Nippon Shokubai Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Nippon Shokubai faces moderate supplier power due to specialized feedstocks, intense rivalry from global chemical peers, and growing substitute risks from greener polymers, while scale and IP provide defensive advantages. This brief snapshot only scratches the surface—dive deeper to quantify force ratings and strategic levers. Unlock the full Porter's Five Forces Analysis to explore Nippon Shokubai’s competitive dynamics in detail.

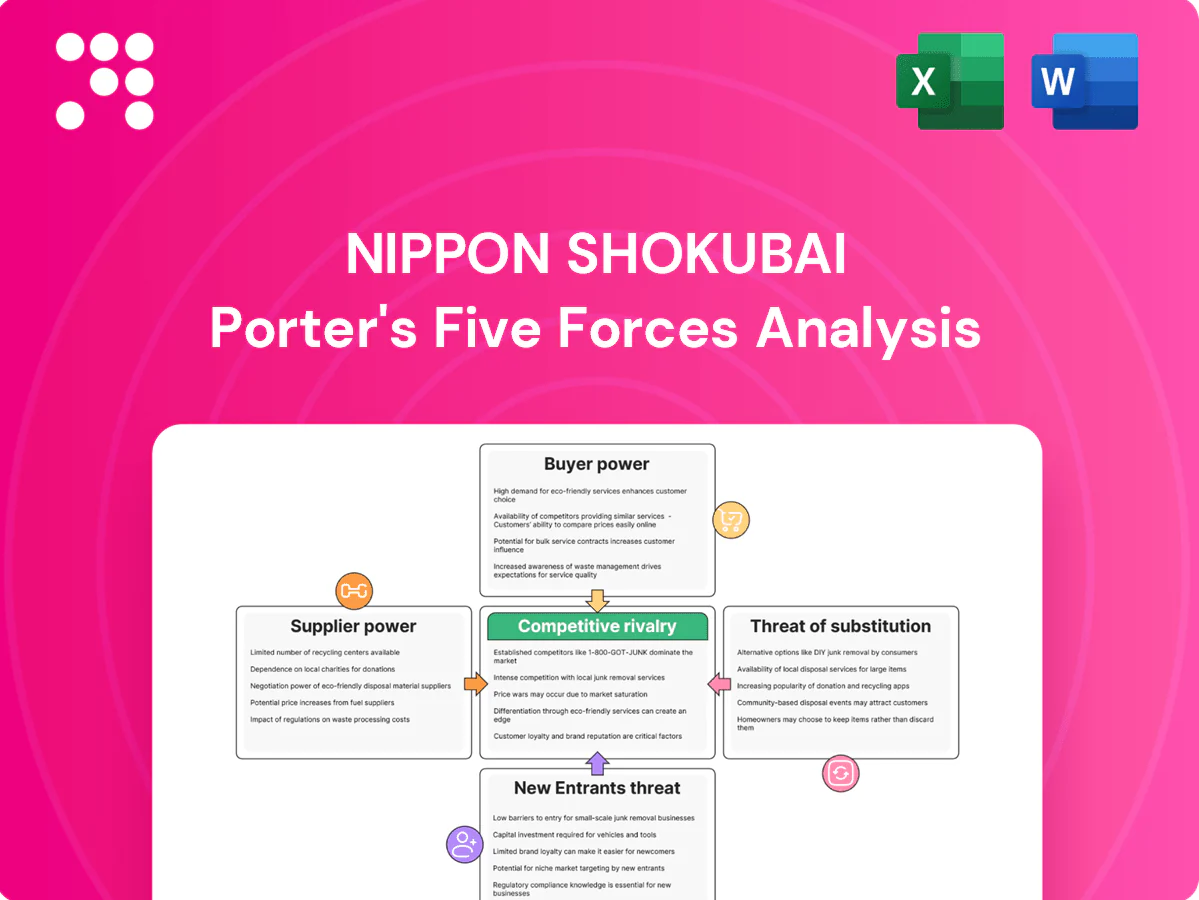

Suppliers Bargaining Power

Petrochemical feedstock concentration

Core inputs like propylene, ethylene and caustic soda come from a concentrated supplier base—top 10 producers held roughly 60% of global propylene/ethylene capacity in 2024, boosting supplier leverage. Price volatility tied to naphtha/crude cycles produced swings up to ±30% in 2024, strengthening sellers. Long-term contracts and hedging have tempered shocks for Nippon Shokubai, while backward integration and multi-sourcing materially reduce exposure.

Specialty catalyst and additive dependence

Certain catalysts and additives are proprietary and sourced from few vendors, driving supplier power; process requalification for substitutes can take 3–12 months and create non-trivial switching costs. Joint development agreements with suppliers have reduced price volatility in comparable chemical segments by up to 10% in 2024. Inventory buffers of 2–8 weeks are commonly used to mitigate interruptions.

Logistics and energy constraints

Steam, power and industrial gases are often supplied by local monopolies, giving suppliers strong leverage over chemical producers; 2024 saw renewed energy price volatility that pressured margins across Japan's specialty-chemicals sector. Energy spikes feed directly into COGS, but onsite cogeneration and long-term PPAs have been adopted to blunt supplier power and stabilize unit costs. Geographic diversification of plants further spreads operational risk and exposure to localized utility constraints.

Quality and specification rigidity

High-purity specifications for acrylic acid and SAPs effectively restrict approved suppliers to a very small cohort, increasing supplier bargaining power as fewer vendors can meet purity and consistency demands.

Tighter specs raise switching costs and price leverage, though vendor qualification programs and multi-year audits have widened options for Nippon Shokubai over time.

Statistical quality agreements (SQA) and KPI-based contracts are increasingly used to enforce performance and mitigate supply risk.

- narrow approved supplier pools

- higher switching costs → greater supplier leverage

- vendor qualification programs expand sourcing

- SQA enforceable KPIs reduce operational risk

Sustainability and compliance requirements

Stricter ESG sourcing in 2024, reinforced by CBAM rollouts and buyer mandates, narrows low-carbon feedstock suppliers and strengthens supplier leverage; compliance premiums and certification costs raise input costs and can add margin pressure for Nippon Shokubai. Collaborative traceability projects reduce supply-risk and lessen bargaining asymmetry, while third-party certifications expand the pool of acceptable sustainable suppliers.

- ESG sourcing limits supplier pool

- Compliance premiums raise input costs

- Traceability reduces supplier power

- Certifications broaden sustainable suppliers

Supplier power high: top10 hold ~60%; firms hedge via integration

Supplier power is high: top‑10 propylene/ethylene producers held ~60% capacity in 2024 and feedstock price swings reached ±30%, while narrow approved supplier pools and energy monopolies raise switching costs; Nippon Shokubai offsets via backward integration, multi‑sourcing, long‑term contracts and onsite cogeneration.

| Metric | 2024 |

|---|---|

| Top‑10 capacity (propylene/ethylene) | ~60% |

| Feedstock price volatility | ±30% |

| Typical inventory buffer | 2–8 weeks |

What is included in the product

Tailored exclusively for Nippon Shokubai, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, barriers to entry, threat of substitutes, and identifies disruptive forces and strategic implications for pricing and profitability.

A concise, one-sheet Porter's Five Forces for Nippon Shokubai that clarifies supplier, buyer, rivalry, entrant and substitute pressures for rapid strategic decisions—customizable pressure levels and a ready-to-use spider chart make it easy to spot relief points and prioritize actions.

Customers Bargaining Power

Large OEMs and converters

Large OEMs and converters in automotive, hygiene and packaging buy at scale and exert strong negotiating pressure on suppliers like Nippon Shokubai, compressing margins. High volume concentration among a handful of buyers grants them pricing leverage and contract terms. Multi-year supply agreements are commonly used to trade lower prices for security of supply. Deep technical service, formulation support and customization increase customer stickiness and raise switching costs.

Product commoditization in basics

Basic chemicals sold by Nippon Shokubai face high price transparency with industry benchmarks such as ICIS and Platts guiding spot and contract pricing in 2024, enabling buyers to switch suppliers on small price differentials. Buyers regularly leverage these indices to negotiate, increasing their bargaining power. Nippon Shokubai reduces price pressure through reliability, logistics performance and on‑time supply. Value‑added grades and specialty formulations segment demand and command premiums.

Qualification and dual-sourcing norms

End-markets increasingly mandate dual-qualified suppliers to reduce supply risk, enabling buyers to switch and exert leverage over Nippon Shokubai; by 2024 dual-sourcing became standard in key automotive and electronics supply chains. Co-development of performance specs with customers raises switching costs where formulations and process know-how are tailored. Strong QA, batch-to-batch consistency and on-time delivery sustain preferred-supplier status and limit buyer bargaining power.

ESG and regulatory pass-through

Cyclical demand and inventory cycles

Cyclical downcycles expand buyer power as customers destock and shift to spot purchases, pressuring Nippon Shokubai’s volumes and margins; upcycles reverse this, tightening supply and rebalancing bargaining. Flexible production planning mitigates margin erosion by shifting output and utilization, while dynamic pricing tied to feedstock indices stabilizes customer relationships and pass-through.

- Downcycles: increased buyer leverage via destocking/spot buys

- Upcycles: supply tightens, buyer power falls

- Defense: flexible production planning

- Pricing: dynamic, feedstock-index linked

OEM pricing power vs buyers: ESG procurement, long contracts and dual-sourcing trends

Large OEMs and converters exert strong price leverage; multi-year contracts are common while value-added grades and co-development raise switching costs. In 2024 ICIS and Platts guided pricing and Japan retains a net-zero by 2050 target, driving ESG procurement. Downcycle destocking increases buyer power; dual-sourcing became standard in key automotive/electronics chains.

| Metric | 2024 |

|---|---|

| Price benchmarks | ICIS, Platts |

| Policy | Japan net-zero 2050 |

| Trend | ESG procurement rise; dual-sourcing standard |

Preview the Actual Deliverable

Nippon Shokubai Porter's Five Forces Analysis

This preview shows the exact Nippon Shokubai Porter's Five Forces Analysis you'll receive upon purchase—no placeholders or samples. The file is fully formatted and ready for immediate download and use, containing the complete professional analysis as displayed here.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Nippon Shokubai faces moderate supplier power due to specialized feedstocks, intense rivalry from global chemical peers, and growing substitute risks from greener polymers, while scale and IP provide defensive advantages. This brief snapshot only scratches the surface—dive deeper to quantify force ratings and strategic levers. Unlock the full Porter's Five Forces Analysis to explore Nippon Shokubai’s competitive dynamics in detail.

Suppliers Bargaining Power

Petrochemical feedstock concentration

Core inputs like propylene, ethylene and caustic soda come from a concentrated supplier base—top 10 producers held roughly 60% of global propylene/ethylene capacity in 2024, boosting supplier leverage. Price volatility tied to naphtha/crude cycles produced swings up to ±30% in 2024, strengthening sellers. Long-term contracts and hedging have tempered shocks for Nippon Shokubai, while backward integration and multi-sourcing materially reduce exposure.

Specialty catalyst and additive dependence

Certain catalysts and additives are proprietary and sourced from few vendors, driving supplier power; process requalification for substitutes can take 3–12 months and create non-trivial switching costs. Joint development agreements with suppliers have reduced price volatility in comparable chemical segments by up to 10% in 2024. Inventory buffers of 2–8 weeks are commonly used to mitigate interruptions.

Logistics and energy constraints

Steam, power and industrial gases are often supplied by local monopolies, giving suppliers strong leverage over chemical producers; 2024 saw renewed energy price volatility that pressured margins across Japan's specialty-chemicals sector. Energy spikes feed directly into COGS, but onsite cogeneration and long-term PPAs have been adopted to blunt supplier power and stabilize unit costs. Geographic diversification of plants further spreads operational risk and exposure to localized utility constraints.

Quality and specification rigidity

High-purity specifications for acrylic acid and SAPs effectively restrict approved suppliers to a very small cohort, increasing supplier bargaining power as fewer vendors can meet purity and consistency demands.

Tighter specs raise switching costs and price leverage, though vendor qualification programs and multi-year audits have widened options for Nippon Shokubai over time.

Statistical quality agreements (SQA) and KPI-based contracts are increasingly used to enforce performance and mitigate supply risk.

- narrow approved supplier pools

- higher switching costs → greater supplier leverage

- vendor qualification programs expand sourcing

- SQA enforceable KPIs reduce operational risk

Sustainability and compliance requirements

Stricter ESG sourcing in 2024, reinforced by CBAM rollouts and buyer mandates, narrows low-carbon feedstock suppliers and strengthens supplier leverage; compliance premiums and certification costs raise input costs and can add margin pressure for Nippon Shokubai. Collaborative traceability projects reduce supply-risk and lessen bargaining asymmetry, while third-party certifications expand the pool of acceptable sustainable suppliers.

- ESG sourcing limits supplier pool

- Compliance premiums raise input costs

- Traceability reduces supplier power

- Certifications broaden sustainable suppliers

Supplier power high: top10 hold ~60%; firms hedge via integration

Supplier power is high: top‑10 propylene/ethylene producers held ~60% capacity in 2024 and feedstock price swings reached ±30%, while narrow approved supplier pools and energy monopolies raise switching costs; Nippon Shokubai offsets via backward integration, multi‑sourcing, long‑term contracts and onsite cogeneration.

| Metric | 2024 |

|---|---|

| Top‑10 capacity (propylene/ethylene) | ~60% |

| Feedstock price volatility | ±30% |

| Typical inventory buffer | 2–8 weeks |

What is included in the product

Tailored exclusively for Nippon Shokubai, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, barriers to entry, threat of substitutes, and identifies disruptive forces and strategic implications for pricing and profitability.

A concise, one-sheet Porter's Five Forces for Nippon Shokubai that clarifies supplier, buyer, rivalry, entrant and substitute pressures for rapid strategic decisions—customizable pressure levels and a ready-to-use spider chart make it easy to spot relief points and prioritize actions.

Customers Bargaining Power

Large OEMs and converters

Large OEMs and converters in automotive, hygiene and packaging buy at scale and exert strong negotiating pressure on suppliers like Nippon Shokubai, compressing margins. High volume concentration among a handful of buyers grants them pricing leverage and contract terms. Multi-year supply agreements are commonly used to trade lower prices for security of supply. Deep technical service, formulation support and customization increase customer stickiness and raise switching costs.

Product commoditization in basics

Basic chemicals sold by Nippon Shokubai face high price transparency with industry benchmarks such as ICIS and Platts guiding spot and contract pricing in 2024, enabling buyers to switch suppliers on small price differentials. Buyers regularly leverage these indices to negotiate, increasing their bargaining power. Nippon Shokubai reduces price pressure through reliability, logistics performance and on‑time supply. Value‑added grades and specialty formulations segment demand and command premiums.

Qualification and dual-sourcing norms

End-markets increasingly mandate dual-qualified suppliers to reduce supply risk, enabling buyers to switch and exert leverage over Nippon Shokubai; by 2024 dual-sourcing became standard in key automotive and electronics supply chains. Co-development of performance specs with customers raises switching costs where formulations and process know-how are tailored. Strong QA, batch-to-batch consistency and on-time delivery sustain preferred-supplier status and limit buyer bargaining power.

ESG and regulatory pass-through

Cyclical demand and inventory cycles

Cyclical downcycles expand buyer power as customers destock and shift to spot purchases, pressuring Nippon Shokubai’s volumes and margins; upcycles reverse this, tightening supply and rebalancing bargaining. Flexible production planning mitigates margin erosion by shifting output and utilization, while dynamic pricing tied to feedstock indices stabilizes customer relationships and pass-through.

- Downcycles: increased buyer leverage via destocking/spot buys

- Upcycles: supply tightens, buyer power falls

- Defense: flexible production planning

- Pricing: dynamic, feedstock-index linked

OEM pricing power vs buyers: ESG procurement, long contracts and dual-sourcing trends

Large OEMs and converters exert strong price leverage; multi-year contracts are common while value-added grades and co-development raise switching costs. In 2024 ICIS and Platts guided pricing and Japan retains a net-zero by 2050 target, driving ESG procurement. Downcycle destocking increases buyer power; dual-sourcing became standard in key automotive/electronics chains.

| Metric | 2024 |

|---|---|

| Price benchmarks | ICIS, Platts |

| Policy | Japan net-zero 2050 |

| Trend | ESG procurement rise; dual-sourcing standard |

Preview the Actual Deliverable

Nippon Shokubai Porter's Five Forces Analysis

This preview shows the exact Nippon Shokubai Porter's Five Forces Analysis you'll receive upon purchase—no placeholders or samples. The file is fully formatted and ready for immediate download and use, containing the complete professional analysis as displayed here.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Nippon Shokubai faces moderate supplier power due to specialized feedstocks, intense rivalry from global chemical peers, and growing substitute risks from greener polymers, while scale and IP provide defensive advantages. This brief snapshot only scratches the surface—dive deeper to quantify force ratings and strategic levers. Unlock the full Porter's Five Forces Analysis to explore Nippon Shokubai’s competitive dynamics in detail.

Suppliers Bargaining Power

Petrochemical feedstock concentration

Core inputs like propylene, ethylene and caustic soda come from a concentrated supplier base—top 10 producers held roughly 60% of global propylene/ethylene capacity in 2024, boosting supplier leverage. Price volatility tied to naphtha/crude cycles produced swings up to ±30% in 2024, strengthening sellers. Long-term contracts and hedging have tempered shocks for Nippon Shokubai, while backward integration and multi-sourcing materially reduce exposure.

Specialty catalyst and additive dependence

Certain catalysts and additives are proprietary and sourced from few vendors, driving supplier power; process requalification for substitutes can take 3–12 months and create non-trivial switching costs. Joint development agreements with suppliers have reduced price volatility in comparable chemical segments by up to 10% in 2024. Inventory buffers of 2–8 weeks are commonly used to mitigate interruptions.

Logistics and energy constraints

Steam, power and industrial gases are often supplied by local monopolies, giving suppliers strong leverage over chemical producers; 2024 saw renewed energy price volatility that pressured margins across Japan's specialty-chemicals sector. Energy spikes feed directly into COGS, but onsite cogeneration and long-term PPAs have been adopted to blunt supplier power and stabilize unit costs. Geographic diversification of plants further spreads operational risk and exposure to localized utility constraints.

Quality and specification rigidity

High-purity specifications for acrylic acid and SAPs effectively restrict approved suppliers to a very small cohort, increasing supplier bargaining power as fewer vendors can meet purity and consistency demands.

Tighter specs raise switching costs and price leverage, though vendor qualification programs and multi-year audits have widened options for Nippon Shokubai over time.

Statistical quality agreements (SQA) and KPI-based contracts are increasingly used to enforce performance and mitigate supply risk.

- narrow approved supplier pools

- higher switching costs → greater supplier leverage

- vendor qualification programs expand sourcing

- SQA enforceable KPIs reduce operational risk

Sustainability and compliance requirements

Stricter ESG sourcing in 2024, reinforced by CBAM rollouts and buyer mandates, narrows low-carbon feedstock suppliers and strengthens supplier leverage; compliance premiums and certification costs raise input costs and can add margin pressure for Nippon Shokubai. Collaborative traceability projects reduce supply-risk and lessen bargaining asymmetry, while third-party certifications expand the pool of acceptable sustainable suppliers.

- ESG sourcing limits supplier pool

- Compliance premiums raise input costs

- Traceability reduces supplier power

- Certifications broaden sustainable suppliers

Supplier power high: top10 hold ~60%; firms hedge via integration

Supplier power is high: top‑10 propylene/ethylene producers held ~60% capacity in 2024 and feedstock price swings reached ±30%, while narrow approved supplier pools and energy monopolies raise switching costs; Nippon Shokubai offsets via backward integration, multi‑sourcing, long‑term contracts and onsite cogeneration.

| Metric | 2024 |

|---|---|

| Top‑10 capacity (propylene/ethylene) | ~60% |

| Feedstock price volatility | ±30% |

| Typical inventory buffer | 2–8 weeks |

What is included in the product

Tailored exclusively for Nippon Shokubai, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, barriers to entry, threat of substitutes, and identifies disruptive forces and strategic implications for pricing and profitability.

A concise, one-sheet Porter's Five Forces for Nippon Shokubai that clarifies supplier, buyer, rivalry, entrant and substitute pressures for rapid strategic decisions—customizable pressure levels and a ready-to-use spider chart make it easy to spot relief points and prioritize actions.

Customers Bargaining Power

Large OEMs and converters

Large OEMs and converters in automotive, hygiene and packaging buy at scale and exert strong negotiating pressure on suppliers like Nippon Shokubai, compressing margins. High volume concentration among a handful of buyers grants them pricing leverage and contract terms. Multi-year supply agreements are commonly used to trade lower prices for security of supply. Deep technical service, formulation support and customization increase customer stickiness and raise switching costs.

Product commoditization in basics

Basic chemicals sold by Nippon Shokubai face high price transparency with industry benchmarks such as ICIS and Platts guiding spot and contract pricing in 2024, enabling buyers to switch suppliers on small price differentials. Buyers regularly leverage these indices to negotiate, increasing their bargaining power. Nippon Shokubai reduces price pressure through reliability, logistics performance and on‑time supply. Value‑added grades and specialty formulations segment demand and command premiums.

Qualification and dual-sourcing norms

End-markets increasingly mandate dual-qualified suppliers to reduce supply risk, enabling buyers to switch and exert leverage over Nippon Shokubai; by 2024 dual-sourcing became standard in key automotive and electronics supply chains. Co-development of performance specs with customers raises switching costs where formulations and process know-how are tailored. Strong QA, batch-to-batch consistency and on-time delivery sustain preferred-supplier status and limit buyer bargaining power.

ESG and regulatory pass-through

Cyclical demand and inventory cycles

Cyclical downcycles expand buyer power as customers destock and shift to spot purchases, pressuring Nippon Shokubai’s volumes and margins; upcycles reverse this, tightening supply and rebalancing bargaining. Flexible production planning mitigates margin erosion by shifting output and utilization, while dynamic pricing tied to feedstock indices stabilizes customer relationships and pass-through.

- Downcycles: increased buyer leverage via destocking/spot buys

- Upcycles: supply tightens, buyer power falls

- Defense: flexible production planning

- Pricing: dynamic, feedstock-index linked

OEM pricing power vs buyers: ESG procurement, long contracts and dual-sourcing trends

Large OEMs and converters exert strong price leverage; multi-year contracts are common while value-added grades and co-development raise switching costs. In 2024 ICIS and Platts guided pricing and Japan retains a net-zero by 2050 target, driving ESG procurement. Downcycle destocking increases buyer power; dual-sourcing became standard in key automotive/electronics chains.

| Metric | 2024 |

|---|---|

| Price benchmarks | ICIS, Platts |

| Policy | Japan net-zero 2050 |

| Trend | ESG procurement rise; dual-sourcing standard |

Preview the Actual Deliverable

Nippon Shokubai Porter's Five Forces Analysis

This preview shows the exact Nippon Shokubai Porter's Five Forces Analysis you'll receive upon purchase—no placeholders or samples. The file is fully formatted and ready for immediate download and use, containing the complete professional analysis as displayed here.