario tabs without macros so non‑finance teams can update and act fast.

Customers Bargaining Power

Large chains and enterprises

Global hotel groups (Marriott operates ~8,400 properties/1.4M rooms in 2024), QSRs and big-box retailers (Walmart reported $611B revenue in FY2024) buy at scale and demand custom terms; their consolidation concentrates negotiating power over price and product roadmap. RFP-driven procurement cycles force competitive concessions and discounts, while complex multinational deployments and integration needs raise switching costs, reducing pure take-it-or-leave-it pressure.

High switching and integration costs

Deep integrations with PMS, POS, CRS, loyalty and payments make Shiji replacements risky, with typical integration projects costing $50k–$250k and multi-week migrations that amplify downtime exposure. Data migration, staff retraining and certification periods deter churn and give buyers leverage to secure extended support and feature SLAs. Once embedded, vendors defend ARPU via value-led upsells like channel management, payments and loyalty modules.

Preference for open APIs and interoperability

Buyers increasingly mandate open, well-documented APIs to avoid vendor lock-in, with 2024 surveys showing over 60% of enterprise hospitality buyers ranking API openness as a critical procurement criterion. Compliance with HTNG/OTA standards and event-driven architectures is now table stakes for RFPs. High API quality and partner marketplace presence can sway procurement and accelerate time-to-live; poor interoperability often triggers shortlist elimination and squeezes pricing.

Outcome-based expectations

Clients now demand outcome-based contracts focused on measurable lifts in RevPAR, table turn, labor efficiency and payment approval rates, shifting negotiations from licenses to ROI and SLA terms; buyers increasingly require credits for missed KPIs and tie renewals to performance. Clear telemetry and 2024 benchmarking data improve vendor defensibility and reduce dispute rates.

- RevPAR/SLA-driven buying

- Credits for missed KPIs

- Telemetry + benchmarking = stronger defense

- Negotiations centered on ROI not licenses

Global compliance and localization demands

Enterprises demand GDPR, PCI DSS, PSD2/SCA and country fiscalization support, forcing vendors to absorb localization costs or lose deals; country-by-country tax and e-invoicing rules—by 2024 adopted in over 130 jurisdictions—raise implementation complexity and OPEX. Buyers use localization scope to push costs onto vendors, but suppliers with proven compliance footprints can resist discounting, often commanding single-digit to low-double-digit premiums.

- Compliance required: GDPR, PCI DSS, PSD2/SCA, fiscalization

- Global e-invoicing mandates: >130 countries (2024)

- Localization shifts cost leverage to buyers

- Compliant vendors capture price premium

Major buyers (8,400 hotels; $611B retail) demand ROI/SLA; 60% value APIs

Large consolidated buyers (Marriott ~8,400 properties/1.4M rooms; Walmart $611B FY2024) exert strong price and terms pressure, but high integration costs ($50k–$250k) and complex global compliance (>130 e-invoicing jurisdictions, GDPR/PCI) raise switching costs. 60% of enterprise buyers rate API openness critical (2024), shifting negotiations to ROI/SLA outcomes and credit-for-KPI models.

| Metric | 2024 Value |

|---|---|

| Marriott properties | ~8,400 / 1.4M rooms |

| Walmart revenue | $611B FY2024 |

| API importance | 60% enterprises |

What You See Is What You Get

Shiji Porter's Five Forces Analysis

This preview shows the exact Shiji Porter's Five Forces Analysis you’ll receive after purchase—no placeholders, no samples. The document is fully formatted and ready for immediate download and use the moment you buy. You’re viewing the final deliverable; what you see is precisely what will be available to you instantly after payment.