Shimao Property Holdings Porter's Five Forces Analysis

From Overview to Strategy Blueprint

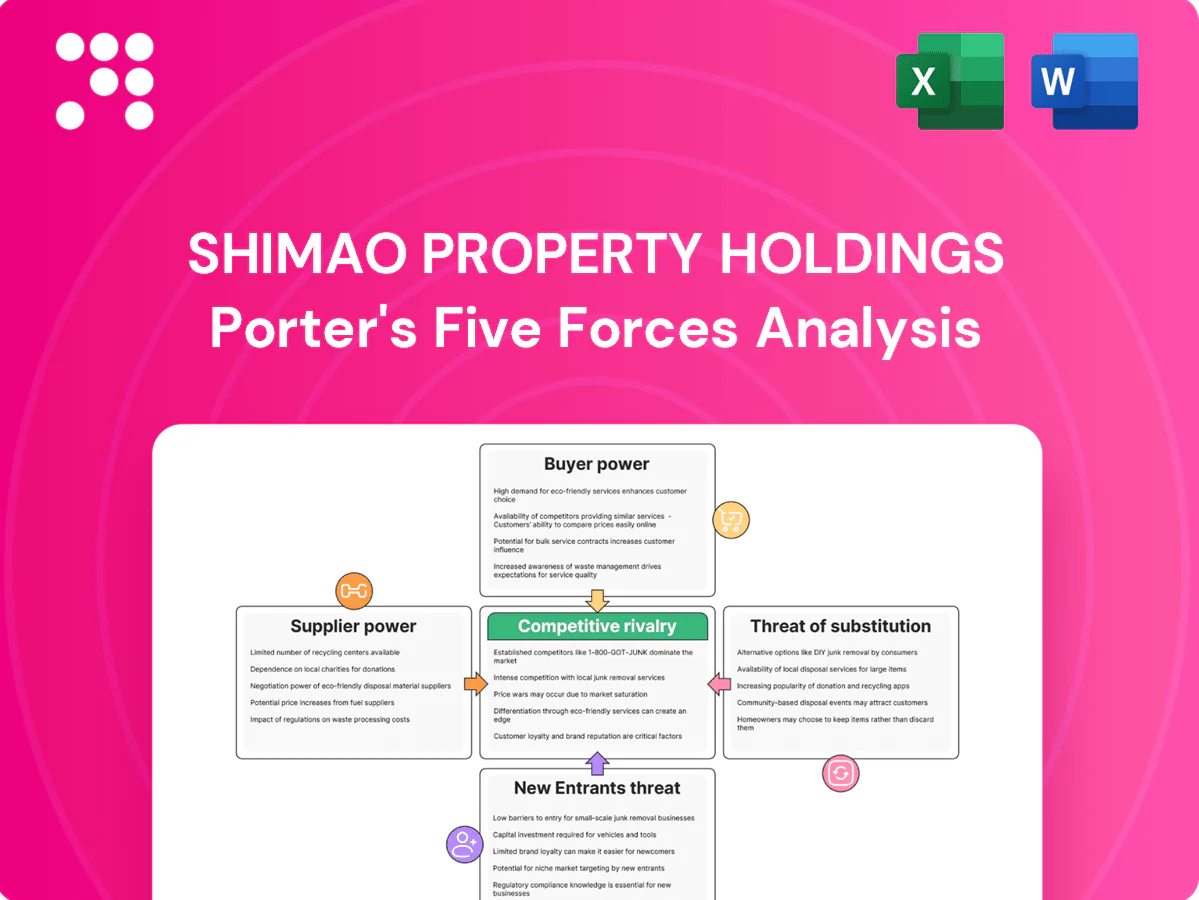

Shimao Property Holdings faces intense rivalry, moderate supplier leverage, strong buyer sensitivity, rising substitute risks from alternate housing models, and regulatory/new-entry pressures shaping margins and growth prospects. This snapshot hints at key tensions—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or planning decisions.

Suppliers Bargaining Power

Land supply by local governments

Chinese local governments control primary land supply via auctions and policy quotas, accounting for over 90% of urban land transfers in 2024. This concentration gives municipalities decisive pricing and timing power, forcing Shimao to align projects with city-level planning to secure prime parcels. Intense competitive bidding in 2024 pushed land premiums higher, compressing margins for developers.

Construction materials volatility

Steel, cement, glass and MEP inputs are supplied by large upstream firms that control over 50% of capacity, exposing Shimao to supplier leverage. Spot steel and cement swings have reached ~20% in peak cycles, with cartel-like dynamics pressuring margins. Long-term framework contracts and volume bundling typically secure 70–90% of baseline volumes but do not eliminate price risk. Logistics bottlenecks create 5–10% regional price dispersion.

General contractors and specialty trades

Tier-1 EPCs and niche subcontractors wield schedule and quality leverage over Shimao, especially in hot markets where capacity is tight and lead times extend. Dual-sourcing and design standardization improve substitutability and reduce single-vendor risk. Strong payment terms and retention mechanisms (progress payments plus retention funds) partially offset supplier bargaining power.

Financing and capital providers

- Banks: tighter credit screens, higher covenants

- Trusts/onshore bonds: selective pricing

- Escrow rules 2024: limited cashflow flexibility

- Shimao: track record and collateral shape terms

Design, tech, and hotel operators

Brand architects, smart-building vendors and hotel flags provide differentiation but remain limited in number, giving suppliers moderate bargaining power; in 2024 hotel management/franchise fees typically ran 3–5% of room revenue and smart-building solutions saw roughly a 10% CAGR to 2024, supporting premium pricing and royalties for signature partners. Shimao’s multi-asset scale and repeat business strengthen procurement leverage, while growing in-house design and operations reduce supplier dependence in key areas.

- Few premium partners — higher royalties (3–5% of room revenue in 2024)

- Smart-building market ~10% CAGR to 2024 — vendor premium pricing

- Scale + repeat projects = stronger bargaining

- In-house capabilities = lower dependency

Municipal land control, supplier concentration and bank tightening squeeze margins and timing

Municipal control of land (>90% of urban transfers in 2024) gives cities decisive pricing/timing power. Key materials suppliers hold >50% capacity with spot steel/cement swings ~20%, while framework contracts cover ~70–90% baseline volumes. Banks tightened credit in 2024 and escrow rules cut liquidity; hotel fees 3–5% and smart-building CAGR ~10% lift vendor leverage.

| Factor | 2024 metric | Impact on Shimao |

|---|---|---|

| Land | >90% municipal transfers | High timing/pricing risk |

| Materials | >50% capacity; ~20% price swings | Margin pressure |

| Contracts | 70–90% volumes | Partial risk mitigation |

| Finance | Tighter bank covenants; escrow rules | Liquidity constraint |

| Premium partners | Hotel fees 3–5%; smart-building CAGR ~10% | Moderate supplier power |

What is included in the product

Uncovers key competitive drivers—buyer and supplier power, industry rivalry, entry barriers and substitutes—tailored to Shimao Property Holdings; highlights disruptive threats, pricing influence and strategic levers to protect margins and market position.

A concise one-sheet Porter’s Five Forces for Shimao Property Holdings that quantifies competitive pressures and produces an instant radar chart for quick strategic decisions; easily customize inputs for regulatory shifts or market cycles and paste-ready for pitch decks—no macros required.

Customers Bargaining Power

Price-sensitive homebuyers

Residential buyers increasingly shop by price-per-square-meter across nearby comps, using listing portals that make unit-level pricing visible and directly comparable.

Transparent platforms and secondary-market price discovery, in a sector that represents roughly 25% of China’s economy, materially increase buyer leverage.

In soft markets purchasers demand discounts, freebies and staged payments, so Shimao must align launch pricing to expected absorption velocity to protect margins.

Institutional and commercial tenants

Office and retail tenants press Shimao on rent, fit-out allowances and lease lengths, with anchor tenants able to win concessions that become mall-wide benchmarks. STR reported China hotel RevPAR recovered to about 90% of 2019 levels in 2024, keeping hotel customers rate-sensitive and channel-driven. Shimao’s 2024 mixed-use projects boost cross-footfall and tenant stickiness, reducing churn.

Low switching costs

Buyers in 2024 can readily switch among competing projects within the same district due to abundant mid-market supply and minimal product differentiation, amplifying their bargaining power. Brand reputation and after-sales service from Shimao partially raise switching costs by creating trust signals. Comprehensive amenities and community operations increasingly lock in resident preference, reducing churn despite low financial switching barriers.

Pre-sale dependency

Developers' reliance on pre-sales for cash flow gives early buyers leverage over pricing, payment schedules and contract terms; construction milestones and delivery assurances become primary negotiation points. Refund and change policies shape perceived risk and thus buyer bargaining power, and Shimao’s recent delivery track record is decisive for sustaining pre-sales momentum.

- Pre-sale cash flow dependence

- Milestone-based negotiations

- Refund/change policy impact

- Delivery record drives trust

Digital comparison and reviews

Proptech platforms aggregate pricing, layouts and user feedback, and about 70% of buyers consult online reviews (2024), raising customers' bargaining power; negative reviews can force price concessions or higher marketing spend and demand verifiable specs on build quality and HOA fees; Shimao must actively manage digital reputation and publish certified property data.

- Proptech aggregation increases transparency

- Negative reviews drive concessions/marketing

- Demand for verifiable specs and HOA fees

70% check reviews; price/sqm transparency tightens pricing

Buyers compare price/sqm across listings; 70% consult online reviews in 2024, boosting negotiation leverage. Transparent platforms and secondary-market discovery (property sector ~25% of China GDP) force Shimao to price for absorption to protect margins. Pre-sales dependence and delivery record remain key bargaining levers; hotel RevPAR ~90% of 2019 in 2024 keeps rate sensitivity high.

| Metric | 2024 |

|---|---|

| Buyers using online reviews | 70% |

| Sector share of GDP | ~25% |

| Hotel RevPAR vs 2019 | ~90% |

Preview Before You Purchase

Shimao Property Holdings Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Shimao Property Holdings Porter's Five Forces analysis evaluates buyer and supplier power, competitive rivalry, threat of new entrants and substitutes, and regulatory pressures. It highlights strengths like scale and landbank alongside risks from indebtedness, market saturation and policy constraints. The file is professionally formatted and ready for immediate use.

From Overview to Strategy Blueprint

Shimao Property Holdings faces intense rivalry, moderate supplier leverage, strong buyer sensitivity, rising substitute risks from alternate housing models, and regulatory/new-entry pressures shaping margins and growth prospects. This snapshot hints at key tensions—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or planning decisions.

Suppliers Bargaining Power

Land supply by local governments

Chinese local governments control primary land supply via auctions and policy quotas, accounting for over 90% of urban land transfers in 2024. This concentration gives municipalities decisive pricing and timing power, forcing Shimao to align projects with city-level planning to secure prime parcels. Intense competitive bidding in 2024 pushed land premiums higher, compressing margins for developers.

Construction materials volatility

Steel, cement, glass and MEP inputs are supplied by large upstream firms that control over 50% of capacity, exposing Shimao to supplier leverage. Spot steel and cement swings have reached ~20% in peak cycles, with cartel-like dynamics pressuring margins. Long-term framework contracts and volume bundling typically secure 70–90% of baseline volumes but do not eliminate price risk. Logistics bottlenecks create 5–10% regional price dispersion.

General contractors and specialty trades

Tier-1 EPCs and niche subcontractors wield schedule and quality leverage over Shimao, especially in hot markets where capacity is tight and lead times extend. Dual-sourcing and design standardization improve substitutability and reduce single-vendor risk. Strong payment terms and retention mechanisms (progress payments plus retention funds) partially offset supplier bargaining power.

Financing and capital providers

- Banks: tighter credit screens, higher covenants

- Trusts/onshore bonds: selective pricing

- Escrow rules 2024: limited cashflow flexibility

- Shimao: track record and collateral shape terms

Design, tech, and hotel operators

Brand architects, smart-building vendors and hotel flags provide differentiation but remain limited in number, giving suppliers moderate bargaining power; in 2024 hotel management/franchise fees typically ran 3–5% of room revenue and smart-building solutions saw roughly a 10% CAGR to 2024, supporting premium pricing and royalties for signature partners. Shimao’s multi-asset scale and repeat business strengthen procurement leverage, while growing in-house design and operations reduce supplier dependence in key areas.

- Few premium partners — higher royalties (3–5% of room revenue in 2024)

- Smart-building market ~10% CAGR to 2024 — vendor premium pricing

- Scale + repeat projects = stronger bargaining

- In-house capabilities = lower dependency

Municipal land control, supplier concentration and bank tightening squeeze margins and timing

Municipal control of land (>90% of urban transfers in 2024) gives cities decisive pricing/timing power. Key materials suppliers hold >50% capacity with spot steel/cement swings ~20%, while framework contracts cover ~70–90% baseline volumes. Banks tightened credit in 2024 and escrow rules cut liquidity; hotel fees 3–5% and smart-building CAGR ~10% lift vendor leverage.

| Factor | 2024 metric | Impact on Shimao |

|---|---|---|

| Land | >90% municipal transfers | High timing/pricing risk |

| Materials | >50% capacity; ~20% price swings | Margin pressure |

| Contracts | 70–90% volumes | Partial risk mitigation |

| Finance | Tighter bank covenants; escrow rules | Liquidity constraint |

| Premium partners | Hotel fees 3–5%; smart-building CAGR ~10% | Moderate supplier power |

What is included in the product

Uncovers key competitive drivers—buyer and supplier power, industry rivalry, entry barriers and substitutes—tailored to Shimao Property Holdings; highlights disruptive threats, pricing influence and strategic levers to protect margins and market position.

A concise one-sheet Porter’s Five Forces for Shimao Property Holdings that quantifies competitive pressures and produces an instant radar chart for quick strategic decisions; easily customize inputs for regulatory shifts or market cycles and paste-ready for pitch decks—no macros required.

Customers Bargaining Power

Price-sensitive homebuyers

Residential buyers increasingly shop by price-per-square-meter across nearby comps, using listing portals that make unit-level pricing visible and directly comparable.

Transparent platforms and secondary-market price discovery, in a sector that represents roughly 25% of China’s economy, materially increase buyer leverage.

In soft markets purchasers demand discounts, freebies and staged payments, so Shimao must align launch pricing to expected absorption velocity to protect margins.

Institutional and commercial tenants

Office and retail tenants press Shimao on rent, fit-out allowances and lease lengths, with anchor tenants able to win concessions that become mall-wide benchmarks. STR reported China hotel RevPAR recovered to about 90% of 2019 levels in 2024, keeping hotel customers rate-sensitive and channel-driven. Shimao’s 2024 mixed-use projects boost cross-footfall and tenant stickiness, reducing churn.

Low switching costs

Buyers in 2024 can readily switch among competing projects within the same district due to abundant mid-market supply and minimal product differentiation, amplifying their bargaining power. Brand reputation and after-sales service from Shimao partially raise switching costs by creating trust signals. Comprehensive amenities and community operations increasingly lock in resident preference, reducing churn despite low financial switching barriers.

Pre-sale dependency

Developers' reliance on pre-sales for cash flow gives early buyers leverage over pricing, payment schedules and contract terms; construction milestones and delivery assurances become primary negotiation points. Refund and change policies shape perceived risk and thus buyer bargaining power, and Shimao’s recent delivery track record is decisive for sustaining pre-sales momentum.

- Pre-sale cash flow dependence

- Milestone-based negotiations

- Refund/change policy impact

- Delivery record drives trust

Digital comparison and reviews

Proptech platforms aggregate pricing, layouts and user feedback, and about 70% of buyers consult online reviews (2024), raising customers' bargaining power; negative reviews can force price concessions or higher marketing spend and demand verifiable specs on build quality and HOA fees; Shimao must actively manage digital reputation and publish certified property data.

- Proptech aggregation increases transparency

- Negative reviews drive concessions/marketing

- Demand for verifiable specs and HOA fees

70% check reviews; price/sqm transparency tightens pricing

Buyers compare price/sqm across listings; 70% consult online reviews in 2024, boosting negotiation leverage. Transparent platforms and secondary-market discovery (property sector ~25% of China GDP) force Shimao to price for absorption to protect margins. Pre-sales dependence and delivery record remain key bargaining levers; hotel RevPAR ~90% of 2019 in 2024 keeps rate sensitivity high.

| Metric | 2024 |

|---|---|

| Buyers using online reviews | 70% |

| Sector share of GDP | ~25% |

| Hotel RevPAR vs 2019 | ~90% |

Preview Before You Purchase

Shimao Property Holdings Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Shimao Property Holdings Porter's Five Forces analysis evaluates buyer and supplier power, competitive rivalry, threat of new entrants and substitutes, and regulatory pressures. It highlights strengths like scale and landbank alongside risks from indebtedness, market saturation and policy constraints. The file is professionally formatted and ready for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Shimao Property Holdings faces intense rivalry, moderate supplier leverage, strong buyer sensitivity, rising substitute risks from alternate housing models, and regulatory/new-entry pressures shaping margins and growth prospects. This snapshot hints at key tensions—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or planning decisions.

Suppliers Bargaining Power

Land supply by local governments

Chinese local governments control primary land supply via auctions and policy quotas, accounting for over 90% of urban land transfers in 2024. This concentration gives municipalities decisive pricing and timing power, forcing Shimao to align projects with city-level planning to secure prime parcels. Intense competitive bidding in 2024 pushed land premiums higher, compressing margins for developers.

Construction materials volatility

Steel, cement, glass and MEP inputs are supplied by large upstream firms that control over 50% of capacity, exposing Shimao to supplier leverage. Spot steel and cement swings have reached ~20% in peak cycles, with cartel-like dynamics pressuring margins. Long-term framework contracts and volume bundling typically secure 70–90% of baseline volumes but do not eliminate price risk. Logistics bottlenecks create 5–10% regional price dispersion.

General contractors and specialty trades

Tier-1 EPCs and niche subcontractors wield schedule and quality leverage over Shimao, especially in hot markets where capacity is tight and lead times extend. Dual-sourcing and design standardization improve substitutability and reduce single-vendor risk. Strong payment terms and retention mechanisms (progress payments plus retention funds) partially offset supplier bargaining power.

Financing and capital providers

- Banks: tighter credit screens, higher covenants

- Trusts/onshore bonds: selective pricing

- Escrow rules 2024: limited cashflow flexibility

- Shimao: track record and collateral shape terms

Design, tech, and hotel operators

Brand architects, smart-building vendors and hotel flags provide differentiation but remain limited in number, giving suppliers moderate bargaining power; in 2024 hotel management/franchise fees typically ran 3–5% of room revenue and smart-building solutions saw roughly a 10% CAGR to 2024, supporting premium pricing and royalties for signature partners. Shimao’s multi-asset scale and repeat business strengthen procurement leverage, while growing in-house design and operations reduce supplier dependence in key areas.

- Few premium partners — higher royalties (3–5% of room revenue in 2024)

- Smart-building market ~10% CAGR to 2024 — vendor premium pricing

- Scale + repeat projects = stronger bargaining

- In-house capabilities = lower dependency

Municipal land control, supplier concentration and bank tightening squeeze margins and timing

Municipal control of land (>90% of urban transfers in 2024) gives cities decisive pricing/timing power. Key materials suppliers hold >50% capacity with spot steel/cement swings ~20%, while framework contracts cover ~70–90% baseline volumes. Banks tightened credit in 2024 and escrow rules cut liquidity; hotel fees 3–5% and smart-building CAGR ~10% lift vendor leverage.

| Factor | 2024 metric | Impact on Shimao |

|---|---|---|

| Land | >90% municipal transfers | High timing/pricing risk |

| Materials | >50% capacity; ~20% price swings | Margin pressure |

| Contracts | 70–90% volumes | Partial risk mitigation |

| Finance | Tighter bank covenants; escrow rules | Liquidity constraint |

| Premium partners | Hotel fees 3–5%; smart-building CAGR ~10% | Moderate supplier power |

What is included in the product

Uncovers key competitive drivers—buyer and supplier power, industry rivalry, entry barriers and substitutes—tailored to Shimao Property Holdings; highlights disruptive threats, pricing influence and strategic levers to protect margins and market position.

A concise one-sheet Porter’s Five Forces for Shimao Property Holdings that quantifies competitive pressures and produces an instant radar chart for quick strategic decisions; easily customize inputs for regulatory shifts or market cycles and paste-ready for pitch decks—no macros required.

Customers Bargaining Power

Price-sensitive homebuyers

Residential buyers increasingly shop by price-per-square-meter across nearby comps, using listing portals that make unit-level pricing visible and directly comparable.

Transparent platforms and secondary-market price discovery, in a sector that represents roughly 25% of China’s economy, materially increase buyer leverage.

In soft markets purchasers demand discounts, freebies and staged payments, so Shimao must align launch pricing to expected absorption velocity to protect margins.

Institutional and commercial tenants

Office and retail tenants press Shimao on rent, fit-out allowances and lease lengths, with anchor tenants able to win concessions that become mall-wide benchmarks. STR reported China hotel RevPAR recovered to about 90% of 2019 levels in 2024, keeping hotel customers rate-sensitive and channel-driven. Shimao’s 2024 mixed-use projects boost cross-footfall and tenant stickiness, reducing churn.

Low switching costs

Buyers in 2024 can readily switch among competing projects within the same district due to abundant mid-market supply and minimal product differentiation, amplifying their bargaining power. Brand reputation and after-sales service from Shimao partially raise switching costs by creating trust signals. Comprehensive amenities and community operations increasingly lock in resident preference, reducing churn despite low financial switching barriers.

Pre-sale dependency

Developers' reliance on pre-sales for cash flow gives early buyers leverage over pricing, payment schedules and contract terms; construction milestones and delivery assurances become primary negotiation points. Refund and change policies shape perceived risk and thus buyer bargaining power, and Shimao’s recent delivery track record is decisive for sustaining pre-sales momentum.

- Pre-sale cash flow dependence

- Milestone-based negotiations

- Refund/change policy impact

- Delivery record drives trust

Digital comparison and reviews

Proptech platforms aggregate pricing, layouts and user feedback, and about 70% of buyers consult online reviews (2024), raising customers' bargaining power; negative reviews can force price concessions or higher marketing spend and demand verifiable specs on build quality and HOA fees; Shimao must actively manage digital reputation and publish certified property data.

- Proptech aggregation increases transparency

- Negative reviews drive concessions/marketing

- Demand for verifiable specs and HOA fees

70% check reviews; price/sqm transparency tightens pricing

Buyers compare price/sqm across listings; 70% consult online reviews in 2024, boosting negotiation leverage. Transparent platforms and secondary-market discovery (property sector ~25% of China GDP) force Shimao to price for absorption to protect margins. Pre-sales dependence and delivery record remain key bargaining levers; hotel RevPAR ~90% of 2019 in 2024 keeps rate sensitivity high.

| Metric | 2024 |

|---|---|

| Buyers using online reviews | 70% |

| Sector share of GDP | ~25% |

| Hotel RevPAR vs 2019 | ~90% |

Preview Before You Purchase

Shimao Property Holdings Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Shimao Property Holdings Porter's Five Forces analysis evaluates buyer and supplier power, competitive rivalry, threat of new entrants and substitutes, and regulatory pressures. It highlights strengths like scale and landbank alongside risks from indebtedness, market saturation and policy constraints. The file is professionally formatted and ready for immediate use.