SIA Engineering SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

SIA Engineering’s SWOT highlights resilient MRO capabilities, strategic airline partnerships, and exposure to cyclical travel demand, alongside margin pressure from competition and capital intensity. Our full SWOT unpacks competitive moats, regulatory risks, and growth levers with financial context and strategic recommendations. Purchase the complete report for a ready-to-use Word and Excel package to inform investment or strategic decisions.

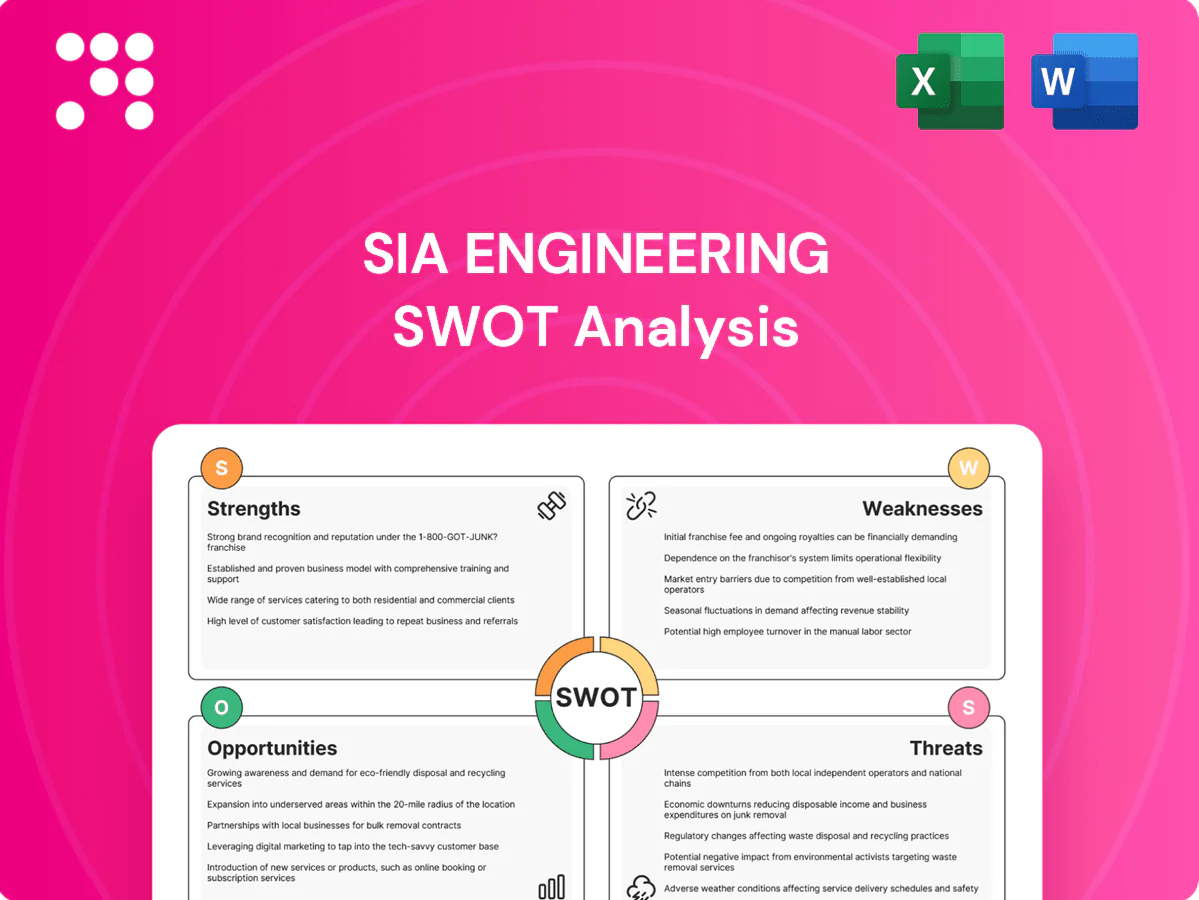

Strengths

End-to-end MRO suite

SIA Engineering offers true end-to-end MRO—line, airframe, engine, component MRO plus engineering and fleet management—providing one-stop solutions that cut turnaround and integration risk for airlines. Certified by major regulators including EASA, FAA, CAAC and CAAS, SIAEC (established 1992) leverages bundled service packages to deepen customer wallet share and improve retention.

Strategic Changi hub

Operating from Changi—with four terminals, three runways and links to over 100 airlines serving about 380 cities—gives SIA Engineering unrivalled Asia‑Pacific connectivity and reliability. Efficient cargo and ramp logistics and local aircraft availability shorten maintenance cycles, supporting on‑time delivery. Singapore’s stable regulatory regime and top‑ranked talent pool (GTCI leader) underpin premium service quality.

Deep OEM and airline ties

With over 30 years of partnerships and joint ventures with OEMs and major carriers, SIA Engineering secures technology transfer and a steady workload stream. The company aligns closely with new platforms and repair methodologies through collaborative OEM programs and JV engineering cells. Embedded ties to the SIA Group provide an anchor customer base while the firm’s OEM-backed credibility attracts third-party airlines seeking certified support.

Quality, safety, and approvals

SIA Engineering maintains a strong safety culture and certified quality systems with airworthiness approvals from CAAS, FAA and EASA, enabling cross-border work and complex C- and D-checks across operator fleets. Low rework rates and consistent turn-around times reinforce reliability for premium carriers, making its reputation a key differentiator in higher-yield segments.

- Approvals: CAAS, FAA, EASA

- Strength: low rework, reliable TAT

- Competitive edge: premium-segment reputation

Asia-Pacific market position

SIA Engineering’s strong brand across Asia‑Pacific positions it to benefit from the region’s rapid post‑pandemic fleet and traffic recovery and from OEM backlogs driving demand for maintenance on new‑generation A320neo/A220 and 787/787‑class aircraft; deep experience on these types underpins a sustained service pipeline and selective pricing power in niche heavy‑maintenance and component services.

- Regional brand strength

- New‑gen aircraft expertise

- Sustained MRO pipeline

- Selective pricing power

Changi MRO hub with OEM JVs and CAAS/FAA/EASA-certified A320neo/A220/787 expertise

SIA Engineering delivers end-to-end MRO (line, airframe, engine, component) with strong OEM JVs and SIA Group anchoring, certified by CAAS, FAA and EASA, yielding low rework and reliable TAT. Based at Changi (100+ airlines, ~380 cities) it leverages regional connectivity and deep expertise on A320neo/A220/787 to sustain a premium service pipeline.

| Metric | Value |

|---|---|

| Established | 1992 |

| Approvals | CAAS, FAA, EASA |

| Changi network | 100+ airlines / ~380 cities |

| Core services | Line/airframe/engine/component MRO |

| Key types | A320neo, A220, 787 |

What is included in the product

Provides a concise strategic overview of SIA Engineering’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, operational capabilities, growth drivers, and market risks to inform strategic decisions.

Provides a concise, industry-tailored SWOT matrix for SIA Engineering to quickly align MRO strategy, cost controls and resource allocation; editable format enables rapid updates as fleet mix, regulatory or client priorities change.

Weaknesses

Cyclicality exposure

SIA Engineering's revenue is highly dependent on airline flight hours and scheduled checks that are often deferred during downturns; global RPK fell about 66% in 2020 (IATA), illustrating how sharply demand can collapse. Revenue volatility during shocks such as pandemics or recessions is significant, with limited ability to pass fixed costs through instantly. Cash flows are highly sensitive to the pace of traffic recovery.

High-cost home base

As of 2024 Singapore labor and facility costs are roughly 2–3× higher than regional hubs such as Malaysia and Indonesia, raising SIAEC’s unit costs; elevated staff and hangar expenses squeeze margins on labor‑intensive heavy maintenance. This margin pressure makes price‑sensitive work susceptible to offshoring, risking mix and volume declines. Greater productivity and digital automation investments are required to close the cost gap.

Customer concentration

SIA Engineering shows material client concentration, with the SIA Group and a handful of large carriers accounting for c.60% of revenue, exposing the firm to bargaining power and volume risk if key customers insource or rebid major contracts. A concentrated revenue mix limits pricing flexibility and margin diversification. Continued expansion across geographies and platforms is recommended to dilute customer risk.

Capital and talent intensity

Capital and talent intensity: SIA Engineering faces heavy upfront capex for tooling, hangars and certifications and ongoing certified-training costs; experienced licensed engineers are scarce regionally, slowing ramp-up when new fleets or engines (e.g., LEAP, GTF) are introduced, creating utilization risk if demand lags investment.

- High capex for infrastructure and certifications

- Ongoing training and licensing costs

- Shortage of experienced licensed engineers

- Ramp-up challenges with new fleets/engines

- Utilization risk if demand trails investment

Limited aftermarket IP

Limited aftermarket IP leaves SIA Engineering constrained where OEMs control technical manuals, repair approvals and parts pricing, capping margins on certain engines and components via licensing and approved-scheme exclusivity. Dependence on OEM-approved repair schemes reduces scope for internal innovation and creates a weak negotiating position within PBH ecosystems where OEMs set terms.

- OEM control of manuals and parts

- Licensing caps margins

- Reliance on approved repair schemes

- Weak bargaining in PBH contracts

MRO margins at risk: 2–3× cost gap, 60% client concentration, −66% demand drop

SIA Engineering faces revenue volatility tied to flight hours—global RPK fell ~66% in 2020 (IATA)—making cash flows sensitive to demand shocks. Singapore labor and hangar costs run ~2–3× regional peers, pressuring margins and exposing work to offshoring. c.60% revenue concentration with SIA Group and few carriers raises client‑power and rebid risk. High capex, scarce licensed engineers and OEM control of IP limit margin and scaling flexibility.

| Metric | Value |

|---|---|

| Revenue concentration | c.60% SIA Group |

| Labor/facility cost | ~2–3× regional peers (2024) |

| Demand shock | RPK −66% (2020, IATA) |

| Key risks | High capex, talent shortage, OEM IP control |

Preview Before You Purchase

SIA Engineering SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, showing key strengths, weaknesses, opportunities and threats. Purchase unlocks the complete, editable and fully detailed version ready for download.

Elevate Your Analysis with the Complete SWOT Report

SIA Engineering’s SWOT highlights resilient MRO capabilities, strategic airline partnerships, and exposure to cyclical travel demand, alongside margin pressure from competition and capital intensity. Our full SWOT unpacks competitive moats, regulatory risks, and growth levers with financial context and strategic recommendations. Purchase the complete report for a ready-to-use Word and Excel package to inform investment or strategic decisions.

Strengths

End-to-end MRO suite

SIA Engineering offers true end-to-end MRO—line, airframe, engine, component MRO plus engineering and fleet management—providing one-stop solutions that cut turnaround and integration risk for airlines. Certified by major regulators including EASA, FAA, CAAC and CAAS, SIAEC (established 1992) leverages bundled service packages to deepen customer wallet share and improve retention.

Strategic Changi hub

Operating from Changi—with four terminals, three runways and links to over 100 airlines serving about 380 cities—gives SIA Engineering unrivalled Asia‑Pacific connectivity and reliability. Efficient cargo and ramp logistics and local aircraft availability shorten maintenance cycles, supporting on‑time delivery. Singapore’s stable regulatory regime and top‑ranked talent pool (GTCI leader) underpin premium service quality.

Deep OEM and airline ties

With over 30 years of partnerships and joint ventures with OEMs and major carriers, SIA Engineering secures technology transfer and a steady workload stream. The company aligns closely with new platforms and repair methodologies through collaborative OEM programs and JV engineering cells. Embedded ties to the SIA Group provide an anchor customer base while the firm’s OEM-backed credibility attracts third-party airlines seeking certified support.

Quality, safety, and approvals

SIA Engineering maintains a strong safety culture and certified quality systems with airworthiness approvals from CAAS, FAA and EASA, enabling cross-border work and complex C- and D-checks across operator fleets. Low rework rates and consistent turn-around times reinforce reliability for premium carriers, making its reputation a key differentiator in higher-yield segments.

- Approvals: CAAS, FAA, EASA

- Strength: low rework, reliable TAT

- Competitive edge: premium-segment reputation

Asia-Pacific market position

SIA Engineering’s strong brand across Asia‑Pacific positions it to benefit from the region’s rapid post‑pandemic fleet and traffic recovery and from OEM backlogs driving demand for maintenance on new‑generation A320neo/A220 and 787/787‑class aircraft; deep experience on these types underpins a sustained service pipeline and selective pricing power in niche heavy‑maintenance and component services.

- Regional brand strength

- New‑gen aircraft expertise

- Sustained MRO pipeline

- Selective pricing power

Changi MRO hub with OEM JVs and CAAS/FAA/EASA-certified A320neo/A220/787 expertise

SIA Engineering delivers end-to-end MRO (line, airframe, engine, component) with strong OEM JVs and SIA Group anchoring, certified by CAAS, FAA and EASA, yielding low rework and reliable TAT. Based at Changi (100+ airlines, ~380 cities) it leverages regional connectivity and deep expertise on A320neo/A220/787 to sustain a premium service pipeline.

| Metric | Value |

|---|---|

| Established | 1992 |

| Approvals | CAAS, FAA, EASA |

| Changi network | 100+ airlines / ~380 cities |

| Core services | Line/airframe/engine/component MRO |

| Key types | A320neo, A220, 787 |

What is included in the product

Provides a concise strategic overview of SIA Engineering’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, operational capabilities, growth drivers, and market risks to inform strategic decisions.

Provides a concise, industry-tailored SWOT matrix for SIA Engineering to quickly align MRO strategy, cost controls and resource allocation; editable format enables rapid updates as fleet mix, regulatory or client priorities change.

Weaknesses

Cyclicality exposure

SIA Engineering's revenue is highly dependent on airline flight hours and scheduled checks that are often deferred during downturns; global RPK fell about 66% in 2020 (IATA), illustrating how sharply demand can collapse. Revenue volatility during shocks such as pandemics or recessions is significant, with limited ability to pass fixed costs through instantly. Cash flows are highly sensitive to the pace of traffic recovery.

High-cost home base

As of 2024 Singapore labor and facility costs are roughly 2–3× higher than regional hubs such as Malaysia and Indonesia, raising SIAEC’s unit costs; elevated staff and hangar expenses squeeze margins on labor‑intensive heavy maintenance. This margin pressure makes price‑sensitive work susceptible to offshoring, risking mix and volume declines. Greater productivity and digital automation investments are required to close the cost gap.

Customer concentration

SIA Engineering shows material client concentration, with the SIA Group and a handful of large carriers accounting for c.60% of revenue, exposing the firm to bargaining power and volume risk if key customers insource or rebid major contracts. A concentrated revenue mix limits pricing flexibility and margin diversification. Continued expansion across geographies and platforms is recommended to dilute customer risk.

Capital and talent intensity

Capital and talent intensity: SIA Engineering faces heavy upfront capex for tooling, hangars and certifications and ongoing certified-training costs; experienced licensed engineers are scarce regionally, slowing ramp-up when new fleets or engines (e.g., LEAP, GTF) are introduced, creating utilization risk if demand lags investment.

- High capex for infrastructure and certifications

- Ongoing training and licensing costs

- Shortage of experienced licensed engineers

- Ramp-up challenges with new fleets/engines

- Utilization risk if demand trails investment

Limited aftermarket IP

Limited aftermarket IP leaves SIA Engineering constrained where OEMs control technical manuals, repair approvals and parts pricing, capping margins on certain engines and components via licensing and approved-scheme exclusivity. Dependence on OEM-approved repair schemes reduces scope for internal innovation and creates a weak negotiating position within PBH ecosystems where OEMs set terms.

- OEM control of manuals and parts

- Licensing caps margins

- Reliance on approved repair schemes

- Weak bargaining in PBH contracts

MRO margins at risk: 2–3× cost gap, 60% client concentration, −66% demand drop

SIA Engineering faces revenue volatility tied to flight hours—global RPK fell ~66% in 2020 (IATA)—making cash flows sensitive to demand shocks. Singapore labor and hangar costs run ~2–3× regional peers, pressuring margins and exposing work to offshoring. c.60% revenue concentration with SIA Group and few carriers raises client‑power and rebid risk. High capex, scarce licensed engineers and OEM control of IP limit margin and scaling flexibility.

| Metric | Value |

|---|---|

| Revenue concentration | c.60% SIA Group |

| Labor/facility cost | ~2–3× regional peers (2024) |

| Demand shock | RPK −66% (2020, IATA) |

| Key risks | High capex, talent shortage, OEM IP control |

Preview Before You Purchase

SIA Engineering SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, showing key strengths, weaknesses, opportunities and threats. Purchase unlocks the complete, editable and fully detailed version ready for download.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

SIA Engineering’s SWOT highlights resilient MRO capabilities, strategic airline partnerships, and exposure to cyclical travel demand, alongside margin pressure from competition and capital intensity. Our full SWOT unpacks competitive moats, regulatory risks, and growth levers with financial context and strategic recommendations. Purchase the complete report for a ready-to-use Word and Excel package to inform investment or strategic decisions.

Strengths

End-to-end MRO suite

SIA Engineering offers true end-to-end MRO—line, airframe, engine, component MRO plus engineering and fleet management—providing one-stop solutions that cut turnaround and integration risk for airlines. Certified by major regulators including EASA, FAA, CAAC and CAAS, SIAEC (established 1992) leverages bundled service packages to deepen customer wallet share and improve retention.

Strategic Changi hub

Operating from Changi—with four terminals, three runways and links to over 100 airlines serving about 380 cities—gives SIA Engineering unrivalled Asia‑Pacific connectivity and reliability. Efficient cargo and ramp logistics and local aircraft availability shorten maintenance cycles, supporting on‑time delivery. Singapore’s stable regulatory regime and top‑ranked talent pool (GTCI leader) underpin premium service quality.

Deep OEM and airline ties

With over 30 years of partnerships and joint ventures with OEMs and major carriers, SIA Engineering secures technology transfer and a steady workload stream. The company aligns closely with new platforms and repair methodologies through collaborative OEM programs and JV engineering cells. Embedded ties to the SIA Group provide an anchor customer base while the firm’s OEM-backed credibility attracts third-party airlines seeking certified support.

Quality, safety, and approvals

SIA Engineering maintains a strong safety culture and certified quality systems with airworthiness approvals from CAAS, FAA and EASA, enabling cross-border work and complex C- and D-checks across operator fleets. Low rework rates and consistent turn-around times reinforce reliability for premium carriers, making its reputation a key differentiator in higher-yield segments.

- Approvals: CAAS, FAA, EASA

- Strength: low rework, reliable TAT

- Competitive edge: premium-segment reputation

Asia-Pacific market position

SIA Engineering’s strong brand across Asia‑Pacific positions it to benefit from the region’s rapid post‑pandemic fleet and traffic recovery and from OEM backlogs driving demand for maintenance on new‑generation A320neo/A220 and 787/787‑class aircraft; deep experience on these types underpins a sustained service pipeline and selective pricing power in niche heavy‑maintenance and component services.

- Regional brand strength

- New‑gen aircraft expertise

- Sustained MRO pipeline

- Selective pricing power

Changi MRO hub with OEM JVs and CAAS/FAA/EASA-certified A320neo/A220/787 expertise

SIA Engineering delivers end-to-end MRO (line, airframe, engine, component) with strong OEM JVs and SIA Group anchoring, certified by CAAS, FAA and EASA, yielding low rework and reliable TAT. Based at Changi (100+ airlines, ~380 cities) it leverages regional connectivity and deep expertise on A320neo/A220/787 to sustain a premium service pipeline.

| Metric | Value |

|---|---|

| Established | 1992 |

| Approvals | CAAS, FAA, EASA |

| Changi network | 100+ airlines / ~380 cities |

| Core services | Line/airframe/engine/component MRO |

| Key types | A320neo, A220, 787 |

What is included in the product

Provides a concise strategic overview of SIA Engineering’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, operational capabilities, growth drivers, and market risks to inform strategic decisions.

Provides a concise, industry-tailored SWOT matrix for SIA Engineering to quickly align MRO strategy, cost controls and resource allocation; editable format enables rapid updates as fleet mix, regulatory or client priorities change.

Weaknesses

Cyclicality exposure

SIA Engineering's revenue is highly dependent on airline flight hours and scheduled checks that are often deferred during downturns; global RPK fell about 66% in 2020 (IATA), illustrating how sharply demand can collapse. Revenue volatility during shocks such as pandemics or recessions is significant, with limited ability to pass fixed costs through instantly. Cash flows are highly sensitive to the pace of traffic recovery.

High-cost home base

As of 2024 Singapore labor and facility costs are roughly 2–3× higher than regional hubs such as Malaysia and Indonesia, raising SIAEC’s unit costs; elevated staff and hangar expenses squeeze margins on labor‑intensive heavy maintenance. This margin pressure makes price‑sensitive work susceptible to offshoring, risking mix and volume declines. Greater productivity and digital automation investments are required to close the cost gap.

Customer concentration

SIA Engineering shows material client concentration, with the SIA Group and a handful of large carriers accounting for c.60% of revenue, exposing the firm to bargaining power and volume risk if key customers insource or rebid major contracts. A concentrated revenue mix limits pricing flexibility and margin diversification. Continued expansion across geographies and platforms is recommended to dilute customer risk.

Capital and talent intensity

Capital and talent intensity: SIA Engineering faces heavy upfront capex for tooling, hangars and certifications and ongoing certified-training costs; experienced licensed engineers are scarce regionally, slowing ramp-up when new fleets or engines (e.g., LEAP, GTF) are introduced, creating utilization risk if demand lags investment.

- High capex for infrastructure and certifications

- Ongoing training and licensing costs

- Shortage of experienced licensed engineers

- Ramp-up challenges with new fleets/engines

- Utilization risk if demand trails investment

Limited aftermarket IP

Limited aftermarket IP leaves SIA Engineering constrained where OEMs control technical manuals, repair approvals and parts pricing, capping margins on certain engines and components via licensing and approved-scheme exclusivity. Dependence on OEM-approved repair schemes reduces scope for internal innovation and creates a weak negotiating position within PBH ecosystems where OEMs set terms.

- OEM control of manuals and parts

- Licensing caps margins

- Reliance on approved repair schemes

- Weak bargaining in PBH contracts

MRO margins at risk: 2–3× cost gap, 60% client concentration, −66% demand drop

SIA Engineering faces revenue volatility tied to flight hours—global RPK fell ~66% in 2020 (IATA)—making cash flows sensitive to demand shocks. Singapore labor and hangar costs run ~2–3× regional peers, pressuring margins and exposing work to offshoring. c.60% revenue concentration with SIA Group and few carriers raises client‑power and rebid risk. High capex, scarce licensed engineers and OEM control of IP limit margin and scaling flexibility.

| Metric | Value |

|---|---|

| Revenue concentration | c.60% SIA Group |

| Labor/facility cost | ~2–3× regional peers (2024) |

| Demand shock | RPK −66% (2020, IATA) |

| Key risks | High capex, talent shortage, OEM IP control |

Preview Before You Purchase

SIA Engineering SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, showing key strengths, weaknesses, opportunities and threats. Purchase unlocks the complete, editable and fully detailed version ready for download.